Drive Away with Less: Your Ultimate Guide to Low Down Payment Car Loans

Drive Away with Less: Your Ultimate Guide to Low Down Payment Car Loans Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering unparalleled freedom and convenience. However, the thought of a substantial upfront payment can often be a major roadblock. This is where low down payment car loans come into play, opening the door for countless individuals to secure the vehicle they need without draining their savings.

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. Based on my experience, understanding the nuances of low down payment options is crucial for making an informed decision. This comprehensive guide is designed to empower you with all the knowledge you need, from understanding the pros and cons to navigating the application process, ensuring you drive away with confidence.

Drive Away with Less: Your Ultimate Guide to Low Down Payment Car Loans

What Exactly Are Low Down Payment Car Loans?

A low down payment car loan is precisely what it sounds like: a financing option that requires a smaller percentage of the vehicle’s purchase price paid upfront compared to traditional loans. While a typical down payment might range from 10% to 20%, a low down payment could be as little as 5%, or even less in some specific scenarios. In some rare cases, you might even encounter "zero down payment" offers, though these often come with their own set of considerations.

These loans are particularly appealing to individuals who have limited immediate cash but possess a stable income and a decent credit history. They allow you to conserve your savings for emergencies, home improvements, or other essential expenses, rather than tying up a large sum in a car purchase. It’s about managing your immediate cash flow while still achieving your transportation goals.

The concept isn’t about avoiding a down payment entirely, but rather minimizing the initial financial burden. This flexibility makes car ownership more accessible, especially for first-time buyers or those recovering from unexpected expenses. However, it’s vital to understand that a smaller upfront investment typically means a larger amount financed, which has implications for your overall loan.

The Allure and Reality: Pros and Cons of Low Down Payment Car Loans

While the appeal of driving off the lot with minimal cash out of pocket is undeniable, it’s essential to weigh the benefits against the potential drawbacks. Understanding both sides will help you determine if a low down payment car loan is the right fit for your financial situation.

The Advantages: Why Low Down Payments Are Attractive

One of the most significant advantages is immediate access to a vehicle. You don’t have to wait months or years to save up a large sum, allowing you to address your transportation needs quickly. This is particularly beneficial if your current vehicle has unexpectedly broken down or if you’re starting a new job that requires a reliable commute.

Another major benefit is the ability to preserve your savings and emergency funds. Life is unpredictable, and having a financial cushion is incredibly important. A low down payment means more of your hard-earned money stays in your bank account, ready for unexpected medical bills, home repairs, or job loss. It offers peace of mind knowing you have liquid assets available.

Low down payment loans also offer flexibility for those with limited upfront cash. Not everyone has thousands of dollars readily available for a down payment, especially younger buyers, recent graduates, or individuals managing other significant expenses. These loans make car ownership a tangible reality for a broader demographic, removing a major barrier to entry.

Finally, for those with limited credit history, securing a low down payment car loan can be an opportunity to build or improve your credit score. Making consistent, on-time payments demonstrates financial responsibility, which can positively impact your credit profile over time. This can open doors to better interest rates and terms on future loans, from mortgages to personal loans.

The Disadvantages: The Other Side of the Coin

While beneficial, low down payment loans do come with their own set of financial considerations. The most prominent is higher monthly payments. Since you’re financing a larger portion of the car’s price, your principal loan amount is higher. Spread over the same loan term, this inevitably leads to a larger payment each month, which can strain your budget if not carefully managed.

Consequently, you will also end up paying more interest over the loan term. A larger principal loan amount means more interest accrues over the life of the loan. Even if the interest rate is the same, the total dollar amount of interest paid will be higher compared to a loan with a substantial down payment. This increases the overall cost of the vehicle significantly.

A common pitfall with low down payment loans is a higher risk of negative equity, also known as being "upside down" on your loan. This occurs when the outstanding balance of your loan is more than the current market value of your car. Cars depreciate quickly, especially in the first few years. With a small down payment, you might owe more than the car is worth very early in the loan term, making it difficult to sell or trade in the vehicle without incurring a financial loss.

Furthermore, lenders might impose stricter qualification criteria or higher interest rates for low down payment loans, especially if your credit score isn’t stellar. The lower your upfront investment, the higher the risk for the lender, which they often mitigate by offering less favorable terms to less qualified applicants. You might also find that some lenders are simply unwilling to offer very low down payment options.

