Demystifying Bank of America Used Car Loan Requirements: Your Ultimate Guide to Approval

Demystifying Bank of America Used Car Loan Requirements: Your Ultimate Guide to Approval Carloan.Guidemechanic.com

Navigating the world of auto financing can feel like a complex journey, especially when you’re seeking a used car loan. Among the myriad of lenders, Bank of America stands out as a prominent financial institution, offering competitive rates and a streamlined application process for millions. But what exactly does it take to secure a used car loan from them? What are the Bank of America Used Car Loan Requirements you need to meet?

As an expert in auto financing and a seasoned blogger, I understand the importance of clarity and preparation. This comprehensive guide is designed to cut through the jargon, providing you with an in-depth understanding of every criterion Bank of America considers. Our goal is to equip you with the knowledge to approach your loan application with confidence, significantly increasing your chances of approval and getting you behind the wheel of your next used car.

Demystifying Bank of America Used Car Loan Requirements: Your Ultimate Guide to Approval

Why Choose Bank of America for Your Used Car Loan?

Before diving into the specifics, it’s worth briefly considering why Bank of America is a popular choice for auto financing. They offer a vast network of branches, a robust online platform, and a reputation for stability. Many applicants appreciate their competitive interest rates and the convenience of managing their loan alongside other banking products.

Their digital tools allow for easy pre-qualification and application, making the entire process more accessible. For those already banking with Bank of America, the process can often feel even more integrated and straightforward. It’s this blend of reliability and modern convenience that draws many prospective used car buyers to their services.

The Core Philosophy: What Bank of America Looks For in a Borrower

Every lender, including Bank of America, assesses a potential borrower through a specific lens. This philosophy is built around three fundamental pillars: your creditworthiness, your ability to repay the loan, and the suitability of the vehicle itself. Understanding these core principles will help you prepare your application effectively.

They want to ensure you have a history of responsible financial behavior, that you can comfortably afford the monthly payments, and that the car you intend to purchase represents a sound investment. Meeting these broad expectations is the first step toward a successful Bank of America used car loan application. Let’s break down each specific requirement in detail.

1. Understanding Bank of America’s Credit Score Requirements

Your credit score is arguably the single most important factor Bank of America will consider. It acts as a snapshot of your financial reliability, indicating how well you’ve managed debt in the past. Lenders use this three-digit number to assess the risk associated with lending you money.

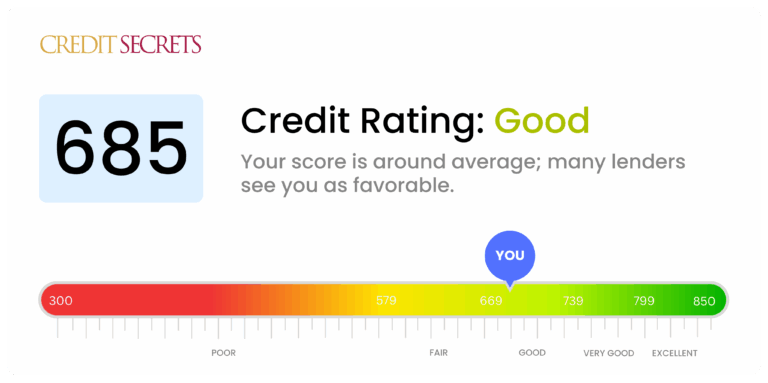

What is a Good Credit Score for a Used Car Loan?

While Bank of America doesn’t publish an official minimum credit score, based on my experience, most successful applicants for their best rates typically have a FICO score of 680 or higher. A score in the "good" to "excellent" range (generally 700+) positions you as a very attractive borrower, often qualifying you for lower interest rates and more favorable loan terms.

Applicants with scores between 620 and 679 might still be approved, but they could face higher interest rates. This is because a lower score suggests a slightly elevated risk profile to the lender. It’s crucial to remember that your credit score is just one piece of the puzzle, albeit a very significant one.

What if Your Credit Isn’t Perfect?

If your credit score falls below the ideal range, don’t despair. There are still avenues to explore. One option is to consider applying with a co-signer who has excellent credit. A co-signer essentially guarantees the loan, mitigating some of the risk for Bank of America. This can significantly improve your chances of approval and potentially secure a better interest rate.

