Drive Smarter: Unleashing the Power of the SECU Car Loan Calculator for Your Next Vehicle

Drive Smarter: Unleashing the Power of the SECU Car Loan Calculator for Your Next Vehicle Carloan.Guidemechanic.com

The dream of a new car often comes with the exciting rush of possibilities – the open road, new adventures, and that unmistakable new car smell. However, for many, this excitement can quickly turn into anxiety when faced with the complexities of car financing. Understanding interest rates, loan terms, and monthly payments can feel like navigating a maze.

This is precisely where a powerful tool like the SECU Car Loan Calculator becomes your indispensable co-pilot. It’s more than just a simple online widget; it’s a gateway to financial clarity, empowering you to make informed decisions and secure the best possible deal for your next vehicle.

Drive Smarter: Unleashing the Power of the SECU Car Loan Calculator for Your Next Vehicle

In this super comprehensive guide, we’re going to dive deep into everything you need to know about the SECU Car Loan Calculator. We’ll explore its features, how to use it effectively, common pitfalls to avoid, and crucial financial planning strategies that will put you in the driver’s seat of your car buying journey. Our goal is to equip you with the knowledge to not just dream about your next car, but to own it with confidence and peace of mind.

Why a Car Loan Calculator is Your Best Friend Before Buying a Car

Embarking on the car buying journey without a clear financial roadmap is akin to setting off on a long trip without GPS. You might eventually get there, but you’ll likely encounter unexpected detours and frustrations along the way. A reliable auto loan calculator, especially one provided by a trusted institution like SECU, acts as your financial GPS.

Based on my experience, many car buyers jump into showrooms without a clear financial picture. They get caught up in the excitement of a new model or a great deal on the sticker price, only to be surprised by the actual monthly payment or the total cost of the loan. This can lead to buyers stretching their budget too thin or, worse, walking away from a deal they thought was perfect.

The primary benefit of using a car loan calculator is the ability to visualize your financial commitment before you even step foot in a dealership. It allows you to experiment with different scenarios, understand the impact of various interest rates and loan terms, and ultimately define a comfortable monthly payment that aligns with your budget. This proactive approach transforms you from a reactive buyer into an informed negotiator, ready to secure a loan that truly works for you.

Diving Deep into the SECU Car Loan Calculator: What It Is and How It Works

So, what exactly is the SECU Car Loan Calculator? At its core, it’s a free, user-friendly online tool provided by State Employees’ Credit Union (SECU) designed to help prospective car buyers estimate their potential monthly car loan payments. It’s a simulation tool that takes a few key pieces of information and, in return, provides a snapshot of your future financial obligations.

The calculator operates on a straightforward principle: you input specific financial variables, and it crunches the numbers to give you an estimated monthly payment. This isn’t just a random guess; it uses a standard loan amortization formula to accurately project your payment schedule. Understanding how it works demystifies the car financing process, making it accessible even for those new to borrowing.

Pro tips from us: Always use the most accurate figures you have when inputting data into the calculator. Even small differences in interest rates or loan amounts can significantly alter your estimated monthly payment, so precision is key for truly valuable insights. The calculator empowers you to play "what if" scenarios, giving you control over your financial planning.

Mastering the Inputs: Variables You Need to Understand

To get the most accurate and useful results from the SECU Car Loan Calculator, you need to understand the three primary variables it requires: the loan amount, the interest rate, and the loan term. Each of these plays a critical role in determining your final monthly payment and the total cost of your loan.

1. The Loan Amount: How Much Do You Really Need?

The "loan amount" isn’t simply the sticker price of the car. It’s the total sum of money you intend to borrow after factoring in any down payment, trade-in value, and potentially other costs. For instance, if a car costs $30,000, and you have a $5,000 down payment, your loan amount would be $25,000.

However, it’s crucial to remember that the total amount you need to finance often includes more than just the vehicle’s price. Sales tax, registration fees, title fees, and sometimes even an extended warranty or GAP insurance can be rolled into your loan. Common mistakes to avoid are underestimating the total amount needed, which can lead to unpleasant surprises or a larger loan than anticipated. Always consider all potential costs when determining your true loan amount.

2. The Interest Rate (APR): Your Cost of Borrowing

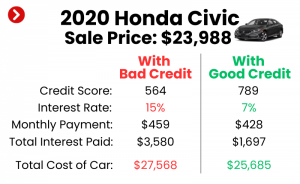

The interest rate, often expressed as an Annual Percentage Rate (APR), is arguably the most impactful variable. It represents the cost of borrowing money from SECU, or any lender for that matter. A lower interest rate means you pay less over the life of the loan, while a higher rate significantly increases your total cost.

Several factors influence the interest rate you qualify for. Your credit score is paramount; a higher score typically indicates less risk to lenders, leading to better rates. Other factors include the loan term (shorter terms often have lower rates), market conditions, and the lender’s specific policies. For the most accurate estimations with the SECU Car Loan Calculator, you’ll want to check SECU’s current auto loan rates, which are usually published on their official website. You can find up-to-date information directly from their official site at .

