Drive Smarter: Unlocking the Best Car Loans with Credit Unions Near You

Drive Smarter: Unlocking the Best Car Loans with Credit Unions Near You Carloan.Guidemechanic.com

Buying a car is one of the most significant financial decisions many of us make. Beyond choosing the right make and model, securing the right financing can save you thousands of dollars over the life of the loan. While traditional banks and dealership financing are common options, there’s a powerful alternative often overlooked: credit unions.

Based on my extensive experience in personal finance and auto lending, credit unions consistently offer some of the most competitive rates and borrower-friendly terms available. They are member-owned, non-profit financial institutions, which means their primary goal isn’t maximizing shareholder profit but rather serving their members. This fundamental difference often translates into better deals for you, the borrower.

Drive Smarter: Unlocking the Best Car Loans with Credit Unions Near You

This comprehensive guide will dive deep into why credit unions are often the best choice for car loans, how to find the top ones "near you," and critical steps to ensure you secure the best possible terms. If you’re looking to finance your next vehicle intelligently, keep reading – your wallet will thank you.

Why Credit Unions Are a Game-Changer for Car Loans

When it comes to securing an auto loan, many consumers default to the first offer they receive, often from a dealership or a major bank. However, smart borrowers know that exploring all options is key. Credit unions stand out for several compelling reasons that directly benefit car loan applicants.

1. Lower Interest Rates: Your Path to Significant Savings

One of the most attractive benefits of credit unions is their propensity to offer lower interest rates on car loans compared to traditional banks. This isn’t just a minor difference; it can lead to substantial savings over the loan’s term. Because credit unions are non-profit organizations, any surplus earnings are typically returned to members in the form of lower loan rates, higher savings rates, and reduced fees.

Pro tips from us: Even a half-percent difference in APR can translate to hundreds, if not thousands, of dollars saved over a five-year loan. Always compare the Annual Percentage Rate (APR) from multiple sources, not just the monthly payment. This will give you the true cost of borrowing.

2. Personalized Service and Member-Centric Approach

Unlike large corporate banks, credit unions often pride themselves on providing highly personalized service. They understand that each member’s financial situation is unique. This means you’re less likely to be treated as just another number and more likely to receive tailored advice and support throughout the loan application process.

Based on my experience, this personalized touch can be invaluable, especially if you have a less-than-perfect credit history or unique financial circumstances. Loan officers at credit unions are often more willing to work with you to find a solution that fits your budget and needs, rather than adhering to rigid, one-size-fits-all policies.

3. Flexible Loan Terms and Understanding Your Needs

Credit unions are often more flexible with their loan terms and conditions. While banks might have stricter requirements for loan duration or down payment percentages, credit unions sometimes offer more adaptable options. This flexibility can be crucial for aligning your loan with your monthly budget and long-term financial goals.

For instance, they might be more accommodating with slightly longer terms to lower monthly payments, or they might offer more lenient policies for refinancing existing loans. This adaptability stems from their focus on member welfare rather than strict profit margins.

4. Community Focus and Local Investment

Credit unions are deeply rooted in their communities. Their members often live and work in the same areas, fostering a sense of shared ownership and mutual support. This local focus means that your membership and loan payments contribute directly to the economic well-being of your community.

Many credit unions also offer financial literacy programs and community outreach initiatives, further demonstrating their commitment beyond just providing banking services. This can be a significant draw for those who prefer to keep their money within local economies.

How to Find the Best Credit Union for Your Car Loan "Near Me"

The "near me" aspect is critical when searching for a credit union. Unlike national banks, credit unions typically have specific membership eligibility requirements, often tied to where you live, work, or your affiliation with certain groups. Here’s how to pinpoint the best options.

1. Start with Targeted Local Search Strategies

The internet is your best friend here. Begin with simple, yet effective, Google searches. Try phrases like:

- "Best credit unions for car loans "

- "Auto loan rates credit union near me"

- "Credit unions with low car loan rates in "

- "Local credit union car loan reviews"

These searches will typically bring up credit unions operating in your geographical area. Pay attention to the top results and those with strong local reviews.

