Drive Smarter in the Heart of America: Unlocking the Best Car Loan Rates in Kansas City

Drive Smarter in the Heart of America: Unlocking the Best Car Loan Rates in Kansas City Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, especially when you’re aiming for the best car loan rates in Kansas City. Whether you’re eyeing a brand-new SUV, a reliable used sedan, or a rugged truck, securing a favorable auto loan is paramount to your financial well-being. A great rate can save you thousands over the life of your loan, making your dream car more affordable.

In this comprehensive guide, we’ll dive deep into everything you need to know about finding and securing competitive Kansas City auto loans. We’ll cover local lending options, essential preparation steps, smart strategies, and expert tips to ensure you drive away with not just a great vehicle, but also a fantastic deal. Get ready to empower your car-buying journey in the City of Fountains!

Drive Smarter in the Heart of America: Unlocking the Best Car Loan Rates in Kansas City

Why Kansas City Matters When Seeking Car Loans

Kansas City isn’t just a geographical location; it’s a vibrant economic hub with its own unique lending landscape. The local market dynamics, the presence of numerous community banks, credit unions, and a competitive auto dealership scene, all contribute to the opportunities available for car buyers. Understanding this local flavor is crucial for anyone seeking the best car loan rates in Kansas City.

Based on my experience in the automotive finance sector, local lenders often have a deeper understanding of the Kansas City community. This can sometimes translate into more personalized service and, in specific cases, potentially more flexible loan terms or rates compared to purely national institutions. They are often invested in fostering local relationships.

Moreover, the density of dealerships and financial institutions in the greater Kansas City metropolitan area means there’s a healthy level of competition. This competition among lenders and sellers is ultimately a benefit to you, the consumer, as it encourages them to offer more attractive financing packages to earn your business. This is why shopping locally for your car financing KC can be a very smart move.

Deconstructing Car Loan Rates: What Influences Your Offer?

Before you even start comparing offers, it’s vital to understand the factors that lenders consider when determining your car loan interest rate. Knowledge is power, and knowing these elements will help you improve your standing and negotiate more effectively. A low interest rate is the cornerstone of affordable Kansas City auto loans.

Your Credit Score: The Ultimate Indicator

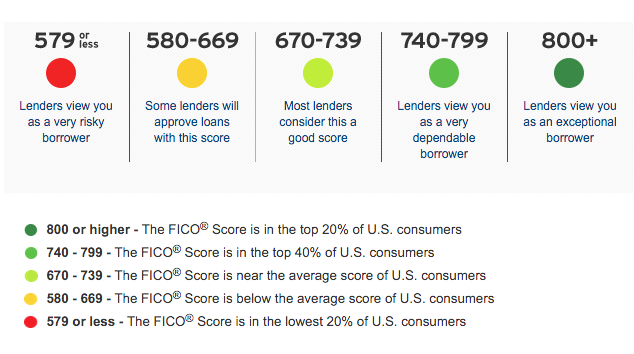

Your credit score is arguably the most significant factor influencing the interest rate you’ll be offered. This three-digit number, generated by credit bureaus, reflects your creditworthiness based on your payment history, amounts owed, length of credit history, new credit, and credit mix. A higher score signals less risk to lenders.

Generally, borrowers with excellent credit (typically 780+) will qualify for the lowest interest rates, often advertised as the "best" rates. Those with good credit (670-779) will also receive very competitive offers. If your score is lower, you might face higher rates, as lenders perceive a greater risk of default.

Pro tips from us: Always check your credit score and report before applying for a car loan. This allows you to identify any errors and understand where you stand. Several free services allow you to check your score, giving you a clear picture of your financial health.

Loan Term: How Long Will You Pay?

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term means lower monthly payments, it almost always results in paying more interest over the life of the loan. This is because the money is borrowed for a longer period, and the interest accrues for longer.

Shorter loan terms, conversely, mean higher monthly payments but significantly less interest paid overall. Lenders also tend to offer slightly lower interest rates for shorter terms because their risk is reduced. When looking for the best car loan rates in Kansas City, consider the total cost, not just the monthly payment.

Based on my experience, many buyers gravitate towards longer terms for the lower monthly payment, but this can be a costly mistake. If your budget allows, opting for the shortest term you can comfortably afford will save you substantial money in the long run.

Down Payment: Your Initial Investment

A down payment is the initial amount of money you pay towards the purchase of the vehicle. Making a substantial down payment reduces the amount you need to borrow, which can lead to a lower monthly payment and, often, a better interest rate. Lenders view a larger down payment as a sign of your commitment and reduced risk for them.

Common mistakes to avoid are neglecting a down payment altogether or making a very small one. This can result in being "upside down" on your loan, meaning you owe more than the car is worth, especially with depreciation. Aim for at least 10-20% for a used car and 20% or more for a new vehicle if possible.

