Demystifying Capital One Used Car Loan APR: Your Ultimate Guide to Securing the Best Rate

Demystifying Capital One Used Car Loan APR: Your Ultimate Guide to Securing the Best Rate Carloan.Guidemechanic.com

Buying a used car can be an incredibly exciting journey. It offers the thrill of a new-to-you vehicle without the steep depreciation of a brand-new model. However, for many, the excitement often gives way to apprehension when it comes to financing. Understanding the nuances of auto loans, especially the Annual Percentage Rate (APR), is crucial for making a financially sound decision.

Among the myriad of lenders, Capital One stands out as a prominent player in the auto loan market, offering solutions for a wide range of credit profiles. If you’re considering a used car and looking to finance it through Capital One, delving into their Used Car Loan APR is not just important – it’s essential. This comprehensive guide will equip you with the knowledge to navigate the complexities, understand the factors that influence your rate, and ultimately help you secure the best possible deal. Our goal is to empower you to make informed choices, saving you money and stress in the long run.

Demystifying Capital One Used Car Loan APR: Your Ultimate Guide to Securing the Best Rate

Understanding APR: More Than Just an Interest Rate

Before we dive specifically into Capital One, it’s vital to grasp what APR truly means. Many prospective car buyers mistakenly equate the interest rate with the total cost of their loan. While the interest rate is a significant component, the Annual Percentage Rate (APR) provides a much more accurate picture of the real cost of borrowing.

The interest rate is essentially the cost of borrowing the principal amount of money, expressed as a percentage. It determines how much extra you pay the lender for the privilege of using their funds. However, auto loans often come with additional fees and charges, such as origination fees, documentation fees, or processing fees.

The APR bundles these extra costs into a single, annualized percentage. This means it represents the total cost of your loan over a year, including both the interest and any mandatory lender fees. By looking at the APR, you get a standardized measure that allows for a much more accurate comparison between different loan offers. Focusing solely on the interest rate can lead to an incomplete understanding of your financial obligation, potentially costing you more in the end. Always compare APRs when shopping for an auto loan.

Factors Influencing Your Capital One Used Car Loan APR

Your Capital One Used Car Loan APR isn’t a one-size-fits-all figure. It’s a highly personalized rate determined by a complex interplay of several financial and vehicle-specific factors. Understanding these elements will help you anticipate your potential rate and take proactive steps to improve it.

1. Your Credit Score: The Cornerstone of Your Rate

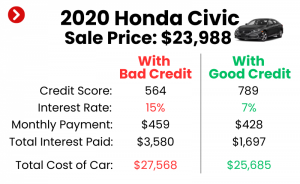

Without a doubt, your credit score is the single most influential factor in determining the APR you’ll be offered. Lenders, including Capital One, use your credit score as a primary indicator of your creditworthiness – essentially, how likely you are to repay the loan on time.

- Excellent Credit (780-850): Borrowers in this tier are considered low-risk and typically qualify for the lowest APRs available. They demonstrate a strong history of responsible borrowing and repayment.

- Good Credit (670-779): Most consumers fall into this category. You’ll likely receive competitive rates, though perhaps not the absolute lowest. Capital One is generally favorable to borrowers in this range.

- Fair Credit (580-669): This range indicates some past credit challenges, but you’re still considered lendable. You can expect higher APRs to compensate the lender for the increased risk. Capital One is known for working with borrowers in this category, offering a pathway to financing.

- Poor Credit (Below 580): Borrowers with scores in this range often face significant hurdles. Loans may be harder to obtain, and if approved, the APRs will be substantially higher. Capital One’s "Auto Navigator" tool is particularly helpful for those with challenging credit, as it provides pre-qualification without a hard credit inquiry.

Pro Tip from Us: Based on my experience, checking your credit report and score before you even start shopping for a car is non-negotiable. This allows you to identify any errors and understand where you stand. You can get free annual credit reports from AnnualCreditReport.com. For more detailed strategies on boosting your credit score, check out our article on .

2. The Loan Term: Length vs. Total Cost

The loan term, or the repayment period, also significantly impacts your APR and the total amount of interest you’ll pay. Common terms for used car loans range from 36 to 72 months, sometimes even longer.

- Shorter Loan Terms (e.g., 36-48 months): These typically come with lower APRs because the lender’s risk is reduced over a shorter period. While your monthly payments will be higher, you’ll pay significantly less interest over the life of the loan.

