Drive Smarter: Mastering Your Car Loan Calculator With Down Payment

Drive Smarter: Mastering Your Car Loan Calculator With Down Payment Carloan.Guidemechanic.com

Buying a new or used car is an exciting milestone, often representing freedom, convenience, or a necessary upgrade. However, the thrill can quickly fade when confronted with the complexities of financing. For most, securing a car loan is a crucial step in the process, and understanding how your down payment impacts that loan is paramount. This isn’t just about crunching numbers; it’s about making a financially sound decision that serves you well for years to come.

As an expert blogger and SEO content writer with years of experience in personal finance, I’ve seen firsthand how a well-planned car purchase can save thousands of dollars, while a rushed decision can lead to significant financial strain. This comprehensive guide will empower you to navigate the world of car financing, specifically focusing on the indispensable tool that is the car loan calculator with down payment. We’ll dive deep into its mechanics, its benefits, and how to leverage it to secure the best possible deal.

Drive Smarter: Mastering Your Car Loan Calculator With Down Payment

Unpacking the Essentials: Car Loans and Down Payments

Before we punch numbers into any calculator, let’s establish a clear understanding of the fundamental components at play: the car loan and the down payment. Think of them as two sides of the same financial coin, working in tandem to get you behind the wheel.

What Exactly is a Car Loan?

A car loan is a secured loan specifically designed to finance the purchase of a vehicle. When you take out a car loan, a lender (like a bank, credit union, or dealership finance department) provides you with the money to buy the car, and in return, you agree to repay that amount, plus interest, over a set period. The car itself serves as collateral, meaning if you fail to make your payments, the lender has the right to repossess it.

The terms of a car loan typically include the principal amount (the money borrowed), the interest rate (the cost of borrowing), and the loan term (the duration over which you’ll repay the loan, usually in months). Each of these elements significantly influences your monthly payment and the total cost of your vehicle.

The Crucial Role of a Down Payment

A down payment is an initial upfront payment you make towards the purchase price of the car. Instead of financing the entire cost of the vehicle, you contribute a portion of it out of your own pocket. This reduces the amount you need to borrow from the lender. While it might feel like a significant chunk of money to part with initially, a down payment is one of the most powerful tools you have to control your car financing.

Based on my experience helping countless individuals with their vehicle purchases, the down payment isn’t just a formality; it’s a strategic move. It demonstrates your financial commitment to the purchase, signals lower risk to lenders, and directly impacts the terms you’ll receive. Without a down payment, you’d be financing 100% of the car’s value, which can lead to higher monthly payments and greater overall interest costs.

Why Your Down Payment is a Game Changer

Many buyers view a down payment as an obstacle, but savvy car shoppers understand it as an investment that pays dividends throughout the life of the loan. Let’s explore the multifaceted benefits of making a substantial down payment on your next vehicle.

1. Significantly Lower Monthly Payments

This is perhaps the most immediate and tangible benefit. When you make a down payment, you reduce the principal amount of the loan. A smaller loan amount directly translates to lower monthly payments. This can free up cash flow in your budget, making your car more affordable on a day-to-day basis.

Imagine financing a $30,000 car. With no down payment, you borrow $30,000. With a $5,000 down payment, you only borrow $25,000. Even with the same interest rate and loan term, the difference in monthly outlay can be substantial, providing more financial breathing room.

2. Substantial Reduction in Total Interest Paid

While lower monthly payments are great, the long-term savings on interest can be even more impactful. Interest is calculated on the outstanding loan balance. By reducing the principal from the outset with a down payment, you immediately reduce the amount of money on which interest accrues. This effect compounds over the life of the loan.

Pro tips from us: Even a seemingly small increase in your down payment can shave hundreds, if not thousands, off the total interest you’ll pay over a typical 5-year car loan. This is pure savings that stays in your pocket.

3. Access to Better Loan Terms and Lower Interest Rates

Lenders perceive a larger down payment as a sign of financial stability and lower risk. When you have more equity in the car from day one, the lender’s exposure to loss is reduced. This can make you a more attractive borrower, potentially qualifying you for lower interest rates and more favorable loan terms.

