Drive Away with Confidence: Your Ultimate Guide to Guaranteed Used Car Loans

Drive Away with Confidence: Your Ultimate Guide to Guaranteed Used Car Loans Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex maze, especially when you’re facing credit challenges. Many people dream of owning a reliable vehicle but worry that a low credit score or lack of credit history will stand in their way. This is where the concept of a "Guaranteed Used Car Loan" comes into play, offering a beacon of hope for countless individuals.

But what exactly does "guaranteed" mean in this context? Is it truly a sure thing, or are there important nuances to understand? As an expert in automotive finance and a professional SEO content writer, I’ve seen firsthand how these loans can transform lives. This comprehensive guide will demystify guaranteed used car loans, explain how they work, and provide you with the essential knowledge to secure the best possible deal. Our ultimate goal is to equip you with the insights needed to drive away in a dependable used car, regardless of your credit situation.

Drive Away with Confidence: Your Ultimate Guide to Guaranteed Used Car Loans

Unpacking the "Guaranteed" Promise in Used Car Loans

The term "guaranteed" can be a bit misleading in the financial world. It rarely means everyone will automatically qualify without any conditions. Instead, in the realm of used car loans, it typically signifies a very high likelihood of approval for individuals who might otherwise struggle to get financing through traditional routes.

Think of it less as an ironclad promise for everyone and more as a commitment from specific lenders to work with a broader range of credit profiles. These lenders specialize in helping people with bad credit, no credit, or unique financial situations. They understand that life happens, and a credit score doesn’t always tell the whole story.

Who Benefits Most from These Loans?

Based on my experience, individuals who find the most value in guaranteed used car loans often fall into specific categories:

- Bad Credit History: If you’ve had past financial difficulties, such as bankruptcies, repossessions, or numerous late payments, traditional banks might turn you down. Guaranteed loans offer a viable alternative.

- No Credit History: Young adults, recent immigrants, or anyone who hasn’t used credit extensively often face a "credit Catch-22." You need credit to get credit. These loans provide an entry point.

- Low Income or Unconventional Employment: Lenders focusing on guaranteed approval often have more flexible income requirements, considering various income sources beyond a standard 9-to-5 job.

- Previous Loan Denials: If you’ve been turned down elsewhere, these specialized lenders are often your next best step.

These loans are designed to bridge the gap, providing access to essential transportation while also offering an opportunity to rebuild or establish a positive credit history.

How Do They Differ from Traditional Car Loans?

The primary distinction lies in the lender’s risk assessment. Traditional lenders, like major banks, rely heavily on credit scores (FICO, VantageScore) to gauge risk. A lower score typically means a higher perceived risk, often leading to denial or very high interest rates.

Guaranteed approval lenders, on the other hand, employ a more holistic approach. While they still consider your credit report, they place greater emphasis on other factors. They’re looking for signs of current financial stability and your ability to repay, even if your past credit isn’t perfect. This often involves a deeper dive into your income, employment history, and down payment capabilities.

Why Used Cars Are a Smart Choice for Challenging Credit

When credit is a concern, opting for a used car over a new one is often a strategic and financially sound decision. This choice isn’t just about saving money upfront; it significantly improves your chances of loan approval and sets you up for greater long-term success.

Lower Cost, Lower Risk

Used cars generally come with a lower purchase price compared to their brand-new counterparts. This immediately translates to a smaller loan amount needed. A smaller loan means less risk for the lender, making them more willing to approve applicants with less-than-perfect credit. The lower principal also means lower monthly payments, which directly improves your debt-to-income ratio, a key metric for lenders.

Furthermore, depreciation is a major factor. New cars lose a significant portion of their value the moment they’re driven off the lot. Used cars have already undergone this initial depreciation, meaning they hold their value better over the life of your loan. This reduces the risk of being "upside down" on your loan, where you owe more than the car is worth.

Easier Approval, Greater Accessibility

Because the loan amount is smaller and the asset (the used car) has a more stable value, lenders specializing in guaranteed approval find used car loans less risky. This translates into more accessible financing options for you. They understand that a used car is often a necessity for work, school, and daily life, and they aim to provide that critical access.

