Drive Smarter, Not Harder: Your Ultimate Guide to Securing Thrifty Car Loans

Drive Smarter, Not Harder: Your Ultimate Guide to Securing Thrifty Car Loans Carloan.Guidemechanic.com

Buying a car is a significant financial decision, often ranking as one of the largest purchases many individuals make after a home. It’s an exciting prospect, envisioning yourself cruising in a new (or new-to-you) vehicle. However, the excitement can quickly turn into anxiety when faced with complex financing options, high interest rates, and the fear of overpaying. This is precisely where the concept of "Thrifty Car Loans" comes into play – a strategic approach to financing your vehicle that prioritizes long-term savings, financial stability, and smart decision-making.

This comprehensive guide is designed to empower you with the knowledge and tools needed to navigate the car loan landscape with confidence. We’ll delve deep into every facet of securing an affordable auto loan, ensuring you understand not just what to do, but why it matters. Our goal is to transform you from a passive borrower into an informed, savvy consumer, capable of securing a deal that truly benefits your wallet. By the end of this article, you’ll be well-equipped to make choices that lead to substantial savings over the lifetime of your car loan, proving that driving smarter begins with financing smarter.

Drive Smarter, Not Harder: Your Ultimate Guide to Securing Thrifty Car Loans

Understanding the "Thrifty" Mindset in Car Financing

Being "thrifty" isn’t about being cheap; it’s about being smart, strategic, and resourceful with your money. When applied to car loans, it means looking beyond the attractive monthly payment and considering the total cost of ownership over the entire loan term. A thrifty approach aims to minimize interest paid, reduce overall expenses, and align your car purchase with your broader financial goals.

This mindset requires a proactive stance. It involves thorough research, careful budgeting, and a willingness to negotiate. It’s about making informed decisions that prevent financial strain down the road, ensuring your car is an asset that enhances your life, rather than a burden that depletes your savings. Ultimately, a thrifty car loan is one that respects your budget and contributes to your financial well-being.

The Cornerstone of Thrifty Car Loans: Your Credit Score

Your credit score is arguably the single most important factor influencing the interest rate you’ll be offered on a car loan. Lenders use this three-digit number to assess your creditworthiness – essentially, how risky you are as a borrower. A higher credit score signals a lower risk, translating directly into more favorable interest rates and better loan terms. Conversely, a lower score can mean significantly higher interest, costing you thousands more over the life of the loan.

Based on my experience, individuals with excellent credit scores (typically 720+) often qualify for the absolute best rates, sometimes even 0% APR promotions. Even a difference of a few points can shift you into a different tier of interest rates. Therefore, understanding and improving your credit score should be one of your top priorities before even stepping foot in a dealership or applying for a loan.

Common mistakes to avoid include applying for multiple lines of credit or loans in a short period, which can temporarily ding your score. Also, failing to check your credit report for errors can lead to an unfairly low score. It’s crucial to obtain your free credit report from annualcreditreport.com and dispute any inaccuracies promptly. A healthy credit score is your most powerful tool in securing a truly thrifty car loan.

Setting a Realistic Budget: The First Step to a Thrifty Loan

Before you even start browsing cars, the absolute first step towards a thrifty car loan is to establish a realistic budget. This goes far beyond just calculating a comfortable monthly payment. You need to consider the total cost of car ownership, which includes not only the loan principal and interest but also insurance premiums, fuel costs, maintenance, repairs, and even potential registration fees.

Pro tip from us: Many people make the mistake of focusing solely on the monthly payment. While important, a low monthly payment might come with a longer loan term, meaning you pay significantly more in interest over time. Instead, determine your maximum affordable total car cost. Use online calculators to factor in these additional expenses.

Consider your overall financial picture. How will a car payment impact your ability to save for other goals, pay off existing debt, or cover unexpected emergencies? A thrifty budget means selecting a car and a loan that fits comfortably within your financial capacity, without stretching your resources thin. It’s about sustainable affordability, not just initial affordability.

