Do I Qualify For A Car Loan? Your Ultimate Guide to Auto Loan Approval

Do I Qualify For A Car Loan? Your Ultimate Guide to Auto Loan Approval Carloan.Guidemechanic.com

Navigating the world of car loans can feel like deciphering a complex code. For many, the burning question remains: "Do I qualify for a car loan?" This isn’t just a simple yes or no answer; it involves a detailed look into various aspects of your financial life that lenders scrutinize. Understanding these factors is the first crucial step toward securing the vehicle you need.

In this comprehensive guide, we’ll peel back the layers of auto loan eligibility, providing you with an in-depth understanding of what lenders truly look for. Our goal is to empower you with the knowledge to confidently approach the car buying process, significantly increasing your chances of approval and securing favorable loan terms. By the end of this article, you’ll not only know if you qualify but also how to improve your qualification standing.

Do I Qualify For A Car Loan? Your Ultimate Guide to Auto Loan Approval

I. Understanding the Basics: What Lenders Look For

When you apply for a car loan, lenders aren’t just looking at your enthusiasm for a new ride. They’re assessing risk. Their primary concern is whether you have the ability and willingness to repay the loan on time, every time. This assessment involves evaluating a combination of financial indicators that paint a picture of your financial health.

Lenders use a consistent set of criteria to determine if you meet their qualification standards. These criteria help them predict your reliability as a borrower. Think of it as a financial background check, designed to protect both the lender and, in a way, you from taking on a loan you can’t afford.

Understanding these core components is paramount. It allows you to anticipate potential hurdles and proactively address them before you even step foot in a dealership or apply online.

II. The Cornerstone: Your Credit Score (And History)

Without a doubt, your credit score and credit history are the most influential factors in determining if you qualify for a car loan. These numbers are a quick summary of your financial past, indicating how responsibly you’ve handled debt previously.

A. What is a Credit Score?

A credit score is a three-digit number, typically ranging from 300 to 850, that reflects your creditworthiness. The two most common scoring models are FICO and VantageScore. These scores are calculated based on various factors in your credit report, including payment history, amounts owed, length of credit history, new credit, and credit mix.

A higher score signifies lower risk to lenders, making you a more attractive borrower. Conversely, a lower score suggests a higher risk, potentially leading to higher interest rates or even outright denial.

B. How Credit Scores Impact Car Loans

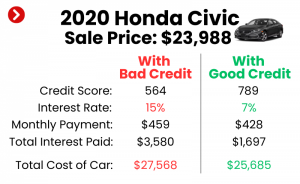

Your credit score directly influences the interest rate you’ll be offered. Borrowers with excellent credit (typically 780+) often qualify for the lowest rates, sometimes even 0% APR promotions. Those with good credit (670-739) will still receive competitive rates, though slightly higher. Fair credit (580-669) means higher rates, reflecting the increased risk.

If your score falls into the poor credit category (below 580), qualifying for a traditional car loan becomes significantly harder. You might face much higher interest rates, stricter terms, or be directed towards subprime lenders.

C. Building and Improving Your Credit

Based on my experience, many people underestimate the power of proactively improving their credit score. Even small improvements can lead to significant savings on interest over the life of a car loan. Start by checking your credit report for errors and disputing any inaccuracies.

Consistently paying all your bills on time is the single most effective way to boost your score. Reduce your credit card balances to lower your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. Opening new credit responsibly and maintaining a diverse credit mix can also help over time.

III. Your Financial Health: Income and Employment Stability

Beyond your credit score, lenders need assurance that you have the financial capacity to make your monthly car loan payments. This is where your income and employment stability come into play.

A. Steady Income is Key

Lenders want to see a consistent and reliable source of income. This demonstrates your ability to meet your financial obligations. They typically look for a minimum income threshold, though this can vary based on the loan amount requested and the lender’s specific policies.

Your gross monthly income is what they’ll primarily consider. The higher and more stable your income, the more comfortable lenders will be approving your loan, potentially for a larger amount or with better terms.

B. Employment History Matters

A stable employment history signals reliability. Lenders prefer to see that you’ve been employed at your current job, or within the same industry, for a significant period – often six months to two years or more. Frequent job changes, especially within different fields, can be viewed as a red flag, indicating potential instability.

If you’re self-employed, lenders will typically require a longer history of self-employment (usually two years) and more extensive documentation, such as tax returns, to verify your income.

C. Income Verification

To verify your income, lenders will request specific documentation. This commonly includes recent pay stubs (typically the last two or three), W-2 forms from the past one or two years, and sometimes tax returns. If you receive income from other sources, such as social security or disability, you’ll need to provide official documentation for those as well.

Our pro tip here is to have all your income verification documents organized and ready before you apply. This streamlines the process and demonstrates your preparedness to the lender.

IV. Managing Your Debts: The Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is a critical metric that lenders use to assess your ability to take on new debt. It provides a clear picture of how much of your monthly gross income is already consumed by existing debt payments.

A. What is DTI?

Your DTI ratio is calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your total monthly debt payments (mortgage/rent, credit cards, student loans, personal loans) are $1,500 and your gross monthly income is $4,000, your DTI would be 37.5% ($1,500 / $4,000 = 0.375).