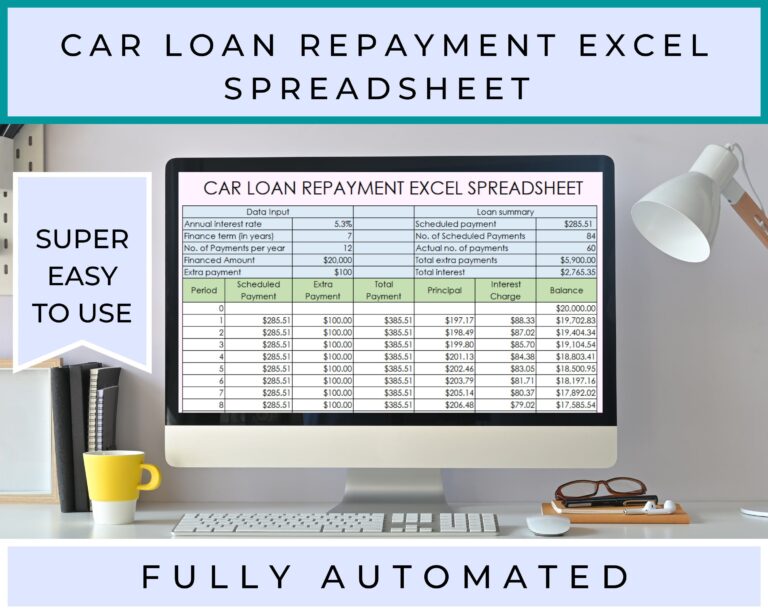

Pro tips from us: Always request a full amortization schedule from your lender. This document clearly outlines how much interest you’ll pay over the loan’s lifetime and helps you visualize the true cost of your financing decision.

Who Qualifies? Key Factors Lenders Consider

Securing a low down payment car loan isn’t just about finding a willing lender; it’s about presenting yourself as a reliable borrower. Lenders evaluate several key financial indicators to assess your ability to repay the loan. Understanding these factors can significantly improve your chances of approval and help you secure better terms.

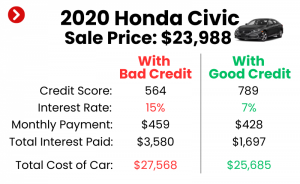

The cornerstone of any loan approval is your credit score. This three-digit number is a snapshot of your creditworthiness, reflecting your payment history, outstanding debts, length of credit history, and types of credit used. A higher credit score (generally above 670 for "good" credit) indicates lower risk to lenders, making them more likely to approve you for a low down payment loan with competitive interest rates. Conversely, a lower score might lead to higher interest rates or a requirement for a larger down payment.

Your debt-to-income ratio (DTI) is another critical factor. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. Lenders typically prefer a DTI of 36% or less, though some might go up to 43%. A lower DTI indicates that you have sufficient income to comfortably manage your existing debts and take on a new car loan without becoming overextended.

Income stability and employment history also play a significant role. Lenders want to see proof of consistent earnings, ideally from the same employer for at least two years. This demonstrates a reliable source of income for repaying the loan. Freelancers or those with irregular income might need to provide more extensive financial documentation or have a longer history of self-employment to qualify.

The vehicle choice itself can influence loan approval. Lenders often view newer, more reliable cars as less risky because they hold their value better and are less likely to require expensive repairs that could impact your ability to pay. Extremely old or high-mileage vehicles might be harder to finance with a low down payment due to their rapid depreciation and higher risk of mechanical issues.

Finally, the loan-to-value (LTV) ratio is paramount for low down payment loans. This ratio compares the amount you’re borrowing to the car’s appraised value. With a low down payment, your LTV will be higher, meaning the lender is taking on more risk relative to the car’s immediate value. Lenders have internal LTV limits, and exceeding them might require a larger down payment or result in a denial.

Strategies for Securing the Best Low Down Payment Car Loan

Navigating the car loan market can feel overwhelming, but with the right strategies, you can significantly improve your chances of securing a favorable low down payment car loan. It’s all about preparation and informed decision-making.

One of the most crucial strategies is to shop around and compare offers. Don’t limit yourself to the first lender you find or the dealership’s financing department. Explore options from various sources, including traditional banks, local credit unions, and reputable online lenders. Each institution has different lending criteria and rates, and what works for one might not be the best for another.

Getting pre-approved for a loan before you even step foot on a dealership lot is a game-changer. Based on my experience, pre-approval gives you immense negotiating power. It provides a clear understanding of your borrowing limit and the interest rate you qualify for, effectively turning you into a cash buyer. This allows you to focus on negotiating the car’s price, rather than being swayed by monthly payment figures that might hide unfavorable loan terms.

