Do You Get A Car Loan Before Buying A Car? Your Ultimate Guide to Smart Auto Financing

Do You Get A Car Loan Before Buying A Car? Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is an exciting milestone, often marking a significant personal or family investment. Yet, for many, the thrill of choosing a new vehicle quickly turns into anxiety when faced with the complexities of financing. One of the most common questions that arises early in this process is: Do you get a car loan before buying a car?

This isn’t just a simple yes or no question; it’s a strategic decision that can dramatically impact your entire car-buying experience, from the price you pay to the interest rate you secure. As an expert in automotive finance and a seasoned buyer, I’ve seen firsthand how understanding this critical step can empower consumers and save them thousands. This comprehensive guide will dissect the "before vs. during" debate, providing you with the knowledge and tools to navigate car financing like a pro.

Do You Get A Car Loan Before Buying A Car? Your Ultimate Guide to Smart Auto Financing

By the end of this article, you’ll not only have a clear answer but also a robust strategy to ensure you drive away with the best possible deal. Let’s dive in and unlock the secrets to smart auto financing.

The Core Question: Before or During? Understanding Your Options

The central dilemma for many prospective car buyers revolves around the timing of their loan application. Should you secure financing before you even step foot on a dealership lot, or is it better to wait and let the dealership handle the loan process while you’re buying the car?

While both approaches are common, one undeniably offers more control, transparency, and often, better financial outcomes for the buyer. This approach is known as pre-approval, and it’s a game-changer for anyone serious about getting a great deal on their next vehicle.

Pre-approval essentially means that an independent lender (like a bank, credit union, or online lender) reviews your financial situation and provisionally agrees to lend you a certain amount of money at a specific interest rate, before you’ve even picked out a car. You’ll receive a pre-approval letter detailing these terms.

On the other hand, waiting until you’re at the dealership means you’re relying on their finance department to arrange a loan for you. While convenient, this often puts you at a significant disadvantage, as we’ll explore in detail.

Why Pre-Approval is Your Secret Weapon: The "Before" Advantage

Based on my experience guiding countless individuals through the car-buying maze, getting pre-approved for a car loan before you start shopping is hands down the smartest move you can make. It transforms you from a vulnerable buyer into a powerful, informed negotiator. Let’s break down why this strategy is so effective.

1. Power to Negotiate Like a Cash Buyer

Imagine walking into a dealership with a pre-approval letter in hand. You’re not just a potential buyer; you’re essentially a "cash buyer" in the eyes of the salesperson. You already have your financing secured, which means the dealership’s primary focus shifts from selling you a loan to selling you a car.

This puts immense power in your hands. You can negotiate the vehicle’s price independently, without the salesperson trying to manipulate the numbers by bundling the car price and loan terms together. You know exactly what loan terms you qualify for, allowing you to separate the car purchase from the financing discussion.

2. Crystal Clear Budget Clarity

One of the biggest pitfalls in car buying is falling in love with a vehicle you can’t truly afford. Pre-approval eliminates this risk entirely. By getting approved for a specific loan amount beforehand, you establish a firm upper limit for your car budget.

This clarity allows you to shop for vehicles within your financial comfort zone. You’ll know exactly how much car you can realistically purchase, preventing emotional overspending and ensuring your monthly payments are manageable. It’s about making a practical decision, not an impulsive one.

3. Streamlined Dealership Experience and Time Savings

Nobody enjoys spending hours at a dealership, especially in the finance office. With a pre-approved loan, you significantly cut down on the time spent on paperwork and negotiations. You’ve already done the heavy lifting of securing your financing.

When you arrive at the dealership, you can focus purely on test driving, inspecting the vehicle, and negotiating the purchase price. Once a price is agreed upon, you simply present your pre-approval letter, and the dealer can finalize the sale, often much quicker than if they had to arrange financing from scratch.

4. Avoiding Dealership Markups and Hidden Fees

Dealerships often make a substantial portion of their profit not just from selling cars, but also from arranging financing. They might mark up the interest rate offered by their lending partners, keeping the difference as profit. This is perfectly legal but can cost you hundreds or even thousands of dollars over the life of the loan.