This ratio helps lenders understand if you have enough disposable income left over to comfortably afford a new car payment in addition to your current financial commitments.

B. Ideal DTI for Car Loans

While there’s no universally "perfect" DTI, most lenders prefer to see a DTI ratio of 43% or lower. Some may even prefer it to be below 36%. A lower DTI indicates that you have more financial wiggle room, making you a less risky borrower.

If your DTI is too high, adding a new car payment could stretch your finances too thin, increasing the likelihood of missed payments. Lenders are wary of this scenario.

C. Lowering Your DTI

If your DTI is on the higher side, there are strategies to improve it. The most direct approach is to pay down existing debts, especially those with high monthly payments like credit cards. Increasing your income, if possible, will also help lower the ratio.

A common mistake to avoid is not knowing your DTI before applying. Calculate it yourself first. If it’s high, consider focusing on debt reduction for a few months before seeking a car loan. This preparation can significantly improve your chances of approval and secure better terms.

V. The Power of a Down Payment

Making a down payment on a car loan is one of the smartest financial moves you can make. It demonstrates your commitment, reduces the loan amount, and lessens the risk for the lender.

A. Why Down Payments are Crucial

A down payment reduces the principal amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan’s life. From a lender’s perspective, a down payment provides an immediate equity stake in the vehicle. If you default, they have a better chance of recouping their losses by selling the car.

It also signals to the lender that you are serious about the purchase and have some financial discipline, as you’ve saved money for the initial outlay.

B. Recommended Down Payment Amounts

While it’s possible to get a car loan with no money down, it’s generally not advisable, especially if you have less-than-perfect credit. For new cars, a down payment of at least 10-20% of the vehicle’s purchase price is often recommended. For used cars, where depreciation is faster, a higher down payment of 15-25% can be even more beneficial.

The more you put down, the better your loan terms are likely to be. It also helps you avoid being "upside down" on your loan (owing more than the car is worth) early in the ownership period.

C. The Benefits of a Larger Down Payment

Beyond reducing your monthly payments and interest, a larger down payment can open doors to better interest rates, even if your credit score isn’t stellar. It acts as a mitigating factor for other potential weaknesses in your application.

Furthermore, it provides you with instant equity, protecting you against rapid depreciation. Should you need to sell the car sooner than expected, you’re less likely to find yourself in a negative equity position.

VI. Choosing the Right Vehicle: Price and Age

The type of vehicle you intend to purchase also plays a role in whether you qualify for a car loan. Lenders consider the car’s value, age, and even its mileage when assessing the risk of the loan.

A. Vehicle Affordability

Lenders want to ensure that the car’s price is reasonable relative to your income and the loan terms. They typically have limits on the loan-to-value (LTV) ratio, which compares the loan amount to the car’s appraised value. If the car is overpriced for its market value, or if you’re trying to finance too much beyond the car’s worth (e.g., adding aftermarket products into the loan), it can hinder approval.

It’s crucial not to overextend yourself. A good rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 10-15% of your gross monthly income.

B. New vs. Used Car Loans

Lenders generally view new car loans as less risky than used car loans. New cars come with warranties, have predictable maintenance schedules, and hold their value better initially (though they depreciate quickly). This often translates to lower interest rates and longer loan terms for new vehicles.

Used cars, while cheaper to purchase, can sometimes be riskier for lenders due to unknown maintenance history, higher mileage, and faster depreciation rates. This can lead to higher interest rates and shorter loan terms compared to new car loans.

C. Vehicle Age and Mileage

The age and mileage of a used car are significant factors. Lenders often have restrictions on how old a vehicle can be or how many miles it can have to qualify for financing, especially for longer loan terms. Older cars with very high mileage represent a higher risk of mechanical failure, which could leave you with a non-functional asset and a loan to repay.

Some lenders might not finance vehicles older than a certain age (e.g., 10-12 years) or with mileage exceeding a certain threshold (e.g., 100,000-150,000 miles). This is important to consider when you’re car shopping.

VII. Essential Documentation You’ll Need

Being prepared with the right documents can significantly speed up the car loan application process. Lenders require these to verify your identity, income, residency, and other crucial details.

Here’s a common list of what you’ll typically need:

- Proof of Identity: A valid government-issued photo ID (driver’s license, state ID, passport).

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms (last 1-2 years), or tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement showing your current address.

- Social Security Number (SSN): For credit checks.

- Proof of Insurance: You’ll need to show proof of full coverage insurance before driving off with the car, as it’s typically a loan requirement.

- Trade-in Information (if applicable): Title, registration, and payoff amount for your current vehicle.

Having these documents organized and easily accessible will demonstrate your readiness and seriousness to the lender.

VIII. The Application Process: Steps to Success

Understanding the application process itself is key to maximizing your chances of approval and securing the best possible loan terms. It’s not just about filling out forms; it’s about strategic planning.

A. Get Pre-Approved

From years of observing the auto loan market, getting pre-approved is one of the most powerful steps you can take. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a certain amount at a specific interest rate, before you’ve even chosen a car.