Know your credit score and history inside and out. Obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review them for any inaccuracies. Dispute any errors promptly, as even small mistakes can negatively impact your score. A good credit score is your strongest asset when seeking competitive low down payment loan terms.

Budget wisely, focusing not just on the monthly payment, but on the total cost of the loan over its entire term. Factor in interest, potential fees, insurance, and ongoing maintenance. A low monthly payment might seem attractive, but if it’s spread over a very long term, you could end up paying significantly more in interest overall. Use online calculators to project the total cost.

If your credit isn’t strong, consider a co-signer. A co-signer with excellent credit and a stable financial history can significantly improve your chances of approval and help you secure a better interest rate. However, remember that a co-signer is equally responsible for the loan, so choose someone you trust and who understands the commitment.

When you’re at the dealership, negotiate beyond just the price of the car. Discuss the entire loan package: the interest rate, the loan term, and any additional fees. Sometimes, a dealer might be willing to slightly adjust the vehicle price or throw in an incentive to secure your business, especially if you come in with a strong pre-approval.

Finally, if you have an existing vehicle, don’t forget the power of a trade-in. The value of your trade-in can directly serve as a down payment, reducing the amount you need to finance. Research your car’s trade-in value beforehand using reputable sources like Kelley Blue Book or Edmunds, so you have a realistic expectation.

Common Mistakes to Avoid When Seeking a Low Down Payment Car Loan

The path to a low down payment car loan can be fraught with missteps if you’re not careful. Common mistakes can lead to higher costs, financial strain, or even loan denial. Being aware of these pitfalls will help you navigate the process more smoothly and save you money in the long run.

One of the most common mistakes is focusing solely on the monthly payment. While an affordable monthly payment is important, it doesn’t tell the whole story. Dealers sometimes stretch loan terms to 72 or even 84 months to achieve a low monthly figure, but this significantly increases the total interest paid and the risk of negative equity. Always consider the total cost of the loan and the interest rate.

Another critical error is not getting pre-approved. As discussed, pre-approval gives you leverage and a clear understanding of your financial standing. Without it, you’re walking into a dealership blind, making it easier for them to manipulate the numbers to their advantage, often focusing on monthly payments rather than the overall deal.

Many buyers also make the mistake of ignoring the total cost of the loan and the interest paid. A low down payment means you’re financing more, which means more interest. Failing to calculate the grand total can lead to a rude awakening about how much you’re actually paying for the car over its lifetime. Always ask for the total amount to be paid back.

Skipping the fine print in the loan agreement is a recipe for disaster. Loan documents can be lengthy and filled with jargon, but every clause is important. Overlooking details about prepayment penalties, late fees, or specific terms and conditions can lead to unexpected charges or limitations later on.

Common mistakes to avoid are also underestimating additional costs of car ownership. Beyond the loan, you’ll have insurance premiums, registration fees, maintenance, and fuel costs. A low down payment doesn’t alleviate these ongoing expenses. Ensure your budget can comfortably accommodate all aspects of car ownership, not just the loan payment.

Falling for "zero down" offers without understanding the implications is another pitfall. While tempting, these offers often come with higher interest rates, longer loan terms, or stricter qualification requirements, ultimately costing you more over time. Always read the fine print and compare it to other loan options.

Finally, letting the dealer run multiple credit checks without your consent can negatively impact your credit score. Each "hard inquiry" can slightly lower your score. Ideally, you should have your pre-approval in hand, and the dealer should only need to run one check to verify your existing offer.

Alternative Options to Reduce Your Upfront Costs

While low down payment car loans are a popular choice, they aren’t the only way to minimize your initial outlay. Exploring alternative options can help you find a financial solution that best fits your needs and budget, potentially saving you money or offering different benefits.

One distinct alternative is leasing a vehicle. Instead of buying, leasing allows you to essentially rent a new car for a fixed period, typically two to four years. Lease payments are often lower than loan payments for the same car, and the upfront costs (like a security deposit or first month’s payment) are usually much less than a traditional down payment. However, you don’t own the car, and there are mileage limits and potential wear-and-tear charges.

Another practical approach is to buy a less expensive used car. The total cost of a used car is naturally lower than a new one, which means the required down payment will also be significantly less. You might even find that you can afford to pay cash for a reliable used vehicle, eliminating the need for a loan and interest payments altogether. This also reduces the risk of negative equity.

For those who have a little more time, saving up a larger down payment remains the most financially prudent strategy. Even an extra few hundred or a thousand dollars can make a noticeable difference in your monthly payment and the total interest you pay. A larger down payment reduces the principal loan amount, lessens your monthly burden, and reduces your risk of going upside down on the loan.

