Doubling Down on Driving Dreams: Can You Have Two Co-Signers On A Car Loan?

Doubling Down on Driving Dreams: Can You Have Two Co-Signers On A Car Loan? Carloan.Guidemechanic.com

Securing a car loan can often feel like navigating a complex maze, especially for those with a limited credit history, a lower credit score, or an ambitious car purchase in mind. Many aspiring car owners find themselves wondering about the best strategies to boost their approval chances and secure favorable terms. One common question that arises is: Can you have two co-signers on a car loan?

The short and definitive answer is yes, you absolutely can have two co-signers on a car loan. This often-overlooked option can significantly strengthen your application, opening doors to better interest rates and a higher likelihood of approval. In this comprehensive guide, we’ll delve deep into the mechanics of having multiple co-signers, exploring the myriad benefits, potential pitfalls, and essential considerations to ensure a smooth journey to car ownership.

Doubling Down on Driving Dreams: Can You Have Two Co-Signers On A Car Loan?

Based on my extensive experience in the auto finance world, understanding the nuances of co-signing, particularly with multiple parties, is crucial. It’s not just about getting approved; it’s about setting up a sustainable financial arrangement for everyone involved. Let’s embark on this detailed exploration together.

The Foundation: Understanding the Role of a Co-Signer

Before we dive into the specifics of having two co-signers, it’s vital to grasp the fundamental role a single co-signer plays in a car loan application.

A co-signer is essentially a second party who agrees to be legally responsible for the loan if the primary borrower defaults on payments. They don’t typically take ownership of the vehicle, but their financial strength and creditworthiness are factored into the lender’s decision. This arrangement primarily benefits the primary borrower by mitigating the lender’s risk.

Lenders often require a co-signer when the primary applicant’s financial profile isn’t strong enough on its own. This could be due to a low credit score, a short credit history, an unstable income, or a high debt-to-income ratio. The co-signer’s promise to pay acts as a safety net, making the loan less risky for the financial institution.

For the primary borrower, securing a co-signer can mean the difference between approval and rejection. It can also lead to more attractive loan terms, such as a lower interest rate, which can save thousands of dollars over the life of the loan. It’s a powerful tool for those looking to establish or rebuild their credit while acquiring a necessary asset.

Doubling Down: The Power of Two Co-Signers on a Car Loan

Now, let’s address the core question: why would someone consider having two co-signers, and how does it work?

Having two co-signers on a car loan is essentially an amplification of the security provided by a single co-signer. When you bring two financially strong individuals onto your loan application, you are presenting an even more robust financial picture to the lender. This significantly reduces the perceived risk associated with lending to the primary borrower.

Lenders assess risk by looking at factors like credit scores, income stability, and existing debt. If the primary borrower’s profile is weak, adding one co-signer helps. Adding two co-signers, each with a solid credit history and reliable income, creates a much stronger guarantee. It tells the lender that there are now three parties, rather than just two, who are legally obligated to ensure the loan is repaid.

This option is particularly common and beneficial for young adults just starting their credit journey, individuals who have experienced financial setbacks, or those looking to finance a more expensive vehicle than their individual profile might typically allow. It’s a strategic move to leverage collective financial strength for a shared goal.

The Undeniable Advantages of Having Two Co-Signers

Opting for two co-signers can unlock a range of significant benefits that might otherwise be out of reach for a single borrower. These advantages extend beyond just securing approval, impacting the overall cost and feasibility of your car loan.

First and foremost, the increased likelihood of loan approval is a major draw. With two additional individuals vouching for the loan’s repayment, lenders are far more comfortable extending credit. This is especially true if the primary borrower has a very low credit score or no credit history at all.

