Demystifying Your $10,000 Car Loan: What Your Monthly Payment Really Looks Like

Demystifying Your $10,000 Car Loan: What Your Monthly Payment Really Looks Like Carloan.Guidemechanic.com

Buying a car is a significant financial decision, and for many, it involves taking out a loan. The prospect of securing a $10,000 car loan can feel manageable, but the burning question that often arises is: "How much would a $10,000 car loan be a month?" It’s a critical query that influences your budget, lifestyle, and overall financial health.

The truth is, there isn’t a single, straightforward answer. Your monthly payment on a $10,000 car loan is a dynamic figure, shaped by a confluence of factors ranging from economic conditions to your personal financial standing. As an expert in personal finance and automotive lending, I’ve guided countless individuals through this maze, and I can tell you that understanding these variables is paramount to making an informed decision. This comprehensive guide will break down every element, provide practical examples, and equip you with the knowledge to confidently navigate your car loan journey.

Demystifying Your $10,000 Car Loan: What Your Monthly Payment Really Looks Like

The Core Question: How Much Would a $10,000 Car Loan Be a Month? (And Why It Varies)

When you borrow $10,000 to purchase a car, your monthly payment isn’t simply $10,000 divided by the number of months you plan to repay it. That calculation would ignore the fundamental cost of borrowing money: interest. Lenders charge interest as a fee for letting you use their capital, and this interest significantly impacts your monthly outlay and the total cost of the loan.

Think of your monthly payment as a puzzle with several interconnected pieces. Each piece represents a factor that can either increase or decrease the amount you send to your lender each month. Understanding these individual components is the first step toward accurately estimating your payment and ensuring it aligns with your financial capabilities. Let’s dive into the key players that determine your $10,000 car loan monthly payment.

Decoding the Key Factors Influencing Your Monthly Payment

Several critical elements dictate the size of your monthly car loan payment. Ignoring any one of them can lead to unexpected financial strain or missed opportunities for savings.

1. The All-Important Interest Rate

The interest rate is arguably the most influential factor in determining your monthly car loan payment. It’s the percentage of the principal loan amount that lenders charge you for borrowing their money. A higher interest rate means you’ll pay more each month, and significantly more over the life of the loan.

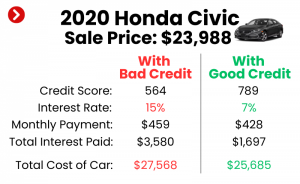

Based on my experience, interest rates are not arbitrarily assigned; they are meticulously calculated based on several criteria. Your credit score is the primary determinant. Individuals with excellent credit scores (typically 720+) are perceived as lower risk, qualifying them for the most favorable, lower interest rates. Conversely, a lower credit score indicates a higher risk to the lender, resulting in a higher interest rate to compensate for that perceived risk. Market conditions, such as the prime rate set by central banks, also play a role, influencing the overall cost of borrowing for all consumers.

2. The Loan Term: How Long You’ll Be Paying

The loan term, or repayment period, refers to the length of time you have to pay back the $10,000 loan. Common car loan terms range from 36 months (3 years) to 72 months (6 years), and sometimes even longer. This factor has a direct, inverse relationship with your monthly payment.

A shorter loan term, such as 36 or 48 months, will result in a higher monthly payment because you’re compressing the repayment of $10,000 (plus interest) into fewer installments. However, a significant advantage of a shorter term is that you’ll pay substantially less in total interest over the life of the loan. Conversely, a longer loan term, like 60 or 72 months, will lead to a lower monthly payment, making it seem more affordable upfront. The trade-off here is that you’ll accrue more interest over the extended period, meaning the total cost of your $10,000 car will be considerably higher. Pro tips from us: while a lower monthly payment might seem appealing, always calculate the total cost of the loan to understand the true financial impact.

3. The Power of a Down Payment

A down payment is the amount of money you pay upfront for the car, reducing the total amount you need to borrow. Even with a $10,000 car loan, making a down payment can significantly impact your monthly payment. If you put down $1,000, you’re only borrowing $9,000 instead of $10,000.

