Decoding Your Navy Federal Car Loan APR: A Comprehensive Guide to Securing the Best Auto Rates

Decoding Your Navy Federal Car Loan APR: A Comprehensive Guide to Securing the Best Auto Rates Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but navigating the world of auto loans can often feel like deciphering a complex code. For active duty military personnel, veterans, and their families, Navy Federal Credit Union stands out as a beacon of trust and competitive financial products. Understanding your Navy Federal Car Loan APR isn’t just about knowing a number; it’s about unlocking the true cost of your loan and empowering yourself to make the smartest financial decision.

This super comprehensive guide is designed to be your ultimate resource, demystifying everything you need to know about securing an auto loan through Navy Federal. We’ll delve deep into what APR truly means, the unique advantages Navy Federal offers, the critical factors that influence your rates, and actionable strategies to help you achieve the lowest possible APR. Our goal is to equip you with the knowledge and confidence to drive away with a fantastic deal, ensuring your vehicle purchase is both joyful and financially sound.

Decoding Your Navy Federal Car Loan APR: A Comprehensive Guide to Securing the Best Auto Rates

What Exactly is APR, and Why Does it Matter So Much for Your Car Loan?

Before we dive into the specifics of Navy Federal’s offerings, let’s clarify a fundamental concept: Annual Percentage Rate, or APR. Many people confuse APR with a simple interest rate, but they are distinctly different and understanding this distinction is crucial for any borrower. The interest rate is the percentage you pay on the principal loan amount, essentially the cost of borrowing money.

However, APR provides a more holistic view of the total cost of your loan. It includes not only the interest rate but also any additional fees associated with the loan, such as administrative fees, origination fees, or other charges rolled into the loan amount. Essentially, APR represents the true annual cost of borrowing money, expressed as a percentage of the loan amount. This comprehensive figure allows you to accurately compare different loan offers.

A lower APR directly translates to less money paid over the life of your loan. Even a small difference in percentage points can save you hundreds, or even thousands, of dollars, especially on larger loan amounts or longer terms. When evaluating Navy Federal auto loan rates, always focus on the APR to understand the full financial commitment. It’s the single most important number to consider when comparing loan offers and making an informed decision about your vehicle financing.

The Navy Federal Advantage: Why Consider Them for Your Auto Loan?

For military members, veterans, and their families, Navy Federal Credit Union isn’t just another financial institution; it’s a trusted partner built on a foundation of serving those who serve. This unique mission translates into distinct advantages when it comes to auto loans, often setting them apart from traditional banks and other lenders. Their commitment to the military community shapes their offerings, making them a prime choice for a car loan for military personnel.

Eligibility for Navy Federal membership extends to all branches of the armed forces, veterans, Department of Defense civilians, and their immediate families. This broad inclusion ensures that a vast segment of the military community can access their competitive financial products. Unlike many commercial banks driven solely by profit, Navy Federal operates as a not-for-profit credit union, meaning their earnings are typically reinvested into providing better rates and services to their members.

Based on my experience, Navy Federal truly understands the unique financial situations and challenges faced by military families, from deployments to frequent moves. This understanding often translates into flexible loan terms, tailored advice, and exceptional member service that goes beyond a transactional relationship. They frequently offer some of the most competitive Navy Federal auto loan rates in the market, making them a top contender for the best car loan for veterans and active duty personnel. Their member-centric approach aims to empower you, not just lend to you.

Key Factors Influencing Your Navy Federal Car Loan APR

Understanding that not everyone receives the same APR is the first step toward securing the best rate for you. Several critical factors play a significant role in determining your specific Navy Federal Car Loan APR. By knowing these elements, you can strategically position yourself to qualify for the most favorable terms. These are the primary factors affecting car loan rates that Navy Federal, like any lender, will consider.

Your Credit Score: The Cornerstone of Your Rate

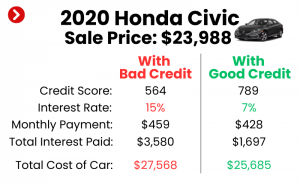

Your credit score is arguably the most impactful factor in determining your loan’s APR. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score signals to lenders that you are a responsible borrower, thereby reducing their perceived risk.