Down Payments: Your Secret Weapon for Thrifty Financing

Making a substantial down payment is one of the most effective strategies for securing a thrifty car loan. A down payment directly reduces the amount of money you need to borrow, which in turn reduces the total interest you’ll pay over the life of the loan. It’s like putting money in your own pocket in the long run.

Beyond saving on interest, a larger down payment can also make you a more attractive borrower to lenders. It shows financial responsibility and reduces the lender’s risk, potentially qualifying you for even lower interest rates. Furthermore, a significant down payment can help you avoid being "upside down" on your loan – owing more than the car is worth – which is a common problem with minimal or no down payment loans.

Strategies for saving for a down payment include setting aside a portion of your income each month, selling an old car, or even delaying your purchase for a few months to accumulate more funds. While 10-20% of the car’s value is often recommended, any amount you can put down will make a difference. Every dollar saved on interest is a dollar you keep.

Exploring Your Thrifty Car Loan Options

The car loan market is diverse, offering various avenues for financing. To secure a truly thrifty car loan, it’s essential to explore all your options rather than settling for the first offer you receive. Each type of lender has its own advantages and disadvantages, and what works best for one person might not be ideal for another.

Dealership Financing: This is often the most convenient option, as you can arrange financing directly at the dealership. They act as intermediaries, connecting you with various lenders. While convenient, the rates offered might not always be the most competitive, as they often include a markup for the dealership. However, dealerships sometimes offer special promotional rates, especially on new vehicles, which can be very attractive.

Banks and Credit Unions: These traditional financial institutions are often excellent sources for competitive car loan rates. Credit unions, in particular, are known for offering lower interest rates and more personalized service due to their member-owned structure. If you have an existing relationship with a bank or credit union, start there. They may offer preferred rates or streamlined application processes for their loyal customers.

Online Lenders: The rise of online lending platforms has revolutionized car financing. These lenders offer speed, convenience, and often highly competitive rates because they have lower overhead costs. Websites like LightStream, Capital One Auto Finance, or others allow you to apply for pre-approval from the comfort of your home, often receiving multiple offers in minutes. This allows for easy comparison shopping without pressure.

Based on my experience, it’s crucial to shop around extensively. Don’t limit yourself to just one type of lender. Get quotes from at least three different sources – a dealership, a bank/credit union, and an online lender – to ensure you’re getting the best possible rate and terms for your financial situation.

The Pre-Approval Advantage: Empowering Your Car Hunt

One of the most powerful tools in your thrifty car loan arsenal is loan pre-approval. Pre-approval means a lender has reviewed your financial information, including your credit score and income, and has provisionally agreed to lend you a certain amount of money at a specific interest rate. This process typically involves a "hard inquiry" on your credit report, so it’s best done when you’re serious about buying.

The benefit of pre-approval is immense. It transforms you from a speculative shopper into a cash buyer, giving you significant leverage at the dealership. You walk in knowing exactly how much you can spend and what interest rate you’ve already secured. This allows you to focus solely on negotiating the car’s price, rather than getting entangled in discussions about financing terms, which dealers often use to maximize their profits.

Common mistake to avoid: Many buyers head to the dealership without pre-approval, putting themselves at a distinct disadvantage. Without a pre-approved offer in hand, you have no benchmark to compare against the dealership’s financing options. This can lead to accepting a higher interest rate than you deserve. With pre-approval, you can confidently say, "I already have financing at X%." If the dealer can’t beat it, you walk away with your pre-approved loan.