Pro tips from us: Focus on vehicles that are 3-5 years old with reasonable mileage. These cars offer a great balance of reliability and affordability, making them attractive to both borrowers and lenders. Avoid vehicles that are too old or have excessive mileage, as lenders may see them as a higher risk due to potential maintenance issues.

An Opportunity to Rebuild Credit

Securing a guaranteed used car loan isn’t just about getting a car; it’s a powerful tool for financial rehabilitation. By making consistent, on-time payments, you actively build a positive payment history, which is the most influential factor in your credit score.

Every payment you make contributes to improving your creditworthiness. Over time, this can open doors to better interest rates on future loans, credit cards, and even mortgages. It’s a stepping stone towards greater financial freedom and stability.

Key Factors Lenders Consider Beyond Your Credit Score

While your credit score plays a role, lenders offering guaranteed used car loans look at a broader picture. They want to assess your current ability to repay the loan, not just your past financial performance. Understanding these factors will help you prepare a stronger application.

Income Stability and Employment History

This is perhaps the most critical factor. Lenders need assurance that you have a consistent and reliable source of income to make your monthly payments. They typically look for:

- Proof of Employment: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns for self-employed individuals.

- Minimum Income Requirements: While flexible, most lenders will have a minimum monthly income threshold (e.g., $1,500 – $2,000 before taxes).

- Employment Longevity: A stable work history (e.g., 6 months to a year or more at the same job) demonstrates reliability.

Based on my experience, lenders are often more lenient on the type of income, including social security, disability, or structured settlements, as long as it’s verifiable and stable.

Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to determine if you can comfortably afford an additional car payment without becoming overextended.

For example, if your gross monthly income is $3,000 and your total monthly debt payments (rent/mortgage, credit cards, other loans) are $1,000, your DTI is 33%. Lenders typically prefer a DTI ratio below 40-50%, including the new car payment. A lower DTI indicates less financial strain and a higher capacity for repayment.

The Power of a Down Payment

Making a down payment is one of the most effective ways to strengthen your loan application, especially with credit challenges. Here’s why:

- Reduces Loan Amount: A larger down payment means you borrow less, which lowers your monthly payments and the total interest paid over the life of the loan.

- Shows Commitment: It demonstrates to the lender that you are financially invested in the purchase and serious about repayment.

- Builds Equity Immediately: You start with equity in the car, reducing the risk of being upside down on your loan.

- Lowers Lender Risk: Less money loaned means less risk for the lender, making them more likely to approve your application.

Pro tips from us: Even a modest down payment of 10-20% can significantly improve your chances and potentially lead to better loan terms. Don’t underestimate its impact.

The Role of a Co-signer

If your credit is particularly challenging, or your income is on the lower side, a co-signer can be a game-changer. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments.

This significantly reduces the risk for the lender, as they have another party to pursue for repayment. However, common mistakes to avoid are not fully understanding the co-signer’s responsibility. It’s a serious commitment that affects their credit as well, so choose someone you trust and ensure you’re both clear on the implications.

Vehicle Choice and Value

The specific used car you choose also impacts your loan approval. Lenders prefer vehicles that hold their value well and are not excessively old or high-mileage.

- Age and Mileage: Most lenders have limits on the age and mileage of vehicles they will finance (e.g., no older than 10-12 years, no more than 150,000 miles).

- Market Value: The car’s value, typically assessed using guides like Kelley Blue Book (KBB) or NADA, ensures the loan amount is reasonable compared to the vehicle’s worth. This protects both you and the lender.

Residency Stability

Lenders also consider how long you’ve lived at your current address. A stable residency history suggests a more settled life and can be seen as a positive indicator of reliability. Frequent moves, especially without a clear reason, can sometimes raise red flags, though this is usually a secondary factor.

The Application Process for Your Guaranteed Used Car Loan

Securing a guaranteed used car loan is a streamlined process, but understanding each step will empower you to navigate it successfully. It’s not just about filling out forms; it’s about presenting yourself as a reliable borrower.

Step 1: Pre-qualification vs. Pre-approval

Before you even step onto a dealership lot, understanding the difference between pre-qualification and pre-approval is crucial.