3. The Loan Term: Finding Your Sweet Spot

The loan term, also known as the loan duration, is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This variable has a direct and significant impact on both your monthly payment and the total interest you’ll pay.

A shorter loan term, such as 36 or 48 months, means higher monthly payments because you’re paying off the principal faster. However, it also means you’ll pay significantly less in total interest over the life of the loan. Conversely, a longer loan term, like 72 or 84 months, results in lower monthly payments, making the car seem more affordable in the short term. The trade-off, however, is that you’ll pay substantially more in total interest due to the extended borrowing period. Finding the sweet spot between an affordable monthly payment and a reasonable total interest cost is a key part of financial planning.

Step-by-Step Guide: Using the SECU Car Loan Calculator Effectively

Using the SECU Car Loan Calculator is straightforward, but knowing the best practices ensures you get the most out of this powerful tool. Let’s walk through the process step-by-step to maximize your financial insights.

- Navigate to SECU’s Official Website: Your first step is to visit the State Employees’ Credit Union website. Always ensure you are on the legitimate site to access accurate and secure tools.

- Locate the Car Loan Calculator: Look for sections related to "Loans," "Auto Loans," or "Calculators." Most financial institutions prominently feature these tools for easy access.

- Input Your Desired Loan Amount: This is the net amount you plan to borrow after any down payment or trade-in. As discussed, make sure to factor in taxes and fees for a realistic figure.

- Enter Your Estimated Interest Rate (APR): This is where checking SECU’s current rates becomes crucial. Use the rate you anticipate qualifying for based on your credit score and the loan term you’re considering. If unsure, use an average rate provided by SECU as a starting point, and then try a range of rates to see the impact.

- Select Your Desired Loan Term: Choose the number of months you’d like to take to repay the loan (e.g., 60 months for a 5-year loan).

- Calculate and Interpret Results: Once all variables are entered, click "Calculate" (or similar). The calculator will instantly display your estimated monthly payment and often the total interest you’d pay over the life of the loan.

Pro tip: Don’t just run one scenario. Experiment! Try different loan amounts (e.g., with a larger or smaller down payment), various interest rates (if you’re unsure of your exact qualification), and different loan terms. This allows you to see how each variable impacts your budget and helps you find a comfortable and sustainable payment plan.

Beyond the Calculator: Essential Financial Planning for Your Car Purchase

While the SECU Car Loan Calculator is an invaluable tool, it’s just one piece of the larger financial planning puzzle. A truly smart car purchase requires a holistic approach that considers several other critical factors.

1. Your Credit Score: The Foundation of Your Loan

Your credit score is arguably the most important number when it comes to securing a car loan. It’s a three-digit representation of your creditworthiness, and lenders use it to assess the risk of lending to you. A higher credit score (generally above 700) typically qualifies you for lower interest rates, saving you thousands over the life of the loan.

Based on my experience, many first-time buyers overlook the importance of checking their credit score before applying for a loan. Knowing your score allows you to address any inaccuracies or take steps to improve it, such as paying down existing debts or correcting errors on your credit report. For more detailed advice on improving your credit score, check out our guide on .

2. The Power of a Down Payment

Making a significant down payment is one of the smartest financial moves you can make when buying a car. A larger down payment directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also helps you build equity in your vehicle faster and can even help you qualify for better interest rates.

Consider aiming for at least 10-20% of the car’s purchase price as a down payment. This not only lightens your loan burden but also provides a buffer against depreciation, helping to prevent you from being "upside down" on your loan (owing more than the car is worth).

3. Understanding Your Trade-In Value

If you have an existing vehicle, trading it in can significantly reduce the amount you need to finance for your new car. Before heading to the dealership, get an estimate of your car’s trade-in value from reputable sources like Kelley Blue Book or Edmunds. This information gives you leverage in negotiations and helps you accurately determine your final loan amount.

Don’t just accept the first offer from a dealership; having an independent valuation empowers you to negotiate a fair price for your trade-in, further optimizing your overall car purchase.

4. Budgeting for Ownership Costs: Beyond the Monthly Payment

Common mistakes to avoid are focusing solely on the monthly loan payment and forgetting about the ongoing costs of car ownership. These expenses can add up quickly and significantly impact your overall budget.

Consider these crucial ownership costs:

- Car Insurance: Premiums vary widely based on your vehicle, driving record, age, and location. Get quotes before you buy.

- Fuel Costs: Estimate your weekly or monthly fuel expenses based on your commute and driving habits.

- Maintenance and Repairs: All cars need regular maintenance (oil changes, tire rotations) and occasional repairs. Factor in a contingency fund.

- Registration and Licensing Fees: Annual fees can vary by state and vehicle type.

