Demystifying Your Monthly Payment On A $50,000 Car Loan: The Ultimate Comprehensive Guide

Demystifying Your Monthly Payment On A $50,000 Car Loan: The Ultimate Comprehensive Guide Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is often exciting, but when the price tag hits $50,000, the financial implications can quickly become overwhelming. Many prospective buyers find themselves staring at this figure, wondering: "What will my monthly payment be on a $50,000 car loan?" This isn’t a simple question with a single answer, as numerous variables come into play. Understanding these factors is crucial for making an informed decision that aligns with your financial health.

As expert bloggers and professional SEO content writers, our mission is to peel back the layers of complexity surrounding a $50,000 car loan. We aim to provide you with a super comprehensive, informative, and truly in-depth guide that demystifies every aspect of your potential monthly payment. Our goal is to equip you with the knowledge needed to navigate car financing with confidence, ensuring you secure a deal that’s not just affordable, but also smart. Let’s dive deep into the world of auto loans and uncover the real costs involved.

Demystifying Your Monthly Payment On A $50,000 Car Loan: The Ultimate Comprehensive Guide

The Foundation: What Exactly Influences Your $50,000 Car Loan Payment?

Calculating your exact monthly payment on a $50,000 car loan involves more than just plugging numbers into a simple calculator. It’s a dynamic interplay of several key financial elements. Understanding each of these components is the first step towards accurately estimating your payment and taking control of your auto financing journey.

1. The Power of the Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is arguably the most significant factor determining your monthly payment and the total cost of your $50,000 car loan. This percentage represents the cost of borrowing money from a lender. A higher interest rate means you’ll pay more for the privilege of taking out the loan, directly increasing your monthly obligation.

Based on my experience working with countless individuals navigating car financing, even a seemingly small difference in APR can translate into hundreds or even thousands of dollars over the life of your loan. For instance, a 1% difference on a $50,000 loan over 60 months can impact your monthly payment by around $25, adding up to $1,500 in total interest paid. This highlights the critical importance of securing the lowest possible interest rate.

2. The Loan Term: How Long Will You Be Paying?

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a direct, inverse relationship with your monthly payment. A longer loan term will generally result in a lower monthly payment, making the car seem more affordable in the short term.

However, pro tips from us, seasoned financial observers, suggest caution when opting for extended loan terms. While they reduce your immediate cash outflow, they almost always lead to paying significantly more interest over the life of the loan. Furthermore, a longer term increases the risk of negative equity, where your car depreciates faster than you pay off the loan, leaving you owing more than the car is worth.

3. Your Down Payment: Cash Upfront, Savings Down the Road

A down payment is the initial sum of money you pay towards the purchase of the car, reducing the amount you need to borrow. This is a powerful tool for managing your monthly payment on a $50,000 car loan. The larger your down payment, the less money you finance, which directly lowers your monthly payment and the total interest you’ll accrue.

Consider a $50,000 car. If you put down $5,000, you’re only financing $45,000. If you manage a $10,000 down payment, your loan principal drops to $40,000. This not only shrinks your monthly obligation but also provides a buffer against depreciation, reducing the chances of going "underwater" on your loan.

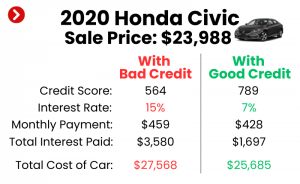

4. Your Credit Score: The Ultimate Financial Report Card

Your credit score is a numerical representation of your creditworthiness, and it’s perhaps the single most influential factor in determining the interest rate you’ll be offered. Lenders use this score to assess the risk of lending you money. A high credit score (generally 720 and above) signals to lenders that you are a responsible borrower, often leading to the most favorable interest rates.

Conversely, a lower credit score indicates a higher risk, prompting lenders to offer higher interest rates to compensate for that perceived risk. This can drastically increase your monthly payment on a $50,000 car loan. For a deeper dive into improving your credit score, read our detailed guide on .

5. Sales Tax, Fees, and Additional Charges

It’s a common mistake to overlook the ancillary costs associated with buying a car, particularly a $50,000 one. These often include sales tax (which varies by state), registration fees, documentation fees, and sometimes even dealer add-ons. These charges can easily add several thousand dollars to the total amount you need to finance, directly impacting your monthly payment.

For example, a 7% sales tax on a $50,000 car adds $3,500 to the price. If you roll this into your loan, your financed amount is now $53,500 before interest. Always factor these extra costs into your budget to avoid any unwelcome surprises when you finalize the deal.

Practical Scenarios: Estimating Your Monthly Payment on a $50,000 Car Loan

To give you a clearer picture, let’s explore some illustrative scenarios for a $50,000 car loan. Please remember these are estimates; actual rates and payments will vary based on market conditions, your specific lender, and personal financial profile. These calculations assume a standard amortization schedule.