Another strategy is to dedicate time to improving your credit score before applying. This could involve paying down existing debts, disputing any errors on your credit report, or simply waiting for negative marks to age off. Even a slight improvement can make a difference in the loan offers you receive.

Pro Tip from Us: Always check your credit score and report well before you even start looking for a car. Services like AnnualCreditReport.com allow you to get a free report from each of the three major credit bureaus annually. Review it carefully for any inaccuracies that could be unfairly impacting your score. Addressing these errors can boost your credit and enhance your loan prospects.

2. Income and Employment Stability: Proving Your Ability to Repay

Beyond your credit history, Bank of America needs assurance that you have a steady and sufficient income to comfortably make your monthly loan payments. This isn’t just about having a job; it’s about demonstrating financial stability. They want to see that you have a reliable source of funds to meet your financial obligations.

Why Income and Employment History Matter

Lenders analyze your income to determine your debt-to-income (DTI) ratio, a critical metric we’ll discuss shortly. They also look at your employment history to gauge stability. A long tenure at your current job, or a consistent work history within the same industry, signals reliability. Frequent job changes, especially in different fields, might raise a red flag about future income consistency.

Generally, Bank of America prefers to see at least six months to a year of stable employment. If you’re self-employed, they will typically require two years of tax returns to demonstrate consistent income. This helps them understand your average earnings and predict your future repayment capacity.

Providing Proof of Income

When applying for a Bank of America used car loan, you’ll need to furnish documentation to verify your income. This usually includes recent pay stubs (typically the last two to three months) from your employer. If you receive W-2 forms, these might also be requested.

For self-employed individuals, or those with varied income sources, tax returns (often the last two years) are essential. Bank statements might also be reviewed to show consistent deposits. Having these documents organized and ready will streamline your application process significantly.

Understanding Your Debt-to-Income (DTI) Ratio

Your DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt (including mortgage/rent, credit card minimums, student loans, and the proposed car payment) is $1,500 and your gross monthly income is $4,000, your DTI is 37.5%.

Bank of America, like most lenders, prefers a DTI ratio of 36% or lower, though some flexibility exists, especially for applicants with excellent credit. A high DTI indicates that a significant portion of your income is already committed to existing debts, potentially making it harder to afford a new car payment. A lower DTI suggests you have more disposable income, making you a less risky borrower.

Common Mistakes to Avoid Are: Underestimating your current debt obligations or overestimating your net income. Be honest and thorough when calculating your DTI; lenders will verify these figures. Not factoring in all existing debt can lead to an inaccurate picture of your financial standing.

3. Down Payment Considerations for a Used Car Loan

While Bank of America may not always require a down payment, making one is almost always a smart financial move. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also demonstrates your commitment to the purchase.

The Benefits of Making a Down Payment

Even a small down payment can make a difference. A larger down payment, however, brings significant advantages. It signals to Bank of America that you are serious about the purchase and have some equity in the vehicle from day one. This reduces the lender’s risk, often translating into better loan terms and potentially a lower interest rate for you.

Furthermore, a substantial down payment can help you avoid becoming "upside down" on your loan, where you owe more than the car is worth. This is particularly relevant for used cars, which can depreciate quickly. Aiming for at least 10-20% of the vehicle’s purchase price as a down payment is a solid strategy.

Pro Tip from Us: Start saving for your down payment as early as possible. Even small, consistent contributions can add up. The more you can put down upfront, the stronger your application will be, and the better your financial position will be in the long run.

4. Vehicle Specific Requirements: Not Just Any Used Car Will Do

It’s not just about you; the car you intend to purchase also needs to meet Bank of America’s criteria. Lenders view the vehicle as collateral for the loan, so they have specific standards to ensure its value and reliability. This is particularly important for used cars, where condition can vary widely.

Age and Mileage Limits

Bank of America typically places limits on the age and mileage of used vehicles they will finance. While these can vary, a common guideline is that the vehicle should be no more than 7-10 model years old and have less than 100,000-120,000 miles on the odometer. Cars that are older or have significantly higher mileage are generally seen as higher risk due to potential maintenance issues and faster depreciation.

