Demystifying BECU Car Loan Interest Rates: Your Ultimate Guide to Driving a Better Deal

Demystifying BECU Car Loan Interest Rates: Your Ultimate Guide to Driving a Better Deal Carloan.Guidemechanic.com

Securing a car loan is a significant financial decision, and for many in the Pacific Northwest and beyond, BECU (Boeing Employees’ Credit Union) stands out as a top contender. Known for its member-centric approach and often competitive offerings, BECU is a popular choice for financing vehicles. However, understanding the intricacies of BECU car loan interest rates is crucial to ensure you’re getting the best possible deal.

This comprehensive guide will demystify everything you need to know about BECU’s auto loan interest rates. We’ll dive deep into what influences these rates, how to navigate the application process, and actionable strategies to secure a favorable agreement. Our goal is to empower you with the knowledge to approach your next car purchase with confidence, ensuring you drive away not just with a new car, but with a smart financial decision.

Demystifying BECU Car Loan Interest Rates: Your Ultimate Guide to Driving a Better Deal

Understanding BECU: A Unique Lender in the Auto Loan Landscape

Before we delve into the specifics of interest rates, it’s essential to grasp what makes BECU different from traditional banks. BECU operates as a credit union, meaning it’s a not-for-profit financial cooperative owned by its members. This fundamental difference often translates into benefits for borrowers.

Unlike banks that aim to maximize profits for shareholders, credit unions like BECU prioritize their members’ financial well-being. This model can lead to more favorable loan terms, including potentially lower interest rates on car loans, and fewer fees compared to commercial banks. It’s a core reason why BECU is often a first choice for many seeking auto financing.

To access BECU’s services, including their car loans, you must first become a member. Membership is generally open to anyone who lives, works, worships or attends school in Washington state, or has relatives who are BECU members. This inclusive approach has made it accessible to a wide demographic, far beyond just Boeing employees.

Based on my experience, understanding the credit union model is crucial because it sets the stage for their competitive offerings. Their structure allows them to pass on savings to members in the form of lower rates and better service, which is a significant advantage when you’re looking for an auto loan.

The Anatomy of BECU Car Loan Interest Rates: Beyond the Percentage

When you hear "car loan interest rate," it refers to the cost of borrowing money, expressed as a percentage of the loan amount. However, it’s vital to differentiate between the quoted interest rate and the Annual Percentage Rate (APR). While the interest rate is the base cost, the APR provides a more complete picture of the total cost of borrowing.

The APR includes the interest rate plus any additional fees or charges associated with the loan, such as origination fees. For car loans, these fees are typically minimal or non-existent, making the interest rate and APR often very close. Nevertheless, always ask for the APR to understand the true cost.

BECU’s credit union structure allows them to offer highly competitive APRs. They aim to provide value to their members, and this often translates into rates that are at or below the market average for well-qualified borrowers. This focus on member benefit is a cornerstone of their lending philosophy.

Most car loans, including those from BECU, come with fixed interest rates. This means your interest rate will remain the same throughout the life of your loan, providing predictable monthly payments. This stability is a significant advantage, protecting you from potential rate increases over time.

Key Factors Influencing Your BECU Car Loan Interest Rate

Several critical factors determine the interest rate you’ll be offered on a BECU car loan. Understanding these elements is the first step toward securing the most favorable terms. It’s not just about what BECU offers; it’s also about how you present yourself as a borrower.

Let’s break down each of these influential factors in detail, providing you with insights into how they impact your rate.

1. Your Credit Score: The Cornerstone of Your Rate

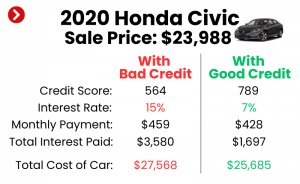

Your credit score is arguably the most significant factor influencing your BECU car loan interest rate. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders, including BECU, use this score to assess the risk of lending to you.

A higher credit score indicates a lower risk to the lender, typically resulting in a lower interest rate. Conversely, a lower score suggests a higher risk, leading to a higher interest rate to compensate the lender for that perceived risk. BECU, like other lenders, categorizes applicants into different credit tiers.

Generally, credit scores range from 300 to 850. An excellent credit score (typically 780+) will unlock BECU’s lowest advertised rates. A good score (700-779) will still qualify you for very competitive rates, while a fair score (620-699) might see a slight increase. Scores below 620 could result in significantly higher rates or even require a co-signer.

