Drive Smart: Your Ultimate Guide to Pre-Approved Car Loans for Private Party Purchases

Drive Smart: Your Ultimate Guide to Pre-Approved Car Loans for Private Party Purchases Carloan.Guidemechanic.com

Are you dreaming of finding that perfect used car from a private seller, but worried about navigating the financing? You’re not alone. Many buyers find the private party car buying process daunting, especially when it comes to securing a loan. The good news? A pre-approved car loan for a private party purchase can transform your car-buying experience, offering peace of mind, bargaining power, and a smoother transaction.

As an expert blogger and professional SEO content writer, I understand the challenges and opportunities in the private car market. This comprehensive guide will demystify pre-approved private party auto loans, providing you with all the knowledge you need to drive away in your ideal vehicle with confidence. We’ll dive deep into what these loans entail, why they’re a game-changer, how to secure one, and crucial tips for a seamless purchase.

Drive Smart: Your Ultimate Guide to Pre-Approved Car Loans for Private Party Purchases

What Exactly is a Pre-Approved Car Loan for a Private Party?

Let’s start by defining our terms. A pre-approved car loan for a private party sale is a financing offer from a lender where they agree to lend you a specific amount of money, at a particular interest rate, before you’ve even found the car you want to buy. The key differentiator here is "private party." Unlike traditional auto loans that often involve dealerships, this type of pre-approval is specifically designed for purchasing a vehicle directly from an individual seller.

This means you walk into negotiations with a private seller with the financial backing already secured. The lender has assessed your creditworthiness and determined how much they are willing to finance. This pre-approval gives you the purchasing power of a cash buyer, making you a very attractive prospect to private sellers who often prefer quick and straightforward transactions.

It’s essentially a conditional commitment from a financial institution. They’re saying, "We’re ready to lend you X amount, provided the car meets our criteria and you finalize the purchase within a certain timeframe." This distinction is vital for understanding its immense value in the private car market.

Why Consider a Pre-Approved Loan for a Private Party Purchase?

Based on my extensive experience, pursuing a pre-approved loan before engaging with private sellers offers numerous advantages that can save you time, money, and stress. Here’s why this approach is highly recommended:

1. Enhanced Negotiation Power

Imagine approaching a private seller knowing exactly how much you can spend. This financial clarity gives you a significant edge in negotiations. You’re not guessing or waiting for loan approval; you’re a serious buyer with funds ready to go. Sellers often prioritize speed and certainty, and a pre-approved loan signals that you are prepared to close the deal swiftly.

This power allows you to focus solely on negotiating the car’s price, rather than simultaneously juggling loan details. You can confidently make an offer, knowing it’s backed by a financial institution.

2. Clear Budgetary Boundaries

One of the most common mistakes buyers make is falling in love with a car outside their budget. A pre-approved loan sets a clear financial limit, helping you shop smarter. You’ll know your maximum affordable price, including interest and potential fees, right from the start.

This prevents emotional overspending and ensures you select a vehicle that comfortably fits your financial plan. It brings discipline to your search, narrowing down options to those truly within reach.

3. Streamlined Buying Process

Private party sales can sometimes be complex, involving multiple steps. With pre-approval, the financing hurdle is largely cleared upfront. Once you find the right car, the process transitions to vehicle inspection, paperwork, and fund disbursement, rather than waiting for a loan decision.

This expedites the overall transaction, making it a smoother experience for both you and the seller. It removes a significant layer of uncertainty and accelerates the path to ownership.

4. Competitive Interest Rates

Lenders often offer more competitive interest rates for pre-approved loans because they have thoroughly vetted your financial profile. You have the opportunity to shop around for the best rates and terms before you’re under pressure to buy. This proactive approach can lead to substantial savings over the life of the loan compared to last-minute financing options.

Shopping for a loan separately from shopping for a car allows you to compare offers from various banks, credit unions, and online lenders, ensuring you secure the most favorable terms.

5. Protection and Peace of Mind

A pre-approved loan provides a layer of security. The lender will often require certain checks on the vehicle, such as a title check, before finalizing the loan. This due diligence can protect you from purchasing a vehicle with hidden liens or other legal issues.

Knowing your financing is secure also reduces stress throughout the search and purchase process. You can focus on finding the perfect car, confident that the financial piece of the puzzle is already in place.

The Pre-Approval Process: A Step-by-Step Guide

Securing a pre-approved car loan for a private party doesn’t have to be complicated. By following these steps, you can navigate the process efficiently and effectively.

