Decoding Your Monthly Payment On a $13,000 Car Loan: An Expert’s Comprehensive Guide

Decoding Your Monthly Payment On a $13,000 Car Loan: An Expert’s Comprehensive Guide Carloan.Guidemechanic.com

Embarking on the journey to purchase a car is exciting, but navigating the financial landscape can often feel overwhelming. One of the most common questions potential car owners ask is, "What will my monthly payment be?" This is especially true when considering a specific loan amount, like a $13,000 car loan. Understanding the intricacies behind this figure is crucial for smart financial planning and avoiding unexpected surprises.

As an expert blogger and professional SEO content writer, I’ve spent years analyzing the automotive financing market. My goal with this extensive guide is to demystify the monthly payment on a $13,000 car loan, providing you with a complete toolkit to understand, calculate, and even optimize your payments. We’ll dive deep into every factor that influences your loan, ensuring you make an informed decision that fits your budget perfectly.

Decoding Your Monthly Payment On a $13,000 Car Loan: An Expert’s Comprehensive Guide

Understanding the Foundation: What Truly Shapes Your Car Loan Payment?

Calculating the monthly payment on a $13,000 car loan isn’t as simple as plugging numbers into a basic calculator. Several critical factors intertwine to determine the final figure you’ll pay each month. Grasping these elements is the first step toward financial empowerment in your car buying process.

The Core: Your Loan Amount (The $13,000 Principal)

Naturally, the principal amount you borrow forms the base of your monthly payment. In our scenario, we’re focusing on a $13,000 car loan. This figure represents the amount the lender provides after any down payment, trade-in value, and before interest is applied. It’s the money you are obligated to repay.

However, remember that the "sticker price" of a car isn’t always the loan amount. Sales tax, registration fees, and other charges can increase the total amount you need to finance, even if the car itself costs $13,000. Always clarify the exact principal amount you’ll be borrowing.

The Cost of Borrowing: Interest Rates Explained

The interest rate is arguably the most significant factor after the principal itself. It’s essentially the cost you pay for borrowing the money, expressed as a percentage of the loan amount. A higher interest rate means a larger portion of your monthly payment goes towards interest, increasing your total cost over the loan’s life.

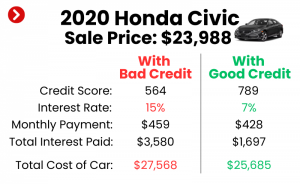

Based on my experience, interest rates are primarily influenced by your credit score, the lender’s policies, current market conditions, and the loan term. Even a seemingly small difference in the interest rate can lead to substantial savings or additional costs over the life of your $13,000 car loan. Shopping around for the best rate is not just a suggestion; it’s a necessity.

The Time Horizon: How Loan Terms Impact Your Payment

The loan term, or the duration over which you agree to repay the loan, directly affects your monthly payment. Common terms for car loans range from 36 months (3 years) to 72 months (6 years), and sometimes even longer.

A longer loan term will typically result in a lower monthly payment on a $13,000 car loan. This is because you’re spreading the repayment over more months. However, a crucial point to remember is that a longer term also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term will lead to higher monthly payments but significantly less total interest paid. It’s a trade-off between monthly affordability and overall cost.

Reducing Your Principal: The Power of a Down Payment

A down payment is the initial amount of money you pay upfront for the car, reducing the amount you need to borrow. For a $13,000 car loan, putting down even a small amount can make a notable difference.

Pro tips from us: Making a substantial down payment is one of the most effective strategies to lower your monthly payments and reduce the total interest you pay. It also signals to lenders that you are a lower-risk borrower, potentially leading to better interest rates. It immediately reduces your principal, meaning you borrow less from the start.

The Value of Your Old Ride: Trade-In Equity

Similar to a down payment, the equity from your trade-in vehicle can significantly reduce your loan amount. If your current car is worth more than what you owe on it, that positive equity can be applied directly to your new purchase.

This reduces the principal for your $13,000 car loan, making your monthly payments more manageable. Always get multiple appraisals for your trade-in to ensure you’re getting a fair value.

