Do You Need a Car Loan to Buy a Car? Unlocking the Smart Way to Drive Home Your Next Vehicle

Do You Need a Car Loan to Buy a Car? Unlocking the Smart Way to Drive Home Your Next Vehicle Carloan.Guidemechanic.com

The dream of owning a car is a powerful one. For many, it represents freedom, independence, and convenience. But as you navigate the exciting journey of car ownership, a fundamental question often arises: Do you need a car loan to buy a car? It’s a question that doesn’t have a simple "yes" or "no" answer, but rather a nuanced exploration of personal finance, priorities, and long-term goals.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals grapple with this decision. This comprehensive guide will dissect the complexities of car financing, helping you understand whether a car loan is a necessity, a smart strategic move, or perhaps an avoidable burden. We’ll delve deep into the pros and cons of paying cash versus taking out a loan, explore crucial factors that influence your choice, and equip you with the knowledge to make an informed decision that truly benefits your financial future.

Do You Need a Car Loan to Buy a Car? Unlocking the Smart Way to Drive Home Your Next Vehicle

The Core Question: Do You Really Need a Car Loan?

Let’s cut straight to the chase. No, you absolutely do not inherently need a car loan to buy a car. If you have enough cash readily available to cover the full purchase price of the vehicle you desire, you can certainly buy it outright. This method offers distinct advantages, primarily freedom from debt and interest payments.

However, for a significant portion of the population, purchasing a car with cash isn simply not feasible. Vehicles, especially new ones, represent a substantial investment. This is where car loans step in, transforming a large, immediate expense into manageable monthly payments. The decision, therefore, isn’t about whether a loan is required in a universal sense, but whether it’s the right choice for your specific financial situation.

Buying a Car with Cash: The Ideal Scenario (and its Realities)

Imagine walking into a dealership, pointing to your dream car, and paying for it in full with a single transfer. This scenario, while appealing, comes with its own set of considerations.

The Undeniable Advantages of Paying Cash

When you pay cash for a car, you immediately eliminate several financial headaches. You don’t owe anyone money for your vehicle, which is a fantastic feeling of freedom. This means no monthly car payments weighing down your budget.

Furthermore, paying cash means you avoid paying interest. Over the life of a typical car loan, interest charges can add hundreds or even thousands of dollars to the total cost of the vehicle. By paying upfront, every dollar you spend goes directly towards the car itself, not to the lender.

Finally, owning your car outright provides immediate equity. There’s no lien on your title, giving you complete control. Should you decide to sell the car in the future, the proceeds are entirely yours, without needing to satisfy a loan first.

The Often-Overlooked Disadvantages and Opportunity Costs

While attractive, paying cash isn’t always the best financial move for everyone. The most significant drawback is the potential for tying up a large sum of your capital. This money could otherwise be earning returns in investments, contributing to a retirement fund, or serving as a crucial emergency fund.

Based on my experience, draining your savings to buy a car outright can leave you vulnerable to unexpected expenses. What if your roof needs repair, or you face a medical emergency shortly after buying the car? Having a robust emergency fund is paramount for financial security, and sacrificing it for a car purchase can be a risky gamble.

Another consideration is the opportunity cost. If your money could be invested in something that yields a higher return than the interest rate you’d pay on a car loan, then financing might actually be the smarter move. For example, if you can get a car loan at 5% APR, but you can invest your cash in a diversified portfolio yielding 8-10% annually, you’d be financially better off taking the loan and investing your cash.

When Paying Cash Makes Sense

Paying cash is an excellent option if you have a substantial emergency fund already in place, no high-interest debt (like credit card debt), and sufficient disposable income that the car purchase won’t deplete your financial security. It’s particularly appealing for buying a used car where the total cost is more manageable, or if you simply prefer the peace of mind that comes with being debt-free.

When It Might Not Be the Best Idea

It’s generally not advisable to pay cash if it means depleting your emergency savings, delaying important investments (like retirement contributions), or if you have other high-interest debts that could be paid off instead. Remember, a car depreciates quickly, while your savings and investments, ideally, should grow.

The World of Car Loans: Why Most People Choose Them

For the vast majority of car buyers, financing through a loan is the most practical path to vehicle ownership. Car loans offer flexibility and allow individuals to acquire reliable transportation without liquidating all their assets.

Accessibility to Better Cars

Car loans make it possible to purchase a newer, more reliable, or safer vehicle than you might be able to afford with cash upfront. This can be crucial for families, daily commuters, or those who need a specific type of vehicle for work or personal needs. By spreading the cost over several years, you can access a wider range of options that better suit your lifestyle.