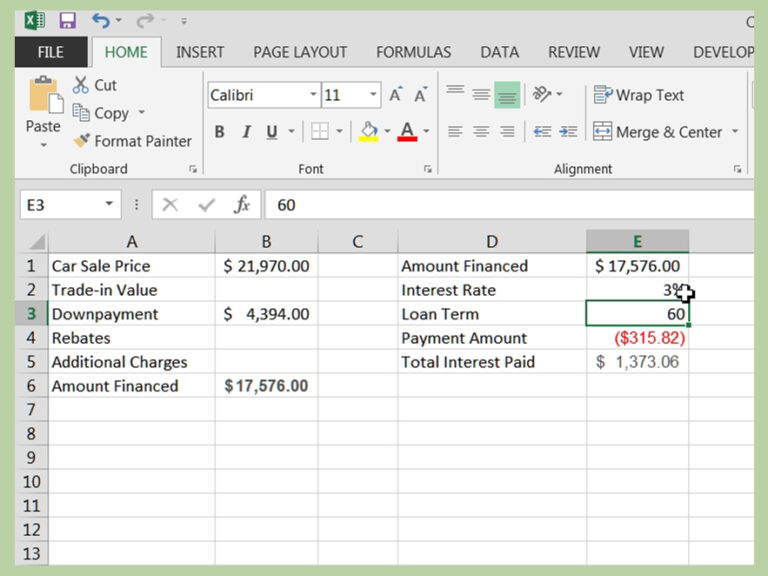

Deciphering Loan Terms: Interest Rates, APR, and Loan Duration

Understanding the jargon associated with car loans is vital for making thrifty decisions. The two most critical terms are the interest rate and the Annual Percentage Rate (APR), along with the loan duration. Misinterpreting these can cost you dearly.

The interest rate is the percentage charged by the lender for borrowing the principal amount. It determines how much extra you pay on top of the car’s price. However, the Annual Percentage Rate (APR) is the true annual cost of borrowing money, encompassing not only the interest rate but also any additional fees or charges associated with the loan. Always compare APRs, as this gives you a more accurate picture of the total cost. A loan with a slightly lower interest rate but higher fees might actually have a higher APR.

The loan duration, or term, refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term might offer lower monthly payments, it almost always results in paying significantly more interest over the life of the loan. For example, a 72-month loan might have lower monthly payments than a 48-month loan, but the cumulative interest paid will be substantially higher.

Pro tip: Aim for the shortest loan term you can comfortably afford. This minimizes the total interest paid and helps you build equity in your vehicle faster. A thrifty car loan balances an affordable monthly payment with a manageable loan duration to keep overall costs down.

Navigating the Application Process for Thrifty Car Loans

Once you’ve done your research, set your budget, and secured pre-approval offers, the actual application process is relatively straightforward. However, being prepared can make it even smoother and faster. Lenders need to verify your identity, income, and financial stability before finalizing a loan.

Typically, you’ll need to provide documentation such as proof of income (pay stubs, tax returns), proof of residence (utility bills, lease agreement), government-issued identification (driver’s license), and details about your current debts and assets. Some lenders may also request bank statements to verify your cash flow. Having these documents organized and readily available will expedite the process.

Lenders look for consistency and reliability. A stable employment history, a low debt-to-income ratio, and a solid credit history all contribute to a favorable application. If you have any unusual circumstances, such as recent job changes or gaps in employment, be prepared to explain them clearly. Transparency and preparation are key to a successful and thrifty car loan application.

Hidden Costs and Fees: What to Watch Out For

While the interest rate and APR are major components of your car loan cost, it’s crucial to be aware of other potential fees that can inflate the total amount you pay. A thrifty borrower scrutinizes every line item in the loan agreement to avoid unexpected expenses. These "hidden costs" can significantly erode your savings if not identified and challenged.

Common fees include origination fees, which are charges for processing the loan; documentation fees, charged by dealerships for handling paperwork; and prepayment penalties, which are fees for paying off your loan early. While some fees are standard, others can be negotiable or simply unnecessary. Always ask for a detailed breakdown of all charges.

Pro tip from us: Always read the fine print of your loan agreement carefully before signing. Don’t hesitate to ask questions about any fee you don’t understand or that seems excessive. If a lender or dealership is unwilling to provide clear explanations or tries to rush you, consider it a red flag. A truly thrifty car loan has transparent terms with minimal, justifiable fees.