Breaking Down the $13,000 Car Loan: Practical Payment Scenarios

To provide a clear picture, let’s explore various scenarios for a $13,000 car loan with different credit scores, interest rates, and loan terms. Please note these are estimates, and actual rates may vary. We will assume no down payment for simplicity in comparing the impact of interest and term.

Scenario 1: The Advantage of Excellent Credit (780+)

With excellent credit, you are considered a low-risk borrower, qualifying for the most favorable interest rates.

- Estimated Interest Rate: 3.5% – 5.0% APR

- Monthly Payment Examples:

- 36 Months (3 Years) at 4.0% APR: Approximately $381 – $383 per month. While the monthly payment is higher, the total interest paid will be minimal, around $700.

- 48 Months (4 Years) at 4.0% APR: Approximately $294 – $296 per month. This term offers a good balance between a manageable monthly payment and reasonable total interest.

- 60 Months (5 Years) at 4.0% APR: Approximately $239 – $241 per month. This significantly lowers your monthly obligation but increases the total interest paid to roughly $1,000.

Having excellent credit means you have more flexibility to choose a term that aligns with your budget and financial goals. You can opt for a shorter term to save on interest or a longer one for lower monthly payments without a drastic increase in overall cost.

Scenario 2: Navigating with Good Credit (670-739)

Good credit is solid and opens doors to competitive rates, though not always the absolute lowest.

- Estimated Interest Rate: 6.0% – 8.0% APR

- Monthly Payment Examples:

- 36 Months (3 Years) at 7.0% APR: Approximately $401 – $403 per month. The total interest paid here would be around $1,500, nearly double that of excellent credit.

- 48 Months (4 Years) at 7.0% APR: Approximately $311 – $313 per month. This keeps your monthly payment reasonable but means over $2,000 in total interest.

- 60 Months (5 Years) at 7.0% APR: Approximately $257 – $259 per month. While seemingly attractive for its low monthly cost, the total interest climbs to over $2,500, adding significantly to the true cost of your $13,000 car loan.

For those with good credit, careful consideration of the loan term is vital. While a longer term makes monthly payments more affordable, the cumulative interest cost becomes much more pronounced than with excellent credit.

Scenario 3: Fair/Average Credit (580-669)

Borrowers with fair or average credit might face higher interest rates due to perceived higher risk.

- Estimated Interest Rate: 10.0% – 15.0% APR

- Monthly Payment Examples:

- 36 Months (3 Years) at 12.0% APR: Approximately $431 – $433 per month. The total interest in this scenario is substantial, approaching $2,500.

- 48 Months (4 Years) at 12.0% APR: Approximately $342 – $344 per month. This payment might feel more manageable, but the total interest paid on your $13,000 car loan would be over $3,300.

- 60 Months (5 Years) at 12.0% APR: Approximately $289 – $291 per month. While offering the lowest monthly burden, the total interest skyrockets to over $4,300.

Common mistakes to avoid are focusing solely on the monthly payment with fair credit. The total cost of the loan becomes very high at these interest rates. It might be wise to consider improving your credit score before taking on such a loan or opting for a less expensive vehicle.

Scenario 4: Challenging with Poor Credit (Below 580)

With poor credit, interest rates can be exceptionally high, making a $13,000 car loan quite expensive.

- Estimated Interest Rate: 18.0% – 25.0% APR (or even higher)

- Monthly Payment Examples:

- 36 Months (3 Years) at 20.0% APR: Approximately $480 – $482 per month. The total interest paid could exceed $4,300.

- 48 Months (4 Years) at 20.0% APR: Approximately $389 – $391 per month. The total interest here would be over $5,700.

- 60 Months (5 Years) at 20.0% APR: Approximately $334 – $336 per month. This makes the $13,000 car loan cost over $20,000 in total, with more than $7,000 in interest alone.

For those with poor credit, securing a $13,000 car loan might be challenging, and the cost could be prohibitive. It’s often advisable to explore options like a co-signer, saving for a larger down payment, or working on credit repair before committing to such high-interest rates. The long-term financial strain can be significant.