2. Understand and Meet Membership Eligibility Requirements

This is arguably the most crucial step in joining a credit union. Eligibility rules vary widely but commonly include:

- Geographical location: Living or working in a specific county or region.

- Employer affiliation: Working for a particular company or industry.

- Association/Organization membership: Being part of a specific group, church, or union.

- Family ties: Having a family member who is already a member.

- "Easy to Join" options: Some credit unions allow anyone to join by making a small donation to a specific charity or organization (e.g., the American Consumer Council).

Always check the "Join Us" or "Membership" section of a credit union’s website to understand their specific requirements before applying for a loan. Don’t be discouraged if one doesn’t fit; there are often many options available.

3. Compare Car Loan Rates, Terms, and Fees

Once you’ve identified a few credit unions you’re eligible to join, it’s time to compare their offerings. Don’t just look at the advertised "starting from" rates. Dig deeper into:

- APR (Annual Percentage Rate): This is the true cost of borrowing, including interest and any fees.

- Loan Terms: How long is the loan for (e.g., 36, 48, 60, 72 months)? Shorter terms mean higher monthly payments but less interest paid overall.

- Fees: Are there application fees, origination fees, or prepayment penalties? Most credit unions have fewer fees than banks.

- Special Offers: Do they have any current promotions for new members or specific vehicle types?

Common mistakes to avoid are: only looking at the lowest monthly payment. A low monthly payment often means a longer loan term, which can result in paying significantly more interest over time. Always consider the total cost of the loan.

4. Check Reputation and Read Member Reviews

Before committing, take some time to research the credit union’s reputation. Look for reviews on Google, Yelp, and other financial review sites. Pay attention to comments regarding:

- Customer service: How responsive and helpful are their staff?

- Application process: Is it smooth and efficient, or bogged down by bureaucracy?

- Transparency: Are their terms and fees clearly communicated?

- Problem resolution: How do they handle issues or complaints?

A credit union with consistently positive reviews indicates a reliable and member-focused institution. Conversely, repeated complaints about hidden fees or poor service are major red flags.

The Car Loan Application Process at a Credit Union: What to Expect

Applying for a car loan at a credit union is similar to applying at a bank, but with a few key differences reflecting their member-centric approach. Understanding the process can help you prepare and secure the best deal.

1. Get Pre-Approved: Your Negotiating Powerhouse

Based on my experience, getting pre-approved for a car loan before you step onto a dealership lot is one of the smartest moves you can make. Pre-approval from a credit union means they’ve reviewed your financial situation and provisionally agreed to lend you a specific amount at a certain interest rate. This acts as a maximum budget and gives you immense negotiating power.

When you have a pre-approval in hand, you become a cash buyer in the eyes of the dealership. This allows you to negotiate the car’s price separately from the financing, often leading to a better deal on both fronts. If the dealership can beat your credit union’s rate, great! If not, you have a solid backup.

2. Gather Your Essential Documents

Regardless of whether you’re seeking pre-approval or a full application, you’ll need several key documents. Having these ready will streamline the process:

- Proof of Identity: Driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN, and purchase price.

Some credit unions might also ask for bank statements or other financial records, especially for larger loan amounts or if your income is irregular.

3. Understand Your Credit Score and Its Impact

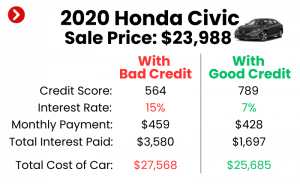

Your credit score is a numerical representation of your creditworthiness and significantly influences the interest rate you’ll be offered. Generally, higher scores (e.g., 700+) qualify for the best rates, while lower scores (e.g., below 600) may result in higher rates or require a co-signer.

It’s wise to check your credit score and report before applying. You can get free copies of your credit report from AnnualCreditReport.com. If you spot errors, dispute them immediately. For more detailed information on improving your credit score, you might want to check out .

4. The Role of Debt-to-Income Ratio (DTI)

Lenders, including credit unions, look at your Debt-to-Income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower.