Pro tips from us: Always know your credit score before you apply for any loan. You can obtain a free credit report annually from each of the three major credit bureaus (Experian, Equifax, TransUnion) and often get your score for free through various financial apps or credit card providers. Rectifying any errors on your report or improving your score beforehand can save you hundreds, if not thousands, of dollars over the life of your car loan.

2. Loan Term: How Long You’ll Be Paying

The loan term, or the length of time you have to repay the loan, also plays a substantial role in determining your interest rate. BECU offers a range of loan terms, typically from 36 to 84 months, though specific options may vary.

Generally, shorter loan terms come with lower interest rates. This is because the lender’s risk decreases over a shorter period. While a shorter term means higher monthly payments, you’ll pay significantly less in total interest over the life of the loan.

Conversely, longer loan terms (e.g., 72 or 84 months) often have higher interest rates. Lenders perceive a higher risk when money is borrowed for an extended period, leading to a slight increase in the rate. Although longer terms result in lower monthly payments, you’ll end up paying more interest overall.

For instance, a 60-month loan might have a lower interest rate than a 72-month loan, even for the same borrower and vehicle. It’s a trade-off between monthly affordability and the total cost of the loan. Carefully consider your budget and long-term financial goals when choosing a loan term.

3. Down Payment Amount: Your Equity in the Vehicle

The size of your down payment directly impacts the loan amount and, consequently, the risk perceived by BECU. A larger down payment means you’re borrowing less money, and you have more equity in the vehicle from day one.

When you put down a significant amount, you reduce the lender’s exposure. This lower risk can often translate into a more favorable interest rate. Lenders view borrowers with substantial down payments as more committed and less likely to default on the loan.

Furthermore, a larger down payment helps avoid being "upside down" on your loan, where you owe more than the car is worth. This situation can arise quickly due to vehicle depreciation. BECU, like other lenders, appreciates a healthy Loan-to-Value (LTV) ratio, which is the loan amount divided by the car’s value. A lower LTV (meaning a larger down payment) is always more attractive.

Aiming for a down payment of at least 10-20% of the vehicle’s purchase price is a strong strategy. Not only can it potentially lower your interest rate, but it also reduces your monthly payments and the total amount of interest you’ll pay over time.

4. Vehicle Type and Age: New vs. Used Car Rates

The type and age of the vehicle you’re financing also influence BECU car loan interest rates. New cars typically qualify for lower interest rates than used cars. This is due to several factors.

New vehicles generally have a higher resale value and are less likely to require immediate costly repairs, making them a more secure asset for the lender. Their predictable depreciation schedule also reduces risk. BECU often advertises specific, attractive rates for new car loans.

Used cars, on the other hand, usually come with slightly higher interest rates. This is because used vehicles carry more inherent risk; their value can be more volatile, they might have hidden mechanical issues, and their depreciation curve can be less predictable. The older the used car, the higher the perceived risk and potentially the interest rate.

Common mistakes to avoid are underestimating the impact of vehicle age on your interest rate. While an older used car might have a lower purchase price, the higher interest rate could diminish some of those upfront savings over the life of the loan. Always compare the total cost.

5. Debt-to-Income (DTI) Ratio: Your Financial Capacity

Your Debt-to-Income (DTI) ratio is another crucial metric BECU considers. It’s a percentage that compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover your loan payments.

Lenders use DTI to assess your ability to manage additional debt. A DTI ratio below 36% is generally considered excellent, while ratios above 43% might signal potential financial strain. BECU will look at your DTI to ensure that taking on a new car loan won’t overextend your financial capacity.

A low DTI ratio signifies that you are a responsible borrower with the financial bandwidth to comfortably make your car loan payments. This can contribute to BECU offering you a more favorable interest rate, as the risk of default is lower.

To improve your DTI, focus on reducing existing debt, such as credit card balances or personal loans, before applying for a car loan. Alternatively, increasing your income can also lower this ratio. Both strategies demonstrate greater financial stability to BECU.

6. Your Relationship with BECU: Member Advantages

While not always a published factor, your existing relationship with BECU can sometimes offer subtle advantages. As a credit union, BECU values long-term member relationships.

