Don’t Just Drive Away: The Ultimate Guide to Comparing Two Car Loans Like a Pro

Don’t Just Drive Away: The Ultimate Guide to Comparing Two Car Loans Like a Pro Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone for many. The thrill of getting behind the wheel of your dream vehicle can be intoxicating. However, amidst the excitement, one crucial step often gets overlooked: meticulously comparing your car loan options.

Many buyers simply accept the first financing offer presented, often from the dealership. This common oversight can cost you thousands of dollars over the life of your loan. As an expert in personal finance and auto financing, I’ve seen countless individuals pay more than they needed to, simply because they didn’t take the time to compare two car loans effectively.

Don’t Just Drive Away: The Ultimate Guide to Comparing Two Car Loans Like a Pro

This comprehensive guide is designed to empower you. We’ll dive deep into every aspect of auto loan comparison, providing you with the knowledge and strategies to secure the best possible deal. Our ultimate goal is to help you make an informed decision, save money, and drive away with confidence, knowing you’ve mastered your car financing.

Why You MUST Compare Car Loan Offers

You wouldn’t buy the first car you see without test-driving others, would you? The same principle applies, even more critically, to your car loan. Financing is often the largest financial commitment associated with your vehicle purchase.

Save Significant Money

The primary reason to compare two car loans (or more!) is to save money. Even a small difference in the interest rate can translate into hundreds or even thousands of dollars in total interest paid over several years. This is money that could stay in your pocket or be used for other financial goals.

Understand Your Financial Commitment

Comparing offers forces you to look beyond just the monthly payment. It helps you grasp the full scope of your financial obligation, including fees, total interest, and the loan’s duration. This holistic understanding is vital for responsible budgeting and long-term financial health.

Gain Negotiation Power

When you have multiple pre-approved loan offers in hand, you walk into the dealership with significant leverage. You’re not relying solely on their financing department. Based on my experience, having competing offers allows you to negotiate not just the car’s price, but also the financing terms.

Avoid Buyer’s Remorse

Rushing into a loan agreement can lead to regret later on. Taking the time to compare ensures you’re confident in your decision. It eliminates the nagging feeling that you might have gotten a better deal elsewhere, contributing to a more satisfying car ownership experience.

The Essential Metrics: What to Look For When You Compare Two Car Loans

When you have two car loan offers sitting side-by-side, it’s easy to get overwhelmed by the numbers. However, by focusing on key metrics, you can quickly cut through the noise and identify the better deal. Let’s break down each crucial factor in detail.

Interest Rate vs. Annual Percentage Rate (APR)

This is perhaps the most fundamental distinction you need to understand. Many people confuse these two terms, but they are critically different.

The interest rate is simply the percentage a lender charges you for borrowing the principal amount. It’s the cost of borrowing the money, expressed as a percentage of the loan amount. While important, it doesn’t tell the whole story.

The Annual Percentage Rate (APR), on the other hand, represents the true annual cost of your loan. It includes not only the interest rate but also any additional fees associated with the loan, such as origination fees, processing fees, or discount points. This comprehensive figure is standardized across lenders, making it the most accurate metric for direct comparison.

Pro tip from us: Always compare two car loans based on their APR, not just the interest rate. The loan with a slightly higher interest rate but no fees might actually have a lower APR than a loan with a lower interest rate but hefty upfront charges. For a deeper dive into understanding these rates, you might find this external resource on Investopedia’s explanation of APR vs. Interest Rate helpful.

