Demystifying Car Loan Terms: How Many Months Is A Car Loan Really?

Demystifying Car Loan Terms: How Many Months Is A Car Loan Really? Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, but the financial mechanics behind it, especially understanding car loan terms, can often feel like navigating a maze. One of the most common questions people ask is, "How many months is a car loan?" The answer isn’t a simple fixed number; it’s a spectrum of possibilities, each with its own set of financial implications.

As an expert blogger and professional SEO content writer, I understand the importance of making informed decisions when it comes to significant purchases. This comprehensive guide is designed to shed light on the typical car loan lengths, the factors that influence them, and how you can choose the best term for your financial situation. Our ultimate goal is to empower you to drive off the lot not just with a new car, but with a smart, sustainable financial plan.

Demystifying Car Loan Terms: How Many Months Is A Car Loan Really?

Understanding the Foundation: What Exactly is a Car Loan Term?

Before diving into specific lengths, let’s clarify what a "car loan term" actually means. In simple terms, the car loan term refers to the duration, measured in months, over which you agree to repay the money you borrowed to purchase your vehicle. This period dictates the number of payments you’ll make and significantly influences the size of your monthly payment and the total interest you’ll pay over the life of the loan.

Think of it as the repayment schedule. A shorter term means fewer payments but larger individual amounts, while a longer term spreads the cost over more months, resulting in smaller individual payments. However, as we’ll explore, the seemingly attractive lower monthly payment of a longer term often comes with a higher total cost due due to accumulated interest.

The Most Common Car Loan Lengths: A Detailed Look

When you walk into a dealership or apply for an auto loan, you’ll encounter a range of standard loan terms. While there’s no universal "right" answer for everyone, understanding the typical options is your first step toward making a sound decision. Based on my experience in the automotive finance industry, these are the terms you’ll most frequently encounter:

The 60-Month (5-Year) Car Loan: The Sweet Spot for Many

The 60-month car loan, or a five-year term, has long been considered the industry standard and a popular choice for many car buyers. It strikes a balance between manageable monthly payments and a reasonable repayment period. This term is often seen as a middle ground, making it accessible for a wide range of budgets.

For many, a 60-month loan offers a comfortable monthly payment without stretching the repayment period excessively. It allows borrowers to build equity in their vehicle at a decent pace, often reaching a point where the car’s value exceeds the loan balance before major depreciation sets in. This term is particularly attractive for those who want to pay off their car relatively quickly without feeling overwhelmed by very high monthly installments.

The 72-Month (6-Year) Car Loan: Growing in Popularity

In recent years, the 72-month car loan has gained significant traction, especially as vehicle prices continue to rise. This six-year term offers even lower monthly payments than a 60-month loan, making more expensive vehicles seem more affordable within a buyer’s monthly budget. It’s an attractive option for those who prioritize a lower immediate financial outlay each month.

However, the allure of lower monthly payments comes with a trade-off. Over a 72-month period, you will undoubtedly pay more in total interest compared to a shorter loan term, even with the same interest rate. Furthermore, extending the loan to six years means you’ll be making payments for a longer duration, potentially holding onto the car for a significant portion of its useful life while still owing money on it. This term is often chosen by those who need to keep their monthly expenses down to afford a newer or more feature-rich vehicle.

The 84-Month (7-Year) Car Loan and Beyond: Proceed with Caution

The longest car loan terms, stretching to 84 months (seven years) or even 96 months (eight years), have become increasingly available. These extended terms offer the lowest possible monthly payments, which can make luxury vehicles or high-end SUVs appear surprisingly affordable on a month-to-month basis. For some, these longer terms are the only way to fit a desired vehicle into their tight monthly budget.

From our perspective as financial experts, approaching an 84-month or longer car loan requires extreme caution. While the low monthly payment is appealing, the total interest paid over such an extended period can be astronomical, significantly increasing the overall cost of the vehicle. Moreover, the risk of "negative equity" – owing more on the car than it’s worth – becomes much higher and lasts for a longer duration. This is a common mistake to avoid: focusing solely on the monthly payment without considering the total cost and the depreciation of the asset.

Shorter Terms (24, 36, 48 Months): The Financially Savvy Choice

On the other end of the spectrum are shorter car loan terms, typically 24, 36, or 48 months (two, three, or four years). These terms are less common simply because they demand significantly higher monthly payments. However, for those who can comfortably afford them, shorter terms offer substantial financial advantages.

The primary benefit of a short-term loan is the dramatic reduction in the total amount of interest paid over the life of the loan. You build equity in your vehicle much faster, and you’ll be debt-free sooner. This frees up your monthly budget for other financial goals or future vehicle purchases. Pro tips from us: if your budget allows, always lean towards the shortest loan term you can manage. It’s a testament to sound financial planning and can save you thousands in interest.