Beyond the Monthly Payment: Unpacking Hidden Costs and Considerations

While the monthly loan payment is a major factor, it’s just one piece of the car ownership puzzle. Overlooking other associated costs can quickly derail your budget.

The Inevitable: Sales Tax and Registration Fees

Almost every car purchase involves sales tax, which varies significantly by state and even locality. This tax is typically applied to the vehicle’s purchase price before financing, but it can sometimes be rolled into your loan, increasing the principal. Registration fees and license plate costs are also one-time or annual expenses required by your state.

Always factor these into your overall budget. For a $13,000 car loan, sales tax alone could add several hundred dollars, while registration fees are typically in the tens or hundreds of dollars. These are non-negotiable costs.

Essential Protection: Car Insurance

If you finance a car, comprehensive and collision insurance coverage is almost always a mandatory requirement from your lender. This protects their asset (the car) in case of an accident or theft. Insurance premiums can vary widely based on your age, driving record, location, and the specific vehicle.

Based on my experience, many first-time car buyers or those upgrading fail to adequately budget for insurance. Get insurance quotes before finalizing your car purchase to understand this significant recurring expense. It’s a crucial part of your total monthly car-related outlay.

Keeping It Running: Maintenance and Repairs

Every car, new or used, requires ongoing maintenance like oil changes, tire rotations, and occasional repairs. For a $13,000 car, it’s likely a used vehicle, which might have more immediate maintenance needs than a brand-new one.

Pro tips from us: Allocate a portion of your monthly budget for routine maintenance and an emergency fund for unexpected repairs. Neglecting maintenance can lead to more expensive problems down the road. Consider a pre-purchase inspection by an independent mechanic for any used vehicle.

The Fuel Factor: Gas Prices

Fuel costs are a constant companion for car owners. The type of car you choose (e.g., fuel-efficient compact vs. larger SUV) and your daily commute will dictate this expense.

Even with a budget-friendly $13,000 car loan, high fuel consumption can quickly eat into your finances. Research the car’s average MPG (miles per gallon) and estimate your weekly fuel costs.

Optional, But Common: Extended Warranties

Dealers often offer extended warranties or service contracts, especially for used vehicles. These can cover certain repairs beyond the manufacturer’s warranty. While they offer peace of mind, they also come with a significant upfront cost that can sometimes be rolled into your loan.

Carefully evaluate if an extended warranty is right for you. Sometimes, these are overpriced, and a robust emergency savings fund might be a more financially sound option. Understand the coverage and exclusions thoroughly.

Strategies to Optimize Your Monthly Payment on a $13,000 Car Loan

Now that we understand the factors, let’s explore actionable strategies to make your $13,000 car loan more manageable and cost-effective.

1. Boost Your Down Payment

As discussed, a larger down payment directly reduces the principal amount you need to borrow. This immediately translates to lower monthly payments and less interest paid over the loan’s life. Even an extra $500 or $1,000 can make a noticeable difference.

Consider waiting a little longer to save up more cash if your current savings are minimal. This patience can save you significant money in the long run and give you a stronger financial footing.

2. Prioritize Improving Your Credit Score

Your credit score is king when it comes to interest rates. Before applying for a $13,000 car loan, take steps to improve your credit. This could involve paying down existing debts, disputing errors on your credit report, or simply waiting for negative marks to age off.

to learn more about actionable steps. A higher score translates to a lower APR, which directly reduces both your monthly payment and total interest.

3. Shop Around for the Best Lenders and Rates

Never settle for the first loan offer you receive, especially from the dealership. Dealership financing can be convenient, but it might not always be the most competitive.

Based on my experience, applying for pre-approval from multiple lenders – including banks, credit unions, and online lenders – is crucial. This allows you to compare offers and leverage them to negotiate better terms. Credit unions, in particular, often offer very competitive rates to their members.

4. Consider a Shorter Loan Term (If Feasible)

While a longer term lowers your monthly payment, it significantly increases the total interest paid. If your budget allows, opting for a shorter loan term (e.g., 36 or 48 months instead of 60) can save you thousands in interest over the life of your $13,000 car loan.

This strategy requires a higher monthly payment, so it’s essential to assess your cash flow carefully. It’s a balance between monthly affordability and long-term savings.