Preserving Cash for Other Investments or Emergencies

One of the biggest advantages of a car loan is that it allows you to keep your savings intact. This preserved capital can then be allocated to other important financial goals, such as a down payment on a home, funding an education, or building a more robust emergency fund. It’s a strategic move to maintain financial liquidity.

Pro tips from us: Always prioritize your emergency fund. It should ideally cover 3-6 months of living expenses. If buying a car with cash would dip into this fund, a loan might be the wiser choice.

Building Credit History

For those looking to establish or improve their credit score, a car loan can be an effective tool. Making consistent, on-time payments demonstrates financial responsibility to credit bureaus. A strong payment history on an installment loan, like a car loan, contributes positively to your credit mix and overall score, which can be beneficial for future borrowing needs like mortgages.

Key Factors to Consider Before Getting a Car Loan

If you decide that a car loan is the right path for you, there are several critical factors you must understand and evaluate. These elements will significantly impact the terms of your loan and your overall financial health.

Your Credit Score: The Gateway to Better Rates

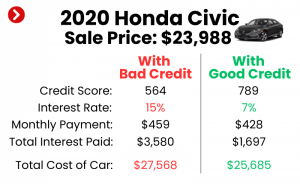

Your credit score is arguably the most important factor in securing a favorable car loan. Lenders use this three-digit number to assess your creditworthiness and determine the risk of lending to you. A higher credit score (generally above 700) indicates a lower risk, translating into lower interest rates and better loan terms.

Conversely, a lower credit score means lenders perceive you as a higher risk, which will likely result in a higher interest rate, increasing the total cost of your loan. Before even looking at cars, check your credit score. You can get free credit reports annually from major credit bureaus.

Pro tips from us: If your credit score isn’t where you’d like it to be, take steps to improve it before applying for a car loan. Pay down existing debts, especially credit card balances, and ensure there are no errors on your credit report. For more detailed guidance, consider reading our article on Understanding Your Credit Score: A Beginner’s Guide (simulated internal link).

The Importance of a Down Payment

While it’s possible to get a car loan with no money down, making a significant down payment is almost always a smart move. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan.

A substantial down payment also helps you avoid being "upside down" on your loan, a situation where you owe more on the car than it’s worth. This can happen quickly with new cars due to rapid depreciation. Aim for at least 10-20% of the car’s purchase price, if possible.

Understanding Interest Rates (APR)

The Annual Percentage Rate (APR) is the true cost of borrowing money. It includes not just the interest rate but also any fees associated with the loan. A lower APR means less money paid back to the lender over time. Interest rates can vary widely based on your credit score, the loan term, the lender, and even the current economic climate.

Common mistakes to avoid are not shopping around for the best APR. Many buyers accept the first loan offer from the dealership, often without realizing they could get a better rate elsewhere. Get pre-approved by multiple lenders – banks, credit unions, and online lenders – before you even step onto the car lot. This gives you leverage in negotiations.

Choosing the Right Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A shorter loan term means higher monthly payments but less interest paid overall. A longer loan term results in lower monthly payments but significantly more interest over the life of the loan.

Based on my experience, many buyers are tempted by longer terms to achieve lower monthly payments. However, be wary of excessively long terms. An 84-month loan means you’ll be paying for a car that is rapidly depreciating for seven years, likely owing more than it’s worth for a good portion of that time. Balance affordability with the total cost.

Your Debt-to-Income (DTI) Ratio

Lenders look at your debt-to-income (DTI) ratio to determine your ability to handle new debt. This ratio compares your total monthly debt payments to your gross monthly income. A high DTI ratio (generally above 43%) signals to lenders that you might be overextended, making it harder to qualify for a loan or get a favorable rate. Ensure your current debt load is manageable before adding a car payment.

Budgeting Beyond the Monthly Payment

The car’s purchase price and loan payment are just the beginning of your expenses. You must also budget for car insurance, fuel, maintenance, repairs, registration fees, and potential parking costs. These ongoing costs can quickly add up, so factor them into your overall budget before committing to a car purchase. For help with this, you might find our article on Budgeting for a Car: A Comprehensive Guide (simulated internal link) useful.

Alternatives to Traditional Car Loans

While traditional car loans are common, they aren’t the only way to finance a vehicle. Understanding alternatives can open up different possibilities depending on your financial situation and needs.

Personal Loans for Car Buying

A personal loan is an unsecured loan, meaning it doesn’t require collateral like the car itself. You receive a lump sum of cash, which you then use to buy the car, and repay the loan in fixed monthly installments. The advantage is that the car is immediately yours, with no lien.

However, personal loans often come with higher interest rates than secured car loans, especially for those with average credit. This is because the lender takes on more risk without collateral. They can be a good option if you have excellent credit and prefer the simplicity, or if you’re buying an older, less expensive car where a traditional auto loan might not be available.