- Longer Loan Terms (e.g., 60-72+ months): These terms offer lower monthly payments, making the car seem more affordable upfront. However, lenders perceive longer terms as higher risk, often resulting in higher APRs. Crucially, you’ll pay much more in total interest over the life of the loan, potentially even owing more than the car is worth at certain points (being "upside down" on your loan).

Finding the sweet spot between an affordable monthly payment and a reasonable total cost is key. For used cars, aiming for a shorter term if your budget allows is often a wise financial decision.

3. Your Down Payment: Reducing Risk, Lowering Rates

A down payment is the initial amount of money you pay towards the car purchase, reducing the amount you need to borrow. The larger your down payment, the lower the risk for the lender.

- Impact on APR: Lenders, including Capital One, are more likely to offer a lower APR when you make a substantial down payment. This is because you have more equity in the vehicle from day one, signaling a greater commitment and reducing the lender’s potential loss if you default.

- Loan-to-Value (LTV) Ratio: Lenders look at your LTV ratio, which compares the loan amount to the car’s value. A lower LTV (meaning a higher down payment) is always more attractive. Aiming for at least 10-20% down on a used car is a strong strategy.

4. Vehicle Specifics: Age, Mileage, and Value

The characteristics of the used car itself play a role in the APR offered. Lenders consider the vehicle’s market value and its potential for depreciation.

- Age and Mileage: Older cars with higher mileage are generally seen as higher risk. They are more prone to mechanical issues, depreciate faster, and may be harder to repossess and resell if you default. Consequently, loans for such vehicles often carry higher APRs.

- Make and Model: Some car makes and models hold their value better than others. Lenders prefer financing vehicles with strong resale value. Capital One will assess the car’s value using industry guides like Kelley Blue Book (KBB) or NADAguides.

- Collateral: The car serves as collateral for the loan. The better the collateral (newer, lower mileage, higher value), the more favorable the loan terms typically are.

5. Your Debt-to-Income (DTI) Ratio: Can You Afford It?

Your Debt-to-Income (DTI) ratio is a crucial metric that lenders use to assess your ability to manage monthly payments. It compares your total monthly debt payments to your gross monthly income.

- Calculation: DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100.

- Lender’s Perspective: Capital One, like other lenders, wants to ensure that taking on a new car payment won’t overextend your finances. A lower DTI ratio indicates you have more disposable income to cover your debts, making you a less risky borrower.

- Ideal DTI: While requirements vary, a DTI ratio below 36% is often considered ideal. A higher DTI might lead to a higher APR or even loan denial, especially if your credit score is not stellar.

6. Co-signer: A Helping Hand (with Caveats)

If your credit score is fair or poor, or your DTI ratio is on the higher side, adding a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower APR.

- Benefits: A co-signer essentially guarantees the loan, taking on equal responsibility for repayment. This reduces the lender’s risk, which can translate to better terms for you.

- Implications: Both you and your co-signer are legally responsible for the loan. If you miss payments, it negatively impacts both your credit scores. A co-signer should be someone you trust implicitly and who understands the full implications of their commitment.

Why Capital One for Used Car Loans?

Capital One has established itself as a leading auto lender for several compelling reasons, particularly for used car financing. Their approach caters to a broad spectrum of borrowers, making them a popular choice.

Firstly, Capital One is renowned for its willingness to work with a diverse range of credit profiles. While many lenders primarily focus on prime and super-prime borrowers, Capital One extends its services to those with good, fair, and even some challenging credit histories. This inclusivity opens doors for many individuals who might otherwise struggle to secure financing.

Secondly, their innovative "Auto Navigator" tool is a game-changer for car buyers. This online platform allows you to get pre-qualified for a loan without impacting your credit score. It provides you with personalized loan terms, including an estimated APR, and lets you browse vehicles from participating dealerships that fall within your approved budget. This transparency and upfront information empower buyers to shop with confidence, knowing their financing is largely in place.

Finally, Capital One boasts a vast network of participating dealerships. This means that once you’re pre-qualified through Auto Navigator, you have a wide array of options to choose from, simplifying the car-buying process. Their strong market presence and user-friendly tools make them a go-to option for many looking to finance a used car.