Step 1: Assess Your Financial Health

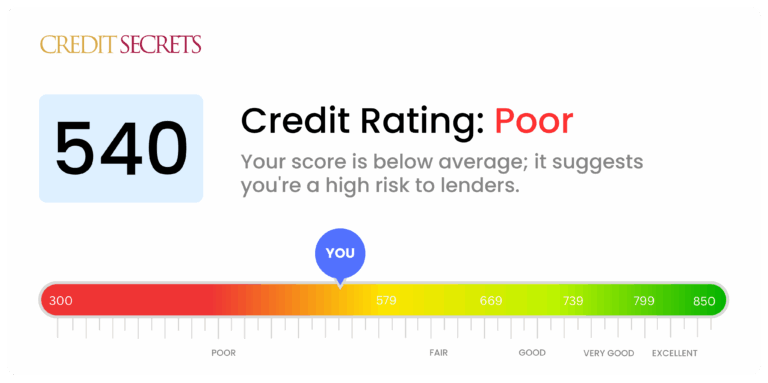

Before approaching any lender, take an honest look at your financial situation. This involves checking your credit score, reviewing your credit report for any inaccuracies, and understanding your debt-to-income (DTI) ratio. Lenders use these metrics to determine your creditworthiness and ability to repay a loan.

A higher credit score typically translates to better interest rates. If your score isn’t where you’d like it, consider taking steps to improve it before applying, such as paying down existing debts or disputing errors on your credit report.

Step 2: Determine Your Ideal Budget

Knowing your pre-approval amount is one thing, but understanding what you can comfortably afford is another. Consider not just the monthly loan payment, but also other car ownership costs like insurance, fuel, maintenance, and registration. Use an online auto loan calculator to estimate payments at various loan amounts and interest rates.

This proactive budgeting helps you set realistic expectations and avoids financial strain down the road. It ensures your car purchase enhances, rather than burdens, your lifestyle.

Step 3: Gather Necessary Documents

Lenders will require specific documentation to process your application. Common requirements include:

- Proof of identity (driver’s license).

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residence (utility bill, lease agreement).

- Social Security number.

- Employer information.

Having these documents ready beforehand will significantly speed up your application process. Being prepared demonstrates your seriousness and efficiency to the lender.

Step 4: Shop for Lenders

Don’t just go with the first lender you find. Shop around and compare offers from various financial institutions. This includes:

- Banks: Traditional banks often have established auto loan departments.

- Credit Unions: Known for competitive rates and personalized service, often requiring membership.

- Online Lenders: Many reputable online platforms specialize in auto loans and can offer quick approvals.

Look beyond just the interest rate; consider fees, loan terms, customer service, and their experience with private party loans. Some lenders are more familiar with this type of transaction than others.

Step 5: Submit Your Application

Once you’ve chosen a few potential lenders, complete their application forms. This typically involves a "soft inquiry" on your credit report initially, which doesn’t affect your score. If you proceed, they will conduct a "hard inquiry," which may temporarily dip your score by a few points. However, multiple hard inquiries for the same type of loan within a short period (usually 14-45 days) are often treated as a single inquiry by credit bureaus, so it’s wise to do your loan shopping within this window.

Be honest and accurate with all information provided. Any discrepancies could delay or even jeopardize your approval.

Step 6: Receive Your Pre-Approval Letter

If approved, the lender will issue a pre-approval letter. This crucial document outlines:

- The maximum loan amount.

- The approved interest rate.

- The loan term (e.g., 36, 48, 60 months).

- Any specific conditions or limitations (e.g., vehicle age, mileage limits).

- The expiration date of the pre-approval.

This letter is your golden ticket to the private party market. Keep it handy as you begin your car search.

Key Factors Lenders Consider for Private Party Loans

When you apply for a pre-approved car loan for a private party, lenders scrutinize several aspects to mitigate their risk. Understanding these factors can help you prepare and improve your chances of approval.

Your Credit Score

Your credit score is arguably the most critical factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score (generally 670 and above) indicates a lower risk to lenders, leading to better interest rates and terms. Lenders want to see a history of responsible financial behavior.

Based on my experience, a good credit score demonstrates financial reliability, which is paramount for securing favorable loan conditions.

Your Income and Debt-to-Income (DTI) Ratio

Lenders need to ensure you have a stable income sufficient to cover your monthly loan payments, in addition to your existing financial obligations. Your debt-to-income (DTI) ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio (typically below 43%) suggests you have enough disposable income to manage new debt without strain.

They want to see that the car loan won’t push you into financial hardship. Consistent employment history also plays a significant role here.

