Drive Smart, Save Big: Your Ultimate Guide to the Best Online Car Loan Lenders

Drive Smart, Save Big: Your Ultimate Guide to the Best Online Car Loan Lenders Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your first set of wheels or an upgrade to a dream machine. However, the joy of a new vehicle can quickly be overshadowed by the daunting process of securing financing. Traditionally, this meant endless trips to dealerships and banks, filling out stacks of paperwork, and negotiating rates in person. But the digital age has revolutionized this experience, bringing the power of choice and convenience directly to your fingertips.

Welcome to the world of online car loan lenders – a game-changer for modern car buyers. This comprehensive guide will not only help you understand why online financing is often the smartest route but also equip you with the knowledge to identify the best online car loan lenders for your unique situation. Our ultimate goal is to empower you to drive away with confidence, knowing you’ve secured the most favorable terms possible.

Drive Smart, Save Big: Your Ultimate Guide to the Best Online Car Loan Lenders

Why Online Car Loan Lenders Are Your Best Bet

In today’s fast-paced world, efficiency and transparency are paramount. Online car loan lenders offer a host of advantages that traditional methods simply can’t match. They’ve become incredibly popular for good reason, streamlining what used to be a complex and time-consuming process.

Unparalleled Convenience and Speed

Imagine applying for a car loan from the comfort of your couch, in your pajamas, at any time of day or night. That’s the reality with online lenders. You can complete applications, upload documents, and receive offers without ever stepping foot in a physical office. This digital convenience saves you precious time and eliminates the hassle of scheduling appointments.

Based on my experience, the ability to quickly compare multiple offers without pressure is invaluable. Many online platforms provide instant pre-qualification, giving you a clear picture of potential rates and terms within minutes. This speed allows you to act quickly when you find the perfect car.

A Wider Array of Comparison Options

One of the biggest benefits of going online is the sheer volume of options available. Instead of being limited to the few banks or credit unions near you, the internet opens up a national marketplace of lenders. This means you can compare interest rates, loan terms, and eligibility requirements from dozens, if not hundreds, of providers.

Pro tips from us: Don’t just settle for the first offer you receive. Aggressively shopping around is the single best way to ensure you’re getting the most competitive rate. Online aggregators and direct lender websites make this comparison process incredibly straightforward.

Potentially Better Rates and Terms

With increased competition comes better deals for consumers. Online lenders often have lower overhead costs compared to traditional brick-and-mortar institutions. These savings are frequently passed on to you in the form of lower interest rates and more flexible loan terms. They are constantly vying for your business, which drives down costs across the board.

Additionally, many online lenders specialize in specific credit profiles, allowing them to offer tailored products. Whether you have excellent credit, good credit, or are working to rebuild your credit, there’s likely an online lender whose niche aligns perfectly with your financial situation.

Enhanced Transparency and Control

The online application process often provides a clearer, more transparent view of your loan terms. You can meticulously review all details, including interest rates, fees, and payment schedules, without feeling rushed or pressured by a salesperson. This allows for informed decision-making and helps you avoid any hidden surprises down the line.

You maintain greater control over the process, from initial research to final signing. This empowerment ensures you fully understand your commitment before agreeing to anything. It’s about making a choice that truly fits your financial plan, not one that’s pushed upon you.

Key Factors to Consider When Evaluating Online Car Loan Lenders

Choosing the "best" online car loan lender isn’t a one-size-fits-all scenario. What’s ideal for one borrower might not be for another. To make an informed decision, you need to evaluate several critical factors. These elements will significantly impact the total cost of your loan and your overall borrowing experience.

Understanding Interest Rates (APR)

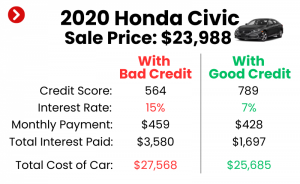

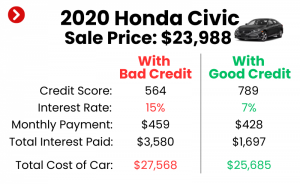

The interest rate is arguably the most crucial factor, as it directly impacts how much you’ll pay over the life of the loan. However, don’t just look at the advertised interest rate; focus on the Annual Percentage Rate (APR). The APR includes not only the interest rate but also any additional fees or charges associated with the loan, giving you a true picture of the total borrowing cost.

A lower APR translates to lower monthly payments and less money paid back over the loan term. Always compare APRs across multiple lenders to get the best deal. Even a half-point difference can save you hundreds, if not thousands, of dollars.