Scenario 1: The Ideal Borrower (Excellent Credit)

- Loan Amount: $50,000

- Interest Rate (APR): 5.0% (Excellent credit, competitive market)

- Loan Term: 60 months (5 years)

- Down Payment: $0 (Though not recommended, for illustrative purposes)

In this scenario, your estimated monthly payment would be approximately $943.56. Over the 60 months, you would pay a total of $6,613.60 in interest.

Scenario 2: The Responsible Buyer (Good Credit with Down Payment)

- Loan Amount: $50,000

- Interest Rate (APR): 7.0% (Good credit, average market)

- Loan Term: 72 months (6 years)

- Down Payment: $5,000 (Financing $45,000)

Here, your estimated monthly payment would be around $760.40 (on the $45,000 financed amount). The total interest paid on the $45,000 loan would be approximately $9,048.80. Notice how the down payment significantly reduces the principal, and the longer term lowers the monthly payment, but the total interest still increases compared to Scenario 1 due to the longer duration and higher APR.

Scenario 3: The Challenged Borrower (Average Credit, Longer Term)

- Loan Amount: $50,000

- Interest Rate (APR): 10.0% (Average credit, higher risk)

- Loan Term: 84 months (7 years)

- Down Payment: $2,000 (Financing $48,000)

In this situation, your estimated monthly payment would be roughly $795.14 (on the $48,000 financed amount). The total interest paid on the $48,000 loan would skyrocket to approximately $18,791.76. This starkly illustrates how a higher interest rate and a longer term dramatically increase the overall cost of borrowing, despite a seemingly manageable monthly payment.

Strategies to Lower Your Monthly Payment on a $50,000 Car Loan

Understanding the factors is one thing; actively working to improve your financial position is another. There are several proactive steps you can take to reduce your monthly payment and overall cost when financing a $50,000 vehicle.

1. Boost Your Credit Score Before Applying

This is perhaps the most impactful strategy. Dedicate time to improving your credit score well before you step into a dealership or apply for a loan. Pay down existing debts, especially credit card balances, and ensure all your bills are paid on time. A higher credit score will directly translate to a lower APR, which, as we’ve seen, significantly reduces your monthly payment.

Common mistakes to avoid are applying for new credit cards right before a car loan application, which can temporarily ding your score. Focus on reducing existing debt and maintaining a consistent payment history.

2. Maximize Your Down Payment

The more cash you put down upfront, the less you need to borrow. This is a straightforward way to reduce your principal loan amount and, consequently, your monthly payments. Aim for at least a 10-20% down payment on a $50,000 car, which would be $5,000 to $10,000. Not only does this lower your monthly cost, but it also helps you build equity in the car faster.

Based on my experience, a substantial down payment can also make you a more attractive borrower to lenders, potentially leading to even better interest rates.

3. Diligently Shop Around for Lenders

Never accept the first loan offer you receive, especially from a dealership. Dealerships often work with multiple lenders, but their initial offer might not be the best available to you. Pro tips from us include contacting your own bank or credit union, and exploring online lenders before visiting the dealership. Getting pre-approved for a loan provides you with leverage and a benchmark rate.

This pre-approval acts like a "shopping pass," giving you a clear idea of the interest rate you qualify for, and enabling you to negotiate the best deal on the car itself, separate from the financing.

4. Negotiate the Car Price Itself

Remember, the loan amount is based on the final sale price of the vehicle. Every dollar you shave off the purchase price directly reduces the principal you need to finance. Don’t be afraid to negotiate. Research market values, understand the dealer’s invoice price, and be prepared to walk away if you don’t feel you’re getting a fair deal.

A $1,000 reduction in the car’s price on a $50,000 loan can save you hundreds in interest over the loan term, in addition to lowering your monthly payment.

5. Consider Refinancing Your Car Loan

If you’ve already taken out a $50,000 car loan and your financial situation has improved (e.g., your credit score has gone up, or interest rates have dropped), refinancing might be an excellent option. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payment or the total interest paid.

If you’re considering refinancing, explore our comprehensive article on to understand if it’s the right move for your situation.

Beyond the Monthly Payment: The True Cost of Car Ownership

While focusing on the monthly payment for your $50,000 car loan is essential, it’s crucial to understand that it’s just one piece of the larger financial puzzle. The true cost of owning a high-value vehicle extends far beyond the loan repayment. Neglecting these additional expenses can quickly derail your budget.

1. Car Insurance: A Non-Negotiable Expense

For a $50,000 car, comprehensive insurance coverage is not only a smart choice but often a requirement by lenders. The cost of insurance for a luxury or high-performance vehicle will be significantly higher than for a more modest car. Factors like your driving record, age, location, and the specific make and model will all influence your premium.

