Decoding Your Drive: What’s the Average Cost of a Car Loan Per Month and How to Master It

Decoding Your Drive: What’s the Average Cost of a Car Loan Per Month and How to Master It Carloan.Guidemechanic.com

The rumble of a new engine, the gleam of fresh paint, the promise of open roads – owning a car is a significant milestone for many. But before you can hit the highway, there’s a crucial financial reality to navigate: the monthly car loan payment. For countless aspiring car owners, the burning question isn’t just "How much does the car cost?" but "What’s the average cost of a car loan per month?"

As an expert in automotive finance and a seasoned blogger, I can tell you there’s no single, simple answer. The "average" is a dynamic figure, influenced by a multitude of factors that can swing your payment by hundreds of dollars. This comprehensive guide will peel back the layers, demystifying the monthly car loan payment, exploring the variables that shape it, and empowering you with strategies to secure the best deal possible. Our ultimate goal is to help you drive away with confidence, knowing you’ve made a smart financial decision.

Decoding Your Drive: What’s the Average Cost of a Car Loan Per Month and How to Master It

The Elusive "Average": Why a Single Number Doesn’t Tell the Whole Story

When you search for the average cost of a car loan per month, you might find figures ranging from $400 to $700 or even more, depending on the source and the year. These numbers are often aggregates that blend a vast array of scenarios, from luxury SUVs to economical sedans, excellent credit scores to challenging ones.

Based on my experience, relying solely on a national average can be misleading. Your personal circumstances – your credit history, the type of car you choose, and even the current economic climate – will ultimately dictate your specific monthly outlay. Instead of chasing a phantom average, it’s far more valuable to understand the components that build that average and how they apply to your situation. This foundational knowledge is key to making informed decisions and securing a favorable auto loan.

Key Factors Influencing Your Monthly Car Loan Payment

To truly understand your potential monthly car payment, we need to dissect the elements that lenders consider. Each of these plays a critical role in shaping the final figure you’ll see on your loan agreement.

1. The Vehicle’s Purchase Price

The most obvious factor is the price of the car itself. Whether you’re eyeing a brand-new model straight from the dealership or a pre-owned gem, the total amount you finance directly impacts your monthly obligation.

A higher vehicle price naturally leads to a larger loan principal, and consequently, a higher monthly payment. New cars typically command higher prices, but also often come with better interest rates due to their lower risk profile for lenders. Used cars are generally more affordable upfront, but their interest rates can sometimes be slightly higher depending on age and mileage. Pro tips from us: Always negotiate the sale price. Even a seemingly small reduction of a few hundred dollars can shave a noticeable amount off your monthly payment over the life of the loan. Remember to factor in sales tax, registration fees, and any dealership add-ons, as these also inflate the total amount you’re financing.

2. Your Down Payment

A down payment is the initial amount of cash you pay upfront when purchasing a car, reducing the total amount you need to borrow. This is one of the most powerful levers you have to lower your average cost of a car loan per month.

A substantial down payment shrinks the principal balance of your loan, directly translating into lower monthly payments. It also reduces the amount of interest you’ll pay over the loan term. Furthermore, a larger down payment signals financial stability to lenders, potentially qualifying you for a lower interest rate. Common mistakes to avoid are putting down too little or no down payment at all, which can lead to negative equity (owing more than the car is worth) early in the loan term. As an expert, I often recommend aiming for at least 20% down on a new car and 10% on a used car, if financially feasible. This not only makes your monthly payments more manageable but also protects you from depreciation.

3. The Loan Term (Duration)

The loan term, or duration, refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a significant impact on both your monthly payment and the total interest you’ll pay.

A longer loan term (e.g., 72 or 84 months) will result in a lower monthly payment because the principal is spread out over more installments. However, this convenience comes at a cost: you’ll pay significantly more in total interest over the life of the loan. Conversely, a shorter loan term (e.g., 36 or 48 months) means higher monthly payments but substantially less total interest paid. Based on my experience, many buyers gravitate towards longer terms to achieve a more "affordable" monthly payment, often overlooking the thousands of extra dollars they’ll pay in interest. Pro tips from us: Strive for the shortest loan term you can comfortably afford. This balance between monthly affordability and total cost is crucial for smart financial planning.

