Does Getting A Car Loan Help Your Credit? The Ultimate Deep Dive

Does Getting A Car Loan Help Your Credit? The Ultimate Deep Dive Carloan.Guidemechanic.com

Navigating the world of personal finance can often feel like deciphering a complex code, especially when it comes to credit scores. One common question that surfaces for many aspiring car owners is: "Does getting a car loan help your credit?" It’s a straightforward question with a nuanced answer, and understanding it is crucial for anyone looking to build a strong financial future.

As an expert blogger and professional SEO content writer, I’ve delved deep into this topic to bring you a comprehensive guide. This article isn’t just about answering a yes or no; it’s about equipping you with the knowledge to make informed decisions that genuinely benefit your credit health. Let’s explore how an auto loan can be a powerful tool for credit building, or, if managed poorly, a significant detriment.

Does Getting A Car Loan Help Your Credit? The Ultimate Deep Dive

The Nuanced Answer: Yes, But With Conditions

To cut straight to the chase: Yes, getting a car loan can absolutely help your credit score, but only under specific, responsible conditions. It’s not a magic bullet, but rather a tool that, when used correctly, can significantly contribute to a healthy credit profile.

The key differentiator lies in how you manage the loan. A car loan offers a unique opportunity to demonstrate financial reliability and discipline. When you consistently meet your payment obligations, you send a clear message to lenders that you are a trustworthy borrower.

However, the inverse is also true. Mishandling a car loan can lead to severe and lasting damage to your credit. This makes understanding the underlying mechanisms of credit scoring and loan management paramount.

Understanding Your Credit Score: The Foundation

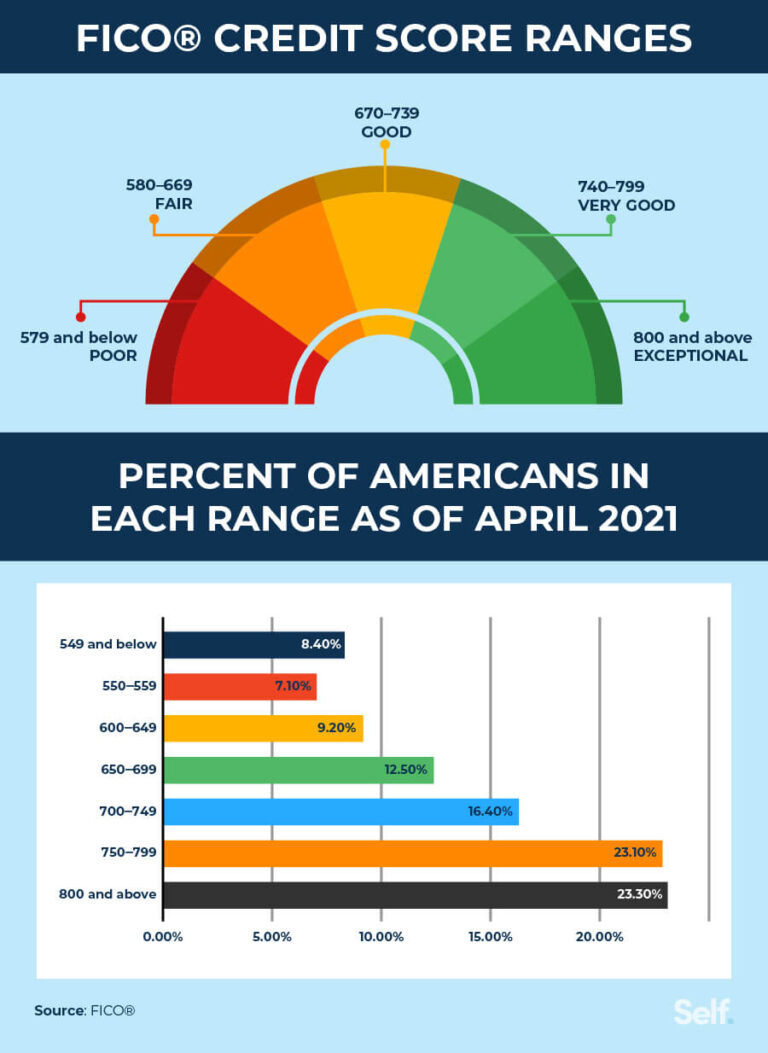

Before we dive deeper into car loans, it’s essential to grasp what a credit score is and why it holds so much weight. Your credit score is a three-digit number that represents your creditworthiness. It’s essentially a report card on your financial responsibility.