If you’ve been a long-standing member, have multiple accounts, use direct deposit, or have a history of responsible borrowing with BECU, this can implicitly strengthen your application. While it might not drastically alter a rate for a high-risk borrower, it can sometimes be the deciding factor in securing the very best rates for qualified individuals.

Think of it as a loyalty bonus. A strong, positive financial history with BECU demonstrates trust and reliability, which can be beneficial during the underwriting process. This personal touch is one of the distinct advantages of banking with a credit union.

For more insights into managing your finances and building a strong relationship with your financial institution, check out our article on .

Navigating BECU’s Car Loan Application Process

Understanding the factors influencing rates is one thing; knowing how to apply effectively is another. BECU’s application process is designed to be straightforward, but preparation is key.

Pre-Approval: Your Strategic Advantage

We highly recommend getting pre-approved for a car loan before you step onto a dealership lot. BECU offers a robust pre-approval process that can give you a clear understanding of:

- How much you can afford: BECU will provide you with a maximum loan amount.

- Your specific interest rate: You’ll know the exact rate you qualify for, based on your credit and other factors.

- Your monthly payment: This helps you budget accurately.

A BECU pre-approval acts as a powerful negotiating tool at the dealership. It shows the dealer you’re a serious buyer with financing already secured, preventing them from marking up the interest rate or pushing you into less favorable financing options. It gives you the power to focus on the car price, not the loan terms.

Required Documentation

When applying for a BECU car loan, whether online or in person, be prepared to provide standard financial documentation. This typically includes:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, W-2s, or tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and purchase price.

Having these documents ready will significantly expedite your application. BECU’s online application is streamlined, but having the information at hand is always helpful.

Strategies to Secure the Best BECU Car Loan Interest Rate

Now that you know what influences your rate, let’s discuss proactive steps you can take to ensure you get the lowest possible BECU car loan interest rate. These strategies can save you thousands of dollars over the life of your loan.

1. Improve Your Credit Score

This is perhaps the most impactful strategy. If your credit score isn’t in the excellent range, dedicating time to improve it before applying can yield substantial savings.

- Pay Bills on Time, Every Time: Payment history is the biggest factor in your credit score.

- Reduce Existing Debt: Lowering your credit card balances (credit utilization) can quickly boost your score.

- Check Your Credit Report for Errors: Dispute any inaccuracies that could be dragging your score down.

- Avoid Opening New Credit Accounts: Multiple hard inquiries in a short period can temporarily lower your score.

Even a small increase in your credit score can move you into a better rate tier with BECU.

2. Save for a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and the lender’s risk. Aim for 20% if possible, especially for new cars. For used cars, a higher percentage can be even more beneficial due to faster depreciation.

Saving diligently for a down payment not only potentially lowers your interest rate but also decreases your monthly payments and reduces the total interest paid over time. It’s a win-win strategy for your budget.

3. Choose a Shorter Loan Term (If Affordable)

While longer terms mean lower monthly payments, they almost always result in higher overall interest costs. If your budget allows, opt for the shortest loan term possible (e.g., 36 or 48 months).

This strategy minimizes the total interest you’ll pay and typically comes with a lower interest rate. Always balance monthly affordability with the total cost of the loan.

4. Consider Refinancing Your Current Car Loan with BECU

If you already have a car loan but your credit score has improved, market rates have dropped, or you initially got a less favorable rate, consider refinancing with BECU.

BECU often offers competitive refinancing rates, allowing you to potentially lower your interest rate, reduce your monthly payment, or shorten your loan term. This can be a smart move to save money on an existing car loan.

5. Shop Around (Even with BECU in Mind)

Even if BECU is your preferred lender, it’s wise to compare their offer with those from other reputable financial institutions. This ensures you’re getting the most competitive rate available.

Based on my experience, many borrowers overlook the power of pre-approval from multiple sources. Having competing offers in hand gives you leverage. If another lender offers a slightly lower rate, you can always ask BECU if they can match or beat it, especially as an existing member.

BECU Car Loan Rates: New vs. Used vs. Refinance

It’s important to recognize that BECU, like most lenders, structures its interest rates differently across various loan types. Here’s a general overview of how rates typically compare:

- New Car Loan Rates: These are almost always the lowest. Lenders prefer new vehicles because they are reliable, hold their value better initially, and pose less risk. BECU’s new car rates are highly competitive.

- Used Car Loan Rates: These are generally slightly higher than new car rates. The older the used vehicle, the higher the rate typically climbs due to increased risk and depreciation. BECU will have a tiered structure for used car rates based on vehicle age.

