Drive Smart: Your Ultimate Guide on How to Avoid Being Upside Down on a Car Loan

Drive Smart: Your Ultimate Guide on How to Avoid Being Upside Down on a Car Loan Carloan.Guidemechanic.com

Buying a new car is often an exhilarating experience. The scent of fresh upholstery, the gleam of new paint, and the promise of open roads ahead can be intoxicating. But beneath this excitement lies a potential financial pitfall that many drivers unwittingly tumble into: being "upside down" on a car loan. This common yet often misunderstood situation can turn your dream car into a financial nightmare, leaving you owing more than the vehicle is actually worth.

Here at , we believe in empowering you with the knowledge to make smart financial decisions, especially when it comes to significant purchases like a car. Based on my extensive experience in automotive finance and consumer education, understanding and preventing negative equity is not just about saving money; it’s about securing your financial peace of mind. This comprehensive guide will equip you with the strategies to navigate the complexities of car financing, ensuring you stay firmly on solid ground and avoid the dreaded upside-down scenario.

Drive Smart: Your Ultimate Guide on How to Avoid Being Upside Down on a Car Loan

What Does "Upside Down" on a Car Loan Really Mean?

Let’s start by clarifying what it means to be upside down, or in "negative equity," on your car loan. Simply put, you are upside down when the outstanding balance of your car loan is greater than the current market value of your vehicle. Imagine your car is worth $15,000, but you still owe $18,000 to the lender. That $3,000 difference represents your negative equity.

This situation isn’t just an abstract financial concept; it has very real and often inconvenient consequences. If you need to sell your car, trade it in, or if it gets totaled in an accident, you’ll be faced with paying the difference out of your own pocket. This can create significant financial stress and limit your options, effectively trapping you in a vehicle you might no longer want or need.

Understanding this core concept is the first step toward safeguarding yourself. Many people don’t realize they’re in negative equity until it’s too late, often at the point of needing a new vehicle or facing an unforeseen life event. Our goal is to ensure you’re never caught off guard.

The Root Causes: Why Do Cars Go Upside Down So Easily?

To effectively avoid negative equity, it’s crucial to understand the primary factors that contribute to it. This isn’t just about making one bad decision; it’s often a combination of several common financing pitfalls. Common mistakes to avoid are underestimating depreciation and overextending your loan term.

1. Rapid Depreciation: The Silent Killer of Car Value

Cars are not investments; they are depreciating assets. This means their value decreases over time, often quite dramatically, especially in the initial years. The moment a new car leaves the dealership lot, its value can drop by 10-20%. Within the first year, it’s not uncommon for a vehicle to lose 20-30% of its original purchase price. This rapid initial depreciation is arguably the single biggest contributor to negative equity.

If your loan balance isn’t paid down quickly enough to keep pace with this value loss, you’ll inevitably find yourself upside down. Different car models and brands depreciate at varying rates, with some holding their value much better than others. Understanding this dynamic is key to making a smart purchase.

2. Insufficient Down Payment: A Weak Foundation

A small or non-existent down payment is another major culprit. When you put little to no money down, you start your loan journey owing almost the entire purchase price of the car. This immediately puts you at a disadvantage against the rapid depreciation discussed above.

A larger down payment creates an immediate buffer, reducing the initial loan amount and giving you a head start in building equity. It’s like building a house on a strong, deep foundation rather than a shallow, unstable one. Many buyers are tempted by "no money down" offers, but these often lead directly to negative equity.

3. Long Loan Terms: The Extended Trap

The allure of lower monthly payments often leads buyers to opt for longer loan terms, stretching out payments over 60, 72, or even 84 months. While this might seem appealing in the short term, it significantly increases the total interest paid and slows down the rate at which you build equity in your vehicle.

With a longer term, your principal balance decreases very slowly, especially in the early years when a larger portion of your payment goes towards interest. This prolonged period means your loan balance stays high for longer, making it easier for depreciation to outpace your payments and push you into negative equity. Based on my experience, 72-month and 84-month loans are particularly risky for this reason.

