Drive Towards Freedom: How Long To Pay Off Your Car Loan With Extra Payments (And Why You Should)

Drive Towards Freedom: How Long To Pay Off Your Car Loan With Extra Payments (And Why You Should) Carloan.Guidemechanic.com

Imagine a life with one less monthly bill, one less financial obligation weighing you down. For many, that dream includes paying off their car loan. The thought of owning your vehicle outright, free and clear, is incredibly appealing. But how long does it really take to achieve this, especially if you start making extra payments?

As an expert blogger and professional SEO content writer who has navigated numerous financial landscapes, I can tell you that strategically applying extra payments to your car loan isn’t just about speed; it’s about smart financial planning. This comprehensive guide will not only show you how to drastically reduce the time it takes to pay off your car, but also reveal the hidden savings and long-term benefits you might be overlooking. Get ready to accelerate your journey to financial freedom!

Drive Towards Freedom: How Long To Pay Off Your Car Loan With Extra Payments (And Why You Should)

The Silent Killer: Understanding Your Car Loan’s Anatomy

Before we dive into the power of extra payments, it’s crucial to understand the fundamental components of your car loan. Many people focus solely on the monthly payment, but there’s a lot more under the hood. Grasping these basics is the first step towards taking control.

What Makes Up Your Car Loan?

- Principal: This is the actual amount of money you borrowed to buy the car. Every extra dollar you pay towards the principal directly reduces your outstanding debt.

- Interest Rate (APR): The annual percentage rate is the cost of borrowing money, expressed as a percentage. A higher APR means you pay more for the privilege of borrowing.

- Loan Term: This is the duration, usually in months (e.g., 60 months, 72 months), over which you’ve agreed to repay the loan. A longer term often means lower monthly payments but significantly more interest paid over the life of the loan.

Most car loans use an amortization schedule. Early in your loan term, a larger portion of your monthly payment goes towards interest, and a smaller part reduces your principal. As you get closer to the end, this ratio flips. This structure is why extra payments made early on have such a profound impact.

The Unstoppable Force: How Extra Payments Supercharge Your Payoff

Making extra payments on your car loan is like giving your financial future a turbo boost. It’s one of the most effective strategies for saving money and achieving debt freedom sooner than planned. The magic lies in how these additional funds are applied.

When you make an extra payment, especially if you specify it should go towards the principal, you’re directly reducing the amount of money the lender uses to calculate your daily interest. Less principal means less interest accrues each day, which in turn means more of your next regular payment will go towards the principal, creating a powerful compounding effect in reverse.

Pro tips from us: Always confirm with your lender that any additional funds are applied directly to the principal balance, not just held as a credit for future payments. A quick call or a note on your payment can ensure your extra efforts are maximized. This seemingly small detail can make a huge difference in your total savings and payoff time.

Calculating the Impact: Seeing the Savings in Action

So, exactly how much time and money can you save? The impact of extra payments can be surprisingly significant, transforming a years-long commitment into a much shorter one. Let’s look at a hypothetical scenario to illustrate this.

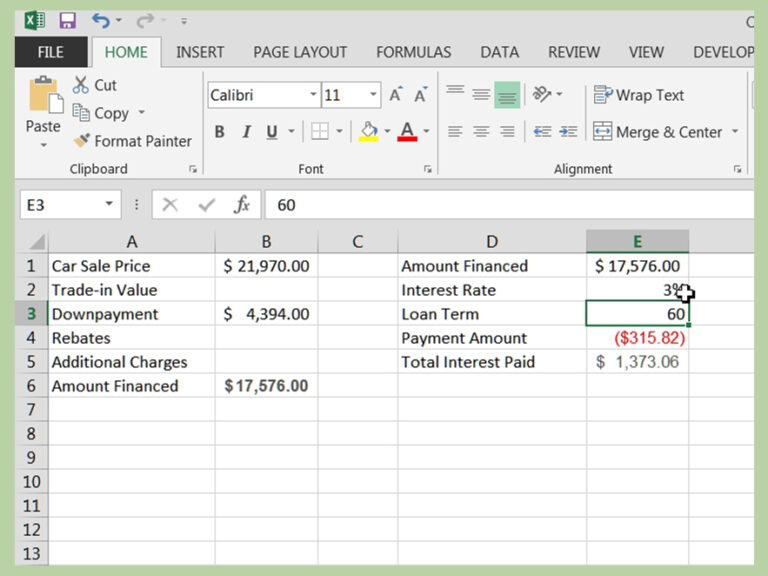

Imagine you have a $25,000 car loan at 6% APR for 60 months.

- Your standard monthly payment would be approximately $483.32.

- Over 60 months, you would pay a total of $4,999.20 in interest.