- Pre-qualification: This is an initial, soft inquiry that estimates what you might qualify for. It doesn’t impact your credit score and gives you a general idea of your borrowing power. It’s a great starting point for budgeting.

- Pre-approval: This involves a more thorough review, often including a hard credit inquiry, and results in a conditional offer of financing. With pre-approval, you know the exact loan amount, interest rate, and terms you’re eligible for before shopping for a car.

Pro tips from us: Always aim for pre-approval. It gives you significant leverage at the dealership, allowing you to focus on the car price rather than the financing.

Step 2: Gathering Necessary Documents

Preparation is key. Having all your documents ready will expedite the application process. You’ll typically need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Proof of Income: Recent pay stubs (2-3 months), W-2s, or tax returns (for self-employed).

- Bank Statements: Usually 1-3 months to show financial activity and stability.

- References: Sometimes required, particularly for buy-here-pay-here dealerships.

Common mistakes to avoid are presenting incomplete or outdated documents. This can cause significant delays and frustration.

Step 3: Where to Apply

Several avenues exist for guaranteed used car loans, each with its own characteristics:

- Dealerships (Subprime Specialists): Many dealerships, particularly larger ones, have dedicated finance departments that work with a network of subprime lenders. They can often match you with a loan product that fits your credit profile. Some specialize entirely in "bad credit auto loans."

- Buy-Here-Pay-Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They offer on-site financing, making approval often truly "guaranteed" if you meet their basic income requirements. However, be aware that interest rates can be higher, and vehicle selection might be limited.

- Online Lenders: Numerous online platforms specialize in connecting individuals with challenging credit to a network of lenders. They offer convenience and the ability to compare multiple offers from the comfort of your home. Websites like Auto Credit Express or Capital One Auto Finance (for specific credit tiers) are good examples.

- Credit Unions: While sometimes less advertised for "guaranteed" loans, many credit unions are member-focused and more willing to work with individuals facing credit challenges, especially if you have a relationship with them.

Step 4: Understanding the Loan Offer

Once you receive an offer, scrutinize every detail. Don’t just look at the monthly payment.

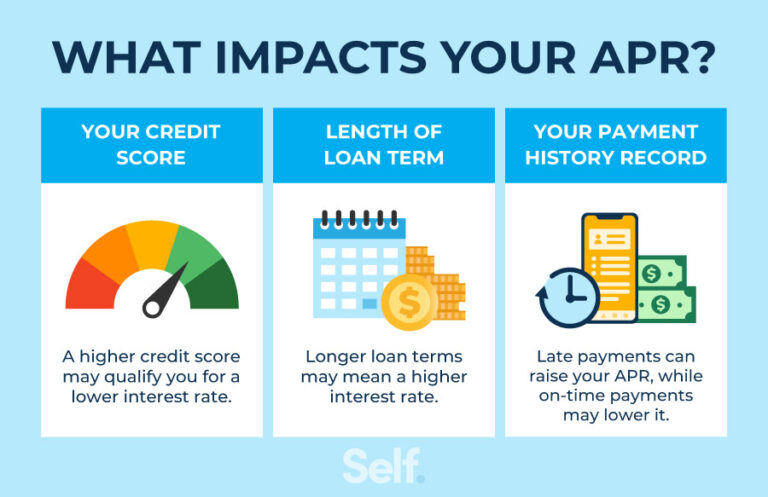

- Interest Rate (APR): This is the cost of borrowing money, expressed as an annual percentage. With challenging credit, expect a higher APR, but always compare offers.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). Longer terms mean lower monthly payments but more interest paid over time.

- Fees: Look out for origination fees, documentation fees, or other charges that can increase the overall cost.

- Total Cost of the Loan: Calculate the total amount you’ll pay over the life of the loan (principal + interest + fees).

Pro tips from us: Don’t just accept the first offer. Compare at least 2-3 different loan offers if possible. Even a small difference in APR can save you hundreds, if not thousands, of dollars over the loan term. For more insights on interest rates, you might find our article helpful.