This reduction in the principal loan amount directly translates to a lower monthly payment. Furthermore, a substantial down payment can sometimes help you secure a better interest rate, as it signals to lenders that you’re a serious and responsible borrower. It also creates immediate equity in your vehicle, protecting you against negative equity (owing more than the car is worth).

4. Additional Fees and Charges

While not directly part of the $10,000 principal, various fees can be rolled into your total loan amount, effectively increasing the sum you finance. These might include origination fees, documentation fees, or even extended warranty costs. While some fees are unavoidable, it’s crucial to understand what you’re paying for.

Always scrutinize the loan agreement for any hidden or unexpected charges. Sometimes, these fees can slightly inflate the total amount you need to finance, subtly pushing your monthly payment a little higher than anticipated. Being aware of these additional costs allows you to negotiate or decide if they’re truly necessary.

Practical Examples: What a $10,000 Car Loan Could Look Like

To illustrate how these factors come together, let’s look at some hypothetical scenarios for a $10,000 car loan. These examples assume no down payment for simplicity, but remember a down payment would reduce the principal and thus the monthly payment.

Scenario 1: Excellent Credit (Low Interest Rate)

- Loan Amount: $10,000

- Interest Rate: 4.0% APR (Excellent Credit)

- Loan Term: 48 months (4 years)

- Estimated Monthly Payment: Approximately $225.79

- Total Interest Paid: ~$837.92

In this scenario, a strong credit profile allows for a competitive interest rate, keeping the overall cost of borrowing relatively low. The 48-month term balances a manageable monthly payment with a reasonable total interest payout.

Scenario 2: Good Credit (Average Interest Rate)

- Loan Amount: $10,000

- Interest Rate: 7.0% APR (Good Credit)

- Loan Term: 60 months (5 years)

- Estimated Monthly Payment: Approximately $198.01

- Total Interest Paid: ~$1,880.60

Here, with a slightly higher interest rate and a longer loan term, the monthly payment drops below $200. However, the trade-off is evident in the increased total interest paid, nearly doubling compared to the excellent credit example. This scenario highlights how extending the term reduces the monthly burden but inflates the total cost.

Scenario 3: Fair Credit (Higher Interest Rate)

- Loan Amount: $10,000

- Interest Rate: 12.0% APR (Fair Credit)

- Loan Term: 72 months (6 years)

- Estimated Monthly Payment: Approximately $195.69

- Total Interest Paid: ~$4,089.68

This example shows how a higher interest rate combined with a very long loan term can still yield a seemingly "affordable" monthly payment. However, the total interest paid skyrockets, making the $10,000 car almost $14,000 in reality. This is a common mistake to avoid: focusing solely on the monthly payment without considering the total cost.

Pro Tip: To get a precise calculation tailored to your specific situation, I highly recommend using an online car loan calculator. A trusted resource like Bankrate’s auto loan calculator can provide immediate, accurate estimates based on your chosen principal, interest rate, and loan term.

Beyond the Monthly Payment: Understanding the True Cost of a $10,000 Car Loan

While knowing "how much would a $10,000 car loan be a month" is essential, it’s only one piece of the puzzle. A truly informed decision requires looking beyond the immediate payment and understanding the comprehensive financial implications.

Total Interest Paid: The Hidden Cost

As demonstrated in the examples above, the total interest paid over the life of the loan can add thousands of dollars to the original $10,000 principal. This is the true "cost of borrowing" and often goes overlooked when buyers are fixated on securing the lowest possible monthly payment. A longer loan term or a higher interest rate dramatically increases this figure.

Always calculate the total amount you’ll repay (principal + total interest) before signing any agreement. This big picture view helps you assess the real value you’re getting for your money. You might find that stretching a loan to 72 months to save $20 a month isn’t worth paying an extra $2,000 in interest.

APR vs. Interest Rate: Know the Difference

It’s crucial to understand the distinction between the stated interest rate and the Annual Percentage Rate (APR). The interest rate is the cost of borrowing money, expressed as a percentage. The APR, however, represents the total cost of the loan over a year, including not only the interest rate but also any additional fees (like origination fees) charged by the lender.