Loan Term (Length of the Loan)

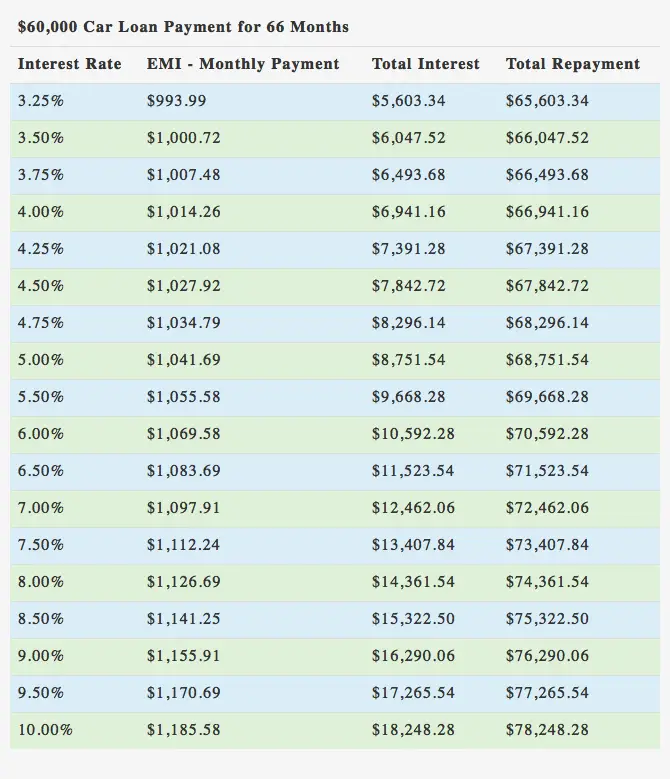

The loan term refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor has a significant impact on both your monthly payment and the total amount of interest you’ll pay over the life of the loan.

A shorter loan term generally means higher monthly payments. However, you’ll pay off the loan much faster and accrue significantly less total interest. This is often the financially savvier choice if your budget can accommodate the higher payments.

Conversely, a longer loan term results in lower monthly payments, which can make a more expensive car seem more affordable. The downside is that you’ll pay substantially more in total interest over time, and you risk owing more on the car than it’s worth (being "upside down" or having negative equity) as it depreciates.

Common mistake to avoid: Many buyers fall into the trap of only focusing on the lowest possible monthly payment. While affordability is key, stretching out a loan for too long can be a very costly decision in the long run. When you compare two car loans, always consider the total cost over the full term, not just the monthly outlay.

Monthly Payment Amount

While not the only factor, your monthly payment is undeniably important for budgeting purposes. It needs to comfortably fit within your regular expenses without straining your finances. An unmanageable monthly payment can lead to financial stress or even default.

When comparing, ensure the proposed monthly payment for each loan is realistic for your budget. Don’t forget to factor in other car ownership costs, such as insurance, fuel, maintenance, and potential repairs. These can add up quickly and impact your true affordability.

It’s a good practice to use an online car loan calculator to play around with different scenarios. Input the loan amount, interest rate, and term to see how changes affect your monthly payment. This helps you visualize your financial commitment clearly.

Fees and Charges

Car loans can come with various fees that aren’t always immediately obvious. These can inflate the overall cost of your financing if you’re not careful. Always ask for a detailed breakdown of all associated charges.

Common fees include:

- Origination fees: A charge for processing the loan.

- Documentation fees: For preparing the loan paperwork.

- Processing fees: Similar to origination, for handling the loan.

- Application fees: Less common, but sometimes charged to apply.

These fees can sometimes be rolled into the loan amount, increasing your principal and therefore the interest you pay. When you compare two car loans, explicitly ask each lender for a complete list of all fees and how they are applied. Transparency is key here.

Prepayment Penalties

A prepayment penalty is a fee charged by some lenders if you pay off your loan early, either by making extra payments or by refinancing. Lenders implement these to recoup some of the interest they would have earned if the loan ran its full course.

If you anticipate having extra cash to pay down your principal faster, or if you think you might refinance in the future, a prepayment penalty could cost you. It’s crucial to check for this clause in any loan agreement.

Common mistake to avoid: Assuming all loans allow penalty-free early repayment. Always read the fine print or directly ask the lender, "Are there any prepayment penalties associated with this loan?" before signing.

Down Payment Requirements

A down payment is the initial sum of money you pay upfront towards the purchase of the car, reducing the amount you need to borrow. While not strictly a loan term, it directly impacts the loan amount and, consequently, your interest payments and monthly installments.