What Exactly Is a Credit Score?

Credit scores, most commonly FICO Scores and VantageScores, are numerical summaries derived from the information in your credit reports. These scores help lenders quickly assess the risk of lending money to you. A higher score typically indicates a lower risk.

This score isn’t just used for loans; it impacts everything from mortgage rates and credit card approvals to insurance premiums and even rental applications. Understanding its components is the first step towards taking control of your financial future.

Why Is Your Credit Score So Important?

A strong credit score is your passport to better financial opportunities. It unlocks lower interest rates on loans, better terms on credit cards, and can even influence your ability to secure housing or certain jobs. Conversely, a poor score can limit your options and cost you significantly more over time.

Based on my experience, many people underestimate the far-reaching impact of their credit score until they need it most. It’s not just about borrowing; it’s about financial flexibility and peace of mind.

Key Factors Influencing Your Credit Score (FICO Model)

Credit scores are calculated using several factors, each weighted differently. Understanding these factors will illuminate exactly how a car loan can play a role.

1. Payment History (35%)

This is the most critical factor. It tracks whether you pay your bills on time. Every single payment, whether on a credit card, mortgage, or car loan, is recorded.

Consistent, on-time payments are the bedrock of a strong credit score. Conversely, even one late payment can have a significant negative impact, especially if your credit history is relatively short. Lenders want to see a reliable track record.

2. Amounts Owed (30%)

This factor considers how much debt you currently have. It looks at the total amount you owe across all your accounts and compares it to your available credit. For revolving credit like credit cards, this is known as credit utilization.

While a car loan adds to your total debt, it’s categorized as an installment loan. Lenders assess your debt-to-income ratio and your overall ability to manage the total amount of debt you carry. Keeping your overall debt manageable is key.

3. Length of Credit History (15%)

This factor measures how long your credit accounts have been open, both the oldest and the newest, and the average age of all your accounts. A longer credit history with well-managed accounts generally looks better to lenders.

When you take out a new car loan, it initially lowers the average age of your accounts. However, as the loan matures and you make consistent payments over several years, it eventually contributes positively to the length of your credit history.

4. Credit Mix (10%)

This factor assesses the different types of credit you have. Lenders like to see a healthy mix of both revolving credit (like credit cards) and installment credit (like car loans or mortgages).

Having a car loan demonstrates your ability to manage a different type of debt compared to a credit card. This diversification shows lenders that you are capable of handling various financial obligations responsibly.

5. New Credit (10%)

This factor considers how many new credit accounts you’ve recently opened and how many hard inquiries have been made on your credit report. Each time you apply for new credit, a "hard inquiry" is typically made, which can temporarily ding your score.

Applying for multiple car loans within a short period can signal to lenders that you might be in financial distress or are taking on too much new debt. It’s important to be strategic about when and how you apply for new credit.

How a Car Loan Can Positively Impact Your Credit

Now that we understand the core components of a credit score, let’s explore precisely how a car loan, when managed diligently, can become a significant asset to your credit profile.

1. Building a Positive Payment History

This is, without a doubt, the most powerful benefit of a car loan. Every single on-time payment you make is a positive entry on your credit report, directly bolstering the largest component of your credit score (35%).

Imagine consistently making your car loan payments for three, four, or even five years. That’s dozens of positive data points demonstrating your reliability as a borrower. Lenders view this as a strong indicator that you will honor future financial commitments.

Based on my experience working with countless individuals on their credit journeys, establishing a solid payment history through an installment loan like a car loan is one of the most effective strategies for long-term credit building. It provides a steady stream of positive activity.

2. Diversifying Your Credit Mix

Having a variety of credit types can be beneficial for your score. Most people start with revolving credit, such as credit cards. A car loan introduces installment credit into your profile.

Installment loans are different because they have a fixed payment amount over a set period, leading to a definite end date. This contrasts with revolving credit, where the balance can fluctuate, and there’s no fixed payoff schedule.