5. Refinance Your Car Loan Down the Road

If your credit score improves significantly after you’ve taken out your $13,000 car loan, or if interest rates drop in the market, refinancing could be an excellent option. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate.

This can reduce your monthly payment, the total interest paid, or both. It’s a smart move to periodically check if refinancing opportunities exist, especially if your initial loan came with a high interest rate due to credit challenges.

Pro Tips from Us: Navigating Your $13,000 Car Loan Like a Pro

As an expert in personal finance and automotive content, I’ve seen countless car buyers make common mistakes that cost them dearly. Here are some essential "pro tips" to ensure your $13,000 car loan experience is as smooth and cost-effective as possible:

Don’t Just Focus on the Monthly Payment

This is perhaps the most critical piece of advice. Dealerships often try to "sell you on the monthly payment." They might offer you a longer term to make the payment seem more affordable, but this usually means you’ll pay significantly more in total interest. Always ask for the total cost of the loan and compare it across different offers.

Understanding the total interest paid over the life of your $13,000 car loan is far more important than just the monthly number. A slightly higher monthly payment for a shorter term can save you hundreds, if not thousands, in the long run.

Understand Your Annual Percentage Rate (APR)

The APR is the true annual cost of your loan. It includes not just the interest rate but also any additional fees charged by the lender, expressed as a single percentage. This provides a more accurate picture of the loan’s actual cost than the interest rate alone.

Always compare APRs when evaluating loan offers. A lower APR directly translates to a lower overall cost for your $13,000 car loan.

Read the Fine Print, Every Single Word

Loan agreements can be complex, filled with jargon. Common mistakes to avoid include skimming the document or assuming you understand everything. Take your time, read every clause, and ask questions about anything you don’t understand.

Pay close attention to prepayment penalties, late payment fees, and any clauses regarding insurance or vehicle modifications. Transparency is key, and an honest lender will be happy to explain every detail.

Budget Realistically for All Car Ownership Costs

Your car budget shouldn’t just include the monthly payment on your $13,000 car loan. As we discussed, you must account for insurance, fuel, maintenance, registration, and potentially parking or tolls.

Based on my experience, many people underestimate these additional costs, leading to financial strain. Create a comprehensive budget that includes all car-related expenses before you commit to a purchase.

Pre-Qualify, Don’t Just Pre-Approve

Pre-qualification gives you an estimate of what you might be approved for without a hard inquiry on your credit, which can temporarily lower your score. Pre-approval, on the other hand, is a firm offer based on a hard credit pull.

Getting pre-qualified from a few lenders allows you to shop for cars with a realistic understanding of your borrowing power and interest rate expectations. It gives you leverage at the dealership.

Consider a Co-Signer (If Your Credit is Challenged)

If you have a lower credit score, a co-signer with excellent credit can significantly improve your chances of approval for a $13,000 car loan and help you secure a much lower interest rate.

However, understand that a co-signer is equally responsible for the loan. If you miss payments, it impacts their credit score, too. This should only be considered with someone you trust implicitly and after a clear discussion of responsibilities.

Don’t Forget the Resale Value

While not directly impacting your monthly payment on a $13,000 car loan, considering a vehicle’s potential resale value is a smart financial move. Some cars hold their value better than others, which can be beneficial when it’s time to sell or trade in.

This helps mitigate depreciation, one of the hidden costs of car ownership. Research vehicle depreciation rates before making your final decision.

Final Thoughts: Driving Towards Financial Confidence

Navigating the world of car loans, especially for a specific amount like a $13,000 car loan, requires a blend of knowledge, careful planning, and strategic action. By understanding the factors that influence your monthly payment, being aware of all associated costs, and implementing smart financial strategies, you can confidently make a decision that aligns with your budget and financial goals.

Remember, the ultimate goal isn’t just to get approved for a loan, but to secure one that is sustainable and doesn’t become a financial burden. Arm yourself with information, shop around, and always prioritize the total cost over just the monthly payment. Your financial well-being is worth the extra effort.

Start your car buying journey wisely, and drive away with confidence!