Maximizing Your Chances: Tips for Approval and Better Terms

Even with "guaranteed" options available, you can take proactive steps to not only secure approval but also to get more favorable loan terms. These strategies demonstrate your commitment and reduce perceived risk for lenders.

1. Save for a Significant Down Payment

As discussed, a down payment is your strongest ally. Aim for at least 10-20% of the vehicle’s purchase price. This immediately lowers your loan amount, reduces your monthly payments, and signals to the lender that you’re a serious and responsible borrower. The more you put down, the better your chances of approval and potentially a lower interest rate.

2. Improve Your Credit Score (Even Slightly)

While these loans are for those with imperfect credit, even small improvements can make a difference. Before applying:

- Check Your Credit Report: Obtain free copies from AnnualCreditReport.com. Dispute any errors.

- Pay Down Small Debts: Reducing your credit card balances or paying off small outstanding loans can quickly improve your credit utilization ratio, boosting your score.

- Catch Up on Late Payments: Bringing any delinquent accounts current shows lenders you’re getting your finances in order.

For a deeper dive into credit improvement, check out our .

3. Consider a Co-signer (Wisely)

If you have a trusted family member or friend with good credit who is willing to co-sign, it can significantly enhance your application. Their strong credit profile can help you secure approval and potentially a much lower interest rate.

However, common mistakes to avoid are not fully discussing the responsibilities. Ensure your co-signer understands they are equally liable for the loan. If you miss payments, their credit will also be negatively impacted. It’s a big ask, so approach it with full transparency.

4. Choose an Affordable and Practical Vehicle

Resist the urge to overspend. Lenders are more comfortable financing a reliable, affordable used car than a luxury model, especially for applicants with credit challenges.

- Stick to Your Budget: Factor in not just the monthly payment but also insurance, fuel, maintenance, and registration costs.

- Practicality Over Flash: A moderately priced sedan or SUV is usually a safer bet than a high-performance or luxury vehicle. This shows financial prudence.

5. Shop Around for Lenders

Don’t settle for the first offer you receive. Apply with a few different lenders (online platforms, credit unions, dealerships) within a short period (typically 14-45 days). Multiple hard inquiries within this timeframe are often treated as a single inquiry by credit bureaus for rate shopping purposes, minimizing the impact on your score.

Comparing offers allows you to find the best interest rate and terms, saving you money in the long run.

6. Demonstrate Income Stability and Prove Everything

Provide all requested documentation promptly and accurately. Lenders appreciate thoroughness. If you have any unusual income sources or employment gaps, be prepared to explain them clearly and concisely. The more transparent and organized you are, the more confidence you instill in the lender.

The Role of Dealerships and Specialized Lenders

Understanding the different types of lenders and dealerships that offer guaranteed used car loans is vital for making an informed decision. Each has its unique approach and suitability for various situations.

Buy-Here-Pay-Here (BHPH) Dealerships

BHPH dealerships are unique because they are both the car seller and the lender. This means they offer in-house financing, often making approval truly "guaranteed" for most applicants who can prove a stable income.

- Pros: Very high approval rates, often don’t rely heavily on credit scores, quick approval process.

- Cons: Typically higher interest rates (sometimes significantly so), limited vehicle selection (often older, higher mileage cars), and payments may be required weekly or bi-weekly.

- Best For: Individuals with severe credit challenges who have been denied elsewhere and need a car immediately, provided they can manage the payment structure and higher rates.

Pro tips from us: If considering a BHPH loan, thoroughly inspect the vehicle, understand all terms, and ensure you can comfortably meet the frequent payment schedule. These loans can be a lifeline but require careful management.

Subprime Lenders

Subprime lenders specialize in providing loans to individuals with less-than-perfect credit. They are typically banks, finance companies, or divisions of larger financial institutions that have specific programs for higher-risk borrowers.

- How They Work: They assess risk differently, focusing more on current income and ability to repay, often requiring a down payment or co-signer. They operate within a network that many traditional dealerships partner with.

- Pros: Offer a pathway to financing when traditional banks won’t, can help rebuild credit, often more competitive rates than BHPH.

- Cons: Higher interest rates than prime loans, potentially longer loan terms, may have stricter vehicle requirements.