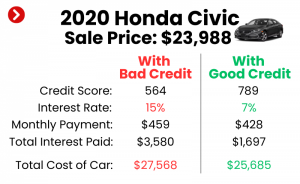

4. High Interest Rates: Inflating Your Debt

A high interest rate inflates the total cost of your loan and, consequently, the total amount you owe. The more interest you pay, the slower you chip away at the principal balance. This means your loan balance remains elevated for a longer period, making you more susceptible to negative equity as the car’s value declines.

Factors like your credit score, the current market rates, and the lender’s policies all influence the interest rate you receive. Securing the lowest possible rate is vital for managing your loan effectively and avoiding an upside-down situation.

5. Rolling Over Negative Equity: The Endless Cycle

One of the most dangerous scenarios is when a buyer trades in a vehicle that already has negative equity and rolls that outstanding balance into the new car loan. This essentially means you’re financing two cars with one loan. You start your new car ownership journey already significantly upside down, often by thousands of dollars.

This practice creates a cycle that is incredibly difficult to break. Each subsequent car purchase carries the debt from the previous one, snowballing your negative equity and making it almost impossible to ever get ahead. This is a common mistake that traps many consumers.

6. Excessive Add-ons: Unnecessary Debt Boosters

Dealerships often offer various add-ons and extended warranties that, while sometimes beneficial, can significantly increase the total amount financed. Things like rustproofing, paint protection, fabric guard, or even overly expensive extended service plans, when added to your loan, inflate your principal balance.

If these add-ons are financed, they immediately contribute to the amount you owe, without adding equivalent value to the car’s market price. This widens the gap between what you owe and what the car is worth, accelerating your journey into negative equity.

Proactive Strategies: How to Avoid Being Upside Down on a Car Loan

Now that we understand the causes, let’s dive into actionable strategies to prevent negative equity. These are the pro tips from us that will empower you to make informed decisions and maintain control over your financial future.

1. Make a Substantial Down Payment

This is arguably the most effective way to avoid negative equity. A significant down payment immediately reduces the principal amount you need to finance, giving you a strong head start against depreciation. We recommend aiming for at least 20% of the car’s purchase price for new cars. For used cars, a 10-15% down payment is a good target.

A larger down payment means lower monthly payments, less interest paid over the life of the loan, and faster equity accumulation. It creates a buffer that allows your loan balance to drop below the car’s value much sooner. Even if 20% isn’t feasible, put down as much as you possibly can. Every dollar you put down upfront is a dollar you don’t finance, saving you interest and building equity faster.

2. Choose a Shorter Loan Term

Resist the temptation of those ultra-long loan terms. While a 72 or 84-month loan might offer a tantalizingly low monthly payment, it’s a trap. Aim for the shortest loan term you can comfortably afford, ideally 36 to 60 months.

A shorter term means higher monthly payments, but you’ll pay significantly less interest overall and build equity much faster. This ensures your loan balance declines at a pace that can keep up with, or even outpace, the car’s depreciation. Based on my experience, a 48-month loan offers an excellent balance between affordability and financial prudence.

3. Understand and Negotiate the Car Price

Don’t just focus on the monthly payment; negotiate the total purchase price of the vehicle. Dealerships often try to steer conversations toward monthly payments because it makes expensive cars seem more affordable. Always research the fair market value of the car you’re interested in using resources like Kelley Blue Book or Edmunds. This research empowers you to negotiate effectively.

By securing a better purchase price, you reduce the total amount you need to finance from the outset. This immediately lessens the gap between what you owe and what the car is worth, making it harder to fall into negative equity. A lower starting price is a powerful advantage.

4. Research Car Depreciation Rates Before Buying

Not all cars depreciate equally. Some models, brands, and even specific trims hold their value much better than others. Before you commit to a purchase, research the typical depreciation rates for the vehicles you’re considering. Websites like J.D. Power or Kelley Blue Book often publish data on vehicles with the best resale value.