4. Your Interest Rate (APR – Annual Percentage Rate)

The interest rate, often expressed as an Annual Percentage Rate (APR), is essentially the cost of borrowing money. It’s a percentage of the principal that lenders charge you for the privilege of using their funds. This single factor can dramatically alter your average cost of a car loan per month.

Several elements converge to determine the APR you’re offered:

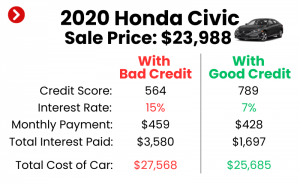

- Your Credit Score: This is arguably the most influential factor. Lenders use your credit score to assess your creditworthiness and the risk you pose. Borrowers with excellent credit scores (750+) typically qualify for the lowest interest rates, sometimes even 0% APR offers. Those with good (680-749), fair (620-679), or poor (below 620) credit will face progressively higher rates to compensate lenders for the increased risk. A difference of just a few percentage points in APR can mean tens or even hundreds of dollars added to your monthly payment.

- The Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s money is tied up for a shorter period.

- Lender Type: Different lenders (banks, credit unions, online lenders, dealership financing) have varying rate structures and eligibility requirements. Shopping around is paramount.

- Market Conditions: Broader economic factors, such as the Federal Reserve’s interest rate decisions, can influence the baseline rates offered by lenders.

- Vehicle Type and Age: Lenders may view older or higher-mileage vehicles as riskier collateral, potentially leading to slightly higher rates.

Pro tips from us: Improving your credit score before applying for a loan is one of the most effective ways to reduce your interest rate. Get pre-approved by multiple lenders before you visit the dealership to compare offers and gain negotiating leverage.

5. Trade-In Value

If you’re trading in your current vehicle, its value can significantly offset the cost of your new purchase, effectively acting as an additional down payment.

The higher the trade-in value, the less you’ll need to finance, leading to a lower monthly car payment. Researching your car’s market value using reputable sources like Kelley Blue Book (KBB) or Edmunds is crucial before heading to the dealership. Common mistakes to avoid are accepting the first trade-in offer without negotiation or without knowing your car’s true worth. Based on my experience, it’s often beneficial to negotiate the trade-in value separately from the price of the new car. Sometimes, selling your old car privately can yield a higher return than a trade-in, giving you more cash for a down payment.

6. Additional Costs Rolled into the Loan

Dealerships often present optional products and services that can be rolled into your car loan, increasing the total amount you borrow. These include:

- Extended Warranties/Service Contracts: These offer coverage beyond the manufacturer’s standard warranty. While they can provide peace of mind, ensure you understand what’s covered, for how long, and if the cost is justified.

- GAP Insurance: Guaranteed Asset Protection (GAP) insurance covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. It’s particularly useful if you make a small down payment or have a long loan term, as depreciation can quickly make your car worth less than you owe.

- Tire and Wheel Protection, Paint Protection, etc.: These are typically add-ons with varying degrees of value.

Rolling these items into your loan increases your principal, meaning you’ll pay interest on them for the entire loan term, raising your average cost of a car loan per month. Pro tips from us: Carefully evaluate each add-on. Ask yourself if it’s truly necessary and if you could purchase it more affordably elsewhere. Don’t be pressured into accepting them without full understanding.

How to Calculate Your Monthly Car Loan Payment (The Basics)

While complex formulas exist, most people rely on online car loan calculators to estimate their monthly car payment. These tools typically require three key pieces of information:

- Loan Amount (Principal): The vehicle’s price minus your down payment and any trade-in value.

- Interest Rate (APR): The percentage rate the lender will charge.

- Loan Term: The number of months you’ll be repaying the loan.

By inputting these figures, the calculator quickly provides an estimated monthly payment. It’s an invaluable tool for budgeting and comparing different loan scenarios. For a more detailed breakdown of how these calculators work and what each input means, check out our guide on "Understanding Car Loan Calculators."

Strategies to Lower Your Average Monthly Car Loan Payment

Now that you understand the factors, let’s explore actionable strategies to reduce your monthly car loan payment and make your car ownership dream more affordable.

- Boost Your Credit Score: This is perhaps the most impactful long-term strategy. Pay all your bills on time, reduce existing debt, and avoid opening new credit lines before applying for a car loan. A higher credit score directly translates to a lower interest rate, significantly decreasing your monthly payment.