Lenders often prefer a larger down payment as it reduces their risk. A substantial down payment can also help you secure a lower interest rate. It’s generally recommended to put down at least 10-20% of the car’s purchase price if possible.

When you compare two car loans, consider how different down payment scenarios might affect the offers. A loan that requires a smaller down payment might seem appealing initially, but it could lead to higher monthly payments and more interest over time.

Lender Reputation and Customer Service

Beyond the numbers, the reputation of your lender and the quality of their customer service are vital considerations. You’ll be in a relationship with this institution for the duration of your loan.

Research online reviews, check their ratings with consumer protection agencies like the Better Business Bureau (BBB), and ask for recommendations. Consider how easy it is to contact their customer service and how responsive they are to inquiries. A lender with a strong track record of transparency and helpfulness can make your loan experience much smoother.

Loan Type (Secured vs. Unsecured)

Most car loans are secured loans, meaning the car itself serves as collateral. If you default on the loan, the lender has the right to repossess the vehicle. This collateral reduces the lender’s risk, which often translates to lower interest rates for the borrower.

While less common for car purchases, some personal loans are unsecured, meaning there’s no collateral. These typically come with higher interest rates because the lender takes on more risk. When comparing car loans, you’ll almost always be looking at secured options, but it’s good to understand the distinction.

A Step-by-Step Guide to Effectively Compare Two Car Loans

Now that you understand the key metrics, let’s walk through a practical, step-by-step process to put this knowledge into action. This structured approach will ensure you don’t miss any critical details.

Step 1: Get Pre-Approved from Multiple Lenders

Before you even step foot on a dealership lot, seek pre-approval from several different financial institutions. This includes your bank, credit unions, and reputable online lenders. Pre-approval gives you a clear idea of the interest rate and loan terms you qualify for, based on your creditworthiness.

Why is this so powerful? Pre-approval provides you with a baseline offer. It separates the car-buying process from the financing process, allowing you to negotiate for the car’s price independently. Based on my experience, having competing offers in hand gives you significant leverage and confidence. Remember, pre-approval typically involves a "soft" credit inquiry, which doesn’t impact your credit score, but a full application will trigger a "hard" inquiry.

Step 2: Gather All the Details

Once you have at least two strong loan offers, it’s time to meticulously gather all the pertinent information for each. The best way to do this is to create a simple comparison spreadsheet.

For each loan offer, list out the following:

- Lender Name

- Offered APR (not just interest rate)

- Loan Term (in months)

- Estimated Monthly Payment

- Total Loan Amount (Principal)

- Any Upfront Fees (origination, documentation, etc.)

- Prepayment Penalties (Yes/No)

- Down Payment Requirement

- Any Specific Conditions or Clauses

Having this information organized side-by-side makes the comparison process much clearer.

Step 3: Calculate the TRUE Cost

Don’t just look at the monthly payment. While it’s important for budgeting, the most revealing metric for comparison is the total cost of the loan. This includes the principal amount borrowed plus all the interest you’ll pay over the loan term, as well as any upfront fees.

You can use online auto loan calculators to input the APR, loan amount, and term to get an accurate estimate of the total interest paid. Compare this figure directly between the two loans. A loan with a slightly lower monthly payment but a longer term might end up costing you significantly more in total interest.

Step 4: Read the Fine Print

This step is non-negotiable. Before committing to any loan, you must thoroughly read the entire loan agreement. Don’t skim. Pay close attention to sections detailing:

- Interest calculation methods

- Late payment penalties

- Default clauses

- Any additional charges not explicitly discussed

- Prepayment penalty clauses

If there’s anything you don’t understand, ask the lender for clarification. A reputable lender will be happy to explain every detail. Common mistakes to avoid are signing without fully comprehending every clause in the contract.

Step 5: Factor in Your Budget and Future Goals

Beyond the numbers on the loan agreement, consider how each loan fits into your broader financial picture. Can you comfortably afford the monthly payments for the entire term, even if unexpected expenses arise?

Think about your future financial goals:

- Are you planning to buy a house soon?

- Do you have other significant debts you’re trying to pay off?