These limits are in place to protect both the borrower and the lender. An older, higher-mileage car is more prone to breakdowns, which could lead to missed payments if the borrower faces unexpected repair costs. It also holds less value as collateral.

Vehicle Value Assessment

Bank of America will assess the market value of the used car you wish to purchase. They often use industry-standard guides like Kelley Blue Book (KBB) or NADAguides to determine the car’s fair market value. The loan amount they approve will generally not exceed this appraised value.

This assessment ensures that you are not overpaying for the vehicle and that the loan amount is reasonable in relation to its worth. The vehicle must also have a clear title, meaning it is not salvage, rebuilt, or branded with other significant issues that could affect its value or legality.

Dealer vs. Private Party Sales

Bank of America generally prefers to finance vehicles purchased from an authorized dealership. While they do offer financing for private party sales, the process can be more involved. When buying from a dealership, the transaction is often more structured, and the dealership handles much of the paperwork directly with the bank.

For private party sales, you’ll likely need to arrange a vehicle inspection, verify the title, and ensure all necessary paperwork is correctly handled. Be prepared for a potentially longer process and more direct involvement in coordinating with the seller and Bank of America.

Common Mistakes to Avoid Are: Falling in love with a vehicle that doesn’t meet the lender’s criteria for age, mileage, or value. Always confirm the car’s specifications with Bank of America’s guidelines before getting too far into the purchasing process.

5. Residency and Age Requirements

These are straightforward but essential requirements for any loan application. You must meet the legal age and residency criteria to enter into a binding financial agreement.

Legal Age

To apply for a loan with Bank of America, you must be at least 18 years old, which is the legal age to enter into a contract in most U.S. states. In some states, the age of majority for certain financial transactions might be 21, so it’s always wise to confirm local regulations.

U.S. Residency

Applicants must be U.S. citizens or permanent residents with a valid U.S. address. You’ll need to provide proof of residency, typically through a driver’s license, state ID, or utility bills addressed to you. This confirms your legal status and ability to reside within the country for the duration of the loan term.

6. Required Documentation: Be Prepared

Having all your documents in order before you apply can significantly speed up the approval process. Bank of America needs various forms of identification and verification to process your loan.

Here’s a checklist of common documents you’ll need:

- Personal Identification: A valid U.S. driver’s license or state-issued ID, along with your Social Security Number (SSN).

- Proof of Address: Recent utility bills (electricity, water, gas) or a lease agreement showing your current residential address.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, or tax returns (last two years, especially for self-employed individuals).

- Bank Account Information: Your Bank of America account details if you’re an existing customer, or information for your primary checking account for loan disbursements and payments.

- Vehicle Information (once you’ve chosen a car): Vehicle Identification Number (VIN), exact mileage, year, make, model, and potentially the seller’s information.

- Proof of Insurance: You will be required to have full coverage insurance on the vehicle before the loan is finalized. This protects both your investment and Bank of America’s collateral.

Pro Tip from Us: Create a dedicated folder, either physical or digital, for all your loan application documents. This organized approach will not only save you time but also present you as a responsible and prepared borrower to Bank of America.

The Bank of America Used Car Loan Application Process

Once you’ve gathered all your information and understand the requirements, the application process itself is fairly straightforward. Bank of America offers a user-friendly online application, which is often the quickest route.

Online Application and Pre-qualification

You can start by visiting the Bank of America auto loan section on their website. They often offer a pre-qualification option, which allows you to see potential rates and terms without impacting your credit score with a hard inquiry. This is an excellent way to gauge your eligibility before committing to a full application.

A full application will involve providing all the details discussed above. This will typically result in a hard inquiry on your credit report, which can slightly lower your score for a short period.

Submitting Documents and Awaiting a Decision

After submitting your application, Bank of America may request additional documentation or clarification. Respond promptly to these requests to keep the process moving. The time it takes for a decision can vary, but many online applications receive a response within a few business days, sometimes even faster.

Common Mistakes to Avoid Are: Applying to multiple lenders simultaneously in a short period. While rate shopping is good, too many hard inquiries can negatively impact your credit score. Try to consolidate your inquiries within a 14-day window, as credit bureaus often count multiple auto loan inquiries during this time as a single inquiry.