With a pre-approved loan, you have a benchmark. You know the best interest rate you qualify for from an independent source. If the dealership offers a better rate, great! But if they don’t, you have a solid alternative ready to go, protecting you from inflated rates and unnecessary fees.

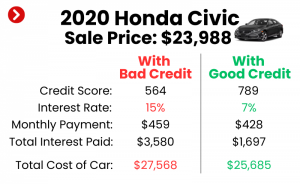

5. Access to Potentially Better Interest Rates

Independent lenders, such as banks and credit unions, often offer more competitive interest rates than what a dealership might initially present. Because these institutions specialize solely in lending, they can sometimes provide better terms, especially if you have a strong credit history.

Shopping around for pre-approval allows you to compare offers from multiple lenders, ensuring you secure the lowest possible Annual Percentage Rate (APR). This direct comparison is incredibly difficult to do effectively once you’re already sitting in the dealership’s finance office under pressure.

6. Focus on the Car, Not the Loan

The car-buying process can be overwhelming. When you combine the excitement of choosing a vehicle with the stress of negotiating a loan, it’s easy to lose focus. Pre-approval separates these two major decisions.

You can dedicate your energy to evaluating the car itself: its features, condition, test drive performance, and suitability for your needs. Once you’ve found the perfect vehicle, the financing aspect is largely settled, allowing for a much smoother and less stressful transaction.

The Step-by-Step Guide to Getting Pre-Approved for a Car Loan

Now that you understand the immense benefits, let’s walk through the practical steps to getting pre-approved for a car loan. This proactive approach will set you up for success.

Step 1: Check Your Credit Score and Report

Your credit score is the single most important factor determining the interest rate you’ll be offered. Lenders use it to assess your creditworthiness and the risk associated with lending to you.

- Understanding Your Score: A higher score (generally 700+) indicates lower risk and qualifies you for the best rates. If your score is lower, understanding it gives you a chance to address any issues before applying.

- Obtain Your Report: Request a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) at AnnualCreditReport.com.

- Review for Accuracy: Scrutinize your reports for any errors, fraudulent activity, or outdated information. Disputing inaccuracies can often boost your score. Based on my experience, many people overlook this crucial step, only to find mistakes that negatively impact their loan offers.

- Improve Your Score (If Needed): If time permits, paying down existing debt, making all payments on time, and avoiding new credit applications can help improve your score.

Step 2: Determine Your Realistic Car Budget

Beyond just the monthly payment, you need to understand the total cost of car ownership. This involves more than just the loan amount.

- Total Loan Amount: How much can you comfortably afford to borrow?

- Down Payment: How much cash can you put down upfront? A larger down payment reduces the loan amount and often leads to better terms.

- Insurance Costs: Get quotes for the vehicles you’re considering; insurance can be a significant expense.

- Maintenance and Fuel: Factor in ongoing operational costs.

- Registration and Taxes: Don’t forget these one-time and recurring fees.

Pro tips from us: Aim for a total car payment (loan + insurance) that doesn’t exceed 10-15% of your net monthly income. This ensures you have room for other essential expenses and savings.

Step 3: Gather Necessary Documents

Lenders will require specific documentation to process your pre-approval application. Having these ready will expedite the process.

- Proof of Income: Pay stubs, W-2 forms, tax returns, or bank statements.

- Proof of Identity: Driver’s license or other government-issued ID.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Employer Information: Name, address, and phone number.

Step 4: Shop Around for Lenders

Don’t settle for the first offer you receive. This is where the "shopping around" aspect truly pays off.

- Banks: Your current bank might offer special rates, but also check other major national and local banks.

- Credit Unions: Often known for competitive rates and personalized service, credit unions are excellent options, especially if you’re already a member or qualify for membership.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans and can offer quick decisions and competitive rates.

- Comparison Websites: Some platforms allow you to get multiple pre-qualified offers with a single application (often a soft credit pull).

External Link: For a deeper dive into choosing the right lender, you might find this guide on How to Choose the Best Auto Loan Lender from the Consumer Financial Protection Bureau helpful.

Step 5: Submit Applications and Understand Credit Inquiries

When you apply for pre-approval, lenders will typically perform a "hard inquiry" on your credit report. This can temporarily lower your credit score by a few points.