For comparison purposes, the APR is a more accurate measure of the total cost of borrowing. When comparing loan offers, always compare the APR, not just the interest rate, to get a true apples-to-apples comparison. This ensures you’re accounting for all costs rolled into the loan.

Don’t Forget Car Ownership Costs

Your car loan payment is just one component of owning a vehicle. When budgeting for a $10,000 car, you must factor in other unavoidable expenses. These include auto insurance, which can vary wildly based on your age, driving record, location, and the car’s value.

Beyond insurance, consider fuel costs, routine maintenance (oil changes, tire rotations), unexpected repairs, and registration fees. These ongoing costs can easily add hundreds of dollars to your monthly expenses, making a seemingly affordable $10,000 car loan payment much heavier on your wallet than anticipated. It’s essential to integrate these into your overall budget before committing to a loan.

Strategies for Securing a Favorable $10,000 Car Loan

Now that you understand the variables, let’s explore how you can actively work towards securing the best possible terms for your $10,000 car loan. Small improvements in these areas can lead to significant savings over the life of your loan.

1. Boost Your Credit Score

Your credit score is your financial report card. A higher score signifies to lenders that you are a responsible borrower, making you eligible for lower interest rates. Before applying for a car loan, review your credit report for errors and take steps to improve your score if needed.

Paying bills on time, reducing existing debt, and avoiding new credit applications in the months leading up to your car purchase can all positively impact your score. Even a 50-point increase can make a difference in the interest rate you’re offered.

2. Save for a Down Payment

As discussed, a down payment directly reduces the amount you need to borrow, thereby lowering your monthly payment and total interest paid. Aim for at least 10-20% of the car’s purchase price. For a $10,000 car, even a $1,000 or $2,000 down payment can make a noticeable difference.

Beyond the immediate financial benefits, a down payment demonstrates your commitment and reduces the lender’s risk, sometimes opening the door to better loan terms. It also helps prevent you from being "upside down" on your loan, where you owe more than the car is worth.

3. Shop Around for Lenders

Never take the first loan offer you receive, especially not from the dealership. Dealerships often mark up interest rates. Pro tips from us: contact multiple financial institutions—banks, credit unions, and online lenders—to compare rates and terms. Credit unions, in particular, are often known for offering competitive auto loan rates.

You can apply for pre-approval from several lenders within a short period (usually 14-45 days, depending on the credit scoring model) without significantly harming your credit score. This is considered a single credit inquiry for rate shopping purposes. This process empowers you with leverage when negotiating at the dealership.

4. Consider a Shorter Loan Term (If Affordable)

While a longer loan term offers lower monthly payments, a shorter term saves you a substantial amount in total interest. If your budget allows, opt for the shortest loan term you can comfortably afford.

For a $10,000 car loan, paying it off in 36 or 48 months rather than 60 or 72 months can save you hundreds, if not thousands, in interest. It also means you’ll own your car outright much sooner.

5. Get Pre-Approval

Getting pre-approved for a loan before you even step foot in a dealership is a powerful strategy. Pre-approval gives you a clear understanding of how much you can borrow, at what interest rate, and what your estimated monthly payment will be.

This knowledge turns you into a cash buyer in the eyes of the dealership, shifting your focus from "Can I afford this monthly payment?" to "Is this car worth the price?" It removes the financial mystery and allows you to negotiate car prices more effectively.

Common mistakes to avoid are going into the dealership without pre-approval, falling in love with a car before knowing your financial limits, and focusing only on the monthly payment without understanding the total cost.

Is a $10,000 Car Loan Right for You? Assessing Affordability

Before committing to a $10,000 car loan, it’s crucial to honestly assess your financial situation and ensure the payments fit comfortably within your budget. Overextending yourself can lead to financial stress and difficulty meeting other obligations.

Budgeting 101: Integrating Your Car Loan

Start by creating a detailed monthly budget. List all your income sources and all your fixed and variable expenses. This includes rent/mortgage, utilities, groceries, existing debt payments, and discretionary spending. Once you have a clear picture, you can see how a new car loan payment would fit in.