A significant down payment also reduces your loan-to-value (LTV) ratio, which is another metric lenders use to assess risk. A lower LTV often translates into more favorable interest rates, helping you secure some of the best car loan rates in Kansas City.

Debt-to-Income Ratio (DTI): Can You Afford It?

Your debt-to-income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to manage monthly payments and repay the loan. A lower DTI indicates you have more disposable income to cover new debt.

While there isn’t a universally fixed DTI cutoff, most lenders prefer borrowers with a DTI of 36% or less, though some might go up to 43% for certain loan types. If your DTI is high, it signals that you might be overextended financially, which could lead to a higher interest rate or even loan denial.

To improve your DTI, consider paying down existing debts or increasing your income before applying for an auto loan. This preparation can significantly improve your chances of getting low interest car loans KC.

Your Lending Avenues in Kansas City: Where to Look

When seeking the best car loan rates in Kansas City, you have several key types of lenders to explore. Each offers distinct advantages, and understanding these differences will help you strategize your approach. Don’t limit yourself to just one option; variety is key to comparison shopping.

Traditional Banks: Local and National Presence

Banks, from large national institutions to smaller local community banks, are a common source for auto loans. They offer a wide range of loan products and often have competitive rates for borrowers with strong credit histories. Many banks also provide convenient online application processes.

Local banks in Kansas City might offer a more personalized touch, especially if you already have an existing relationship with them. They could be more willing to work with long-standing customers. National banks, while sometimes less personal, offer the convenience of widespread branches and robust online platforms.

When approaching banks, be prepared with all your financial documentation. They will thoroughly review your credit history, income, and debt levels. Their rates can vary significantly, so it’s always wise to get quotes from several different institutions.

Credit Unions: Often a Top Contender for Rates

Credit unions are non-profit financial cooperatives owned by their members. This structure often allows them to offer more competitive interest rates on loans and higher yields on savings accounts compared to traditional banks. For Kansas City auto loans, credit unions are frequently among the top contenders for the best rates.

To access a credit union’s services, you usually need to become a member, which often involves meeting certain eligibility criteria (e.g., living in a specific area, working for a particular employer, or being affiliated with a group). Many Kansas City credit unions have broad membership requirements that are easy to meet.

Pro tips from us: Always include local credit unions in your search for low interest car loans KC. Their member-focused approach often translates into excellent customer service and potentially better terms, even for those with less-than-perfect credit.

Dealership Financing: Convenience at a Cost?

Many car dealerships offer financing directly through their finance departments. They act as intermediaries, working with a network of banks and captive lenders (financing arms of car manufacturers like Ford Credit or Toyota Financial Services). This option provides immense convenience, allowing you to complete the car purchase and financing in one location.

Dealerships can sometimes offer attractive promotional rates, especially on new cars from their specific brand. They also have programs for various credit tiers. However, the convenience can sometimes come at a cost; without comparison shopping beforehand, you might not realize if you’re getting the absolute best car loan rates in Kansas City.

Common mistakes to avoid are falling in love with a car and agreeing to the first financing offer without question. Always walk into the dealership with at least one pre-approved loan offer from an external lender. This gives you leverage and a benchmark to compare against.

Online Lenders: Fast and Streamlined Applications

In recent years, online lenders have emerged as a powerful force in the auto loan market. These platforms offer quick pre-approvals, streamlined application processes, and often competitive rates, especially for those with good credit. Their overhead is typically lower, which can sometimes translate into savings for borrowers.

Online lenders provide the flexibility to shop for a loan from the comfort of your home, comparing multiple offers without visiting physical branches. They are a great option for getting auto loan pre-approval Kansas City quickly. However, the process might be less personal than with a local bank or credit union.

Based on my experience, online lenders are excellent for initial rate comparisons. They can provide a solid baseline for what you might expect to pay, which is invaluable when you start negotiating with other lenders or dealerships.

Preparing for Success: Your Car Loan Application Checklist

Securing the best car loan rates in Kansas City isn’t just about finding the right lender; it’s also about presenting yourself as the ideal borrower. Thorough preparation is key to unlocking the most favorable terms.

1. Check Your Credit Score and Report

As mentioned, this is your first and most critical step. Obtain your credit score and a copy of your full credit report from all three major bureaus (Experian, TransUnion, and Equifax). Review them meticulously for any inaccuracies or errors that could be dragging down your score. Disputing errors can sometimes boost your score quickly.

Understanding your score also helps you set realistic expectations for the rates you might qualify for. If your score is lower than you’d like, you might consider taking steps to improve it before applying, even if it means delaying your purchase slightly.