Factors Influencing Your Car Loan Term and Approval

The specific car loan term you’re offered, and indeed your ability to secure financing at all, is not arbitrary. Several key factors play a crucial role in the lender’s decision-making process. Understanding these elements can help you better prepare and potentially secure more favorable terms.

Your Credit Score

Your credit score is arguably the most significant factor. Lenders use it as a snapshot of your financial reliability. A higher credit score (generally 700+) indicates a lower risk, making you eligible for better interest rates and often more flexible loan terms. Conversely, a lower credit score might lead to higher interest rates and could limit your options to shorter terms or require a larger down payment.

Based on my experience, individuals with excellent credit often have the widest array of loan terms to choose from, as lenders are more confident in their ability to repay. This financial leverage is a direct result of responsible credit management.

The Down Payment

The amount of money you put down upfront on your car purchase directly impacts the amount you need to borrow. A larger down payment reduces your loan principal, which in turn can lead to lower monthly payments or allow you to choose a shorter loan term without significantly increasing your monthly outlay. It also signals financial stability to lenders, potentially opening doors to better rates and terms.

A substantial down payment also helps mitigate the risk of negative equity, especially with new cars that depreciate quickly. This is a smart financial move that many overlook when fixated on the lowest monthly payment.

The Interest Rate (APR)

The Annual Percentage Rate (APR) is the true cost of borrowing money, encompassing the interest rate and any additional fees. A lower APR means you’ll pay less in total interest over the life of the loan. The APR is heavily influenced by your credit score, the current market conditions, and the specific lender. Even a seemingly small difference in APR can translate into hundreds or thousands of dollars saved (or spent) over the full loan term.

It’s crucial to compare APRs from multiple lenders before committing to a loan. Don’t just look at the monthly payment; calculate the total cost over different terms with varying APRs.

Vehicle Age and Type

Lenders often view new cars as less risky than used cars, as new vehicles typically come with warranties and are less likely to require immediate expensive repairs. This can sometimes translate into more favorable loan terms, including longer options, for new car purchases. For used cars, especially older models, lenders might be more hesitant to offer very long loan terms due to concerns about the vehicle’s remaining lifespan and potential for costly issues.

The type of vehicle can also play a role. Some lenders might offer special financing for specific makes or models, while others might have stricter criteria for high-performance or luxury vehicles.

Your Monthly Budget and Financial Goals

Ultimately, the best car loan term is one that aligns with your personal financial situation and goals. Your monthly budget dictates how much you can comfortably afford to pay each month without straining your finances. Beyond that, consider your long-term financial objectives. Are you saving for a house, retirement, or another major purchase? A shorter car loan term frees up your budget sooner, while a longer term ties up your cash flow for an extended period.

Pro tips from us: always create a realistic budget that accounts for not just the car payment, but also insurance, fuel, maintenance, and unexpected repairs. Don’t let the desire for a specific car push you into an unsustainable loan term.

The Pros and Cons of Different Loan Lengths: A Head-to-Head Comparison

Choosing between a short-term and a long-term car loan involves weighing various financial advantages and disadvantages. There’s no one-size-fits-all answer, so understanding these trade-offs is crucial for making an informed decision.

Short-Term Loans (e.g., 24, 36, 48 Months)

Pros:

- Less Total Interest Paid: This is the biggest advantage. By paying off your loan quicker, you spend significantly less on interest over the life of the loan. This can amount to thousands of dollars in savings.

- Faster Equity Build-Up: You gain equity in your vehicle much faster, meaning the amount you own outright increases more quickly. This is beneficial if you plan to trade in or sell the car in a few years.

- Quicker Debt Freedom: You’ll be free of car payments sooner, freeing up your monthly budget for other financial goals, investments, or a future vehicle purchase.

- Reduced Risk of Negative Equity: It’s less likely you’ll owe more than the car is worth, especially as vehicles depreciate rapidly in the first few years.

Cons:

- Higher Monthly Payments: The most significant drawback is the higher monthly installment, which requires a larger portion of your budget each month. This might not be feasible for everyone.

- Less Budget Flexibility: Higher payments leave less room in your budget for unexpected expenses or other financial priorities.

Long-Term Loans (e.g., 72, 84 Months)

Pros:

- Lower Monthly Payments: This is the primary appeal. Spreading the cost over more months significantly reduces the individual monthly payment, making more expensive vehicles seem affordable.

- Greater Budget Flexibility (Initially): The lower payment might free up some cash flow for other immediate needs or desires.

Cons:

- Much More Total Interest Paid: This is the biggest financial penalty. Over an extended term, the accumulated interest can add a substantial amount to the overall cost of your vehicle, often thousands more than a shorter term.

- Higher Risk of Negative Equity: Vehicles depreciate rapidly. With a long-term loan, you’re highly likely to be "upside down" on your loan (owe more than the car is worth) for a significant portion of the loan term. This is particularly problematic if your car is totaled or stolen, as your insurance payout might not cover the outstanding loan balance. This is why Gap Insurance is crucial for longer terms.