Generally, scores above 720 are considered excellent, often qualifying borrowers for the lowest available rates. Good scores typically fall between 670 and 719, while average scores range from 580 to 669. If your score is on the lower end, you might still qualify for a loan, but your APR will likely be higher to compensate for the increased risk. Pro tips from us: Always check your credit report from all three major bureaus (Experian, Equifax, TransUnion) before applying for a loan to identify any errors and understand your standing.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, usually expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term typically comes with a lower APR because the lender’s money is tied up for a shorter period, reducing their exposure to risk. However, shorter terms result in higher monthly payments.

Conversely, a longer loan term will likely have a higher APR, but it offers the advantage of lower monthly payments, making the vehicle more "affordable" on a month-to-month basis. While lower monthly payments can be appealing, a longer term means you pay more in interest over the life of the loan. It’s crucial to find a balance between an affordable monthly payment and the total cost of the loan.

Loan-to-Value (LTV) Ratio and Your Down Payment

The Loan-to-Value (LTV) ratio is a comparison of the amount you are borrowing versus the actual value of the car. A higher down payment directly reduces your LTV ratio, as you are financing a smaller portion of the vehicle’s cost. This is a significant factor in securing a better APR.

Putting down a substantial down payment reduces the lender’s risk, as you have more equity in the vehicle from the start. It also means you’ll be financing less, which can lead to lower monthly payments even at the same APR. Pro tips from us: Aim for a down payment of at least 10-20% if possible, as this can significantly improve your chances of getting a favorable how to get a low APR.

Vehicle Type and Age: New vs. Used

The type and age of the vehicle you intend to purchase can also influence your APR. New cars often qualify for lower interest rates compared to used cars. This is because new vehicles generally hold their value better initially and are seen as less risky collateral by lenders.

Used cars, especially older models, typically come with slightly higher APRs. This reflects the increased risk associated with depreciation, potential maintenance issues, and a shorter expected lifespan. While Navy Federal offers competitive rates for both new and used vehicles, it’s a factor to keep in mind when budgeting and considering your financing options.

Your Relationship with Navy Federal

While not explicitly a published factor, your overall banking relationship with Navy Federal can subtly influence your loan approval and potentially your rate. Being a long-standing member in good standing, with multiple accounts, direct deposit, or other financial products, can demonstrate a deeper financial commitment and trustworthiness. This established relationship can sometimes provide a slight edge, especially in borderline situations.

Navigating the Navy Federal Car Loan Application Process

Applying for an auto loan with Navy Federal is a streamlined process designed to be member-friendly, but understanding each step can make it even smoother. Being prepared and knowing what to expect can significantly reduce stress and speed up your approval for a Navy Federal auto loan. The cornerstone of this process often begins with membership.

Membership Requirement: Your First Step

As a credit union, Navy Federal serves its members exclusively. Therefore, the very first step is ensuring you meet their eligibility criteria for Navy Federal membership. This typically includes active duty military, reservists, veterans, Department of Defense civilians, and their immediate family members. If you’re not yet a member, you’ll need to join before applying for any loan products. This ensures you can access all the benefits, including their competitive auto loan rates.

Pre-Approval: Your Secret Weapon in Car Buying

One of the most powerful tools in your car buying arsenal is pre-approval. This step involves Navy Federal reviewing your financial information and tentatively approving you for a loan up to a certain amount, at a specific APR, before you even step foot in a dealership. It’s a non-committal offer that provides immense benefits.

The benefits of getting pre-approved are multifold. First, it gives you a clear budget, so you know exactly how much car you can afford. Second, and perhaps most importantly, it transforms you into a cash buyer in the eyes of the dealership. This provides significant bargaining power, as you can negotiate the vehicle price without the added pressure of securing financing on the spot. Common mistakes to avoid are skipping pre-approval and letting the dealership handle all the financing, which often leads to higher rates and less favorable terms. The pre-approval process with Navy Federal is straightforward and can be done online, by phone, or in person.

Required Documentation: Be Prepared

When you apply for a loan, whether for pre-approval or final approval, Navy Federal will require certain documentation to verify your identity, income, and financial stability. Having these documents ready can expedite the process.