2. Determine Your Budget

Before you even look at cars, establish a clear budget. This includes not just the maximum car price you can afford, but also what you’re comfortable paying monthly, considering insurance, fuel, and maintenance. Don’t forget to factor in the down payment you’re willing to make.

A common mistake is focusing solely on the monthly payment. This can lead to choosing a longer loan term with a higher overall cost. Instead, calculate the total cost of the loan (principal + interest) over its entire duration.

3. Gather Necessary Documents

Lenders will require specific documents to process your application. Having these ready will expedite the process and show you’re a serious applicant. Typical documents include:

- Proof of identity (driver’s license, passport)

- Proof of income (pay stubs, W-2s, tax returns for self-employed)

- Proof of residence (utility bill, lease agreement)

- Bank statements

- Social Security Number

Being organized demonstrates responsibility and makes the application seamless, helping you move closer to securing Kansas City auto loans.

4. Get Pre-Approved for a Loan

This is perhaps the most powerful tool in your car-buying arsenal. Auto loan pre-approval Kansas City means a lender has reviewed your financial information and tentatively approved you for a loan up to a certain amount, at a specific interest rate. This approval is usually valid for a certain period, typically 30-60 days.

With a pre-approval in hand, you transform from a mere car shopper into a cash buyer at the dealership. You know exactly how much you can spend and what your interest rate will be, giving you immense negotiating power. It separates the financing discussion from the car price negotiation, allowing you to focus on getting the best deal on the vehicle itself.

Strategies to Secure the Best Car Loan Rates in Kansas City

Finding the best car loan rates in Kansas City is an active process that requires strategy and diligence. Don’t leave it to chance; employ these proven methods to ensure you get the most favorable terms.

Improve Your Credit Score

Even a slight bump in your credit score can significantly impact your interest rate. If you have time before your purchase, focus on these credit-boosting activities:

- Pay all bills on time, every time.

- Reduce existing debt, especially on credit cards.

- Avoid opening new credit accounts.

- Keep old accounts open (length of credit history helps).

Even a 20-30 point increase can sometimes move you into a better rate tier. This can save you hundreds, if not thousands, over the life of the loan. For more in-depth advice, you might want to Read our guide on ‘Boosting Your Credit Score for a Car Loan’ (internal link placeholder).

Make a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and signals lower risk to lenders. Aim for at least 10-20% of the vehicle’s price. If you can save more, do it. The less you borrow, the less interest you’ll pay overall, even with the same interest rate.

A substantial down payment also protects you from being "upside down" on your loan early on, which is a common scenario with rapidly depreciating assets like cars. This financial stability is appealing to lenders.

Choose a Shorter Loan Term

While tempting for lower monthly payments, longer loan terms (e.g., 72 or 84 months) lead to significantly more interest paid. If your budget allows, opt for a 36-month or 48-month loan. You’ll pay off the car faster and save a considerable amount in interest.

Based on my experience, a 60-month term is often a good balance between manageable monthly payments and reasonable total interest. Anything beyond that should be carefully considered, as the interest burden grows disproportionately.

Shop Around and Compare Offers Aggressively

This is the golden rule for securing the best car loan rates in Kansas City. Don’t settle for the first offer you receive. Apply to multiple lenders – banks, credit unions, and online lenders – within a short timeframe (typically 14-45 days).

Credit bureaus treat multiple auto loan inquiries within this period as a single inquiry, minimizing the impact on your credit score. This allows you to gather several pre-approval offers and then use them to negotiate with each other and with the dealership. This competitive shopping strategy is where you truly win.

Consider a Co-Signer

If you have a limited credit history or a lower credit score, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, taking on equal responsibility for repayment.

Common mistakes to avoid: Ensure both parties fully understand the responsibilities of co-signing. If the primary borrower defaults, the co-signer is legally obligated to make the payments, which can damage their credit. It’s a serious commitment that requires trust and clear communication.

Special Situations for Kansas City Car Buyers

Life happens, and not every car buyer has a pristine credit history or straightforward circumstances. Here’s how to navigate a few common special situations when seeking Kansas City auto loans.

Bad Credit Car Loans in Kansas City

Having bad credit doesn’t mean you can’t get a car loan, but it does mean you’ll likely face higher interest rates. The key is to find lenders specializing in subprime auto loans and to manage your expectations. Many dealerships have "special finance" departments dedicated to helping buyers with challenging credit.

Strategies for bad credit:

- Larger Down Payment: This is even more crucial for bad credit. It reduces the loan amount and signals commitment.

- Shorter Loan Term: While monthly payments will be higher, it can reduce the overall interest paid and the risk to the lender.

- Secured Loans: Some lenders offer secured auto loans, where the car itself acts as collateral.