What Happens After Bank of America Used Car Loan Approval?

Congratulations! If your Bank of America used car loan application is approved, there are a few more steps before you drive off in your new car.

Reviewing Loan Terms and Signing the Contract

Carefully review the loan agreement, paying close attention to the interest rate, monthly payment, loan term, and any fees. Ensure you understand all the terms and conditions before signing. Don’t hesitate to ask questions if anything is unclear.

Disbursement of Funds

Once the contract is signed, Bank of America will disburse the funds. If you’re buying from a dealership, the funds are usually sent directly to them. For private party sales, the funds might be deposited into your account, or a check could be issued to the seller.

Setting Up Payments

You’ll establish how you’ll make your monthly payments. Bank of America often offers automatic payment options from your checking account, which can be convenient and sometimes even qualify you for a slight interest rate discount.

Pro Tips for Boosting Your Chances of Approval

Based on my experience, here are some actionable steps you can take to strengthen your application for a Bank of America used car loan:

- Improve Your Credit Score: Pay bills on time, reduce credit card balances, and avoid opening new credit accounts before applying. Even a few points can make a difference.

- Reduce Your Debt-to-Income (DTI) Ratio: Prioritize paying down existing debts, especially high-interest ones. This shows Bank of America you have more capacity for a new loan.

- Save for a Larger Down Payment: As discussed, a substantial down payment reduces the loan amount and signals financial responsibility.

- Consider a Co-signer: If your credit score or income isn’t ideal, a co-signer with strong credit can significantly enhance your application.

- Shop Smart for the Right Vehicle: Choose a used car that falls well within Bank of America’s age, mileage, and value guidelines. Don’t pick a car that’s too old or too expensive for your budget.

- Be Prepared with All Documentation: Having everything organized and ready shows diligence and can prevent delays in the approval process.

- Check Your Credit Report for Errors: This cannot be stressed enough. Incorrect information can unfairly lower your score. For more in-depth advice on managing your credit, consider reading our article on .

Common Mistakes to Avoid When Applying for a Used Car Loan

Even well-intentioned applicants can make missteps. Here are some common pitfalls to sidestep:

- Not Checking Your Credit Score First: Going into the application blind is a recipe for disappointment.

- Underestimating Your DTI: Be realistic about your current financial obligations.

- Applying for Too Much Loan Amount: Only borrow what you genuinely need and can comfortably afford. Don’t let enthusiasm lead to overspending.

- Not Comparing Offers: While Bank of America is a great choice, it’s always wise to compare their offer with a couple of other reputable lenders to ensure you’re getting the best terms. Our guide on also touches on financing comparisons.

- Not Understanding All Terms and Conditions: Read the fine print! Hidden fees or unfavorable clauses can cost you significantly over time.

Frequently Asked Questions (FAQs)

Let’s address a few common questions related to Bank of America used car loans:

- Can I get a Bank of America used car loan with bad credit? While challenging, it’s not impossible. A strong income, a significant down payment, or a qualified co-signer can improve your chances. However, expect higher interest rates.

- How long does the approval process take? Many applicants receive an initial decision within minutes or hours for online applications. More complex cases or those requiring additional documentation may take a few business days.

- Can I refinance an existing car loan with Bank of America? Yes, Bank of America offers auto loan refinancing. This can be a great option if your credit has improved, or if current interest rates are lower than what you’re currently paying.

Conclusion: Drive Towards Approval with Confidence

Securing a Bank of America used car loan is entirely achievable when you understand and meet their specific requirements. It’s a journey that demands preparation, transparency, and a solid understanding of your own financial standing. From maintaining a healthy credit score and demonstrating stable income to choosing a suitable vehicle and having all your documentation ready, each step contributes to a successful application.

By following the detailed guidance and expert tips outlined in this article, you are now better equipped to navigate the process with confidence. Remember, the ultimate goal is not just to get approved, but to secure a loan that fits comfortably within your budget, allowing you to enjoy your new-to-you vehicle without financial strain. Prepare thoroughly, apply wisely, and soon you’ll be driving off in your desired used car.

For further information directly from the source, you can always visit the Bank of America Auto Loans official page to review their latest offerings and terms.