Budgeting for insurance is critical. Get quotes before you buy the car to avoid any sticker shock. This recurring cost can easily add several hundred dollars to your monthly outgoings.

2. Maintenance and Repairs: Prepare for the Unexpected

While newer $50,000 cars typically come with manufacturer warranties, routine maintenance is still necessary and can be costly. Oil changes, tire rotations, brake pad replacements, and other scheduled services for premium vehicles often come with premium prices. As the car ages, out-of-warranty repairs can be substantial.

Proactively setting aside a maintenance fund each month is a wise financial habit. Don’t let a major repair catch you off guard.

3. Fuel Costs: The More You Drive, the More You Spend

A $50,000 car might be a performance vehicle, an SUV, or a luxury sedan. Each type has varying fuel efficiency. While some might be hybrids, many will require premium fuel or consume more gasoline than an economy car. Your daily commute and driving habits will dictate this expense, but it’s a significant recurring cost that needs to be factored into your monthly budget.

4. Depreciation: The Hidden Cost of Ownership

Cars, especially new ones, begin to lose value the moment they leave the dealership lot. This phenomenon is called depreciation, and for a $50,000 vehicle, the monetary loss can be substantial in the first few years. While depreciation doesn’t directly impact your monthly loan payment, it affects your overall financial position, especially if you plan to trade in or sell the car within a few years.

Understanding depreciation helps you avoid negative equity and makes you a more informed buyer when considering future vehicle purchases.

Common Mistakes to Avoid When Financing a $50,000 Car

As expert financial observers, we’ve witnessed common pitfalls that buyers often stumble into. Avoiding these mistakes is paramount to a successful and financially sound car purchase.

- Focusing Solely on the Monthly Payment: This is perhaps the biggest mistake. While a low monthly payment seems appealing, it often comes at the expense of a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring the Total Cost of the Loan: Beyond the principal, you’re paying interest, fees, and potentially other add-ons. Calculate the grand total to truly understand what your $50,000 car is costing you.

- Not Shopping for Interest Rates: As discussed, different lenders offer different rates. Failing to compare offers can cost you thousands over the loan’s life.

- Rolling Negative Equity into a New Loan: If you owe more on your current car than it’s worth, and you roll that difference into a new $50,000 loan, you’re starting off "underwater." This is a dangerous financial move that increases your new loan principal and makes it harder to get out of debt.

- Skipping a Down Payment Entirely: While sometimes necessary, a zero-down payment significantly increases your monthly burden and puts you at higher risk of negative equity right from the start.

Pro Tips for a Smooth $50,000 Car Loan Experience

To ensure your journey to owning a $50,000 car is as smooth and financially sound as possible, here are some invaluable tips from our experience.

- Get Pre-Approved: Our professional advice leans heavily on the principle of getting pre-approved for a loan before you even set foot in a dealership. This empowers you with a solid interest rate and a clear budget, shifting your focus to negotiating the car price, not the financing.

- Read the Fine Print: Auto loan contracts can be complex. Take your time to read every clause, understand all terms, and ask questions about anything that’s unclear. Don’t rush this crucial step.

- Understand Add-Ons: Dealerships often offer extended warranties, GAP insurance, paint protection, and other extras. While some might be valuable, many are highly profitable for the dealer. Understand what each add-on entails, its true cost, and if it’s genuinely necessary for your situation. Common mistakes to avoid are accepting these without proper consideration, as they can significantly inflate your loan amount.

- Budget Realistically: Beyond the loan payment, factor in insurance, fuel, maintenance, and even potential parking costs. Create a comprehensive monthly budget to ensure your $50,000 car purchase fits comfortably within your financial means.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, if the numbers don’t add up, or if you feel pressured, remember you always have the option to walk away. There will always be another car and another deal.

For official consumer guidance on auto loans, refer to resources like the Consumer Financial Protection Bureau (CFPB), which offers valuable, unbiased information to help consumers make informed financial decisions.

Conclusion: Driving Away with Confidence

Navigating the complexities of a $50,000 car loan requires careful planning, thorough research, and a clear understanding of all the financial components at play. Your monthly payment is a dynamic figure influenced by interest rates, loan terms, down payments, your credit score, and additional fees. By actively managing these factors and avoiding common pitfalls, you can significantly reduce your monthly obligation and the overall cost of ownership.

Our ultimate goal is to empower you to make intelligent financial decisions. By focusing not just on the alluring monthly payment, but on the total cost of the loan and the broader expenses of car ownership, you can drive away with confidence, knowing you’ve secured a deal that truly aligns with your financial well-being. Remember, an informed buyer is a powerful buyer. Use this guide as your roadmap to a smarter car purchase.