Now, let’s introduce an extra payment strategy:

Scenario 1: Adding a Small Amount Monthly

If you simply added an extra $50 to your payment each month (making it $533.32), your loan would be paid off in approximately 52 months instead of 60. You’d save around 8 months of payments and roughly $700 in interest. That’s nearly a month’s worth of savings just by adding a manageable amount!

Scenario 2: One Extra Payment Annually

If you made one extra full payment of $483.32 each year, perhaps using a bonus or tax refund, your 60-month loan could be paid off in about 53 months. This strategy would save you approximately 7 months and over $600 in interest. The beauty here is that it feels less like a continuous squeeze and more like a periodic opportunity.

These examples clearly demonstrate that even small, consistent efforts can yield substantial results. The key is consistency and understanding how your extra money is being utilized. Many online car loan payoff calculators can help you visualize these savings with your specific loan details.

Top Strategies to Accelerate Your Car Loan Payoff

There isn’t a one-size-fits-all approach to paying off your car loan early. The best method depends on your financial situation, income patterns, and discipline. Here are several proven strategies you can employ.

1. The Power of Consistent Increments

This is perhaps the simplest and most sustainable method for many people. Instead of trying to find a large lump sum, you commit to adding a small, manageable amount to your regular monthly payment.

- Round Up: If your payment is $483, round it up to $500. That extra $17 goes directly to principal.

- Fixed Extra Amount: Commit to adding a specific amount, say $25, $50, or even $100, to your payment every month.

- Automate It: Set up an automatic transfer with your bank or loan servicer. This ensures consistency and removes the temptation to spend that extra money elsewhere.

Based on my experience, consistency is key here. Even seemingly small amounts accumulate rapidly over time, significantly reducing both your payoff period and the total interest paid. This method integrates seamlessly into most budgets without causing undue strain.

2. Embrace Bi-Weekly Payments

This strategy is incredibly popular for its subtle yet powerful impact. Instead of making one full payment monthly, you divide your monthly payment by two and pay that amount every two weeks.

- The "13th Payment" Effect: Because there are 52 weeks in a year, you end up making 26 half-payments, which equates to 13 full monthly payments annually instead of 12.

- Faster Principal Reduction: By paying every two weeks, you’re sending money to your lender more frequently, reducing your principal balance sooner. This means less interest accrues between payments.

Many lenders offer a bi-weekly payment option, sometimes for a small fee. Ensure you understand any associated costs. If your lender doesn’t, you can often achieve a similar effect by manually splitting your payment and sending it every two weeks, or simply making one extra payment per year as a lump sum.

3. Strategic Lump Sum Payments

Do you receive periodic windfalls like tax refunds, work bonuses, or inheritance? These can be powerful tools for accelerating your car loan payoff. Applying a one-time lump sum directly to your principal can shave off months, even years, from your loan term.

- Tax Refunds: Instead of spending your refund, consider dedicating a portion or all of it to your car loan.

- Work Bonuses/Commissions: If you receive performance-based pay, earmark a percentage for debt reduction.

- Unexpected Income: Selling old items, a cash gift – any unexpected money can be put to good use here.

Common mistakes to avoid are: Using these windfalls for discretionary spending when you have a clear opportunity to save significant interest on your car loan. While treating yourself is fine, prioritizing debt reduction can have a much larger positive impact on your long-term financial health.

4. The Debt Snowball or Avalanche (as applied to car loans)

While these methods are typically used for overall debt management, they can be adapted for your car loan if it’s part of a larger debt picture.

- Debt Snowball: You pay off your smallest debt first, then roll that payment into the next smallest, and so on. If your car loan is your smallest debt, this method can build momentum and motivation.

- Debt Avalanche: You prioritize paying off the debt with the highest interest rate first. If your car loan has a higher APR than other debts (e.g., student loans, some credit cards), this is the most mathematically efficient method for saving money.

Choosing between these two depends on whether you prioritize psychological wins (snowball) or maximum interest savings (avalanche). Both can be incredibly effective when applied consistently.

Beyond the Savings: The Hidden Benefits of Early Payoff

While saving hundreds or even thousands of dollars in interest is a huge motivator, the advantages of paying off your car loan early extend far beyond just the financial ledger. There are profound psychological and practical benefits as well.

- Increased Cash Flow: Once the car payment is gone, that money is freed up. You can then redirect it towards other financial goals, such as saving for a down payment on a house, investing for retirement, or building a more robust emergency fund. This enhanced cash flow significantly boosts your financial flexibility.

- Improved Debt-to-Income Ratio (DTI): Having fewer outstanding debts improves your DTI, which is a key metric lenders use when evaluating you for mortgages or other loans. A lower DTI makes you a more attractive borrower, potentially leading to better interest rates on future credit.

- Peace of Mind & Reduced Stress: There’s an undeniable sense of relief that comes with eliminating a major monthly expense. That weight lifted can translate into reduced financial stress and a greater sense of security.