Loan Terms and Length

Loan terms refer to the repayment period, typically ranging from 24 to 84 months. A shorter loan term usually comes with a higher monthly payment but a lower overall interest cost. Conversely, a longer loan term means lower monthly payments but you’ll pay more in interest over time.

Common mistakes to avoid are automatically opting for the longest term to achieve the lowest monthly payment. While it might seem appealing initially, it often results in significantly higher total costs and a longer period of indebtedness. Aim for the shortest term you can comfortably afford.

Fees and Charges

While online lenders are generally more transparent, it’s vital to scrutinize the fee structure. Some lenders charge origination fees, application fees, late payment fees, or even prepayment penalties. A prepayment penalty means you’ll be charged if you pay off your loan early.

Always ask for a detailed breakdown of all potential fees. The best online car loan lenders are upfront about their costs and often have minimal or no hidden fees. Carefully review the loan agreement before signing to understand every charge.

Eligibility Requirements

Each online lender has specific criteria for approval, which typically include your credit score, income, debt-to-income ratio, and employment history. Some lenders cater to prime borrowers with excellent credit, offering the lowest rates. Others specialize in subprime loans for those with less-than-perfect credit.

Before applying, check the lender’s stated requirements. Many offer pre-qualification tools that allow you to see if you meet their general criteria without impacting your credit score. This saves you time and protects your credit from unnecessary hard inquiries.

Customer Service and Reputation

Even with a fully online process, good customer service is essential. You might need assistance with your application, have questions about your loan, or encounter issues during repayment. Look for lenders with accessible customer support, whether through phone, email, or live chat.

Check online reviews and ratings from independent sources like the Better Business Bureau or consumer review websites. A lender’s reputation for ethical practices and responsive support can be just as important as their rates. Positive feedback indicates a reliable and trustworthy partner.

Pre-qualification vs. Pre-approval

Understanding the difference between pre-qualification and pre-approval is crucial in your online car loan journey.

- Pre-qualification provides an estimate of what you might be approved for, based on a soft credit inquiry (which doesn’t affect your credit score). It’s a good way to gauge your eligibility and compare potential rates from different lenders without commitment.

- Pre-approval involves a more thorough review of your finances, including a hard credit inquiry (which may slightly ding your credit score). If approved, you receive a conditional offer for a specific loan amount at a certain interest rate. This acts like cash in hand at the dealership, giving you significant negotiating power.

Pro tips from us: Always get pre-approved before stepping into a dealership. It separates the financing from the car purchase, allowing you to negotiate the car price as a cash buyer.

Our Top Picks: Navigating the Landscape of Online Car Loan Lenders

While we can’t name specific companies that might change their offerings, we can highlight the types of online car loan lenders that consistently perform well for different borrower profiles. Understanding these categories will help you target your search effectively.

1. The Low-Rate Leaders (Ideal for Excellent Credit)

For borrowers with stellar credit scores (typically 700+), certain online lenders specialize in offering the absolute lowest APRs available. These lenders often prioritize highly qualified applicants who pose minimal risk. They pride themselves on streamlined applications and competitive terms.

- What they offer: Unbeatable interest rates, flexible loan terms (often with options for shorter periods), high loan limits, and minimal fees. They often have transparent processes with quick approvals.

- Who they are best for: Individuals with excellent credit histories, stable income, and low debt-to-income ratios. Those looking to save the most money on interest over the life of their loan.

- Pros: Lowest possible APRs, fast processing, superior customer service, and often highly flexible repayment options.

- Cons: Very strict eligibility requirements; not suitable for those with average or poor credit.

- Based on my experience: If your credit score is in the "excellent" range, these lenders should be your first stop. You’ve earned the right to the best rates, so don’t settle.

2. The Broad Accessibility Providers (Ideal for Good to Average Credit)

This category includes many popular online lenders that cater to a wide range of credit scores, typically from good (660-699) to average (600-659). They aim to provide competitive rates without the stringent requirements of prime lenders. These platforms often leverage technology to assess risk beyond just a credit score.

- What they offer: Competitive, though not always the absolute lowest, interest rates. A broader range of loan amounts and terms. Often have user-friendly websites and helpful tools.

- Who they are best for: Borrowers with solid credit who might not qualify for the absolute prime rates but are still very reliable. Also good for those with limited credit history but good income.

- Pros: Good balance of rates and accessibility, easy application processes, often quick decisions, and helpful resources for understanding loans.