- Best For: Those with bad credit who have stable income and can afford a moderate down payment, looking for a balance between approval and manageable terms.

Online Lending Platforms

The digital age has brought a surge of online lenders and marketplaces that connect borrowers with various financing options, including those for challenging credit.

- How They Work: You fill out one application, and it’s submitted to a network of lenders, who then provide offers. This allows for quick comparisons without visiting multiple physical locations.

- Pros: Convenience, ability to compare multiple offers from various lenders, often a wide range of loan products.

- Cons: Can be overwhelming with choices, requires careful review of terms, not all online lenders are equally reputable.

- Best For: Individuals who prefer the convenience of online shopping and want to explore multiple options to find the best rate.

Common mistakes to avoid are not thoroughly researching the reputation of online lenders. Always look for positive reviews and check for clear terms and conditions. The Federal Trade Commission (FTC) offers excellent resources on smart car buying, which is always a good external source to consult. You can find valuable information on their website, .

After Approval: Managing Your Loan and Rebuilding Credit

Getting approved for a guaranteed used car loan is a significant achievement, but the journey doesn’t end there. The real value comes from successfully managing your loan and leveraging it as a tool to improve your financial future.

Making Timely Payments – The Cornerstone of Credit Rebuilding

This cannot be stressed enough: make every payment on time, every single month. Your payment history is the most crucial factor in your credit score (accounting for 35% of your FICO score).

- Set Reminders: Use calendar alerts, set up automatic payments from your bank account, or sign up for payment reminders from your lender.

- Prioritize Car Payments: Understand that missing a payment not only incurs late fees but also significantly damages your credit score, undoing all the good work you’re trying to achieve.

Based on my experience, consistency is key. Even if you’ve had past struggles, demonstrating a solid year or two of on-time car payments can dramatically improve your credit profile.

Avoiding Repossession

Repossession is a serious consequence of defaulting on your loan. It means the lender takes back your vehicle due to non-payment. This has devastating effects:

- Credit Damage: A repossession will severely harm your credit score and remain on your report for seven years, making it incredibly difficult to obtain credit in the future.

- Financial Loss: You lose your car, any money you’ve already paid into the loan, and potentially face additional fees from the lender for the repossession and sale of the vehicle.

If you foresee difficulty making a payment, contact your lender immediately. They may be willing to work with you on a temporary payment plan or deferral rather than initiating repossession. Communication is always better than avoidance.

Refinancing Options Later

Once you’ve consistently made payments for 6-12 months and your credit score has improved, you may qualify to refinance your car loan.

- What is Refinancing? It involves taking out a new loan, usually with a lower interest rate, to pay off your current, higher-interest loan.

- Benefits: A lower interest rate means lower monthly payments and less interest paid over the life of the loan. It can save you significant money.

- When to Consider: After your credit score has improved, interest rates have dropped, or your financial situation has stabilized.

Pro tips from us: Keep an eye on your credit score and interest rate trends. Refinancing can be a smart move to further optimize your loan and accelerate your journey to financial health.

How This Loan Can Improve Your Financial Future

A guaranteed used car loan, when managed responsibly, is more than just a means to transportation. It’s an investment in your financial future.

- Credit Score Boost: Consistent payments directly contribute to a higher credit score.

- Access to Better Rates: An improved score opens doors to lower interest rates on future loans, credit cards, and even mortgages.

- Financial Discipline: Successfully managing a car loan instills valuable financial habits that can serve you well across all aspects of your life.

- Increased Opportunities: Reliable transportation can lead to better job opportunities, reduced commute times, and greater overall quality of life.

Drive Away with Confidence

Securing a guaranteed used car loan is an achievable goal, even with credit challenges. It requires understanding how these specialized loans work, knowing what lenders look for, and being prepared to navigate the application process strategically. By focusing on income stability, making a down payment, and meticulously managing your loan, you’re not just buying a car; you’re investing in your financial future.

Don’t let past credit issues deter you from getting the reliable transportation you need. With the right knowledge and a proactive approach, you can drive away with confidence, knowing you’ve taken a significant step towards rebuilding your credit and achieving greater financial freedom. Start your journey today and empower yourself with the wheels you deserve.