Demystifying the Credit Score Minimum For Car Loan: Your Ultimate Guide to Auto Financing

Demystifying the Credit Score Minimum For Car Loan: Your Ultimate Guide to Auto Financing Carloan.Guidemechanic.com

Navigating the world of car loans can feel like deciphering a complex code, and at the heart of that code lies your credit score. Many aspiring car owners often wonder, "What is the credit score minimum for a car loan?" It’s a crucial question, and the answer isn’t always a simple number. Instead, it’s a dynamic range influenced by various factors, all of which we’ll unpack in this comprehensive guide.

Securing favorable auto financing isn’t just about getting approved; it’s about securing the best possible terms for your financial health. A higher credit score can translate into significantly lower interest rates, saving you thousands of dollars over the life of your loan. This article will equip you with the knowledge to understand your credit, improve your standing, and approach the car buying process with confidence, no matter your current credit situation.

Demystifying the Credit Score Minimum For Car Loan: Your Ultimate Guide to Auto Financing

Understanding Credit Scores and Their Impact on Car Loans

Before diving into specific score ranges, let’s establish a foundational understanding of what a credit score is and why it holds so much weight with lenders. Your credit score is essentially a three-digit numerical representation of your creditworthiness. It tells lenders how likely you are to repay borrowed money based on your past financial behavior.

What is a Credit Score? FICO vs. VantageScore

When we talk about credit scores, we’re typically referring to either a FICO Score or a VantageScore. While both models aim to assess your credit risk, they use slightly different methodologies and scoring ranges.

FICO Scores, developed by the Fair Isaac Corporation, are the most widely used scores by lenders, with scores ranging from 300 to 850. VantageScore, a newer model developed by the three major credit bureaus (Experian, Equifax, and TransUnion), also uses a 300-850 range and is gaining popularity. Both scores consider similar factors like payment history, amounts owed, length of credit history, new credit, and credit mix.

Why Lenders Care So Much About Your Credit Score

Lenders use your credit score as a primary tool to assess risk. From their perspective, a higher score indicates a lower risk of default, meaning you’re more likely to make your payments on time. Conversely, a lower score suggests a higher risk, which lenders compensate for by charging higher interest rates or requiring more stringent loan terms.

Based on my experience working with countless individuals seeking auto financing, understanding this risk assessment is paramount. Lenders aren’t just looking at a number; they’re trying to predict your future behavior based on your past.

The Direct Impact on Interest Rates and Loan Terms

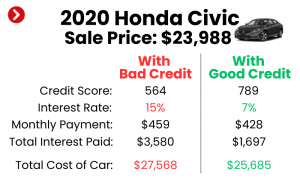

Your credit score directly influences the interest rate you’ll be offered on a car loan. Even a small difference in your score can lead to significant savings or additional costs. For example, a person with an excellent credit score might qualify for an interest rate of 3-5%, while someone with a fair credit score might see rates jump to 8-12% or even higher.

Over a typical five-year car loan, this difference can translate into thousands of dollars in extra interest payments. Furthermore, your credit score can impact the loan terms available, such as the maximum loan amount, the length of the repayment period, and whether you’ll need a co-signer or a larger down payment. The better your credit, the more flexibility and favorable terms you’ll generally receive.

The "Minimum" Credit Score Myth vs. Reality

The idea of a single, universal credit score minimum for a car loan is largely a myth. While lenders do have internal guidelines, there isn’t one magic number that guarantees approval or denial across the board. Instead, it’s a spectrum, with different credit tiers offering varying access to financing and interest rates.

Is There a Hard Minimum? No, It’s a Range

No, there isn’t a hard "minimum" credit score that applies to every lender or every car loan. Different lenders have different risk appetites and lending criteria. Some specialized lenders cater specifically to individuals with lower credit scores, while prime lenders focus on those with excellent credit.

What’s considered "acceptable" can also vary depending on the current economic climate, the type of vehicle you’re buying, and the amount you wish to borrow. It’s more accurate to think of credit scores in categories rather than a strict cut-off point.

Breaking Down Credit Score Tiers for Auto Loans

To better understand what to expect, let’s look at the general credit score tiers commonly used in auto lending. These categories provide a clearer picture of the financing landscape.

- Excellent Credit (781-850): Borrowers in this range are considered prime candidates. They typically qualify for the lowest interest rates, the most flexible terms, and require little to no down payment. Lenders view them as very low risk.

- Good Credit (661-780): This is still a very strong credit tier. Individuals here will receive competitive interest rates and favorable loan terms, though perhaps not the absolute lowest available to excellent credit holders. Approval is generally straightforward.

- Fair Credit (601-660): Borrowers in this category might find approval, but often with higher interest rates than those with good or excellent credit. A down payment might be more frequently requested, and loan terms could be less flexible. This is often the "tipping point" where a credit score minimum for car loan starts to become a real concern.