Demonstrating that you can responsibly manage both types of credit—revolving and installment—shows a broader financial capability to lenders. This positively impacts the "Credit Mix" portion of your score (10%).

3. Establishing a Credit History (Especially for New Borrowers)

If you’re new to credit and have a thin file (meaning few or no credit accounts), a car loan can be an excellent way to get started. It provides a substantial entry point into the credit world.

Many young adults or those who have previously avoided debt find themselves in a "catch-22": they need credit to get credit. A car loan, often with a co-signer or a slightly higher interest rate initially, can break this cycle.

Pro tips from us: If you’re a new borrower, consider a more modest, affordable vehicle. This makes the loan more manageable and increases your chances of consistent on-time payments, setting you up for success.

4. Increasing Your Average Age of Accounts (Eventually)

Initially, adding a new loan will likely decrease the average age of your accounts. This is a temporary effect, and its impact is generally minimal if you have other established accounts.

However, as years pass and you continue to make payments on your car loan, that account matures. A long-standing, well-managed car loan becomes an old, positive account on your report, eventually contributing to a higher average age of accounts and strengthening your "Length of Credit History" (15%).

The Flip Side: When a Car Loan Can Hurt Your Credit

While the potential benefits are clear, it’s equally important to understand the risks. A car loan is a significant financial commitment, and missteps can have severe consequences for your credit score.

1. Late or Missed Payments

This is the most damaging mistake you can make. As discussed, payment history accounts for 35% of your FICO score. Even a single payment reported 30 days late can drop your score significantly.

Repeated late payments or missing payments altogether will severely impact your creditworthiness, making it harder and more expensive to borrow money in the future. Lenders interpret late payments as a high-risk behavior.

Common mistakes to avoid are underestimating the impact of just one late payment. Life happens, but setting up auto-pay or payment reminders can prevent accidental oversights that can cost you dearly.

2. Defaulting on the Loan

If you fail to make payments for an extended period, the lender may declare your loan in default. This can lead to your vehicle being repossessed.

A repossession on your credit report is a major negative mark that can stay there for up to seven years. It signals to all future lenders that you are a very high-risk borrower, making it extremely difficult to get approved for new credit.

3. Taking on Too Much Debt

While a car loan diversifies your credit mix, taking on a loan with payments you can barely afford can lead to financial strain. If your car payment consumes a large portion of your income, it can make it challenging to pay other bills or save money.

This can lead to a high debt-to-income ratio, which lenders consider when assessing your ability to take on more debt. Over-extending yourself financially increases the risk of missed payments across all your accounts.

4. Multiple Hard Inquiries in a Short Period

When you apply for a car loan, lenders perform a "hard inquiry" on your credit report. Each inquiry can cause a small, temporary dip in your score (typically a few points).

If you apply for multiple car loans from different lenders over several weeks or months, each application could result in a separate hard inquiry, compounding the negative effect. However, FICO and VantageScore models usually have a "rate shopping window" (typically 14-45 days).

Within this window, multiple auto loan inquiries are often treated as a single inquiry, recognizing that you’re shopping for the best rate, not necessarily taking on multiple loans. Pro tip: Do all your car loan shopping within a short timeframe to minimize the impact.

5. High Interest Rates & Unmanageable Payments

Accepting a car loan with a very high interest rate, perhaps due to a lower credit score, can lead to disproportionately high monthly payments. These payments might stretch your budget thin, making it difficult to maintain other financial obligations.

A high-cost loan can trap you in a cycle where you’re constantly struggling to meet payments, increasing the risk of default. Always ensure the total cost and monthly payment are truly affordable for your budget.

Strategies for Maximizing Credit Benefits from a Car Loan

If you’ve decided a car loan is right for you, implementing smart strategies will ensure it acts as a credit-building powerhouse rather than a liability.

1. Choose the Right Loan for Your Budget

Before you even step foot in a dealership, determine what you can realistically afford. This isn’t just about the monthly payment, but the total cost of ownership, including insurance, fuel, and maintenance.

Opt for a loan amount and term that results in a comfortable monthly payment. A smaller, more manageable loan is far better for your credit than an expensive one you struggle to pay.

2. Make On-Time Payments – Every Single Time

This cannot be stressed enough. Set up automatic payments from your checking account, or create calendar reminders. Do whatever it takes to ensure your payments are always submitted by the due date.