- Refinance Car Loan Rates: Refinance rates can vary widely depending on your current loan’s terms, your credit score at the time of refinancing, and prevailing market conditions. If your credit has improved since you first took out your loan, you might find BECU’s refinance rates to be very attractive.

Always check BECU’s official website or contact them directly for their current rates for each specific loan type. Rates are dynamic and can change based on market conditions.

Understanding BECU’s Current Rate Environment

BECU car loan interest rates, like all lending rates, are influenced by broader economic conditions. The Federal Reserve’s monetary policy, inflation rates, and the overall health of the economy all play a role in how BECU sets its rates. When the Federal Reserve raises its benchmark interest rate, it typically leads to higher borrowing costs across the board, including auto loans.

Conversely, periods of economic uncertainty or when the Federal Reserve lowers rates can lead to more favorable lending conditions. BECU constantly adjusts its offerings to remain competitive while reflecting the current economic climate. This means the rate you see today might be different from the rate next month.

For the most up-to-date information on BECU’s current auto loan interest rates, it is always best to visit their official auto loan rates page directly: . This ensures you are viewing the most accurate and real-time figures available.

Common Mistakes to Avoid When Applying for a BECU Car Loan

Even with all this knowledge, some common pitfalls can derail your efforts to secure the best BECU car loan. Being aware of these can save you headaches and money.

- Not Checking Your Credit Score: As mentioned, this is fundamental. Don’t go in blind; know where you stand.

- Applying to Too Many Lenders at Once: Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your score. Group your applications within a short window (e.g., 14-45 days) so credit bureaus count them as a single inquiry for rate shopping.

- Focusing Only on Monthly Payment: Dealers often try to "sell" you on a monthly payment, extending the loan term to make it seem affordable. Always look at the total cost of the loan, including interest, over its entire duration.

- Ignoring Additional Fees: While BECU is known for transparency, always read the fine print for any potential fees.

- Not Understanding the Loan Terms Fully: Before signing, ensure you comprehend every aspect of your loan agreement, including prepayment penalties (rare for BECU auto loans, but always check), late payment fees, and what happens in case of default.

Common mistakes we’ve observed include borrowers solely fixating on the monthly payment without considering the long-term financial implications. This often leads to longer loan terms and significantly more interest paid.

Pros and Cons of Choosing BECU for Your Car Loan

While BECU is a fantastic option for many, it’s important to weigh the specific advantages and potential drawbacks.

Pros of a BECU Car Loan:

- Competitive Interest Rates: As a credit union, BECU often offers rates that are among the best in the market, especially for well-qualified borrowers.

- Member-Centric Approach: They prioritize member financial well-being, which can translate to better service and more flexible options.

- Transparent Process: BECU is generally transparent with its loan terms and fees.

- Variety of Loan Options: They offer loans for new, used, and refinancing, with various terms.

- Financial Education Resources: BECU provides numerous resources to help members make informed financial decisions.

Cons of a BECU Car Loan:

- Membership Requirement: You must be a BECU member to apply, which, while easy, is an extra step.

- Limited Branch Network: While they have a strong online presence, their physical branch network is primarily concentrated in Washington state, which could be a drawback for out-of-state members who prefer in-person service.

- Not Always the Absolute Lowest Rate: While highly competitive, no single lender will always have the lowest rate for every individual in every scenario. Shopping around is always wise.

To learn more about the advantages of credit unions in general, read our guide on .

Conclusion: Drive Smarter with BECU

Navigating the world of car loans can feel daunting, but armed with a thorough understanding of BECU car loan interest rates and the factors that influence them, you are well-positioned to make an informed decision. BECU stands out as a strong contender in the auto lending market, offering competitive rates and a member-focused approach that can truly benefit borrowers.

Remember, securing the best rate isn’t just about finding the lowest number; it’s about being a prepared, informed borrower. By understanding your credit score, making a substantial down payment, choosing an appropriate loan term, and being proactive in your application process, you can significantly improve your chances of driving away with a fantastic deal.

Don’t just settle for the first offer. Do your homework, get pre-approved, and leverage your knowledge to negotiate the best possible BECU car loan interest rate. Your financial future, and your new car, will thank you for it. Start by visiting BECU’s official website today to explore their current offerings and begin your pre-approval process.