- Subprime Credit (501-600): This tier presents more challenges. Getting a car loan is still possible, but it will come with significantly higher interest rates, often in the double digits. Lenders might require a substantial down payment, a co-signer, or shorter loan terms to mitigate their risk.

- Deep Subprime Credit (300-500): Financing a car with a score in this range is very difficult through traditional lenders. Options might be limited to specialized subprime lenders, buy-here-pay-here dealerships, or secured loans, all of which come with extremely high interest rates and less favorable terms. The focus here is often on rebuilding credit.

Pro tips from us: Even if your score falls into the "Fair" or "Subprime" categories, don’t give up hope. Understanding these tiers simply helps you set realistic expectations and strategize your approach.

What Lenders Look At Beyond Your Credit Score

While your credit score is undeniably a major factor, it’s not the only piece of the puzzle. Lenders consider several other aspects of your financial profile to make a comprehensive lending decision. These additional factors can sometimes help offset a less-than-perfect credit score or, conversely, cause issues even with good credit.

Income and Employment Stability

Lenders want to ensure you have a steady and sufficient income to comfortably make your monthly car payments. They typically look for consistent employment history, often requiring pay stubs, tax returns, or employment verification. A stable job history demonstrates reliability and the ability to maintain a regular income stream.

Even with an excellent credit score, a lack of verifiable income or a history of frequent job changes could raise a red flag. Lenders want assurance that you can meet your financial obligations consistently over the loan’s term.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another critical metric. It compares your total monthly debt payments (including the potential new car loan) to your gross monthly income. Lenders use this to assess your ability to take on additional debt without becoming overextended.

A lower DTI ratio indicates that you have more disposable income available to cover your new car payment, making you a less risky borrower. Generally, lenders prefer a DTI ratio below 36%, though some may go higher for well-qualified applicants.

Down Payment

Making a significant down payment can dramatically improve your chances of approval, especially if your credit score is on the lower side. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment to the purchase and your ability to save.

Common mistakes to avoid are underestimating the power of a down payment. Even 10-20% of the car’s value can make a substantial difference in loan terms and interest rates, particularly when trying to overcome a borderline credit score minimum for car loan situation.

Loan-to-Value (LTV) Ratio

The loan-to-value (LTV) ratio compares the loan amount to the car’s actual value. If you’re borrowing more than the car is worth (e.g., rolling negative equity from a trade-in into the new loan), your LTV will be high. A high LTV increases the lender’s risk because if you default, they might not recover the full loan amount by repossessing and selling the vehicle.

A lower LTV, often achieved with a good down payment, makes your loan more attractive to lenders. It signals that there’s less risk for them if they need to repossess the vehicle.

Credit History Length and Types

Lenders also examine the length of your credit history and the types of credit you’ve managed. A longer history with a mix of different credit types (e.g., credit cards, student loans, previous car loans, mortgage) demonstrates your ability to handle various financial responsibilities over time.

A short credit history, even with perfect payments, can sometimes be viewed as a higher risk simply because there isn’t enough data to fully assess your long-term behavior. New credit accounts opened recently can also be a red flag, indicating you might be taking on too much debt too quickly.

Strategies for Securing a Car Loan with Different Credit Scores

Your approach to securing a car loan should be tailored to your specific credit profile. What works for someone with excellent credit will be very different from the strategy for someone with a low score.

Excellent/Good Credit: Leverage Your Advantage

If you have an excellent (781-850) or good (661-780) credit score, you’re in a strong negotiating position. Your primary goal should be to secure the absolute lowest interest rate and most favorable terms available.

- Shop Around Aggressively: Don’t just accept the first offer. Get pre-approved from multiple banks, credit unions, and online lenders. Compare their rates and terms meticulously.

- Negotiate: Use competing offers to negotiate with the dealership’s finance department. They may be willing to match or beat external offers to keep your business.

- Keep Loan Terms Short: While you might qualify for longer terms, opt for a shorter loan (e.g., 36-48 months) if the monthly payments are manageable. This reduces the total interest paid significantly.

- Consider a Small Down Payment (or None): With excellent credit, you might not need a large down payment to get a great rate. However, a down payment still reduces your total interest and lowers your monthly payments.

Based on my experience, individuals with top-tier credit often leave money on the table by not fully leveraging their strong financial standing. Pre-approval is your most powerful tool.

Fair Credit: Strategies for Improving Your Chances

If your credit score falls into the fair range (601-660), you’ll need a more strategic approach to avoid excessively high interest rates. The credit score minimum for car loan becomes more relevant here, requiring proactive steps.

- Make a Substantial Down Payment: A larger down payment (e.g., 20% or more) can significantly reduce the lender’s risk and potentially help you qualify for a better rate.

- Consider a Co-signer: If you have a trusted friend or family member with excellent credit, asking them to co-sign the loan can drastically improve your chances of approval and secure a lower interest rate. Be aware that the co-signer is equally responsible for the debt.

- Explore Credit Unions: Credit unions are often more willing to work with members who have fair credit compared to traditional banks, as they are member-owned and community-focused.