Choosing a car known for strong resale value can be a smart long-term strategy. It means that even as your car ages, its market value will decline at a slower rate, making it easier to stay above water on your loan. This is a proactive step that can save you thousands down the line.

5. Consider a Used Car Instead of New

The steepest depreciation occurs in a car’s first few years. By purchasing a quality used car, you let the first owner absorb that initial, dramatic drop in value. A car that is 2-3 years old has already gone through its most significant depreciation period, meaning its value will decline at a much slower rate moving forward.

This strategy allows you to get more car for your money and significantly reduces the risk of being upside down. Pro tip: Look for Certified Pre-Owned (CPO) vehicles, which offer the peace of mind of an inspection and warranty, often at a much better value than new.

6. Be Wary of Rolling Over Negative Equity

If you owe money on your current car, do everything in your power to avoid rolling that balance into a new loan. If you absolutely must trade in a vehicle with negative equity, be prepared to pay the difference out of pocket.

Alternatively, consider selling your current car privately if you can get more for it than a trade-in offer. If you have negative equity, rolling it into a new loan starts you off deep in debt and can quickly lead to an even worse financial situation. It’s a cycle that’s very hard to escape.

7. Avoid Unnecessary Add-ons

Scrutinize every add-on offered at the dealership. While some, like Gap insurance (which we’ll discuss shortly), can be valuable, many others are high-profit items for the dealership that add little to no real value to your car’s resale price. Things like extended warranties, service plans, or cosmetic packages should be carefully considered.

If you decide an add-on is necessary, try to pay for it separately or negotiate its price fiercely. Financing these items simply inflates your loan principal without a corresponding increase in the car’s market value, accelerating your path to negative equity.

8. Secure Your Financing Before Visiting the Dealership

One of the most powerful strategies you can employ is to get pre-approved for a car loan from your bank or credit union before you step foot in a dealership. This gives you a clear understanding of the interest rate and loan terms you qualify for, establishing a baseline.

Having pre-approval empowers you to negotiate confidently. You’ll know if the dealer’s financing offer is truly competitive or if they’re trying to push a higher rate. This separates the financing discussion from the car price negotiation, allowing you to focus on getting the best deal on both.

9. Make Regular Extra Payments

Even small, consistent extra payments can make a huge difference in staying ahead of depreciation. When you make an extra payment, specify that the additional amount should be applied directly to the principal balance of your loan.

This strategy helps you pay down your loan faster, reduce the total interest paid, and build equity more quickly. For example, if your monthly payment is $400, adding just $50 to it each month can shave months off your loan term and save you hundreds in interest. For more detailed strategies on accelerating your loan payoff, check out our article on .

What If You’re Already Upside Down? (Damage Control)

Sometimes, despite best intentions, you might find yourself in a negative equity situation. Don’t panic! While it’s a challenging spot, there are steps you can take to mitigate the damage and work your way back to positive equity.

1. Aggressively Make Extra Payments

If you can afford it, the most direct way out of negative equity is to make larger or more frequent payments. Aim to pay down the principal balance as quickly as possible. Even an extra $25 or $50 a month can make a significant difference over time, slowly closing the gap between what you owe and what your car is worth.

2. Refinance Your Loan (Under the Right Conditions)

Refinancing can be a viable option if market interest rates have dropped, your credit score has improved since you first took out the loan, or if you can secure a significantly lower rate. A lower interest rate means more of your payment goes towards the principal, helping you build equity faster.

However, be cautious: only refinance if you can maintain or shorten your loan term. Common mistake: refinancing for a longer term just to lower your monthly payment. This only prolongs your debt and could keep you in negative equity for even longer.

3. Sell the Car Privately

Selling your car privately often yields a higher price than trading it in at a dealership. If you’re upside down, selling privately means you’ll still need to cover the difference between the sale price and your loan balance, but that difference might be smaller than if you traded it in. This gives you more control over the sale price and your financial obligation.