Lower interest rates, in turn, further reduce your monthly payments and the overall cost of the loan. It’s a virtuous cycle: more down payment, less risk for the lender, better rates for you.

4. Building Equity from Day One

Equity is the portion of an asset you own outright. With a car, it’s the difference between its market value and what you still owe on the loan. A down payment immediately gives you equity in your vehicle. This is important because cars depreciate rapidly, especially in the first few years.

Starting with equity helps cushion the blow of depreciation. You’re less likely to find yourself in a negative equity situation, which we’ll discuss next.

5. Avoiding Negative Equity (Being "Upside Down")

Negative equity, or being "upside down" on your loan, occurs when you owe more on your car than it’s worth. This is a common pitfall, especially for those who put little or no money down. Since cars lose value quickly, particularly right after purchase, it’s easy to fall into this trap.

If your car is totaled or stolen while you have negative equity, your insurance payout might not cover the full loan amount, leaving you to pay the difference out of pocket. A substantial down payment significantly reduces this risk, providing a buffer against rapid depreciation.

6. Potential Insurance Savings

While not directly related to the loan itself, a higher down payment can indirectly influence your car insurance costs. If you finance less of the car’s value, you might not feel the need to purchase expensive gap insurance, which covers the difference between your car’s actual cash value and the remaining loan balance if your car is totaled or stolen.

However, remember that full coverage insurance is typically required by lenders when you have an outstanding loan. You can read more about to ensure you’re adequately covered.

Deconstructing the Car Loan Calculator With Down Payment

Now that we understand the profound benefits of a down payment, let’s turn our attention to the tool that brings it all together: the car loan calculator with down payment. This isn’t just a simple math tool; it’s a powerful financial planning instrument.

What is a Car Loan Calculator With Down Payment?

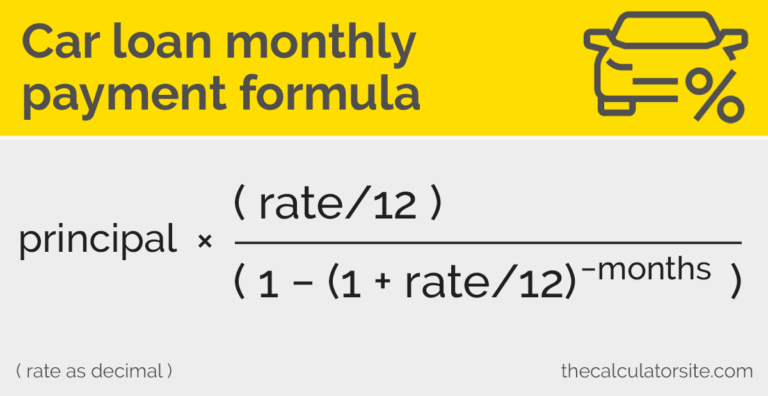

At its core, a car loan calculator with down payment is an online tool that allows you to estimate your potential monthly car payments and the total cost of your loan based on several key financial inputs. Its primary function is to show you how different variables, particularly your down payment, affect your loan outcomes.

This calculator takes the guesswork out of car financing. Instead of wondering "what if," you can plug in various scenarios and see the concrete impact on your budget. It’s a critical first step in setting realistic expectations for your car purchase.

The Key Inputs You’ll Need

To get accurate results from a car loan calculator, you’ll typically need to provide the following information:

- Car Price (or Amount Financed): This is the sticker price of the vehicle you’re considering, before any trade-ins or down payments are applied. If you already know your down payment and trade-in, you might input the ‘amount to finance’ directly.

- Down Payment Amount: This is the cash you plan to put towards the purchase upfront. The calculator will subtract this from the car price to determine the actual loan principal.

- Interest Rate (APR): This is the annual percentage rate (APR) your lender will charge on the loan. It’s crucial to use a realistic estimate here. Your credit score, the loan term, and current market conditions all influence your APR.

- Loan Term (in Months): This is the length of time you have to repay the loan, expressed in months (e.g., 60 months for a 5-year loan, 72 months for a 6-year loan).

The Key Outputs You’ll Receive

Once you input the data, the calculator will quickly process it and present you with vital financial projections:

- Estimated Monthly Payment: This is the most sought-after output. It tells you exactly how much you’ll need to pay each month to cover your loan.