- Co-signer: A co-signer with good credit can be a game-changer.

- Focus on Improvement: Use this loan as an opportunity to rebuild your credit by making consistent, on-time payments.

Pro tips from us: Be wary of "buy here, pay here" dealerships. While they offer loans regardless of credit, their interest rates are often extremely high, and terms can be unfavorable. Exhaust all other options first, including credit unions, which sometimes offer more forgiving terms for their members.

Refinancing Your Car Loan in KC

If you’ve already secured a car loan but your financial situation has improved, or if interest rates have dropped since you bought your car, refinancing could save you money. Refinance car loan Kansas City options are readily available from banks, credit unions, and online lenders.

Reasons to refinance:

- Lower Interest Rate: If your credit score has improved, you might qualify for a significantly lower rate.

- Lower Monthly Payments: You can extend the loan term (though this might increase total interest) to reduce monthly payments.

- Remove a Co-signer: If your credit is now strong enough, you can refinance to remove a co-signer from the loan.

Based on my experience, refinancing can be a smart move if you can reduce your interest rate by at least 1-2 percentage points. Always calculate the total savings over the life of the new loan, considering any potential fees for refinancing.

Expert Pro Tips from Our Team for Kansas City Auto Finance

Beyond the fundamental strategies, these insights from years in the auto finance world can make a significant difference in your search for the best car loan rates in Kansas City.

Read the Fine Print, Every Single Word

It sounds obvious, but many borrowers overlook this critical step. Don’t just skim the loan agreement. Understand every clause, fee, and condition. Pay close attention to the APR (Annual Percentage Rate), prepayment penalties, and late payment fees.

Common mistakes to avoid are signing without fully understanding the terms. If something isn’t clear, ask for clarification. Don’t be rushed. A reputable lender will be happy to explain everything in detail.

Don’t Just Focus on the Monthly Payment

While managing your budget is crucial, fixating solely on the monthly payment can lead to poor long-term financial decisions. A low monthly payment often comes with a longer loan term and a higher total cost due to increased interest.

Always consider the total cost of the loan (principal + total interest paid) and the APR. A slightly higher monthly payment for a shorter term can save you thousands over the life of the loan.

Beware of Add-ons and Extras

Dealerships often try to sell you various add-ons like extended warranties, GAP insurance, paint protection, or VIN etching. While some might have value, many are highly marked up and can significantly increase your loan amount and, consequently, your interest burden.

Pro tips from us: Negotiate these separately, or better yet, decline them at the dealership and research third-party options. For instance, GAP insurance can often be purchased cheaper from your auto insurance provider.

Negotiate, Negotiate, Negotiate!

Everything is negotiable, from the price of the car to the interest rate on your loan. With pre-approval offers in hand, you have immense leverage. Don’t be afraid to pit lenders against each other. Tell Lender A that Lender B offered you a lower rate and see if they can beat it.

This competitive environment is exactly what you need to secure the best car loan rates in Kansas City. Be confident, be informed, and be persistent.

Common Mistakes to Avoid When Getting a Car Loan

To ensure you don’t fall into common traps, steer clear of these pitfalls that many car buyers encounter:

- Not Checking Your Credit Report: As discussed, errors can cost you. Always review your report for accuracy.

- Only Applying to One Lender: Limiting your options means you’re almost certainly leaving money on the table. Cast a wide net.

- Focusing Solely on Monthly Payments: This can lead to longer terms and higher overall costs. Look at the big picture: total cost and APR.

- Ignoring the APR: The Annual Percentage Rate (APR) is the true cost of borrowing, as it includes the interest rate plus certain fees. Always compare APRs, not just interest rates.

- Getting Emotional: Car buying can be exciting, but don’t let emotions cloud your judgment. Stick to your budget and your pre-determined strategy.

- Skipping Pre-Approval: Walking into a dealership without a pre-approval is like walking into a negotiation unarmed.

For a deeper dive into financial literacy around car loans, you can visit the Consumer Financial Protection Bureau’s (CFPB) auto loan guide (external link placeholder). This trusted resource provides unbiased information to help you make informed decisions.

Your Journey to the Best Car Loan Rates in Kansas City Starts Now!

Finding the best car loan rates in Kansas City is an achievable goal, but it demands diligence, research, and a strategic approach. By understanding the factors that influence your rate, exploring all your lending avenues, preparing thoroughly, and employing smart negotiation tactics, you can significantly reduce the cost of your next vehicle.

Remember, the power is in your hands. Arm yourself with knowledge, compare offers, and don’t be afraid to walk away if the deal isn’t right. Your ideal car and an affordable loan are waiting for you in the vibrant automotive market of Kansas City. Start your journey today and drive away with confidence!