- Cons: Rates won’t be as low as for prime borrowers; some fees might apply depending on the lender.

- Pro tips from us: These lenders are excellent for comparing multiple offers. Use their pre-qualification tools to see how your credit profile stacks up against their general criteria.

3. The Second-Chance Specialists (Ideal for Less-Than-Perfect Credit)

For individuals with lower credit scores (below 600) or past financial difficulties, specialized online lenders focus on providing "second-chance" auto loans. While rates will be higher due to increased risk, these lenders offer a vital pathway to car ownership and an opportunity to rebuild credit.

- What they offer: Loans for individuals with poor or limited credit, often with flexible income verification requirements. They focus on your ability to pay now, rather than just your past.

- Who they are best for: Borrowers with bad credit, new immigrants with no credit history, or those recovering from bankruptcy. The goal here is often to get approved and then improve credit for future, better loans.

- Pros: Opportunity to secure financing when traditional banks won’t lend, chance to rebuild credit with on-time payments, and often understanding customer service.

- Cons: Significantly higher interest rates, potentially stricter terms (e.g., higher down payment requirements), and possibly more fees.

- Common mistakes to avoid are: Not understanding that these loans come with a higher cost. Focus on making timely payments to improve your score and refinance later.

- Based on my experience: If you’re in this category, be prepared for higher rates. Your focus should be on getting a reliable vehicle and establishing a consistent payment history to improve your creditworthiness for future financing opportunities.

4. The Member-Focused Providers (Credit Unions and Peer-to-Peer Platforms)

While not always "online-only," many credit unions now offer robust online application portals and competitive rates. Peer-to-peer lending platforms also connect individual investors with borrowers, sometimes offering unique terms.

- What they offer: Credit unions often provide very competitive rates, especially for their members, due to their not-for-profit structure. Peer-to-peer platforms can sometimes be more flexible in their underwriting.

- Who they are best for: Individuals looking for a community-focused approach (credit unions) or those who might benefit from a more personalized assessment (P2P).

- Pros: Often lower rates than traditional banks, personalized service, and a focus on member/borrower success.

- Cons: Credit unions require membership (though it’s usually easy to join); P2P platforms might have longer funding times.

The Online Car Loan Application Process: A Step-by-Step Guide

Navigating the online application process for a car loan can seem intimidating at first, but it’s designed for efficiency. Here’s a clear, step-by-step breakdown to guide you.

- Gather Your Documents: Before you begin, have all necessary information ready. This typically includes your driver’s license, Social Security number, proof of income (pay stubs, tax returns), proof of residence, and details about your current debts and assets. Being prepared speeds up the entire process.

- Pre-qualify with Multiple Lenders: Start by using the pre-qualification tools offered by several online lenders. This allows you to see potential rates and terms without affecting your credit score. It’s a fantastic way to narrow down your options to those most likely to approve you at favorable rates.

- Compare Offers Thoroughly: Once you have a few pre-qualification estimates, carefully compare the APRs, loan terms, fees, and any specific conditions. Remember, the lowest monthly payment isn’t always the cheapest option overall.

- Submit Your Full Application: Choose the lender that offers the best terms and proceed with their full application. This step usually involves a hard credit inquiry, which will show up on your credit report. Be honest and accurate with all information provided.

- Review and Sign the Loan Agreement: If approved, you’ll receive a formal loan offer. Read every single line of the loan agreement before signing. Ensure you understand the APR, total repayment amount, all fees, and the exact payment schedule. Don’t hesitate to ask questions if anything is unclear.

- Fund Your Purchase: Once the agreement is signed, the lender will disburse the funds. This might be directly to you, to the car dealership, or occasionally through a digital transfer. You can then finalize your car purchase with confidence.

Common Mistakes to Avoid When Applying for an Online Car Loan

Even with the ease of online applications, certain pitfalls can cost you money and cause unnecessary stress. Being aware of these common mistakes will help you navigate the process more effectively.

- Not Shopping Around Enough: This is perhaps the biggest mistake. Settling for the first offer you receive means you’re likely leaving money on the table. Always compare offers from at least 3-5 different lenders.

- Ignoring the APR: Focusing solely on the monthly payment or the advertised interest rate can be misleading. The APR gives you the true cost of borrowing, encompassing all fees. Always compare APRs.

- Extending Loan Terms Too Long: While a longer loan term means lower monthly payments, it significantly increases the total interest you’ll pay over time. It also increases the risk of negative equity, where you owe more than the car is worth.