This gives you several advantages:

- Know Your Budget: You’ll know exactly how much car you can afford.

- Stronger Negotiating Position: You become a cash buyer at the dealership, allowing you to focus on the car’s price rather than the monthly payment.

- Compare Offers: You can compare the pre-approved offer with any financing options the dealership presents.

Pre-approvals usually involve a "soft pull" on your credit, which doesn’t affect your score. Once you’re ready to finalize, a "hard pull" will occur.

B. Shopping for Rates

Don’t settle for the first loan offer you receive. Just as you shop for a car, you should shop for your car loan. Contact multiple banks, credit unions, and online lenders. Credit unions, in particular, often offer very competitive rates.

When comparing offers, look beyond just the monthly payment. Focus on the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing.

C. Understanding Loan Terms

The loan term, or length of the loan, significantly impacts your monthly payment and the total interest paid. Longer terms (e.g., 72 or 84 months) result in lower monthly payments but accumulate much more interest over time. Shorter terms (e.g., 36 or 48 months) have higher monthly payments but save you a substantial amount in interest.

Carefully consider your budget and your long-term financial goals when choosing a loan term. Avoid stretching out a loan simply to get a lower monthly payment if it means paying significantly more in the long run.

IX. What If My Qualification Isn’t Ideal? (Addressing Challenges)

It’s common for applicants to face challenges. Don’t despair if your credit isn’t perfect or your income isn’t sky-high. There are still pathways to car loan approval, though they might require different strategies.

A. Bad Credit Car Loans

If you have a low credit score, traditional lenders might be hesitant. However, there are options:

- Subprime Lenders: These lenders specialize in working with borrowers with poor credit. Be prepared for higher interest rates and potentially shorter loan terms to offset the increased risk.

- Co-Signer: A co-signer with good credit can significantly improve your chances of approval and secure better terms. They take on equal responsibility for the loan, so choose someone you trust and who understands the commitment.

- Secured Loan: Some lenders offer secured loans where you use an asset (like savings) as collateral.

- Buy Here, Pay Here Dealerships: These dealerships finance cars directly. While convenient, their interest rates are often very high, and terms can be less favorable. Proceed with caution.

B. No Credit History

First-time car buyers or those new to credit often face the "no credit, no loan" dilemma.

- Co-Signer: This is often the most effective solution for building credit.

- Secured Loan: As mentioned above, using collateral can help.

- First-Time Buyer Programs: Some lenders and dealerships offer specific programs for individuals with no credit history, often with stricter requirements or higher rates.

- Smaller Loan Amount: Start with a less expensive, reliable used car. This reduces the risk for the lender and gives you a chance to build positive payment history.

C. Low Income

If your income is low, lenders will be concerned about your ability to afford the payments.

- Budget for a Cheaper Car: Adjust your expectations to a more affordable vehicle. This reduces the loan amount needed, making it easier to qualify.

- Increase Your Down Payment: A larger down payment reduces the loan amount, making the monthly payments more manageable relative to your income.

- Improve Your DTI: Focus on paying down existing debts to free up more of your income for a car payment.

- Consider a Co-Borrower: Unlike a co-signer, a co-borrower’s income is also considered, which can boost your overall income for qualification purposes.

X. Beyond the Numbers: Other Factors

While credit, income, and debt are paramount, a few other considerations can subtly influence your car loan qualification.

A. Residency Requirements

Lenders generally require proof of permanent residency in the area where you’re applying for the loan. This typically means having a stable address in the state or country where the loan is being originated. They need to confirm you’re not transient and can be reliably reached.

B. Age Restrictions

To legally enter into a loan agreement, you must be at least 18 years old in most states (19 in Alabama and Nebraska, 21 in Mississippi). This is a fundamental legal requirement for any contract.

C. Insurance Requirements

Lenders almost always require you to carry full coverage insurance (collision and comprehensive) on the financed vehicle until the loan is paid off. This protects their investment in case the car is damaged or stolen. You’ll need to provide proof of insurance before you can drive off the lot. The cost of this insurance should be factored into your overall budget. For more details on budgeting for a car, you might find our article on Smart Car Buying Strategies helpful.

Conclusion: Your Roadmap to Car Loan Qualification

Determining "Do I qualify for a car loan?" is a multi-faceted process that rewards preparation and understanding. From your credit score and history to your income stability, debt-to-income ratio, and the size of your down payment, every financial detail contributes to the lender’s decision. Even the vehicle itself plays a role.

By thoroughly assessing your own financial standing against these criteria, you can approach the car loan application process with confidence and clarity. Remember to check your credit report, calculate your DTI, save for a substantial down payment, and explore pre-approval options. If your financial profile isn’t perfect, explore alternatives like co-signers or specialized lenders.

The journey to car ownership doesn’t have to be daunting. With this comprehensive guide, you are now equipped with the knowledge to not only qualify for a car loan but to secure one on the best possible terms. For further reading on managing your finances, check out this trusted external resource: Consumer Financial Protection Bureau’s Auto Loan Guide. Your next vehicle awaits – go get it!