- Total Interest Paid: This figure reveals the total amount of money you’ll pay in interest over the entire life of the loan. It’s often an eye-opener and highlights the long-term cost of borrowing.

- Total Cost of the Loan: This is the sum of your principal loan amount plus the total interest paid. It represents the true cost of financing the car, excluding your down payment.

- Total Cost of the Car (Loan + Down Payment): Some calculators will also show you the full cost of the vehicle, including your down payment plus the total cost of the loan. This provides a complete picture of your investment.

How to Use a Car Loan Calculator Effectively: A Step-by-Step Guide

Using a car loan calculator isn’t just about plugging in numbers once. It’s an iterative process of planning, adjusting, and comparing. Follow these steps to maximize its utility:

Step 1: Determine Your Overall Budget

Before you even look at cars, figure out how much you can truly afford to spend on a car each month, not just on loan payments but also on insurance, fuel, and maintenance. Based on my experience, a common mistake is to focus solely on the monthly payment without considering the bigger picture.

Step 2: Research Car Prices

Identify the specific car models you’re interested in and get a realistic estimate of their market value, both new and used. Websites like Kelley Blue Book or Edmunds are excellent resources for this.

Step 3: Estimate Your Down Payment

Decide how much cash you can realistically put down. Be honest with yourself and avoid depleting your emergency savings. We’ll discuss strategies for maximizing your down payment later.

Step 4: Get Pre-Approved or Estimate Interest Rates

Before visiting a dealership, consider getting pre-approved for a car loan from your bank or credit union. This gives you a concrete interest rate to work with and strengthens your negotiating position. If pre-approval isn’t an option yet, use an estimated APR based on your credit score range. You can learn more about how your credit score impacts loans in our .

Step 5: Experiment with Loan Terms

Play around with different loan terms (e.g., 48, 60, 72, or even 84 months). Observe how extending the loan term lowers your monthly payment but significantly increases the total interest paid. Aim for the shortest term you can comfortably afford.

Step 6: Analyze the Results and Run Multiple Scenarios

This is where the magic happens.

- Scenario 1 (Baseline): Input your desired car price, your estimated down payment, a realistic interest rate, and your preferred loan term. Note the monthly payment and total interest.

- Scenario 2 (Increased Down Payment): Increase your down payment by $1,000 or $2,000. How much does your monthly payment drop? How much interest do you save?

- Scenario 3 (Shorter Loan Term): Keep your down payment the same, but reduce the loan term (e.g., from 72 months to 60 months). See how the monthly payment increases but the total interest decreases dramatically.

- Scenario 4 (Lower Interest Rate): If you improve your credit score or find a better lender, how would a 0.5% or 1% lower interest rate impact your payments?

Pro tips from us: Don’t just settle for the first calculation. The power of the calculator lies in its ability to show you the impact of adjustments. Run as many scenarios as you need to feel confident in your budget.

Strategies for Building and Maximizing Your Down Payment

A larger down payment is almost always beneficial. But how do you accumulate that significant sum without feeling overwhelmed? Here are some effective strategies:

1. Start Saving Diligently and Early

The most straightforward method is to save specifically for your car down payment. Set a realistic goal and create a dedicated savings account. Treat this savings goal with the same importance as any other bill. Even small, consistent contributions add up over time.

Consider setting up automatic transfers from your checking account to your down payment fund immediately after you get paid. Out of sight, out of mind, and your savings grow without you actively thinking about it.

2. Sell Your Current Vehicle Outright

If you have an older car you no longer need, selling it privately can often yield more money than trading it in at a dealership. Use the proceeds directly towards your down payment. This requires a bit more effort (listing, showing, negotiating), but the financial reward can be substantial.

Be realistic about your car’s value. Use online tools to get an accurate appraisal before setting your price.

3. Leverage Tax Refunds or Bonuses

Any unexpected windfalls, such as a tax refund, work bonus, or inheritance, can be excellent sources for a down payment. Instead of spending them, earmark these funds for your car purchase. This can significantly boost your down payment without impacting your regular budget.

4. Strategically Utilize a Trade-In

While selling privately often gets you more, trading in your current car offers convenience. The dealership handles the paperwork and takes the old vehicle off your hands. The value of your trade-in can then be applied directly to your new car’s down payment.

