Drive Towards Freedom: Your Ultimate Guide to Paying Off Your Car Loan Faster

Drive Towards Freedom: Your Ultimate Guide to Paying Off Your Car Loan Faster Carloan.Guidemechanic.com

The open road awaits, but often, the weight of a car loan can feel like a heavy anchor. For many, a vehicle represents freedom, convenience, and necessity. Yet, the monthly payments can tie up a significant portion of your budget for years. Imagine a future where that monthly car payment is gone, freeing up hundreds of dollars to save, invest, or simply enjoy. This isn’t just a pipe dream; it’s an achievable reality.

This comprehensive guide is designed to empower you with the knowledge and actionable strategies to accelerate your car loan payoff. We’ll dive deep into why paying off your car loan early is a smart financial move, unpack the various methods to achieve it, and highlight common pitfalls to avoid. Our goal is to provide you with a roadmap to financial freedom, one payment at a time. Let’s embark on this journey together towards eliminating that car debt and reclaiming your financial power.

Drive Towards Freedom: Your Ultimate Guide to Paying Off Your Car Loan Faster

Why Pay Off Your Car Loan Early? The Compelling Benefits

Deciding to actively pursue an early car loan payoff isn’t just about crossing an item off your to-do list; it’s a strategic financial decision with a multitude of tangible benefits. Understanding these advantages can provide the motivation you need to stay committed to your goal. The impact extends far beyond just one loan, influencing your overall financial health.

Save a Significant Amount on Interest

One of the most immediate and impactful benefits of paying off your car loan early is the substantial amount of money you save on interest. Car loans, like most installment loans, accrue interest over their lifetime. The longer you take to pay off the principal, the more interest you’ll ultimately pay.

By accelerating your payments, you reduce the principal balance more quickly. This means less money is subject to interest charges over time, directly translating into hundreds, or even thousands, of dollars saved. Based on my experience, many individuals are surprised to see just how much extra they end up paying in interest when they only make the minimum payments for the entire loan term.

Achieve Financial Freedom and Peace of Mind Faster

The feeling of being debt-free is incredibly liberating. When you eliminate a car loan, you shed a significant financial obligation, which can dramatically improve your financial flexibility. This newfound freedom means less stress and more peace of mind, knowing that a major monthly expense is no longer looming.

Think about the mental energy you currently spend worrying about bills. Removing one of the largest debts can free up that energy, allowing you to focus on other financial goals or simply enjoy life more. This psychological boost is invaluable and often underestimated until experienced firsthand.

Reduce Your Monthly Expenses and Boost Cash Flow

Once your car loan is fully paid off, that chunk of money you were dedicating to monthly payments is suddenly available. This directly increases your disposable income, giving your monthly budget a much-needed boost. Imagine having an extra $300, $400, or even $500 every month!

This improved cash flow can be redirected towards other financial priorities. You could use it to build an emergency fund, save for a down payment on a house, invest for retirement, or tackle other high-interest debts. It opens up a world of possibilities for strengthening your financial position.

Improve Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a crucial metric that lenders use to assess your ability to manage monthly payments and repay debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI ratio indicates a healthier financial standing.

By paying off your car loan, you reduce your total monthly debt payments, which in turn lowers your DTI ratio. This can make you a more attractive candidate for future loans, such as a mortgage, potentially allowing you to qualify for better interest rates and terms. It’s a strategic move for your long-term financial reputation.

Understanding Your Car Loan: The Foundation for Early Payoff

Before you can effectively devise a strategy to pay off your car loan faster, it’s crucial to understand the intricacies of your existing loan agreement. Many borrowers sign on the dotted line without fully grasping the terms, which can hinder their early payoff efforts. Knowledge is power, especially when it comes to debt.

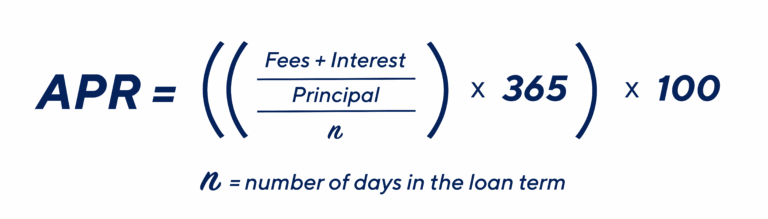

Deconstructing Your Loan Terms: APR, Principal, Interest, and Loan Term

Every car loan is built upon a few fundamental components. The Annual Percentage Rate (APR) is the yearly cost of borrowing money, including interest and other fees. A higher APR means you pay more for the privilege of borrowing. The principal is the actual amount of money you borrowed to purchase the car.