- Look for Dealer Incentives: Sometimes, manufacturers offer special financing deals, even for those with fair credit, especially on new vehicles.

Bad Credit: Realistic Expectations and Alternatives

Securing a car loan with bad credit (500-600) or deep subprime credit (300-500) is challenging but not impossible. You must set realistic expectations regarding interest rates and loan terms.

- Focus on Subprime Lenders: These lenders specialize in working with high-risk borrowers. Be prepared for very high interest rates and strict terms.

- Consider a Secured Car Loan: Some lenders offer secured loans where the car itself acts as collateral. This can sometimes lead to approval, but the terms will still reflect the higher risk.

- Buy-Here-Pay-Here Dealerships: These dealerships offer in-house financing, often without a credit check. However, their interest rates are typically exorbitant, and they may have very unfavorable terms. Use these as a last resort and with extreme caution.

- Save a Large Down Payment: This is even more crucial with bad credit. The more you put down, the less you need to borrow, reducing the risk for the lender.

- Rebuild Your Credit First (if possible): If you can wait, taking steps to improve your credit score before applying will save you significant money in the long run.

Improving Your Credit Score Before You Apply

The best strategy, regardless of your current score, is to improve it. Even a small increase can make a difference in your auto loan offer.

- Check Your Credit Report for Errors: Get free copies of your credit report from AnnualCreditReport.com. Dispute any inaccuracies immediately. Errors are common mistakes to avoid that can unnecessarily drag down your score.

- Pay All Bills on Time: Payment history is the most significant factor in your credit score. Set up reminders or automatic payments to ensure you never miss a due date.

- Reduce Your Credit Utilization: Keep your credit card balances low, ideally below 30% of your available credit. High utilization can significantly lower your score.

- Avoid Opening New Credit Accounts: Resist the urge to open new credit cards or loans in the months leading up to your car loan application. New credit inquiries can temporarily ding your score.

- Address Delinquent Accounts: If you have any accounts in collections or past due, try to resolve them. Even settling accounts can be better than leaving them unresolved.

For more detailed guidance, consider checking out our article on How to Improve Your Credit Score Fast (internal link placeholder). Understanding these fundamental credit-building steps is crucial for anyone aiming to meet or exceed the credit score minimum for car loan requirements.

The Application Process: Navigating Your Options

Once you’ve assessed your credit and prepared your finances, it’s time to navigate the application process. Knowing your options can empower you to make the best choice.

Dealership Financing vs. Banks/Credit Unions

You generally have two main avenues for securing a car loan:

- Banks and Credit Unions: These traditional financial institutions often offer competitive interest rates, especially for those with good credit. They typically provide pre-approval, which allows you to shop for a car knowing exactly how much you can spend and what your interest rate will be.

- Dealership Financing: Dealerships act as intermediaries, connecting you with various lenders (banks, credit unions, and their own captive finance companies). This can be convenient, offering a "one-stop shop" experience. However, their rates might sometimes be marked up, or they may push certain financing products.

The Power of Pre-Approval

Getting pre-approved for a car loan from a bank or credit union before you even step foot on a dealership lot is one of the most powerful strategies. Pre-approval gives you:

- Negotiating Power: You know your maximum loan amount and interest rate, allowing you to focus on the car price, not the monthly payment.

- Budget Clarity: You won’t fall in love with a car you can’t afford.

- Time Savings: Streamlines the financing process at the dealership.

With a pre-approval in hand, you effectively become a cash buyer, which can give you leverage in negotiating the vehicle’s price.

Understanding Loan Offers

When you receive loan offers, don’t just look at the monthly payment. Scrutinize the following:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and certain fees. Always compare APRs, not just interest rates.

- Loan Term: A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but more interest paid over time.

- Total Cost of the Loan: Calculate the total amount you’ll pay back (principal + interest).

- Any Hidden Fees: Read the fine print for origination fees, prepayment penalties, or other charges.

For additional guidance on smart car buying, consider resources like the Consumer Financial Protection Bureau’s Buying a Car guide (external link). Understanding these elements will ensure you choose the best financing option available to you. You might also find our article on Understanding Auto Loan Interest Rates helpful for a deeper dive into how rates are determined (internal link placeholder).

Conclusion

The journey to securing a car loan doesn’t have to be daunting. While there isn’t a single, fixed credit score minimum for a car loan, understanding the nuances of credit tiers, lender expectations, and strategic planning can make all the difference. Your credit score is a powerful tool that dictates the cost of your borrowing, but it’s not the only factor. Income, down payment, and even your negotiation skills play significant roles.

By taking the time to understand your credit, improve your financial standing, and explore your financing options thoroughly, you empower yourself to make informed decisions. Whether you’re aiming for the lowest interest rate with excellent credit or working to rebuild your credit while securing essential transportation, a well-planned approach will always lead to a more favorable outcome. Start today by checking your credit report and setting yourself on the path to financial success and your next vehicle.