- Are you saving for retirement or a large purchase?

A car loan, especially a long one, can impact these goals. Choose the loan that aligns best with your current budget and future aspirations, providing both affordability and financial flexibility.

Step 6: Negotiate (If Possible)

Armed with competing offers and a clear understanding of your preferences, don’t be afraid to negotiate. If one lender offers a slightly better APR but another has no prepayment penalty, you might be able to leverage one offer against the other.

For example, you could approach Lender A with Lender B’s APR and ask if they can match or beat it, especially if you prefer Lender A for other reasons (e.g., better customer service, existing relationship). Remember, lenders want your business, and they often have some flexibility, particularly for well-qualified borrowers. For more expert advice on this, you might find our article on Tips for Negotiating Your Best Car Deal insightful.

Common Pitfalls and How to Avoid Them

Even with the best intentions, car buyers can fall into common traps when securing financing. Being aware of these pitfalls can save you from costly mistakes.

Only Looking at the Monthly Payment

As we’ve emphasized, focusing solely on the lowest monthly payment is a major pitfall. A low monthly payment often comes with a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

Not Checking for Prepayment Penalties

Many buyers assume they can pay off their loan early without issue. Failing to confirm the absence of prepayment penalties can lead to unexpected fees if you decide to accelerate your payments or refinance.

Ignoring Fees and Add-Ons

Dealerships or lenders might try to bundle in various "add-ons" like extended warranties, GAP insurance, or etching protection directly into your loan. While some might be beneficial, always evaluate them separately and ensure you understand their cost and necessity. Never assume they are mandatory.

Not Getting Pre-Approved

Walking into a dealership without pre-approval from an outside lender puts you at a disadvantage. You lose your baseline for comparison and may feel pressured to accept the dealership’s financing without truly understanding if it’s the best offer available to you.

Rushing the Decision

Car buying, and particularly car financing, should not be a rushed process. Take your time to compare offers, read the fine print, and ask questions. A rushed decision is often a regretted decision.

Pro Tips for Smart Car Loan Comparison

To truly master the art of comparing car loans, keep these expert tips in mind:

Cast a Wide Net

Don’t just rely on your primary bank. Get quotes from a diverse range of sources, including local credit unions (which often have very competitive rates), national banks, and specialized online auto loan lenders. The more offers you gather, the better your chances of finding the absolute best deal.

Check Your Credit Score First

Your credit score is the single most important factor influencing the interest rate you’ll be offered. Before you even start applying for loans, get a free copy of your credit report and score. This allows you to understand your standing and address any errors. For more expert advice on managing your finances, check out our guide on Understanding Your Credit Score.

Understand the "Shopping Around" Period

When you apply for multiple car loans within a short period (typically 14-45 days, depending on the credit scoring model), credit bureaus often count these as a single inquiry. This "rate shopping" period is designed to allow consumers to compare offers without unduly harming their credit score. Use this window wisely!

Don’t Be Afraid to Walk Away

If you’re not getting an offer that you feel comfortable with, or if a lender isn’t transparent, be prepared to walk away. There are always other options available, and your financial well-being is paramount.

Consider Refinancing Down the Line

Even if you don’t get the absolute best rate upfront, remember that refinancing is always an option. If your credit score improves, or if interest rates drop, you might be able to refinance your car loan later to secure a lower rate and save money. This can be a smart strategy for long-term savings.

Conclusion: Drive Away with Confidence

Choosing a car loan is a significant financial decision that impacts your budget for years to come. By taking the time to thoroughly compare two car loans (or more!), you’re not just saving money; you’re taking control of your financial future.

Remember to look beyond just the monthly payment. Focus on the APR, understand all fees, consider the loan term, and scrutinize the fine print. Equip yourself with multiple pre-approvals, organize your findings, and don’t hesitate to negotiate.

With the strategies and insights shared in this comprehensive guide, you are now well-prepared to navigate the complexities of auto financing like a seasoned expert. Drive away not just in your new car, but with the confidence that you’ve secured the best possible deal for your financial well-being. Happy driving!