Navigating Capital One’s Used Car Loan Process: Step-by-Step

Understanding the financing process can demystify the entire car-buying experience. Capital One has streamlined its approach to make it as user-friendly as possible.

Step 1: Pre-qualification with Auto Navigator (Soft Pull)

This is perhaps the most crucial first step when considering Capital One. Their Auto Navigator tool allows you to pre-qualify for an auto loan online.

- What it is: You provide some basic financial information, and Capital One gives you an estimated loan amount and APR. This is a "soft pull" on your credit report, meaning it won’t negatively affect your credit score.

- Why it’s crucial: Pre-qualification provides immense clarity. You’ll know your estimated budget, your potential APR, and which dealerships are part of Capital One’s network before you even step foot on a lot. This prevents the disappointment of falling in love with a car you can’t afford and gives you strong negotiation power.

- Benefits: You can confidently shop for a vehicle within your approved budget, compare potential monthly payments, and streamline the actual purchase process. Based on our extensive experience, this step is invaluable for saving time and reducing stress.

Step 2: Shopping for Your Car at a Participating Dealership

Once you have your pre-qualification offer, you can start shopping. Capital One partners with thousands of dealerships across the country.

- Using Your Offer: Utilize the Auto Navigator portal to search for vehicles at approved dealerships that fit your pre-qualified budget. This helps narrow down your options efficiently.

- Test Drives and Inspections: Even with financing in hand, take your time to thoroughly inspect the vehicle, test drive it, and consider having an independent mechanic perform a pre-purchase inspection. Remember, the car itself needs to be a good fit, not just the loan.

Step 3: Formal Application at the Dealership (Hard Pull)

When you’ve found the perfect car, you’ll proceed to the formal application process at the dealership.

- The Hard Inquiry: At this stage, the dealership will submit your information to Capital One (or other lenders) for a final loan approval. This involves a "hard pull" on your credit report, which will temporarily lower your credit score by a few points. This is normal and expected.

- Required Documents: Be prepared to provide identification (driver’s license), proof of income (pay stubs, bank statements), proof of residence (utility bill), and potentially trade-in details if applicable.

- Final Offer: Capital One will then provide a firm loan offer, which may be slightly different from your pre-qualification due to the specific vehicle, final negotiations, and the hard credit inquiry.

Step 4: Loan Finalization and Vehicle Purchase

Once approved, it’s time to finalize the paperwork.

- Review Everything: Carefully review all loan documents, especially the final APR, the total amount financed, the loan term, and any associated fees. Ensure everything matches what you discussed and agreed upon. Don’t be afraid to ask questions until you understand every detail.

- Sign and Drive: After signing, the loan is disbursed, and you drive off in your new-to-you used car!

Maximizing Your Chances for a Lower Capital One Used Car Loan APR

While some factors influencing your APR are fixed, many can be improved with strategic planning. Here’s how you can proactively work towards securing the most favorable Capital One Used Car Loan APR.

- Credit Score Improvement: This is paramount. Pay all your bills on time, keep your credit utilization low (ideally below 30%), and avoid opening new credit accounts right before applying for a car loan. Even small improvements can make a difference in your APR tier.

- Larger Down Payment: As discussed, a substantial down payment signals less risk to the lender. Aim for 10-20% of the car’s purchase price, or even more if feasible. This not only lowers your monthly payments but also reduces the total interest paid over the life of the loan.

- Shorter Loan Term: While it means higher monthly payments, opting for the shortest loan term you can comfortably afford will almost always result in a lower APR and significantly less interest paid overall. Balance affordability with the total cost.

- Shop Around (But Be Smart): Even if Capital One is your preferred lender, it’s wise to get quotes from other banks, credit unions, and online lenders. However, do this within a focused "rate shopping" window (typically 14-45 days) to ensure multiple hard inquiries are treated as a single inquiry by credit bureaus, minimizing impact on your score.

- Consider a Co-signer Wisely: If your credit isn’t ideal, and you have a trusted friend or family member with excellent credit willing to co-sign, this can be a powerful lever for a lower APR. Just ensure all parties understand the full responsibility involved.

- Negotiate the Car Price: Remember that the car price is separate from the loan terms. A lower purchase price means you need to borrow less, which can indirectly lead to a better overall deal and potentially a lower APR on a smaller principal amount.