- Rate Shopping Window: Fortunately, credit scoring models recognize that you’re shopping for the best rate. Multiple hard inquiries for the same type of loan within a specific timeframe (usually 14-45 days, depending on the scoring model) are often counted as a single inquiry. So, apply to multiple lenders within a short window to minimize the impact on your score.

Step 6: Review and Compare Offers

Once you receive pre-approval offers, carefully compare them. Don’t just look at the monthly payment.

- Annual Percentage Rate (APR): This is the true cost of borrowing, encompassing the interest rate and other fees. Always compare APRs.

- Loan Term: The length of the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid over time.

- Fees: Look for any origination fees, application fees, or prepayment penalties.

- Terms and Conditions: Read the fine print carefully.

Choose the offer that best aligns with your budget and financial goals.

Common Mistakes to Avoid During the Car Loan Process

Even with the best intentions, buyers can make mistakes that cost them money. Based on my years in the industry, these are some of the most common pitfalls to sidestep.

1. Focusing Only on Monthly Payments

This is perhaps the most insidious mistake. Salespeople are masters at "payment packing," where they adjust the loan term or add extra products (like extended warranties) to keep the monthly payment seemingly affordable, even if it means a much higher total cost.

Instead: Always focus on the total price of the car and the Annual Percentage Rate (APR) of the loan. A lower monthly payment over a longer term often means paying significantly more in interest over the life of the loan.

2. Not Shopping Around for Loans

As emphasized, failing to get pre-approved or only checking with one lender is a missed opportunity. You’re leaving money on the table by not comparing offers.

Instead: Apply to at least 3-4 different lenders (banks, credit unions, online lenders) within a concentrated period to get the best possible rate. Your pre-approval offers give you leverage.

3. Ignoring Your Credit Report

Many buyers only check their credit score, not their full report. A mistake on your report could be costing you a better interest rate without you even knowing it.

Instead: Obtain and meticulously review all three of your credit reports well in advance of applying for a loan. Dispute any inaccuracies immediately.

4. Letting the Dealership Control the Narrative

When you walk in without pre-approved financing, the dealership often dictates the terms, bundling the car price and loan terms into a single, confusing negotiation. This makes it difficult to know if you’re getting a good deal on either.

Instead: Have your financing in place. This allows you to negotiate the car’s purchase price as a separate transaction, much like a cash buyer. You control the narrative.

5. Impulse Buying

The excitement of a new car can lead to rash decisions, especially when you’re on the dealership lot. Emotional choices rarely lead to the best financial outcomes.

Instead: Stick to your budget. Research thoroughly. Don’t be swayed by high-pressure tactics. If a deal feels rushed or too good to be true, it probably is. Take your time, walk away if necessary, and sleep on it.

When Dealership Financing Might Be an Option (The "During" Scenario)

While pre-approval is generally the superior strategy, there are specific situations where dealership financing might become a viable or even preferable option. However, even in these cases, having a pre-approval in your back pocket is still crucial for comparison.

1. Special Promotional APR Offers

Dealerships, especially those representing specific manufacturers, sometimes offer incredibly low (or even 0%) APR financing as a special promotion. These offers are usually limited to buyers with excellent credit and specific models.

- The Catch: These deals are rare and often require specific loan terms or may not be combinable with other incentives.

- Your Strategy: If you qualify for such an offer, it could beat your pre-approval. But you’ll only know if you have a pre-approval to compare it against.

2. Convenience and Simplicity

For some buyers, the appeal of a "one-stop shop" is strong. Getting the financing and the car all in one place can save time and reduce perceived hassle.

- The Caveat: This convenience often comes at a cost. Without an independent benchmark, you might pay a higher interest rate or agree to less favorable terms.

- Your Strategy: Even if you prefer the convenience, secure a pre-approval first. You can then present it to the dealership and see if they can beat or match your best outside offer.

3. Trade-in Integration

When you’re trading in your old vehicle, integrating that into the financing process at the dealership can sometimes streamline the paperwork.

- The Risk: Dealerships can sometimes manipulate trade-in values and loan terms to make a deal look better than it is.

- Your Strategy: Always get an independent appraisal for your trade-in (e.g., from Kelley Blue Book, Edmunds, or another dealer) before you go to the dealership. Negotiate the car price and your trade-in value separately, then discuss financing.