Negotiating Like a Pro: Securing the Best Deal

Negotiation is a critical skill for securing a thrifty car loan. It’s not just about the interest rate; it’s about the entire package – the car’s price, your trade-in value, and the financing terms. Approaching these aspects separately and strategically can yield significant savings.

First, always negotiate the car’s price independently of your financing. Having a pre-approval in hand empowers you to do this, as you’re effectively a cash buyer. Focus on getting the lowest possible price for the vehicle first. Once that’s settled, then you can compare your pre-approved loan offer with any financing the dealership might present. If the dealer can beat your pre-approved rate, fantastic; if not, stick with your external loan.

Based on my experience, confidence comes from preparation. Know the market value of the car you want and the value of your trade-in (if applicable). Don’t be afraid to walk away if the deal isn’t right. There are always other cars and other dealerships. Remember, the goal is a thrifty car loan, which means getting the best overall value, not just the lowest monthly payment.

Beyond the Purchase: Smart Management of Your Thrifty Car Loan

Securing a thrifty car loan is a fantastic start, but smart financial management doesn’t end when you drive off the lot. How you manage your loan over its term can further enhance your savings and financial well-being. Proactive loan management ensures you stay on track and potentially save even more.

One excellent strategy is to make extra payments whenever possible. Even small additional payments can significantly reduce the principal balance, which in turn reduces the total interest paid and shortens your loan term. You can achieve this by rounding up your monthly payment or making a lump sum payment if you receive a bonus or tax refund. Ensure your loan agreement doesn’t have prepayment penalties before doing so.

Another key aspect is budgeting for ongoing car expenses. A thrifty mindset includes anticipating costs like routine maintenance (oil changes, tire rotations), unexpected repairs, and fuel. Setting aside a dedicated fund for these expenses prevents them from becoming financial emergencies and ensures you can keep your vehicle running smoothly without falling into debt. is also crucial, as comprehensive coverage protects your investment.

When to Consider Refinancing Your Car Loan

Life circumstances and market conditions can change, offering opportunities to make your existing car loan even thriftier. Refinancing means replacing your current car loan with a new one, typically with a different lender or different terms. It’s a strategy worth considering if you can secure a significantly better deal.

There are several compelling reasons to refinance. If your credit score has improved substantially since you first took out the loan, you might qualify for a much lower interest rate. Similarly, if overall interest rates in the market have dropped, refinancing could save you money. Shortening your loan term to pay it off faster, or extending it slightly to lower monthly payments (though this increases total interest), are also valid reasons.

Before refinancing, compare the new loan’s APR, term, and any associated fees to your current loan. Ensure the savings outweigh any costs involved in the refinancing process. provides excellent tips that can help you qualify for better refinancing rates. A thrifty borrower regularly reviews their financial obligations, always looking for opportunities to optimize and save.

Conclusion: Your Journey to Thrifty Car Ownership

Securing a thrifty car loan is not a matter of luck; it’s a result of diligent preparation, informed decision-making, and proactive management. By understanding the critical role of your credit score, setting a realistic budget, exploring diverse lending options, and mastering the art of negotiation, you empower yourself to make smart financial choices that benefit you for years to come.

Remember, a thrifty car loan means more than just a low monthly payment. It signifies a minimized total cost of ownership, reduced interest payments, and a vehicle that genuinely enhances your life without becoming a financial burden. This comprehensive guide has provided you with the foundational knowledge to approach car financing with confidence and expertise.

Now, armed with this invaluable information, you are ready to embark on your journey to thrifty car ownership. Take control, ask questions, compare offers, and never settle for a deal that doesn’t align with your financial goals. Your wallet will thank you. For more trusted financial advice, consider visiting resources like the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/. Start your thrifty car loan journey today and drive smarter, not harder!