Even better, try to pay a few days early if possible. This builds a robust payment history, which is the cornerstone of good credit.

3. Keep Your Debt-to-Income Ratio Healthy

Before taking on a car loan, assess your current debt load. Your debt-to-income ratio (DTI) is a crucial metric. Lenders prefer a DTI of 36% or less, though some may approve up to 43%.

A healthy DTI shows you have enough income to comfortably manage your existing debts, including your new car loan. Avoid taking on other significant debts while you are paying off your car loan.

4. Understand the Loan Terms Fully

Read the fine print. Know your interest rate, the total amount you’ll pay over the life of the loan, any fees, and the exact repayment schedule. Don’t be afraid to ask questions until everything is clear.

Understanding your loan ensures there are no surprises and helps you plan your budget accurately. This proactive approach prevents potential payment issues down the line.

5. Monitor Your Credit Report Regularly

Pull your free credit reports from AnnualCreditReport.com at least once a year. Review them for accuracy and to track your progress. Look for any errors or suspicious activity.

Pro tips from us: Monitoring your credit reports helps you catch identity theft early and ensures that your on-time car loan payments are being reported correctly, maximizing their credit-building potential.

6. Avoid Excessive Credit Applications

While shopping for a car loan, limit your applications to a concentrated period (the "rate shopping window" discussed earlier). Beyond that, try to space out applications for other types of credit.

Constantly applying for new credit, especially without a clear need, can make you appear desperate for funds, which can be a red flag for lenders.

7. Consider a Shorter Loan Term (If Affordable)

While a longer loan term means lower monthly payments, it also means paying more interest over time. If your budget allows, opting for a shorter loan term (e.g., 3-4 years instead of 5-6) can save you money on interest and get you out of debt faster.

Paying off a loan sooner, as long as all payments are on time, will still provide the credit-building benefits while reducing your overall financial obligation. This also frees up your monthly budget sooner for other financial goals.

Alternative Ways to Build Credit (Beyond Car Loans)

While a car loan can be effective, it’s not the only path to building credit. Diversifying your credit-building strategies can be a smart move.

- Secured Credit Cards: These cards require a cash deposit that acts as your credit limit. They’re designed for people with no credit or bad credit to build a positive payment history.

- Credit Builder Loans: Offered by some credit unions and small banks, these loans put the money into a savings account while you make payments. Once the loan is paid off, you get access to the funds.

- Authorized User Status: If a trusted family member with excellent credit adds you as an authorized user on their credit card, their positive payment history can reflect on your report.

- Paying Bills On Time: Services like Experian Boost allow you to get credit for on-time utility and telecom payments. Some rental payment services also report to credit bureaus.

- Small Personal Loans: If a car loan isn’t feasible, a small personal loan (if available) can also act as an installment loan to build credit.

You can learn more about these methods and other strategies for improving your financial health by checking out our related article on (Internal Link Placeholder).

The Bottom Line: Responsible Borrowing is Key

So, does getting a car loan help your credit? Absolutely, but with a resounding emphasis on responsible borrowing and meticulous payment management. A car loan is a significant financial commitment that, when handled correctly, can be a powerful catalyst for a robust credit score.

It offers a clear path to demonstrating reliability, diversifying your credit mix, and building a long, positive payment history. However, it also carries the substantial risk of damaging your credit if payments are missed or if you overextend yourself financially.

Ultimately, the decision to take on a car loan should be a carefully considered one, rooted in a solid understanding of your financial capabilities and a commitment to on-time payments. Your credit score is a reflection of your financial behavior, and a car loan provides an excellent opportunity to showcase your best financial self.

Conclusion

In conclusion, leveraging a car loan to boost your credit score is a strategy that can yield significant long-term benefits. By making informed choices about the loan itself, committing to timely payments, and diligently monitoring your credit health, you can transform an auto loan into a cornerstone of your financial stability.

Remember, every financial decision you make contributes to your overall credit narrative. Choose wisely, stay disciplined, and watch your credit score flourish. Your journey to a stronger financial future starts with educated decisions today. For more in-depth insights into managing various types of debt and their impact on your credit, consider reading this valuable resource on Understanding Debt Types (External Link Placeholder). Start your credit journey wisely and drive towards financial success!