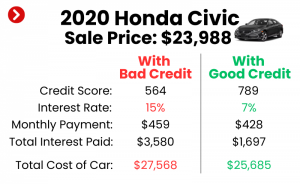

Secondly, you stand a much better chance of securing more favorable interest rates. Interest rates are directly tied to the perceived risk of the loan. With two strong co-signers, that risk is substantially lowered, often translating into a lower Annual Percentage Rate (APR). Over the lifespan of a car loan, even a percentage point difference can save you hundreds or even thousands of dollars.

Another key advantage is the potential for a higher loan amount. If you’re eyeing a specific vehicle that’s slightly above what your individual income or credit score might typically qualify you for, two co-signers can bridge that gap. Their combined financial strength can justify a larger principal amount, giving you more flexibility in your car choice.

Finally, for the primary borrower, this arrangement can be an excellent opportunity to build or rebuild credit. By consistently making on-time payments, the loan activity will be reported to credit bureaus under your name (and the co-signers’ names), positively impacting your credit score over time. This can pave the way for future financial independence. Based on my experience, many young people leverage this exact strategy to kickstart their financial journey responsibly.

Navigating the Downsides: Risks and Disadvantages to Consider

While the benefits are compelling, it’s crucial to approach having two co-signers with a clear understanding of the potential risks and disadvantages involved. This is a significant financial commitment for all parties, and open communication is paramount.

The most substantial risk lies with the co-signers themselves. Each co-signer is equally and fully responsible for the entire loan amount. If the primary borrower fails to make payments, the lender can pursue either or both co-signers for the full outstanding balance. This means their credit scores will be negatively impacted, and their assets could be at risk if they default.

Furthermore, the loan will appear on each co-signer’s credit report, impacting their debt-to-income ratio. This can potentially hinder their ability to secure their own loans (e.g., a mortgage or another car loan) in the future, as lenders will see this existing obligation. It’s a long-term commitment that affects their financial flexibility.

Relationship strain is another common pitfall. Money matters can be incredibly sensitive, and if payment issues arise, it can severely damage relationships between the primary borrower and their co-signers, whether they are family members or close friends. Clear expectations and boundaries are essential from the outset.

For the primary borrower, while you gain approval, you also take on a significant responsibility to protect your co-signers. Failing to make payments not only hurts your own credit but also directly impacts two other people. This can create a feeling of immense pressure and dependency. Common mistakes to avoid are assuming your co-signers understand the full extent of their liability or not keeping them informed about payment status.

Who Makes a Good Co-Signer (And How to Choose Two Wisely)

Selecting even one co-signer is a critical decision, but choosing two requires even more careful consideration. The individuals you select will be intrinsically linked to your financial future for the duration of the loan.

An ideal co-signer possesses several key characteristics. They should have a strong credit score – typically 700 or above – as this is what the lender will primarily be looking at to strengthen your application. They also need a stable and verifiable income, demonstrating their ability to cover payments if necessary. Furthermore, a low debt-to-income ratio shows they aren’t already overextended financially.

Beyond financial metrics, trust and open communication are non-negotiable. You need individuals you can openly discuss finances with, who understand the gravity of their commitment, and who you are confident will maintain their financial stability. Often, co-signers are close family members, such as parents or siblings, precisely because of these existing bonds of trust.

When choosing two co-signers, consider if their combined financial strength truly adds value. For instance, if one co-signer has an excellent credit score and stable income, and the second has a slightly weaker but still good profile, their combined strength will be greater than just one. There’s no requirement for co-signers to be related, but this is often the case for practical and trust reasons. Pro tips from us: have an honest conversation with each potential co-signer, separately and together, explaining the full implications before they agree. Ensure they are comfortable with the commitment.

The Application Process with Two Co-Signers: What to Expect

Applying for a car loan with two co-signers follows a similar process to a single co-signer application, but with added layers of documentation and verification. Being prepared can streamline the entire experience.

The first step is to gather all necessary documents for all three parties. This includes personal identification (driver’s license, social security number), proof of income (pay stubs, tax returns), and proof of residency for the primary borrower and both co-signers. Lenders need a complete financial picture for everyone involved.