Interest is the cost of borrowing the principal, calculated based on your APR and the remaining principal balance. The loan term is the duration over which you’ve agreed to repay the loan, typically ranging from 36 to 84 months. Understanding how these elements interact is key to figuring out how to reduce the overall cost of your loan.

The Amortization Schedule: Where Your Money Goes

An amortization schedule provides a detailed breakdown of each payment you’ll make over the life of your loan. It shows how much of each payment goes towards interest and how much goes towards the principal. In the early stages of a car loan, a larger portion of your monthly payment is allocated to interest, with a smaller amount chipping away at the principal.

As you progress through the loan term, this ratio gradually shifts, with more going towards principal. By making extra payments, you effectively skip ahead on this schedule, directly attacking the principal balance. This is why early extra payments have such a powerful impact on reducing total interest paid.

Crucial Check: Prepayment Penalties

Before you enthusiastically start making extra payments, you absolutely must check your loan agreement for any prepayment penalties. Some lenders include clauses that charge a fee if you pay off your loan before the scheduled term. While less common with car loans than with some other types of loans, they do exist.

Based on my experience, overlooking this detail is a common mistake that can negate some of your savings. Carefully review your loan documents or contact your lender directly to confirm whether any such penalties apply. If there are penalties, calculate if the interest savings still outweigh the penalty fee. In most cases, even with a small penalty, paying off early is still beneficial, but it’s important to be aware.

Proven Strategies to Accelerate Your Car Loan Payoff

Now that you understand the "why" and the "what" of your car loan, let’s explore the actionable "how." There are several powerful strategies you can employ to significantly speed up your car loan payoff. The best approach often involves combining a few of these methods to create a personalized attack plan.

Making Strategic Extra Payments

This is perhaps the most straightforward and effective strategy. Any amount you pay over your minimum monthly payment, when directed properly, goes directly towards reducing your principal balance. Even small, consistent extra payments can make a huge difference over time.

Round Up Your Payments

A simple trick is to round up your monthly payment. If your payment is $342, consider paying $350 or even $375. This seemingly small extra amount, consistently applied each month, adds up significantly over the loan term. It’s an easy way to make an impact without feeling a drastic pinch in your budget.

Implement Bi-Weekly Payments

Instead of making one full payment per month, divide your monthly payment by two and pay that amount every two weeks. Since there are 52 weeks in a year, you’ll end up making 26 half-payments, which equates to 13 full monthly payments per year instead of 12.

This strategy effectively sneaks in an extra full payment each year, directly reducing your principal and cutting down on the overall loan term. Pro tips from us: ensure your lender allows bi-weekly payments and that the extra payment is applied correctly to the principal.

Make One Extra Payment Per Year

If bi-weekly payments feel too complicated, commit to making just one extra full monthly payment each year. You could achieve this by saving a little extra each month or by using a bonus or tax refund. This single extra payment can shave months off your loan term and save you hundreds in interest. It’s a powerful, yet simple, strategy for accelerating your payoff.

Applying Windfalls Directly to Your Principal

Financial windfalls are unexpected boosts to your income, and they present an excellent opportunity to make a significant dent in your car loan. Instead of spending this extra money on discretionary purchases, direct it towards your debt.

Think about tax refunds, work bonuses, inheritances, or even gifts. When these funds come in, resist the urge to splurge. Instead, send the entire amount directly to your car loan’s principal. This lump sum payment can dramatically reduce your outstanding balance, immediately cutting down on future interest accrual. I’ve seen countless individuals transform their finances by strategically using these unexpected funds to pay down debt.

Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan. This strategy is particularly effective if you can secure a lower interest rate or a shorter loan term than your current agreement.

Secure a Lower Interest Rate

If your credit score has improved since you first took out your car loan, or if interest rates have dropped, you might qualify for a significantly lower APR. Refinancing to a lower rate means a larger portion of your monthly payment will go towards the principal, saving you money and accelerating your payoff. Always compare offers from multiple lenders to ensure you’re getting the best possible rate. Learn more about refinancing in our detailed guide on .

Opt for a Shorter Loan Term

Even if your interest rate stays the same, refinancing to a shorter loan term will force you to make larger monthly payments, which directly speeds up your payoff. While this increases your monthly outflow, it drastically reduces the total interest paid over the life of the loan. This is an excellent option if your budget can comfortably handle the increased payment.

Debt Snowball vs. Debt Avalanche: Which Path is Right for You?

If you have multiple debts, incorporating your car loan into a broader debt reduction strategy can be highly effective. The two most popular methods are the debt snowball and the debt avalanche.