While specific thresholds vary, most lenders prefer a DTI below 43%. If your DTI is high, consider paying down other debts before applying for a car loan, or explore options with a co-signer.

5. Consider Your Down Payment

While not always mandatory, a down payment significantly strengthens your loan application. It reduces the amount you need to borrow, lowers your monthly payments, and shows the lender you’re committed to the purchase. A typical down payment is 10-20% of the car’s purchase price.

Pro tips from us: A larger down payment can help you avoid being "upside down" on your loan (owing more than the car is worth), especially with new cars that depreciate quickly.

Pro Tips for Securing the Best Car Loan from a Credit Union

Getting a car loan isn’t just about finding the lowest rate; it’s about smart financial planning and strategic execution. Here are some expert tips to ensure you get the best possible deal.

1. Improve Your Credit Score Before Applying

As mentioned, your credit score is paramount. Before you even start looking for a car, take steps to improve it. This could involve paying down existing debts, making all payments on time, and avoiding opening new credit accounts. Even a small increase in your score can translate to a significantly lower interest rate.

2. Don’t Just Settle – Shop Around!

Even within the realm of credit unions, rates and terms can vary. Don’t just apply to one; aim to get pre-approvals from at least 2-3 different credit unions. This allows you to directly compare offers and leverage them against each other, potentially leading to an even better deal.

3. Negotiate (Yes, Even with Credit Unions)

While credit unions are known for fair dealings, it doesn’t hurt to ask if there’s any flexibility, especially if you have a strong credit profile or another offer in hand. You might be surprised to find they can slightly adjust rates or waive certain fees to keep your business.

4. Consider Shorter Loan Terms

While longer loan terms (e.g., 72 or 84 months) offer lower monthly payments, they dramatically increase the total interest you’ll pay over the life of the loan. If your budget allows, opt for the shortest term possible. You’ll pay off your car faster and save a substantial amount in interest.

For example, a $25,000 loan at 5% APR over 60 months costs $2,960 in interest, but over 72 months, it costs $3,676. That’s over $700 more just for extending the term by a year.

5. Read the Fine Print – Every Single Word

This cannot be stressed enough. Before signing any loan agreement, meticulously read all the terms and conditions. Understand the APR, repayment schedule, any penalties for late payments, and whether there are any prepayment penalties (rare with credit unions but still worth checking).

Common mistakes to avoid are: rushing through the paperwork at the dealership or not understanding key terms. If anything is unclear, ask questions until you fully comprehend every aspect of the agreement.

Beyond the Loan: Additional Credit Union Benefits

Choosing a credit union for your car loan often opens the door to a host of other valuable financial services, solidifying your relationship with a community-focused institution.

1. Financial Counseling and Education

Many credit unions offer free or low-cost financial counseling to their members. This can be incredibly helpful for budgeting, debt management, and future financial planning. They have a vested interest in your financial well-being, as it reflects positively on their community-focused mission.

2. Comprehensive Banking Services

Once you’re a member, you’ll typically have access to all the credit union’s other services, including checking and savings accounts, credit cards, mortgages, and personal loans. Consolidating your financial services with one institution can simplify your financial life and sometimes lead to even better rates on other products.

This holistic approach means they can often provide a more integrated financial solution tailored to your long-term goals.

Conclusion: Drive Off with Confidence and Savings

Finding the best credit unions for car loans near you is more than just a search for a good rate; it’s about making a smart financial choice that aligns with your values. By choosing a credit union, you’re not just getting a loan; you’re becoming part of a community that prioritizes its members’ financial health.

From lower interest rates and personalized service to flexible terms and a genuine commitment to local economies, credit unions offer a compelling alternative to traditional lending institutions. Take the time to research, compare, and prepare, and you’ll be well on your way to securing a car loan that truly benefits you.

Start your search today, compare offers, and drive smarter into your next vehicle purchase. For more insights into making informed financial decisions, visit trusted external resources like the National Credit Union Administration (NCUA) at www.ncua.gov. Happy driving!