- Increase Your Down Payment: The more cash you put down upfront, the less you borrow. Save aggressively, sell your old car privately for a better return, or even consider delaying your purchase to accumulate a larger down payment.

- Choose a Less Expensive Vehicle: This might seem obvious, but it’s often overlooked in the excitement of car shopping. Be realistic about what you need versus what you want. A slightly less expensive model or trim level can make a substantial difference in your monthly payment.

- Shop Around for Lenders: Don’t just accept the first offer, especially from the dealership. Get pre-approved by several banks, credit unions, and online lenders. Compare their interest rates, terms, and fees. This competition can save you a significant amount.

- Negotiate the Car Price: Never pay the sticker price. Dealers expect negotiation. Do your research on fair market value for the specific vehicle you’re interested in and be prepared to haggle.

- Strategically Adjust Your Loan Term: If monthly affordability is your absolute priority, a slightly longer loan term will reduce your monthly payment. However, remember the trade-off: you’ll pay more in total interest. Aim for the shortest term you can comfortably manage to save money in the long run.

- Decline Unnecessary Add-ons: Be firm about declining extended warranties, paint protection, and other extras if you don’t truly need or want them, or if you can find them cheaper elsewhere. These can inflate your loan principal.

- Refinance Your Car Loan: If your credit score has improved since you first financed your car, or if market interest rates have dropped, you might be able to refinance your existing loan for a lower APR. Based on my experience, refinancing can be a game-changer for many car owners, potentially saving them hundreds or thousands over the life of the loan.

The Hidden Costs of Car Ownership (Beyond the Monthly Payment)

While focusing on the average cost of a car loan per month is essential, it’s crucial to remember that it’s only one piece of the car ownership puzzle. There are other significant ongoing expenses that must be factored into your overall budget. Pro tips from us: Always budget for these additional expenses; they can easily add hundreds to your monthly outlay.

- Car Insurance: This is a non-negotiable cost. Rates vary wildly based on your age, driving record, vehicle type, location, and coverage choices. Get insurance quotes before you buy a car.

- Fuel: With fluctuating gas prices, fuel costs can be a substantial monthly expense, especially for daily commuters or those driving less fuel-efficient vehicles.

- Maintenance and Repairs: Cars need oil changes, tire rotations, brake pads, and sometimes unexpected repairs. Budget for regular maintenance to prolong your vehicle’s life and prevent costly breakdowns.

- Registration, Taxes, and Fees: Annual registration renewals, property taxes (in some states), and inspection fees are recurring costs.

- Depreciation: While not a direct monthly payment, depreciation is the silent killer of your car’s value. It’s the loss in value over time and is the largest cost of car ownership for many. Understanding it helps you make smarter buying decisions.

Setting a Realistic Budget for Your Car Loan

To ensure your car loan is truly affordable, it’s vital to integrate it into your broader financial picture. A common guideline is the 20/4/10 Rule:

- 20% Down Payment: Aim for at least 20% of the car’s purchase price as a down payment.

- 4-Year Loan Term: Keep your loan term to four years (48 months) or less to minimize total interest paid.

- 10% of Gross Income: Your total monthly car expenses (loan payment, insurance, and fuel) should not exceed 10% of your gross (pre-tax) monthly income.

This rule provides a solid framework, but your personal circumstances may vary. Conduct a thorough review of your income, fixed expenses, and discretionary spending. Common mistakes to avoid are focusing solely on the monthly payment without considering the bigger picture of your overall financial health. A car should enhance your life, not become a financial burden. For more savvy financial moves related to car ownership, check out our article, "Smart Strategies for Car Ownership."

Conclusion: Drive Smart, Not Just Stylish

The journey to understanding the average cost of a car loan per month is complex, yet incredibly rewarding. As we’ve explored, there’s no universal average, but rather a dynamic figure shaped by your choices, your financial health, and the market. By grasping the key factors – vehicle price, down payment, loan term, and especially your interest rate driven by your credit score – you gain the power to influence your monthly outlay significantly.

Empower yourself with knowledge, shop around for the best rates, negotiate wisely, and always consider the total cost of ownership, not just the monthly payment. Understanding the average cost of a car loan per month is the first step toward smart vehicle financing, allowing you to confidently secure a deal that fits your budget and paves the way for many enjoyable miles ahead. Drive smart, and the road ahead will be much smoother.