The Debt Snowball Method

With the debt snowball, you list all your debts from the smallest balance to the largest, regardless of interest rate. You make minimum payments on all debts except the smallest one, which you aggressively pay down. Once the smallest debt is paid off, you take the money you were paying on it and add it to the payment for the next smallest debt.

This method provides psychological wins as you quickly eliminate smaller debts, building momentum and motivation. For those who need encouragement to stay on track, the debt snowball can be incredibly powerful for paying off car loans and other debts.

The Debt Avalanche Method

The debt avalanche method prioritizes debts by interest rate, from highest to lowest. You make minimum payments on all debts except the one with the highest interest rate, which you attack aggressively. Once that’s paid off, you move to the debt with the next highest interest rate.

This method saves you the most money on interest overall because you’re tackling the most expensive debts first. If your car loan has a high interest rate compared to your other debts, the debt avalanche can be the mathematically optimal choice for paying off car loans and maximizing your savings.

Cutting Expenses and Increasing Income

Sometimes, the simplest solution is to free up more money in your budget. This can involve two main approaches: reducing your spending or increasing your earnings.

Budgeting and Expense Reduction

Take a hard look at your monthly budget. Identify areas where you can cut back, even temporarily. This might mean eating out less, canceling unused subscriptions, or finding cheaper alternatives for everyday purchases. Every dollar saved can be redirected towards your car loan, accelerating your payoff journey. Pro tips from us: use a budgeting app or spreadsheet to track every penny and identify spending leaks.

Boosting Your Income

Consider ways to bring in extra cash. This could involve taking on a side hustle, selling unused items, or asking for a raise at work. Even a few hundred extra dollars a month from a part-time gig or selling crafts can make a significant impact when consistently applied to your car loan principal. The more money you can free up, the faster you’ll reach your debt-free goal.

Common Mistakes to Avoid When Paying Off Your Car Loan

While the goal of paying off your car loan early is noble, certain missteps can hinder your progress or even cost you more in the long run. Being aware of these common pitfalls can help you navigate your journey smoothly and effectively.

Not Checking for Prepayment Penalties

As mentioned earlier, failing to verify if your loan agreement includes prepayment penalties is a significant oversight. Some lenders impose fees for paying off a loan ahead of schedule. Always confirm this detail before making substantial extra payments. If a penalty exists, factor it into your calculations to ensure that the interest savings still outweigh the penalty cost.

Ignoring Your Budget and Overextending Yourself

Getting enthusiastic about paying off debt is great, but it shouldn’t come at the expense of your overall financial stability. Aggressively paying down your car loan without a solid budget can lead to financial strain, making it difficult to cover other essential expenses or build savings. Common mistakes to avoid are neglecting your emergency fund or going into more debt (like credit card debt) just to pay off your car loan. Your budget is your financial compass; stick to it.

Refinancing for a Longer Term (Even with Lower Interest)

While refinancing can be a powerful tool, be wary of extending your loan term, even if you secure a lower interest rate. A longer loan term, even at a reduced APR, often means you’ll pay more in total interest over the life of the loan. The goal is to reduce your total cost and duration, not just your monthly payment. Always crunch the numbers to compare the total cost of the old loan versus the new, refinanced loan.

Neglecting Other High-Interest Debt

Focusing solely on your car loan, especially if you have other debts with significantly higher interest rates (like credit card debt or personal loans), might not be the most financially optimal strategy. The debt avalanche method, which prioritizes high-interest debts, is designed to save you the most money overall. Before dedicating all extra funds to your car loan, assess all your debts and their respective interest rates.

Not Confirming Extra Payments Go to Principal

This is a critical point. When you make an extra payment, explicitly state to your lender that the additional funds should be applied directly to the principal balance. If you don’t specify, some lenders might automatically apply the extra money to your next scheduled payment, which means it merely pre-pays your regular installment and doesn’t reduce the interest-accruing principal as effectively. Always double-check your payment statements to ensure your extra funds are being allocated correctly.

The Psychological Boost of Being Debt-Free

Beyond the tangible financial benefits, paying off your car loan early delivers a profound psychological advantage. The absence of debt has a ripple effect that touches every aspect of your financial and personal life. It’s a feeling that truly needs to be experienced to be fully appreciated.

Stress Reduction and Improved Well-being

Debt is a significant source of stress for millions. The constant pressure of monthly payments, the fear of unexpected expenses, and the general burden of owing money can take a toll on mental and emotional well-being. Eliminating your car loan removes a major source of this stress, leading to a noticeable improvement in your overall peace of mind.

This reduction in financial anxiety can free up mental space, allowing you to focus on other areas of your life with greater clarity and less worry. It’s a cornerstone of achieving true financial freedom.