However, be prepared: dealerships often offer wholesale prices for trade-ins. Do your research beforehand using sites like Edmunds or KBB to know your car’s trade-in value, so you can negotiate effectively.

Common Mistakes to Avoid When Saving for a Down Payment:

- Draining Your Emergency Fund: Never use money from your emergency fund for a down payment. That fund is for unexpected crises, not planned purchases.

- Borrowing for a Down Payment: Taking out another loan to cover your down payment is a dangerous financial move. It adds more debt and typically comes with its own interest, negating the benefits of the down payment.

The Interplay of Interest Rates and Loan Terms

Beyond the down payment, two other critical factors heavily influence your car loan: the interest rate and the loan term. Understanding how they interact is key to optimizing your financing.

The Impact of the Interest Rate (APR)

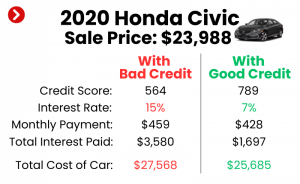

The interest rate, or Annual Percentage Rate (APR), is essentially the cost of borrowing money. It’s expressed as a percentage of the loan amount. A higher APR means you pay more in interest over the life of the loan, while a lower APR means you pay less. Your credit score is the biggest determinant of the APR you’ll qualify for.

Based on my experience as a financial advisor, even a difference of one or two percentage points in your APR can result in hundreds, if not thousands, of dollars saved over the entire loan term. That’s why improving your credit score before applying for a loan is one of the most valuable financial preparations you can make.

The Influence of the Loan Term

The loan term is the length of time you have to repay the loan. Common terms range from 36 to 84 months.

- Shorter Loan Terms (e.g., 36-48 months): These typically result in higher monthly payments but significantly lower total interest paid. You own the car outright faster, building equity more quickly.

- Longer Loan Terms (e.g., 72-84 months): These offer lower monthly payments, making the car seem more "affordable." However, you’ll pay much more in total interest over the longer period. You also risk being upside down on your loan for a longer duration as the car depreciates.

Pro tips from us: While a longer term might seem appealing due to lower monthly payments, always calculate the total cost of the loan with the car loan calculator. You’ll often find that the "sweet spot" for balancing affordability and total cost is around 60 months, but your personal financial situation may dictate otherwise.

Beyond the Calculator: Other Costs to Factor In

A car loan calculator with down payment provides a fantastic estimate for your loan, but it doesn’t cover every expense associated with car ownership. To get a truly accurate picture of your budget, you must consider these additional costs:

- Sales Tax: This is usually a percentage of the car’s purchase price and varies by state. It’s a significant upfront cost that’s often rolled into your loan if you don’t pay it out of pocket.

- Registration and Licensing Fees: These are recurring fees required by your state to legally operate your vehicle. They can vary widely.

- Car Insurance: You’ll need comprehensive and collision insurance if you have a loan. This is an ongoing monthly or semi-annual expense that can be substantial, especially for newer or more expensive vehicles.

- Fuel Costs: Don’t forget the cost of gasoline or charging for electric vehicles. Consider your daily commute and average mileage.

- Maintenance and Repairs: All cars require regular maintenance (oil changes, tire rotations) and eventually, repairs. Factor these into your long-term budget.

- Gap Insurance: If you put a small down payment, gap insurance is highly recommended. It covers the "gap" between what you owe on your loan and what your standard auto insurance will pay if your car is totaled or stolen.

Common mistakes to avoid are focusing solely on the monthly car payment and neglecting these other crucial expenses, leading to an overstretched budget.

When a Smaller Down Payment Might Be Considered (with Caution)

While a substantial down payment is almost always advisable, there are specific circumstances where a smaller down payment, or even none, might be considered, though it comes with inherent risks.

- Exceptional Credit Score and Low-Interest Rate: If you have an immaculate credit score (e.g., 800+) and qualify for a promotional 0% APR or extremely low-interest rate, the benefit of reducing interest paid by a large down payment is diminished. However, even then, a down payment reduces the principal and thus the monthly payment.