Leasing a Car

Leasing isn’t buying, but it’s a popular alternative for acquiring a new car. When you lease, you essentially rent the car for a set period (typically 2-4 years) and pay for its depreciation during that time. Monthly lease payments are generally lower than loan payments for the same vehicle.

Leasing is ideal for those who enjoy driving new cars every few years, prefer lower monthly payments, and don’t drive excessive mileage. However, you don’t own the car at the end of the lease, and there are often mileage restrictions and wear-and-tear clauses that can lead to additional fees.

Public Transport and Ride-Sharing

For some, especially those living in urban areas with robust public transportation systems, owning a car might not be a necessity at all. Relying on buses, trains, subways, and ride-sharing services like Uber or Lyft can be significantly cheaper than the total cost of car ownership, which includes payments, insurance, fuel, and maintenance. This option is worth considering if your lifestyle allows for it.

The Car Buying Journey: A Step-by-Step Guide

Regardless of whether you choose to pay cash or take a loan, navigating the car buying process effectively is key. Here’s a structured approach:

- Assess Your Needs and Budget: Before anything else, define what kind of car you need (size, features, fuel efficiency) and, critically, how much you can truly afford, including all ongoing costs.

- Check Your Credit (If Considering a Loan): Obtain your credit report and score. This step is non-negotiable for anyone looking to finance.

- Get Pre-Approved for a Loan (If Applicable): Shop around with banks, credit unions, and online lenders to get pre-approved. This gives you a clear budget and negotiating power at the dealership.

- Research Vehicles: Use online resources, reviews, and consumer reports to narrow down models that fit your needs and budget. Compare prices, reliability, and safety features.

- Test Drive: Never buy a car without test driving it first. Pay attention to how it handles, accelerates, brakes, and if it’s comfortable for you.

- Negotiate: Don’t be afraid to negotiate the price of the car. If you have a pre-approved loan, you can negotiate the cash price of the car first, separate from financing.

- Finalize the Purchase: Read all paperwork carefully before signing. Understand every fee, term, and condition.

Pro Tips for Smart Car Financing

Navigating the world of car loans can feel overwhelming, but a few expert tips can make a significant difference.

- Don’t Just Focus on the Monthly Payment: This is a common trap. A lower monthly payment often comes with a longer loan term and much more interest paid over time. Always ask for the total cost of the loan.

- Read the Fine Print: Every document you sign, especially the loan agreement, contains crucial details. Understand the interest rate, fees, prepayment penalties (if any), and what happens if you miss a payment.

- Avoid Unnecessary Add-ons: Dealerships often try to sell you extended warranties, paint protection, or VIN etching. While some might have value, many are overpriced or unnecessary. Research their value and decline if you don’t need them.

- Consider Refinancing Later: If your credit score improves significantly after you get your initial loan, or if interest rates drop, you might be able to refinance your car loan for a lower APR, saving you money.

- Know Your Trade-in Value Separately: If you’re trading in your old car, negotiate its value independently of the new car’s price. This prevents the dealership from bundling the figures and obscuring the actual deals.

Common Mistakes to Avoid When Buying a Car

Based on my experience helping people with their car purchases, certain pitfalls appear repeatedly. Avoiding these can save you a lot of money and stress.

- Not Budgeting for Total Cost of Ownership: As mentioned earlier, ignoring insurance, maintenance, and fuel costs can lead to financial strain even with an affordable monthly payment.

- Falling for "Zero Down" Without Understanding Implications: While appealing, a zero-down loan means you finance the entire cost of the car, often leading to being upside down on the loan sooner. If you can afford a down payment, make one.

- Only Getting One Loan Offer: This is a cardinal sin of car financing. Always compare offers from at least three different lenders to ensure you’re getting the most competitive rate.

- Ignoring Your Credit Report: Errors on your credit report can negatively impact your loan terms. Review it well in advance to dispute any inaccuracies.

- Buying More Car Than You Need/Can Afford: It’s easy to get swept up in the excitement of a new vehicle. Stick to your budget and needs, not just your wants. Overspending can lead to financial stress down the line.

Conclusion: Your Smart Path to Car Ownership

So, do you need a car loan to buy a car? The answer is clear: not always, but often, it’s the most practical and financially sound approach for many. The ultimate decision rests on your individual financial health, your goals, and your comfort level with debt.

Whether you choose to pay cash and enjoy immediate debt-free ownership, or strategically utilize a car loan to preserve your savings and build credit, the key is to be informed, prepared, and disciplined. By understanding the factors involved, shopping smartly for both the vehicle and the financing, and avoiding common mistakes, you can drive home your next car with confidence, knowing you’ve made a decision that aligns with your long-term financial well-being. Drive smart, not just fast!