Increased Financial Flexibility and Options

With one less major monthly payment, your financial flexibility skyrockets. That money is now yours to command. You have more options for how you allocate your income, whether it’s saving for a down payment on a home, funding a child’s education, or investing for retirement.

This flexibility empowers you to make proactive financial decisions rather than being constantly reactive to debt obligations. It creates a buffer against unexpected life events and allows you to pursue larger financial goals with greater ease.

Ability to Save and Invest More Aggressively

Once your car loan is paid off, the funds previously earmarked for that payment can be strategically redirected into savings and investments. This dramatically accelerates your progress towards other financial milestones. You can build up your emergency fund more quickly, contribute more to your retirement accounts, or even start a new investment portfolio.

The compounding effect of these redirected funds over time can be astonishing. It’s not just about paying off debt; it’s about shifting your financial trajectory towards long-term wealth creation. Once you’ve conquered your car loan, consider exploring our guide on .

What to Do After Your Car Loan is Paid Off

Congratulations! You’ve successfully navigated the journey of paying off your car loan. This is a significant accomplishment and a moment worth celebrating. But the journey doesn’t end here. This newfound financial freedom opens up exciting new possibilities for your money.

Celebrate Your Achievement!

First and foremost, take a moment to acknowledge your hard work and discipline. This is a big win! You’ve successfully tackled a major debt and reached an important financial milestone. Acknowledge your efforts with a small, budget-friendly celebration. It reinforces positive financial habits and provides a sense of accomplishment.

Redirect Your Old Car Payment Towards New Goals

This is where your financial discipline truly pays off. The money you were previously sending to your car lender each month is now available. Treat this "phantom payment" as if it still exists, but redirect it strategically towards your next financial goal.

Perhaps you want to aggressively pay off another debt, build up a robust emergency fund, or supercharge your retirement savings. Whatever your next priority, commit to sending that exact car payment amount to your new goal every month.

Build a Robust Emergency Fund

If you don’t already have one, or if yours is insufficient, now is the perfect time to build or bolster your emergency fund. Aim for at least three to six months’ worth of essential living expenses saved in an easily accessible, high-yield savings account. This fund acts as a financial safety net, protecting you from unexpected job loss, medical emergencies, or major home repairs without going back into debt.

Tackle Other Debts (Especially High-Interest Ones)

With your car loan gone, you can now focus your attention on other outstanding debts. Prioritize those with the highest interest rates, such as credit card balances or personal loans, using either the debt snowball or debt avalanche method. The momentum you built paying off your car loan can be incredibly powerful in eliminating other financial obligations.

Save for Your Next Car (Cash Purchase?)

Looking ahead, consider saving up to pay for your next vehicle in cash. Imagine never having another car payment again! By setting aside your old car payment amount into a dedicated "new car fund," you can accumulate enough to make a cash purchase, saving you thousands in future interest. This is the ultimate financial power move for vehicle ownership.

Real-World Scenario: Sarah’s Journey to Car Loan Freedom

I’ve seen countless individuals transform their finances by diligently applying these strategies. Consider Sarah, a client who had a $20,000 car loan at 6% interest over 60 months, resulting in a monthly payment of approximately $387. She felt constrained by this payment.

After discussing her options, Sarah decided to implement a few key strategies. First, she committed to rounding up her payment to $400 each month, adding an extra $13. She also dedicated half of her $1,500 tax refund each year ($750) directly to her principal.

These seemingly small actions had a huge impact. The extra $13/month and $750/year allowed her to pay off her loan in just 48 months instead of 60. This saved her over $700 in interest and freed up her monthly budget a full year earlier than planned. Sarah then redirected her $387 "phantom payment" into her emergency fund, which she built up to a healthy six months’ expenses within another year. Her story is a testament to the power of consistent, strategic effort.

Conclusion: Your Path to Car Loan Freedom Starts Today

Paying off your car loan early is more than just a financial goal; it’s a strategic move towards greater financial freedom, reduced stress, and an improved overall financial outlook. By understanding your loan, implementing proven strategies like extra payments and refinancing, and avoiding common pitfalls, you can significantly accelerate your journey to being debt-free.

The benefits are clear: substantial interest savings, enhanced cash flow, and the invaluable peace of mind that comes with owning your vehicle outright. Don’t let your car loan dictate your financial future. Take control today by applying these insights and making a conscious effort to eliminate this debt. Start small, stay consistent, and celebrate each step along the way. Your future self, free from car payments, will thank you.

Remember, every extra dollar you put towards your principal is a dollar saved from future interest. It’s a powerful investment in your own financial well-being. Begin your journey towards car loan freedom today, and unlock a brighter financial future.

External Resource: For more in-depth financial planning and budgeting tools, you can explore resources provided by trusted organizations like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.