Down Payment Amount

While not always mandatory, offering a down payment can significantly improve your loan application. A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk. It also demonstrates your commitment and reduces your loan-to-value (LTV) ratio, potentially securing you a better interest rate.

Pro tips from us: Even a small down payment can make a difference, both for the lender and for reducing your overall interest paid.

Vehicle-Specific Criteria

Unlike dealer financing where the car is often new or certified pre-owned, private party sales involve a wider range of vehicles. Lenders will have specific criteria for the car itself, such as:

- Age: Many lenders have limits on how old a car can be (e.g., no older than 10-12 years).

- Mileage: There might be maximum mileage restrictions (e.g., under 150,000 miles).

- Value: The loan amount cannot exceed the car’s fair market value, often determined by guides like Kelley Blue Book (KBB) or NADAguides.

- Condition: While they won’t typically inspect it for pre-approval, the car must be in good, roadworthy condition to qualify for financing upon final purchase.

Always clarify these vehicle requirements with your potential lender during the pre-approval phase.

Navigating the Private Sale with Your Pre-Approved Loan

Once you have your pre-approval letter in hand, the real fun begins: finding your car. But the process doesn’t end there. Here’s how to skillfully navigate the private sale to ensure a smooth transaction.

1. Finding the Right Car

Armed with your budget and pre-approval, begin your search. Utilize online marketplaces, local classifieds, and word-of-mouth. Focus on cars that fit your lender’s criteria regarding age, mileage, and value. Don’t be afraid to cast a wide net, but always keep your pre-approval terms in mind.

Remember, the pre-approval is for you, not a specific car. The car still needs to meet the lender’s conditions for final approval.

2. The All-Important Vehicle Inspection

This step cannot be stressed enough. Before finalizing any purchase, arrange for a pre-purchase inspection (PPI) by an independent, certified mechanic of your choosing. Common mistakes to avoid are skipping this crucial step or relying solely on the seller’s assurances. A PPI can uncover hidden mechanical issues, accident damage, or other problems that could cost you thousands down the road.

Based on my experience, a thorough inspection is your best defense against buyer’s remorse and unexpected repairs. It’s a small investment that provides immense protection.

3. Negotiating the Price

Your pre-approval gives you leverage. You know your maximum budget, and you’re ready to buy. Use the findings from your vehicle inspection to negotiate the price. If the mechanic found minor issues, you have grounds to ask for a discount to cover potential repair costs. Be firm but fair, and always be prepared to walk away if the deal isn’t right.

Research the car’s market value using KBB or NADAguides beforehand to inform your offer.

4. Completing the Paperwork

This is where the private party transaction requires careful attention. You’ll need:

- Bill of Sale: A legally binding document detailing the buyer, seller, vehicle information (VIN, make, model, year, mileage), sale price, and date. Both parties should sign it.

- Vehicle The seller must provide a clear title, free of any liens. This is crucial for transferring ownership. The lender will often want to review the title to ensure it’s clean and that they can place their lien on it.

Ensure all names, addresses, and vehicle details are accurate on both documents. Pro tips from us: never take possession of a car without a signed bill of sale and the title in hand (or arrangements made directly with your lender for title transfer).

5. Lender’s Involvement and Fund Disbursement

Once you’ve agreed on a price and the vehicle has passed any necessary checks (e.g., title check, valuation by the lender), your lender will typically handle the fund disbursement.

- They may issue a check directly to the seller.

- They might provide you with a cashier’s check made out to the seller.

- In some cases, funds are transferred electronically.

Crucially, the lender will likely take possession of the vehicle’s title, holding it until the loan is fully repaid. They will then send you the "clear" title. Confirm these specific steps with your lender well in advance.

Common Mistakes to Avoid with Private Party Car Loans

Even with pre-approval, certain pitfalls can derail your private party car purchase. Being aware of these common mistakes can save you a lot of headache and potential financial loss.

1. Skipping the Pre-Purchase Vehicle Inspection

As mentioned, this is paramount. Failing to get an independent inspection is one of the biggest risks in a private sale. Sellers, whether intentionally or not, may not be fully aware of a vehicle’s mechanical issues. You could end up with a money pit. Always invest in a PPI.

2. Not Understanding All Loan Terms

Don’t just focus on the interest rate. Read the entire loan agreement carefully. Pay attention to fees (origination fees, late payment fees), prepayment penalties, and specific conditions related to private party sales. If something is unclear, ask your lender for clarification.

Common mistakes to avoid are signing documents you don’t fully comprehend, which can lead to unexpected costs later.