Typically, you’ll need:

- Proof of Identity: Government-issued ID (driver’s license, military ID).

- Proof of Income: Pay stubs, W-2 forms, tax returns, or direct deposit statements.

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information (if already selected): VIN, make, model, year, mileage.

For pre-approval, some of this might not be immediately necessary, but having income verification on hand is always a good idea.

Application Channels: Choose Your Convenience

Navy Federal offers multiple convenient ways to apply for your auto loan:

- Online: Their website provides a user-friendly application portal where you can complete the entire process from the comfort of your home.

- Phone: You can speak directly with a loan officer by calling their member service line, who can guide you through the application.

- Branch Visit: If you prefer face-to-face interaction, you can visit any Navy Federal branch to apply in person.

Each method offers flexibility, allowing you to choose the option that best suits your needs and schedule.

Understanding the Offer: What to Look For

Once approved, Navy Federal will provide you with a loan offer outlining the terms. Carefully review this document. Pay close attention to:

- The APR: This is the most crucial number, representing your total cost of borrowing.

- Loan Term: Confirm the number of months for repayment.

- Monthly Payment: Ensure it fits comfortably within your budget.

- Total Cost of the Loan: This includes the principal plus all interest paid over the term.

Don’t hesitate to ask questions if anything is unclear. Navy Federal prides itself on transparency and member education.

Strategies for Securing the Best Navy Federal Car Loan APR

While Navy Federal is known for competitive rates, your individual actions can significantly influence the Navy Federal Car Loan APR you ultimately receive. Implementing smart financial strategies before and during the application process can lead to substantial savings over the life of your loan. These tactics are designed to show Navy Federal that you are a low-risk borrower, making you eligible for their most favorable Navy Federal auto loan rates.

1. Boost Your Credit Score

Improving your credit score is the single most effective way to lower your APR. Lenders view higher scores as an indicator of financial responsibility.

- Pay Bills On Time, Every Time: Payment history is the largest component of your credit score. Set up automatic payments to avoid missing due dates.

- Reduce Existing Debt: Lowering your credit card balances or other revolving debt improves your credit utilization ratio, which positively impacts your score.

- Review Your Credit Report for Errors: Incorrect information can unfairly drag down your score. Obtain free copies of your credit report annually and dispute any inaccuracies promptly.

- Avoid New Credit Applications: Limit applying for new credit cards or loans in the months leading up to your car loan application, as each hard inquiry can temporarily lower your score.

For more detailed advice on improving your credit score, check out our guide on .

2. Increase Your Down Payment

As discussed, a larger down payment reduces the loan amount and the Loan-to-Value (LTV) ratio. This translates directly into less risk for Navy Federal, making them more likely to offer you a lower APR.

- Save Aggressively: Prioritize saving for a down payment as early as possible.

- Trade-In Value: If you have a vehicle to trade in, maximize its value to contribute more towards your new car purchase.

- The Power of 20%: Aim for at least a 20% down payment if feasible, as this often eliminates the need for GAP insurance and significantly lowers your monthly payments and total interest.

3. Choose a Shorter Loan Term (If Feasible)

While longer terms mean lower monthly payments, they almost always come with a higher APR and significantly more interest paid over time.

- Assess Your Budget: Honestly evaluate how much you can comfortably afford each month without straining your finances.

- Balance Affordability and Total Cost: If you can manage a slightly higher monthly payment, opting for a 48 or 60-month term instead of 72 or 84 months can save you a substantial amount in interest and secure a better APR.

4. Consider a Co-Signer (If Necessary)

If your credit score is less than ideal, or if you’re a young borrower with limited credit history, a co-signer with excellent credit can help you qualify for a better APR.

- Choose Wisely: A co-signer shares equal responsibility for the loan, so choose someone you trust and who understands the commitment.

- Build Your Own Credit: Use this opportunity to establish a positive payment history, so you can qualify on your own for future loans.

5. Leverage Pre-Approval to Your Advantage

Don’t underestimate the power of being pre-approved by Navy Federal before you start negotiating at the dealership.

- Shop with Confidence: You know your budget and your exact APR, allowing you to focus solely on the vehicle price.

- Bargaining Power: Dealers are more likely to offer their best price when they know you already have financing secured. They might even try to beat Navy Federal’s pre-approved rate, giving you an even better deal.