- High-Yield Savings/Investment Account: If your money is earning a higher return in a high-yield savings account or investment than the interest rate you’d pay on the car loan, it could theoretically be more financially advantageous to keep your cash invested. This requires careful calculation and a strong understanding of financial markets, and it’s generally not recommended for the average car buyer due to market volatility.

- Short Loan Term: If you commit to a very short loan term (e.g., 24-36 months), the risk of being upside down on your loan is reduced, even with a smaller down payment, because you’re paying down the principal quickly. However, this also means very high monthly payments.

Important Caveat: Even in these scenarios, a down payment still reduces your monthly payment and your overall financial exposure. Always aim for a substantial down payment if your financial situation allows.

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with the best intentions, users can make errors that lead to inaccurate financial planning. Be mindful of these common pitfalls:

- Ignoring Additional Costs: As discussed, focusing only on the car’s price and loan payment without factoring in tax, title, registration, and insurance can lead to budgeting surprises.

- Assuming a Low Interest Rate: Don’t just pick the lowest interest rate you see online. Get pre-approved or use a realistic rate based on your credit score to ensure your calculations are accurate.

- Focusing Only on the Monthly Payment: While important, the monthly payment shouldn’t be your sole focus. Always look at the total interest paid and the total cost of the car over the loan term. A low monthly payment often means a longer loan and much more interest paid.

- Not Accounting for Trade-In Value Properly: If you’re trading in a car, ensure you get a fair and accurate valuation. Don’t let the dealership inflate your trade-in value only to inflate the new car’s price. Use online valuation tools beforehand.

- Not Trying Different Scenarios: The power of the calculator is in its flexibility. Failing to run multiple scenarios with varying down payments, interest rates, and loan terms means you’re missing out on optimizing your deal.

The Power of Pre-Approval: Your Secret Weapon

Before you step foot on a dealership lot, one of the most strategic moves you can make is to get pre-approved for a car loan from an independent lender (like your bank or credit union).

What is Pre-Approval?

Pre-approval means a lender has reviewed your credit history and financial situation and has conditionally agreed to lend you a specific amount of money at a particular interest rate, subject to final verification.

Why is Pre-Approval Beneficial?

- Negotiating Power: You walk into the dealership knowing exactly how much you can borrow and at what rate. This gives you immense leverage, as you can negotiate the car price as a cash buyer, rather than being swayed by monthly payment figures.

- Realistic Rates: It provides you with a realistic interest rate to plug into your car loan calculator, making your financial planning much more accurate.

- Focus on the Car Price: With financing squared away, you can focus solely on negotiating the best possible price for the vehicle itself, rather than getting caught up in confusing payment discussions.

- Avoid Dealer Markups: Dealerships often try to mark up interest rates on loans. With a pre-approval in hand, you can confidently decline less favorable rates offered by the dealer’s finance department.

Consulting trusted external sources like this can provide additional peace of mind and reinforce your knowledge.

Building Your Financial Confidence for the Road Ahead

The journey to buying a car can feel daunting, filled with jargon and complex financial decisions. However, by understanding the mechanics of a car loan calculator with down payment, you’re not just buying a vehicle; you’re investing in financial literacy and control.

Empowerment comes from knowledge. When you meticulously plan your purchase, understand the impact of every variable, and use tools like the calculator effectively, you transform from a passive buyer into an informed negotiator. This approach doesn’t just save you money; it builds confidence in your financial decision-making abilities, a skill that extends far beyond car buying.

Conclusion: Drive Away with Confidence

The car loan calculator with down payment is more than just a convenient online tool; it’s an indispensable ally in your car-buying journey. It demystifies the financing process, allowing you to visualize the impact of your choices on your budget and long-term financial health. By understanding the power of a solid down payment, exploring various loan terms and interest rates, and factoring in all associated costs, you can make an informed decision that saves you money and stress.

Remember, a substantial down payment is your strongest leverage, leading to lower monthly payments, reduced total interest, and greater equity from day one. Combine this with strategic use of the car loan calculator and the advantage of pre-approval, and you’re well on your way to securing the best possible deal on your next vehicle.

Don’t leave your car financing to chance. Start planning, use a reliable car loan calculator with down payment, and drive away with confidence, knowing you’ve made a smart financial choice. Your wallet will thank you for it.