3. Ignoring Your Credit Report and Score

Applying for a loan without first checking your credit can lead to disappointment or higher interest rates. A low score or errors on your report can negatively impact your loan terms. Be proactive in managing your credit health.

4. Falling for Scams or Unclear Titles

Private party sales, unfortunately, can be targets for scammers. Be wary of deals that seem too good to be true, sellers who pressure you, or those unwilling to provide full vehicle history or allow an inspection. Always verify the seller’s identity and ensure the vehicle’s title is clean, in the seller’s name, and free of any liens.

A lien on the title means a third party (often another lender) has a claim on the vehicle, and the seller doesn’t fully own it. Your lender will verify this, but it’s good for you to be aware.

5. Overlooking Vehicle History Reports

While not a substitute for a mechanical inspection, a vehicle history report (like CarFax or AutoCheck) provides invaluable information. It can reveal past accidents, flood damage, salvage titles, odometer fraud, and service history. This report is a small investment that offers critical insights into a car’s past.

Pro Tips for a Smooth Private Party Car Loan Transaction

Based on my years observing the automotive market, these professional tips can further enhance your private party car buying experience.

Get a Comprehensive Vehicle History Report

Always, always obtain a CarFax or AutoCheck report. This provides a detailed history of the car, including accidents, service records, ownership changes, and title issues. This report, coupled with a PPI, gives you a full picture of the vehicle’s health and background.

Consider an Escrow Service

For larger transactions, an escrow service can add an extra layer of security. An independent third party holds the funds until all conditions of the sale (e.g., title transfer, vehicle delivery) are met. This protects both buyer and seller.

Meet in a Safe, Public Place

When meeting the seller, especially for the first time, choose a well-lit, public location during daylight hours. Some police departments even offer designated "safe exchange zones" for private transactions. Safety should always be a priority.

Don’t Rush the Process

Buying a car is a significant financial decision. Take your time. Don’t feel pressured by the seller or the urgency of your pre-approval expiration date. If something feels off, it probably is. A patient approach ensures you make a well-informed decision.

Confirm Lender Requirements for the Vehicle

Before you get too far down the road with a specific car, double-check that it meets all your lender’s requirements. This includes age, mileage, type of vehicle, and any specific title conditions. It’s frustrating to find the perfect car only to learn your lender won’t finance it.

Comparing Lenders: What to Look For Beyond the Rate

While interest rates are a major factor, a truly savvy buyer looks at the bigger picture when comparing lenders for a private party car loan.

1. Interest Rates and APR

Naturally, you want the lowest possible interest rate. However, also pay attention to the Annual Percentage Rate (APR), which includes the interest rate plus certain fees, giving you a more accurate picture of the total cost of borrowing. A lower APR means less money paid over the life of the loan.

2. Fees and Charges

Some lenders charge origination fees, application fees, or even prepayment penalties if you pay off your loan early. These fees can add up. Ensure you understand all potential charges before committing. Transparency is key.

3. Loan Terms and Flexibility

Consider the length of the loan (e.g., 36, 48, 60 months). Shorter terms mean higher monthly payments but less interest paid overall. Longer terms reduce monthly payments but increase total interest. Choose a term that aligns with your budget and financial goals. Also, ask about any flexibility in payment dates or options for deferment in case of financial hardship.

4. Customer Service and Reputation

A lender’s reputation for customer service can make a big difference, especially if you encounter issues during the process. Read online reviews, check their ratings with organizations like the Better Business Bureau, and ask about their responsiveness and ease of communication. A good lender will make the process as smooth as possible.

5. Experience with Private Party Loans

Some lenders are more accustomed to financing private party sales than others. Lenders with specific experience in this area often have streamlined processes and a better understanding of the unique documentation and title transfer requirements involved. This can prevent delays and confusion.

Conclusion: Drive Away with Confidence

Securing a pre-approved car loan for a private party purchase is more than just getting financing; it’s about empowering yourself as a buyer. It equips you with negotiation power, clarifies your budget, streamlines the transaction, and provides peace of mind throughout the journey. By following the steps outlined in this comprehensive guide, from assessing your financial health to meticulously inspecting your chosen vehicle, you’ll be well-prepared to navigate the private car market like a seasoned pro.

Remember, patience, thorough research, and attention to detail are your best allies. Don’t rush, ask questions, and always prioritize your financial well-being. With a solid pre-approval in hand, you’re not just buying a car; you’re investing in a smarter, more secure way to drive your next vehicle home. Happy car hunting!