6. Explore Refinancing Options

If you already have a car loan with another lender at a higher APR, or if your credit score has significantly improved since you financed your current vehicle, Navy Federal’s refinancing options could save you money.

- Check Current Rates: Compare your existing loan’s APR with Navy Federal’s current auto loan rates.

- Evaluate Benefits: Refinancing can lower your monthly payment, reduce your overall interest paid, or shorten your loan term.

- Simple Process: Navy Federal makes refinancing an existing auto loan a straightforward process, often without hidden fees.

Based on years of helping clients, these strategies consistently yield better rates and more favorable loan terms. Applying these tips can make a significant difference in your car buying experience with Navy Federal. You can find official details on Navy Federal’s auto loan offerings directly on their website: .

Beyond the APR: Other Considerations for Your Navy Federal Auto Loan

While securing a low Navy Federal Car Loan APR is paramount, the overall value of your auto loan experience extends beyond that single number. Navy Federal offers additional benefits and considerations that underscore their member-first philosophy, making them an even more attractive choice for your vehicle financing.

No Hidden Fees and Transparent Terms

One of the hallmarks of Navy Federal is their commitment to transparency. Unlike some lenders that might surprise you with application fees, prepayment penalties, or other hidden charges, Navy Federal typically operates with clear and upfront terms. This means the APR they quote you is generally what you’ll pay, without unexpected additions. This straightforward approach provides peace of mind and builds trust, reinforcing their reputation as a member advocate.

GAP Insurance: Protecting Your Investment

When you finance a vehicle, especially a new one, there’s often a period where you owe more on the loan than the car is worth due to depreciation. This is where Guaranteed Asset Protection (GAP) insurance comes in. If your vehicle is stolen or totaled in an accident, your standard auto insurance policy will only pay out the car’s actual cash value, which might be less than your outstanding loan balance.

Navy Federal offers competitive GAP insurance to bridge this financial gap, protecting you from having to pay out-of-pocket for a vehicle you no longer have. It’s an optional but highly recommended add-on, particularly if you make a small down payment or opt for a longer loan term.

Payment Protection: Financial Security for Unforeseen Events

Life is unpredictable, and unexpected events like job loss, disability, or even death can impact your ability to make loan payments. Navy Federal offers payment protection plans designed to safeguard your finances during such challenging times. These plans can cover or defer your loan payments under specific circumstances, providing a crucial safety net.

While it adds a small amount to your monthly payment, the peace of mind it offers can be invaluable. It’s a testament to Navy Federal’s understanding of their members’ lives and their desire to provide comprehensive financial security.

Exceptional Member Service: A Partnership, Not Just a Transaction

Beyond rates and products, Navy Federal is renowned for its outstanding member service. Whether you have questions about your application, need assistance with your payments, or require financial advice, their dedicated team is readily available. This high level of support fosters a sense of partnership, ensuring you feel valued and supported throughout your loan journey and beyond. Their commitment to service truly makes them a standout for the best car loan for veterans and military families.

Thinking about the full cost of car ownership? Our article on can help you budget for all aspects of your new vehicle.

Conclusion: Drive Away Confident with Your Navy Federal Car Loan APR

Navigating the world of auto loans can be complex, but armed with the right knowledge, you can approach the process with confidence and clarity. For the military community and their families, Navy Federal Credit Union presents an unparalleled opportunity to secure competitive Navy Federal Car Loan APRs and benefit from a truly member-centric financial experience. By understanding what APR truly represents, leveraging the unique advantages of Navy Federal, and strategically preparing your finances, you are well on your way to securing the best possible auto loan.

Remember, your credit score, down payment, and chosen loan term are powerful levers in determining your final rate. Don’t underestimate the power of pre-approval to give you the upper hand at the dealership. Whether you’re a first-time car buyer, looking to upgrade, or considering refinancing options, Navy Federal is dedicated to supporting your financial journey. Take the time to prepare, ask questions, and utilize the resources available to you. By doing so, you’ll not only drive away in the car of your dreams but also with a smart, affordable loan that serves your long-term financial well-being. Drive smart, save more, and let Navy Federal help you get there.