Common Mistakes to Avoid When Applying for a Capital One Used Car Loan

Even experienced buyers can fall into common traps. Based on our insights, here are critical mistakes to steer clear of:

- Not Checking Your Credit Score First: This is perhaps the most significant oversight. Going into the process blind leaves you vulnerable and unable to assess the fairness of offers.

- Focusing Only on Monthly Payments: Dealerships often try to "sell" you on a low monthly payment. While important, this can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan and the APR.

- Skipping Pre-qualification: Neglecting Capital One’s Auto Navigator or similar pre-qualification tools from other lenders means you’re shopping without a clear budget or estimated rate, putting you at a disadvantage during negotiations.

- Accepting the First Offer: Whether it’s the dealership’s financing or your initial Capital One offer, always compare it with other options. Even a fraction of a percentage point difference in APR can save you hundreds, if not thousands, over the life of the loan.

- Ignoring the Fine Print: Every clause in your loan agreement matters. Understand prepayment penalties, late fees, and all other terms and conditions before signing.

- Buying More Car Than You Can Afford: It’s easy to get carried away by emotions. Stick to your budget, considering not just the car payment but also insurance, maintenance, and fuel costs. Overextending yourself can lead to financial strain.

Refinancing Your Capital One Used Car Loan: Is It an Option?

Even after you’ve secured a Capital One Used Car Loan, your financial journey doesn’t necessarily end there. Refinancing can be a smart move in certain situations.

-

When Refinancing Makes Sense:

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you might qualify for a much lower APR.

- Lower Interest Rates: General market interest rates may have dropped, making it possible to get a better deal.

- Financial Changes: If your income has increased, or your debt-to-income ratio has improved, you might qualify for more favorable terms.

- Shorten Loan Term: You might want to refinance to a shorter term to pay off the loan faster, even if the monthly payment is higher, thereby reducing total interest.

- Remove a Co-signer: If your credit has improved, you might be able to refinance the loan in your name alone, releasing your co-signer from their obligation.

-

How to Approach Refinancing: You can apply for refinancing directly with Capital One or explore options with other lenders. Shop around and compare APRs, fees, and terms just as you did with your initial loan. Capital One’s pre-qualification process for refinancing can also be a useful starting point.

-

Benefits: Refinancing can lead to lower monthly payments, a lower overall cost of the loan, or a quicker path to debt freedom. It’s always worth exploring if your financial circumstances have changed for the better since your original purchase.

Pro Tips from Our Experience

Having navigated countless auto loan scenarios, we’ve gathered some insights that can truly make a difference in your Capital One Used Car Loan experience:

- "Based on my experience, proactive credit management is key." Don’t wait until you need a loan to think about your credit score. Building and maintaining good credit is an ongoing process that pays dividends across all financial endeavors.

- "Don’t just focus on the car, focus on the entire financial package." The car is only one part of the equation. The loan terms, APR, and total cost of ownership are equally, if not more, important for your financial health.

- "Always get multiple quotes, even if you love Capital One." While Capital One offers excellent tools and rates, competition is healthy. Comparing their final offer against at least two other lenders ensures you’re getting the most competitive rate available to you.

- "The dealership finance office isn’t your only option." While convenient, dealerships often mark up interest rates. Coming in with pre-approved financing from Capital One (or another lender) gives you leverage and often results in a better deal.

- "Understand the total cost, not just the monthly payment." A slightly higher monthly payment on a shorter term loan will almost always save you significant money in the long run by reducing the total interest paid.

Conclusion

Securing a Capital One Used Car Loan at a favorable APR is entirely achievable when you approach the process with knowledge and strategic planning. Understanding what APR truly represents, knowing the factors that influence your rate, and leveraging Capital One’s user-friendly tools like Auto Navigator are your best defenses against overpaying.

By diligently managing your credit, making a strong down payment, carefully considering your loan term, and avoiding common pitfalls, you empower yourself to make informed decisions. Remember, the goal isn’t just to get approved for a loan, but to secure the best possible terms for your financial situation.

Your used car journey should be exciting and financially responsible. Armed with the insights from this comprehensive guide, you are now well-prepared to navigate the complexities of Capital One Used Car Loan APRs and drive away with confidence. Start your Capital One Auto Navigator journey today and take control of your used car financing! Curious about other financing options? Read our comprehensive guide on .