Maximizing your trade-in value is also a powerful strategy. Instead of just accepting the first offer from a dealership, take the time to clean your car, address minor repairs, and research its market value. Getting multiple trade-in offers from different dealerships or even selling your car privately could net you a higher amount, which then directly contributes to your down payment.

The Fine Print: What to Look For in Your Loan Agreement

Once you’ve been approved for a low down payment car loan, the excitement of a new car can make it tempting to rush through the paperwork. However, this is precisely the moment to exercise extreme caution and diligence. The loan agreement is a legally binding document, and understanding every detail is paramount.

The interest rate (APR) is arguably the most critical number in your loan agreement. This percentage represents the annual cost of borrowing money. Even a seemingly small difference in APR can translate into hundreds or thousands of dollars over the loan’s term. Ensure the APR you’re offered matches what you were quoted and compare it to current market rates.

The loan term, or the length of time you have to repay the loan, directly impacts your monthly payments and the total interest paid. While a longer term means lower monthly payments, it also means paying more interest over time and a higher risk of negative equity. Be clear about the term and whether it aligns with your financial goals.

Always look for the total cost of the loan. This figure combines the principal amount borrowed plus all the interest you will pay over the entire loan term. This is the true measure of how much the car will cost you, beyond its sticker price. Don’t be shy about asking the lender to clearly outline this amount.

Prepayment penalties are clauses that might charge you a fee if you pay off your loan early. While not common in all auto loans, they do exist. If you anticipate having extra cash to pay down your principal faster, ensure your loan agreement doesn’t penalize you for doing so.

Be aware of late payment fees and the grace period, if any. Understanding these terms will help you avoid unnecessary charges if an unexpected delay in payment occurs. Pro tips from us: Set up automatic payments to ensure you never miss a due date.

Finally, scrutinize the agreement for any additional fees or add-ons that might have been included without your full understanding. This could include extended warranties, GAP insurance (Guaranteed Asset Protection), or service contracts. While some might be beneficial, ensure they are necessary and not just padding the loan amount. If you don’t want them, don’t sign for them. For more details on understanding various loan terms, you can refer to resources like the Consumer Financial Protection Bureau (CFPB) auto loan guide.

Building a Strong Financial Foundation (Beyond the Loan)

Securing a low down payment car loan is just one step in your financial journey. True financial strength comes from managing your money wisely and planning for the future. Beyond the initial purchase, there are several key areas to focus on that will serve you well for years to come.

The importance of an emergency fund cannot be overstated. Even with a low down payment, unexpected car repairs, job loss, or medical emergencies can quickly derail your budget. Aim to build an emergency fund covering at least three to six months of living expenses. This fund acts as a safety net, preventing you from missing loan payments or resorting to high-interest debt when unforeseen events occur.

Budgeting for car ownership goes beyond just your monthly loan payment. It includes fuel, insurance, routine maintenance (oil changes, tire rotations), and potential repairs. Create a realistic monthly budget that allocates funds for all these expenses. Understanding these ongoing costs ensures you can comfortably afford your vehicle without financial stress. If you’re looking for tips on managing your vehicle expenses, you might find our article on "Budgeting for Your First Car Purchase" helpful.

Credit score management is an ongoing process. Continue to make all your loan and credit card payments on time, keep your credit utilization low, and periodically review your credit report for accuracy. A healthy credit score will not only help you secure better rates on future loans but also open doors to other financial opportunities.

Finally, be aware of future refinancing possibilities. If your credit score improves significantly after a year or two of on-time payments, or if interest rates drop, you might be able to refinance your car loan for a lower interest rate or a more favorable term. This can save you a substantial amount of money over the life of the loan. Keep an eye on market rates and your credit health.

Conclusion: Drive Smarter, Not Harder

Navigating the world of low down payment car loans doesn’t have to be a daunting task. By understanding the intricacies, weighing the pros and cons, and employing smart strategies, you can confidently secure a vehicle that meets your needs without overextending your finances. Remember, the goal isn’t just to get a car, but to do so responsibly and sustainably.

From getting pre-approved to meticulously reviewing the loan agreement, every step in this guide is designed to empower you as a consumer. While a low down payment offers immediate financial flexibility, always consider the long-term implications for your budget and overall financial health. By making informed choices, you can drive away with not just a new car, but also peace of mind and a stronger financial future. Your journey starts with knowledge, and we hope this comprehensive guide has provided you with the tools to make the best decision for your next vehicle purchase.