- Longer Commitment: You’ll be making payments for a much longer period, potentially outliving the car’s warranty or even its reliable lifespan. This means you could be paying for a car that requires significant maintenance or that you no longer even own.

- Slower Equity Build-Up: It takes much longer to build any meaningful equity in the vehicle, reducing your flexibility if you want to trade it in sooner.

Pro Tips for Choosing the Right Car Loan Term

Making the right decision about your car loan term can save you a substantial amount of money and prevent financial stress down the road. Here are some expert tips to guide you:

- Analyze Your Budget Realistically: Don’t just look at the car payment in isolation. Factor in all car-related expenses: insurance, fuel, maintenance, and potential repairs. Can you comfortably afford the monthly payment of a shorter term without stretching your finances thin? Our experience shows that many people overestimate what they can afford.

- Focus on the Total Cost, Not Just the Monthly Payment: This is perhaps the most critical piece of advice. While a lower monthly payment is attractive, always calculate the total amount you will pay over the life of the loan, including all interest. Use online car loan calculators to compare different terms and interest rates.

- Consider Vehicle Depreciation: New cars lose a significant portion of their value in the first few years. A shorter loan term helps you build equity faster, keeping you ahead of depreciation. With longer terms, you often owe more than the car is worth for a considerable period.

- Don’t Stretch Your Budget Too Thin: Avoid taking on a car payment that consumes too large a portion of your monthly income. A general rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income.

- Explore Refinancing Options: If you initially took out a long-term loan due to financial constraints or a lower credit score, you might be able to refinance to a shorter term or a lower interest rate once your financial situation improves or your credit score increases. This can save you money over the remaining loan period.

- Common Mistakes to Avoid Are:

- "Payment Shopping": Only focusing on the lowest monthly payment without considering the total cost or the loan term.

- Ignoring Interest Rates: Not comparing APRs from different lenders. Even a half-point difference can save you hundreds.

- Forgetting About Gap Insurance: Especially with longer terms and minimal down payments, Gap Insurance is vital. It covers the difference between what you owe on your car and its actual cash value if it’s totaled or stolen. Without it, you could still owe thousands on a car you no longer have.

- Overlooking Prepayment Penalties: While rare in standard auto loans, always check your loan agreement for any fees associated with paying off your loan early. Most lenders do not have them, but it’s good practice to verify.

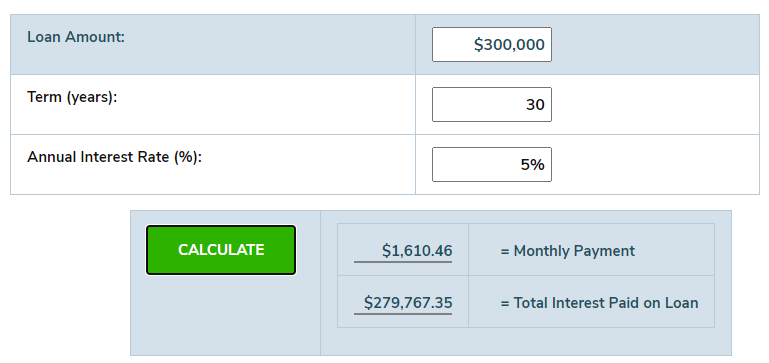

Leveraging a Car Loan Calculator

One of the most powerful tools at your disposal when determining the ideal car loan term is an online car loan calculator. These tools allow you to input different loan amounts, interest rates (APRs), and loan terms, instantly showing you the estimated monthly payment and the total interest you’ll pay.

By experimenting with various scenarios, you can clearly visualize the financial impact of choosing a 60-month loan versus a 72-month or even an 84-month option. This hands-on approach helps you make an evidence-based decision rather than just guessing. You can easily find these calculators on most bank websites, credit union sites, or independent financial planning sites.

Conclusion: Making Your Informed Decision

The question of "how many months is a car loan" doesn’t have a single, definitive answer because the ideal loan term is deeply personal, reflecting your financial health, monthly budget, and long-term goals. While standard terms like 60 or 72 months are prevalent, it’s crucial to look beyond the surface and understand the full financial implications of each option.

Remember, a shorter loan term generally means higher monthly payments but significantly less total interest paid, leading to quicker debt freedom. Conversely, a longer term offers lower monthly payments but comes with a higher overall cost and an increased risk of negative equity. Our advice is always to opt for the shortest loan term you can comfortably afford, considering your entire financial picture.

By taking the time to research, compare options, and use available tools like loan calculators, you can make a car financing decision that not only gets you behind the wheel of your desired vehicle but also aligns perfectly with your financial well-being. Drive smart, not just fast! If you’re interested in diving deeper into related topics, check out our articles on or .