- Full Ownership & Equity: You own your car outright. This means you have full equity in the vehicle. If you decide to sell it, the entire sale price (minus any selling costs) goes directly into your pocket.

- Opportunity for Future Savings: The money you were paying towards your car loan can now be invested, helping you grow your wealth over time. This is a powerful long-term benefit often overlooked. For more in-depth budgeting tips, check out our guide on .

Important Considerations and Potential Downsides

While paying off your car loan early is generally a wise financial move, it’s not always the absolute best first step for everyone. There are a few critical factors to consider before diving in headfirst.

- Prepayment Penalties: While rare with standard car loans, some lenders or specific loan agreements might include a prepayment penalty. This is a fee charged if you pay off your loan early. Always check your loan documents or contact your lender to confirm if such a clause exists. If it does, calculate whether the penalty outweighs the interest savings.

- Opportunity Cost: Is there a better use for your extra money?

- High-Interest Debt: If you have credit card debt with an APR of 18-25% or more, prioritizing that debt will almost always save you more money than paying off a car loan with a 5-7% APR. The mathematical advantage of tackling the highest interest first is undeniable.

- Emergency Fund: This is paramount. Before dedicating extra funds to your car loan, ensure you have a fully funded emergency savings account, typically 3-6 months of living expenses. Life throws curveballs, and having cash reserves prevents you from going into new debt when unexpected expenses arise.

- Investments with Higher Returns: If you have access to investment opportunities that consistently yield returns significantly higher than your car loan’s interest rate, it might be more financially advantageous to invest rather than prepay. However, this comes with higher risk.

As a financial expert, I’ve seen firsthand how neglecting an emergency fund can unravel even the best-laid plans. Secure your safety net first.

Common Mistakes to Avoid When Paying Off Your Car Loan Early

Enthusiasm is great, but avoiding common pitfalls ensures your efforts are truly productive.

- Not Confirming Principal Application: This is perhaps the biggest mistake. As mentioned earlier, if your extra payment is simply held as a credit for future payments, you’re not saving on interest. Always verify with your lender that additional funds are applied directly to the principal balance.

- Neglecting Your Emergency Fund: Rushing to pay off debt without a financial cushion is like building a house without a foundation. One unexpected expense can derail your progress and force you into more debt.

- Ignoring Higher-Interest Debt: If your car loan has a relatively low interest rate compared to other debts you carry (like credit cards), focusing on the car loan first might be mathematically inefficient. Tackle the highest interest debt first to maximize your savings.

- Making Sacrifices That Aren’t Sustainable: Don’t cut your budget so drastically that you feel deprived or stressed. Sustainable progress is better than a sprint that leaves you exhausted and prone to giving up. Find a balance that works for your lifestyle.

- Forgetting to Review Loan Documents: Always know the terms of your loan, including any potential prepayment penalties, before making major changes to your payment strategy.

Expert Tips for Maximizing Your Payoff Journey

Here are some tried-and-true strategies to make your early car loan payoff journey as smooth and effective as possible.

- Automate Everything: Set up automatic payments for both your standard monthly amount and any extra principal payments you commit to. This removes the need for manual action and ensures consistency.

- Track Your Progress: Use a spreadsheet, an online tracking tool, or even a simple notebook to monitor your decreasing principal balance and the interest you’re saving. Seeing your progress can be a huge motivator.

- Revisit Your Budget Regularly: Periodically review your income and expenses. As your financial situation changes, you might find opportunities to increase your extra payments. For example, a raise or a reduction in another expense could free up more cash.

- Stay Focused on the Goal: Remind yourself why you want to pay off your car loan early. Is it for financial freedom? To save for a house? To reduce stress? Keeping your "why" front and center will help you stay disciplined.

- Consider Refinancing (Carefully): If your credit score has improved since you first took out the loan, or if interest rates have dropped significantly, refinancing to a lower APR could reduce your overall interest cost, making your extra payments even more impactful. If you’re considering refinancing, read our comprehensive article: . However, be wary of extending your loan term just for a lower monthly payment, as this often leads to paying more interest in the long run.

Conclusion: Your Road to Car Loan Freedom Starts Now

Paying off your car loan early is a powerful financial move that offers significant benefits, from saving thousands in interest to enjoying the peace of mind that comes with debt freedom. By understanding your loan, implementing smart payment strategies, and avoiding common pitfalls, you can dramatically reduce how long it takes to pay off your car loan with extra payments.

Whether you choose to make small, consistent extra payments, adopt a bi-weekly schedule, or leverage lump sums, every dollar you apply to your principal brings you closer to owning your vehicle outright. Don’t underestimate the compounding effect of these actions. Start by assessing your current loan, reviewing your budget, and choosing a strategy that fits your financial life. Your journey to car loan freedom isn’t just a dream; it’s an achievable goal waiting for you to take the driver’s seat. What extra payment will you make this month? The sooner you start, the sooner you’ll wave goodbye to that car payment forever.