Next, the lender will conduct credit checks on the primary borrower and both co-signers. This is a critical step where their credit scores and histories will be thoroughly scrutinized. The strength of the co-signers’ credit profiles will heavily influence the loan terms offered. Be prepared for a temporary slight dip in everyone’s credit score due to the hard inquiry.

Once approved, all three individuals will need to sign the loan agreement. This is a legally binding contract that outlines the terms, conditions, interest rate, and repayment schedule. It explicitly states that all three parties are jointly and severally liable for the full amount of the loan. It’s imperative that everyone reads and understands every clause before signing. Don’t hesitate to ask the lender questions if anything is unclear.

At the dealership or lender’s office, ensure all names are correctly spelled and all details are accurate on the final paperwork. This attention to detail prevents future complications.

Managing a Car Loan with Multiple Co-Signers Effectively

Securing the loan is just the beginning; effective management is key to a positive outcome for all parties involved. A well-managed loan protects everyone’s credit and preserves relationships.

Establish a clear payment plan and responsibility structure from day one. While the primary borrower is expected to make the payments, it’s wise to have a contingency plan. Who will be notified if a payment is missed? Will the co-signers receive payment reminders? Transparency here is crucial.

Communication is paramount. The primary borrower should regularly update the co-signers on the loan’s status, especially if any financial difficulties arise. Don’t wait until a payment is missed to inform them. Open dialogue can help address issues proactively and prevent defaults.

All parties should monitor their credit reports regularly. This ensures that payments are being reported correctly and can alert co-signers to any potential issues or missed payments by the primary borrower. Many credit monitoring services offer free access to reports.

Finally, consider strategies for removing co-signers in the future. This is often the ultimate goal for the primary borrower seeking financial independence. The most common method is refinancing the car loan once the primary borrower’s credit score has significantly improved and they can qualify for a new loan in their own name. Another option is selling the vehicle and paying off the loan, though this is less ideal. For more detailed insights into this process, you might find our article on particularly helpful.

Exploring Alternatives to Multiple Co-Signers

While having two co-signers can be a powerful solution, it’s not the only path to car ownership. Depending on your situation, other strategies might be more suitable or sustainable in the long run.

One effective alternative is to save for a larger down payment. A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk and potentially improving your chances of approval, even with a less-than-perfect credit score. It also means lower monthly payments.

Another practical option is to consider buying a less expensive car. If your budget or credit profile is limited, opting for a more affordable vehicle can make a significant difference. A lower loan amount is easier to qualify for and easier to manage without external help.

Perhaps the most empowering alternative is to focus on improving your own credit score before applying for a loan. This involves steps like paying bills on time, reducing existing debt, and disputing any errors on your credit report. While this takes time, it builds a foundation for financial independence. To learn more about actionable steps to boost your credit, a trusted resource like Experian offers excellent guidance on .

Finally, for some, a secured loan might be an option. This involves using an asset you already own (like a savings account or CD) as collateral for the loan. While not always feasible for car purchases, it can be a way to secure financing without a co-signer.

Driving Forward with Confidence and Clarity

The journey to car ownership, particularly when navigating the complexities of financing, requires careful thought and strategic planning. The question, "Can you have two co-signers on a car loan?" is met with a resounding yes, offering a viable and often advantageous pathway for many individuals. This option significantly boosts your chances of approval, secures better interest rates, and can be a powerful tool for building your credit.

However, it’s a decision that carries substantial weight for all parties involved. The shared financial responsibility and potential for relationship strain underscore the importance of transparency, trust, and clear communication. By understanding the advantages, meticulously considering the risks, and managing the loan proactively, you can transform this multi-party agreement into a successful stepping stone toward financial stability and the joy of owning your own vehicle.

Ultimately, whether you choose to leverage the power of two co-signers or explore alternative financing strategies, making an informed decision is paramount. Equip yourself with knowledge, communicate openly, and embark on your car ownership journey with confidence and clarity.