In essence, dealership financing should be seen as a comparison point against your pre-approval, not your default option. Never walk in blind.

Pro Tips for a Smooth Car Buying Experience

To further enhance your car buying journey, here are some additional pro tips from us that go beyond just the loan.

1. Know Your Trade-In Value Beforehand

Don’t wait for the dealership to tell you what your old car is worth. Research its market value using reputable online tools like Kelley Blue Book (KBB.com) or Edmunds.com. Get offers from other dealerships or online car buying services (like Carvana or Vroom) to establish a baseline. This prevents the dealer from lowballing you.

2. Separate Negotiations: Car Price vs. Loan vs. Trade-In

This is crucial. Negotiate the price of the new car first. Once that’s settled, then discuss your trade-in. Finally, bring up financing, using your pre-approval as your baseline. Trying to negotiate all three at once is a recipe for confusion and usually results in a less favorable outcome for you.

3. Read the Fine Print – Every Single Document

Before signing anything, thoroughly read all contracts and documents. Pay close attention to:

- The final purchase price of the vehicle.

- The APR and total loan amount.

- Any additional fees or add-ons (extended warranties, paint protection, etc.).

- The total amount you are financing.

Common mistakes to avoid are signing quickly under pressure. If you don’t understand something, ask for clarification. Don’t be afraid to take the contract home to review it if necessary.

4. Don’t Be Afraid to Walk Away

This is your ultimate leverage. If a deal doesn’t feel right, if the numbers don’t add up, or if you feel pressured, be prepared to walk away. There are always other cars and other dealerships. This simple act can often prompt a better offer or give you the space to reconsider.

The Down Payment Dilemma: How Much is Enough?

While securing a car loan before buying a car focuses on the financing terms, your down payment plays a significant role in the overall affordability and structure of that loan. It’s not just about reducing your monthly payment; it’s a strategic financial move.

Importance of a Down Payment

A down payment is the initial sum of money you pay towards the purchase of a car, reducing the amount you need to borrow. Here’s why it’s so important:

- Lower Monthly Payments: A larger down payment directly reduces the principal loan amount, which in turn lowers your monthly payment.

- Reduced Total Interest Paid: Less money borrowed means less interest accrues over the life of the loan, saving you money in the long run.

- Better Loan Terms: Lenders view a significant down payment as a sign of financial stability and commitment. This can qualify you for better interest rates and more favorable loan terms.

- Avoiding "Upside Down" on Your Loan: Cars depreciate rapidly. A substantial down payment helps ensure that you don’t owe more on the car than it’s worth, especially in the early years of ownership. This "equity" can be crucial if you need to sell or trade in the car sooner than planned.

How Much Should You Put Down?

While there’s no magic number, general recommendations exist:

- New Cars: Aim for at least 10-20% of the vehicle’s purchase price. A 20% down payment is often considered ideal for new cars to help offset initial depreciation.

- Used Cars: A 10% down payment is a good starting point for used vehicles, though more is always better.

Even a small down payment is better than none. If a large down payment isn’t feasible, focus on securing the best possible interest rate and a shorter loan term to minimize total costs.

Conclusion: Empowering Your Car Buying Journey

So, do you get a car loan before buying a car? The unequivocal answer, backed by years of experience and countless successful transactions, is a resounding YES. Getting pre-approved for a car loan before you ever step foot on a dealership lot is not just a suggestion; it’s a fundamental strategy for smart auto financing.

By securing your financing first, you empower yourself with:

- Unmatched negotiation leverage.

- Absolute clarity on your budget.

- Access to the best possible interest rates.

- A streamlined, less stressful buying process.

- Protection against common dealership tactics.

This proactive approach transforms you into an informed, confident buyer, allowing you to focus on finding the perfect vehicle at the best possible price, rather than being bogged down by confusing loan terms. Remember to check your credit, compare multiple lenders, and read every document carefully.

Your next car purchase doesn’t have to be a source of anxiety. With the insights and strategies shared in this guide, you’re well-equipped to navigate the world of car financing with expertise and achieve a truly great deal. Drive smart, drive confidently!

For more tips on managing your finances and making big purchases, check out our other articles on or .