A good rule of thumb is that your total car-related expenses (loan payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income. If a $10,000 car loan pushes you beyond this threshold, you might need to reconsider. For a deeper dive into managing your finances, check out our guide on Budgeting for a New Car and Understanding Car Ownership Costs. (Internal Link 1 Placeholder)

The 20/4/10 Rule

A widely recognized guideline for car affordability is the 20/4/10 rule:

- 20% Down Payment: Aim to put at least 20% down on your car.

- 4-Year Loan Term: Finance the car for no more than four years (48 months).

- 10% Income Limit: Your total monthly car expenses (payment, insurance, fuel) should not exceed 10% of your gross monthly income.

While this is a guideline, it’s a solid starting point for assessing if a $10,000 car loan is truly affordable for your situation. Adjustments can be made, but deviating too far from this rule can lead to financial strain.

Build a Contingency Fund

Life is unpredictable, and car ownership comes with unexpected costs. Before taking on a car loan, ensure you have an emergency fund in place, ideally covering 3-6 months of living expenses. This fund acts as a buffer against unexpected repairs, job loss, or other financial setbacks that could jeopardize your ability to make your car payments.

Having this safety net provides peace of mind and prevents you from falling into a debt spiral if unforeseen circumstances arise. Don’t let a car loan leave you vulnerable.

What If You Can’t Afford the Monthly Payment? Alternatives and Solutions

Sometimes, even after careful planning, the numbers just don’t add up, or your financial situation changes after you’ve already taken out a loan. If you find yourself struggling with a $10,000 car loan payment, there are still options available.

Refinancing Your Car Loan

If your credit score has improved since you took out the original loan, or if interest rates have dropped, you might be able to refinance your car loan. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with a more favorable term. This can significantly reduce your monthly payment and/or the total interest paid.

Based on my experience, refinancing is a particularly effective strategy if you initially secured a high-interest loan due to a lower credit score. As your credit improves, you become eligible for better terms. You can learn more about this process in our detailed article: Tips for Refinancing Your Car Loan: Lower Your Payments Today. (Internal Link 2 Placeholder)

Consider Buying a Cheaper Car

If the monthly payments for a $10,000 car are consistently out of reach, it might be a sign that you need to adjust your expectations. Buying a more affordable vehicle, even if it’s less desirable, is a financially sound decision.

A $7,000 or $8,000 car will naturally have lower loan payments and less total interest. Prioritizing practicality over desire can save you significant financial stress in the long run. There are many reliable, pre-owned vehicles available that can meet your transportation needs without breaking the bank.

Explore Other Transportation Options

For some, car ownership might not be the most economical choice at all. If the costs of a $10,000 car loan, insurance, and maintenance are too burdensome, consider alternative transportation methods. Public transportation, ride-sharing services, biking, or walking can be viable and much cheaper options, especially in urban areas.

Sometimes, delaying car ownership until your financial situation improves is the smartest move. It allows you to save more for a larger down payment or build a stronger financial foundation, making future car purchases much easier.

Conclusion: Making an Informed Decision About Your $10,000 Car Loan

The question "How much would a $10,000 car loan be a month?" is multifaceted, with its answer depending on a complex interplay of interest rates, loan terms, your creditworthiness, and any down payment you make. As we’ve explored, understanding these individual components is crucial for accurate budgeting and informed decision-making.

By focusing on improving your credit score, saving for a down payment, diligently shopping for the best rates, and considering a shorter loan term, you can significantly reduce your monthly payment and the total cost of your $10,000 car loan. Remember to look beyond the immediate payment and factor in the total interest, APR, and ongoing ownership costs.

Ultimately, securing a car loan that aligns with your financial goals requires thorough research, careful planning, and a willingness to negotiate. With the insights provided in this guide, you are now well-equipped to navigate the world of car financing and make a wise choice for your next vehicle. Drive confidently, knowing you’ve made an informed decision.

What are your biggest concerns when considering a car loan? Share your thoughts in the comments below!