- Applying for Too Many Loans at Once: Multiple hard credit inquiries in a short period can negatively impact your credit score. Use pre-qualification tools that only involve soft inquiries until you’re ready for a full application with your chosen lender.

- Not Reading the Fine Print: Every loan agreement contains critical details about fees, penalties, and terms. Skipping this step can lead to costly surprises down the road. Take your time and understand every clause.

Pro Tips for Securing the Best Online Car Loan

To truly maximize your chances of getting the most favorable terms, incorporate these expert strategies into your car buying journey.

- Boost Your Credit Score: A higher credit score directly translates to lower interest rates. Before applying, take steps to improve your score: pay bills on time, reduce existing debt, and dispute any errors on your credit report.

- Save for a Down Payment: A substantial down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over time. It also signals to lenders that you’re a lower risk.

- Get Pre-approved: As mentioned earlier, securing pre-approval before visiting a dealership gives you significant leverage. It allows you to negotiate the car’s price separately from the financing, often resulting in a better deal on both fronts. (For more details, check out our guide on Car Loan Pre-Approval: Your Secret Weapon at the Dealership).

- Consider a Shorter Loan Term (If Affordable): While longer terms offer lower monthly payments, a shorter term (e.g., 36 or 48 months) saves you a considerable amount in interest over the life of the loan. Only commit to what you can comfortably afford, but challenge yourself to pay it off faster if possible.

- Negotiate the Car Price Separately: With your financing in hand, you can focus purely on getting the best price for the vehicle. Don’t let the dealership bundle the car price and financing together, as this often makes it harder to see where you can save.

- Understand Your Budget: Before even looking at cars or loans, determine how much you can truly afford for a monthly payment, including insurance, fuel, and maintenance. This prevents you from overextending yourself financially.

- Refinance Later If Needed: If you secure a loan with a higher interest rate due to poor credit, you can always aim to refinance once your credit score improves. Many online lenders specialize in car loan refinancing, offering opportunities to lower your payments or interest rates.

Frequently Asked Questions About Online Car Loans

Here are answers to some common questions that arise when seeking online car financing.

Q: Can I get an online car loan with bad credit?

A: Yes, absolutely. While it might be challenging to secure the lowest rates, many online lenders specialize in working with individuals who have less-than-perfect credit. These "second-chance" lenders focus on your current income and ability to pay, offering a path to car ownership and credit rebuilding. Be prepared for higher interest rates, but it’s definitely possible.

Q: How fast can I get approved for an online car loan?

A: One of the biggest advantages of online lenders is their speed. Many offer instant pre-qualification decisions. For full approval, it can range from a few minutes to a few business days, depending on the lender and the completeness of your application. Once approved, funds can often be disbursed within 24-48 hours.

Q: Will applying for a loan hurt my credit score?

A: Using a lender’s pre-qualification tool typically involves a "soft" credit inquiry, which does not affect your credit score. However, submitting a full loan application will result in a "hard" credit inquiry. This can temporarily ding your credit score by a few points. To minimize the impact, try to complete all your full applications within a 14-45 day window, as credit bureaus often count multiple auto loan inquiries within that period as a single inquiry.

Q: What documents do I need for an online car loan?

A: Generally, you’ll need proof of identity (driver’s license, SSN), proof of income (pay stubs, tax returns, bank statements), proof of residence (utility bill), and information about the vehicle you intend to purchase (if you’ve picked one out). Having these ready will significantly speed up your application process.

Q: Can I use an online car loan for a private party sale?

A: Yes, many online lenders offer financing specifically for private party sales. This is a great option as it allows you to buy a car directly from an individual, potentially saving money compared to a dealership purchase. Be sure to inform your chosen lender that you intend to purchase from a private seller, as the process might differ slightly.

For further reading on financial terms and concepts related to loans, you can always refer to trusted sources like Investopedia: https://www.investopedia.com/terms/c/car-loan.asp

Conclusion: Your Road to Smart Car Financing Starts Online

The journey to buying a new car doesn’t have to be filled with stress and uncertainty, especially when it comes to financing. By leveraging the power of online car loan lenders, you gain access to unparalleled convenience, a vast marketplace of options, and potentially the best rates available. With this comprehensive guide, you’re now equipped to confidently navigate the landscape of online auto financing.

Remember to prioritize understanding the APR, comparing multiple offers, and reading every detail of your loan agreement. Your proactive approach in seeking out the best online car loan lenders will not only save you money but also provide peace of mind as you drive away in your new vehicle. Happy car hunting, and safe travels!