By budgeting for these additional expenses, you ensure that your new car truly fits within your financial comfort zone.

5. The Advantage of Loan Pre-Approval

Getting pre-approved for a car loan before you start shopping is a game-changer. It means SECU, or another lender, has already reviewed your credit and determined the maximum amount you qualify for, along with an estimated interest rate. This transforms you into a cash buyer in the eyes of the dealership, giving you immense negotiation power on the vehicle’s price.

You’ll know your budget limits beforehand, avoiding the pressure of on-the-spot financing decisions. For a deeper dive into this topic, refer to our article on .

The SECU Advantage: Why Consider a Car Loan with SECU?

When it comes to securing an auto loan, choosing the right lender is just as important as choosing the right car. State Employees’ Credit Union (SECU) stands out for several compelling reasons, offering a distinct advantage to its members.

SECU operates as a not-for-profit financial cooperative, meaning it’s owned by its members, not by external shareholders. This fundamental difference translates into a member-centric approach where the focus is on providing value back to the members. Based on my experience, this often results in more competitive rates and lower fees compared to traditional banks.

They offer flexible loan terms designed to fit a variety of budgets and financial situations. Whether you’re looking for a short-term loan to minimize interest or a longer term to keep monthly payments lower, SECU typically provides options. Their personalized service means you’re more likely to speak with a loan officer who understands your individual needs and can guide you through the process, rather than a generic call center. This commitment to community and member well-being makes SECU a strong contender for your car financing needs, complementing the insights gained from their Car Loan Calculator Secu.

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with the best tools, it’s easy to fall into common traps that can skew your financial planning. Being aware of these pitfalls can save you from making costly mistakes.

- Not Considering All Costs: As discussed, the calculator primarily focuses on the loan itself. Common mistakes to avoid are assuming the displayed monthly payment is your only expense. Always factor in taxes, registration, insurance, and ongoing maintenance.

- Using an Unrealistic Interest Rate: Don’t just pick the lowest rate you see advertised. Your actual rate will depend on your credit score and other factors. Use an estimated rate that is realistic for your financial profile, or better yet, get pre-approved to know your exact rate.

- Focusing Only on Monthly Payments: While a low monthly payment is appealing, a longer loan term to achieve that payment means you’ll pay significantly more in total interest. Always look at both the monthly payment and the total cost of the loan.

- Ignoring the Impact of a Down Payment: Skipping a down payment or making a very small one can dramatically increase your loan amount and the interest you pay. The calculator allows you to see the power of a good down payment.

- Failing to Check Your Credit Score: Your credit score is the single biggest determinant of your interest rate. Not knowing it means you’re guessing at the most crucial input for the calculator.

By avoiding these common missteps, you ensure that your use of the SECU Car Loan Calculator leads to truly accurate and valuable financial insights.

Pro Tips for Optimizing Your Car Loan

Beyond merely using the calculator, there are strategic moves you can make to optimize your car loan and save money over the long term.

- Get Pre-Approved: This is perhaps the most powerful tip. Knowing your borrowing power and interest rate before you shop gives you significant leverage at the dealership. It allows you to negotiate the car’s price as a cash buyer, separating the vehicle transaction from the financing.

- Negotiate the Car Price First, Then the Financing: Dealerships often try to bundle everything. Focus on getting the best possible price for the vehicle itself, and only then discuss financing options. If the dealership can’t beat your pre-approved SECU rate, you’re ready to go with your credit union.

- Consider Refinancing If Rates Drop: If interest rates decrease significantly after you’ve secured your loan, or if your credit score improves, explore refinancing your car loan. This could lead to a lower interest rate and substantial savings over the remaining term.

- Round Up Your Payments: If your monthly payment is, say, $385, consider paying $400. That extra $15 goes directly towards your principal, helping you pay off the loan faster and reduce the total interest paid without significantly impacting your budget.

These pro tips, combined with effective use of the Car Loan Calculator Secu, will put you in an advantageous position, allowing you to not only find the right car but also the right financing.

Conclusion: Drive Confidently with Informed Decisions

The journey to purchasing a new vehicle is exciting, and with the right tools and knowledge, it can also be a financially smart and stress-free experience. The SECU Car Loan Calculator stands as a beacon of clarity in the often-murky waters of auto financing. It empowers you to visualize your future payments, understand the true cost of borrowing, and make decisions that align with your financial goals.

By mastering the inputs, understanding the underlying financial principles, and implementing smart planning strategies, you transform from a hopeful car buyer into a financially savvy consumer. You gain the confidence to negotiate, the peace of mind that comes with a well-planned budget, and the satisfaction of knowing you’ve made an informed decision.

So, as you embark on your next car-buying adventure, remember to leverage the power of the SECU Car Loan Calculator. Plan wisely, drive confidently, and enjoy the open road ahead, knowing your finances are in excellent order.