4. Pay the Difference on Trade-in

If you absolutely need a new car and must trade in your current vehicle with negative equity, be prepared to pay the difference out of pocket. This might mean bringing a check to the dealership to cover the negative equity on your old loan before signing for a new one. While painful, it prevents you from rolling that old debt into your new car loan and starting a new cycle of negative equity.

5. Utilize GAP Insurance (If You Have It)

Guaranteed Asset Protection (GAP) insurance is specifically designed for situations where your car is totaled or stolen and you owe more than its actual cash value. If you have GAP insurance and your vehicle meets these conditions, it will pay the difference between what your primary insurer pays and your outstanding loan balance.

This is why we sometimes recommend GAP insurance, especially if you made a small down payment or have a long loan term. It’s a safety net. For a deeper dive into how different types of insurance work, you might find our article on helpful.

Key Takeaways & Actionable Advice

Navigating the world of car loans doesn’t have to be a minefield. By understanding the common pitfalls and employing smart strategies, you can confidently drive away in your new vehicle without the looming threat of negative equity. Pro tips from us include prioritizing your down payment and loan term.

- Be Proactive: Don’t wait until you’re at the dealership to think about financing. Research, plan, and secure your pre-approval beforehand.

- Prioritize a Down Payment: The more you put down, the better your financial standing from day one. Aim for 20% on new cars.

- Choose Shorter Terms: Resist the allure of low monthly payments on long loans. A 36-60 month term is generally ideal.

- Negotiate Smart: Focus on the total purchase price, not just the monthly payment.

- Understand Depreciation: Pick cars that hold their value well and consider buying used.

- Avoid Rolling Debt: Do not carry over negative equity from a previous loan into a new one.

- Stay Informed: Regularly check your car’s market value and your loan balance to monitor your equity position.

Ultimately, avoiding being upside down on a car loan boils down to making informed, financially responsible decisions. It’s about empowering yourself with knowledge and discipline to ensure your car ownership experience remains a joy, not a burden.

Frequently Asked Questions

Q: How much down payment is truly enough to avoid negative equity?

A: While 20% for a new car is often recommended as an ideal starting point, the "enough" amount varies based on the car’s depreciation rate, your loan term, and interest rate. Generally, the more you put down, the safer you are. For used cars, 10-15% is a strong start.

Q: Is GAP insurance always necessary?

A: GAP insurance is most valuable if you make a small down payment, choose a long loan term, or finance a car that depreciates very quickly. If you put down a large sum (20%+) and have a short loan term, you might not need it as much, but it’s always worth considering the peace of mind it offers.

Q: Can I get out of an upside-down loan if I can’t afford extra payments?

A: It’s challenging but possible. Explore refinancing options if your credit has improved or rates have dropped. Selling the car privately and covering the difference is another option. In extreme cases, discussing options with your lender might be necessary, though this should be a last resort.

Q: What’s the best loan term to avoid negative equity?

A: The best loan term is one that allows you to pay down your principal faster than the car depreciates. Based on my experience, 36 to 60 months are generally the safest options. Avoid 72 or 84-month terms if at all possible.

Q: How do I know my car’s current market value?

A: You can get an estimated market value for your car by using online tools from trusted sources like Kelley Blue Book (KBB.com) or Edmunds. These sites allow you to input your car’s make, model, year, mileage, and condition to get a realistic appraisal.

Conclusion

Your car is more than just a mode of transportation; it’s a significant financial asset and a major investment. By understanding the dynamics of depreciation, interest, and loan terms, you gain the power to make choices that protect your financial health. Avoiding being upside down on a car loan isn’t about luck; it’s about education and strategic planning. Implement the strategies outlined in this guide, and you’ll ensure your journey on the road is as financially sound as it is enjoyable. Drive smart, stay informed, and always keep your equity in the green!