Drive with Confidence: Your Ultimate Guide to Insurance That Can Pay Off Your Car Loan

Drive with Confidence: Your Ultimate Guide to Insurance That Can Pay Off Your Car Loan Carloan.Guidemechanic.com

Imagine the unthinkable: a sudden job loss, a disabling accident, or even the total loss of your beloved vehicle. While these scenarios are unsettling to consider, they carry a particularly heavy weight when you have an outstanding car loan. The financial burden can quickly become overwhelming, turning a stressful situation into a full-blown crisis.

But what if there was a safety net? What if certain types of insurance could step in to help cover, or even completely pay off, your car loan when life throws an unexpected curveball? As an expert blogger and professional SEO content writer, I’ve delved deep into the world of automotive finance and insurance. My mission today is to demystify the various insurance options available that can provide crucial protection for your car loan, ensuring you drive with genuine peace of mind.

Drive with Confidence: Your Ultimate Guide to Insurance That Can Pay Off Your Car Loan

This comprehensive guide will explore the different forms of "insurance to pay off car loan," distinguishing between direct loan protection products and broader insurance policies that can indirectly safeguard your financial commitment. We’ll break down how each works, highlight their pros and cons, and offer practical advice based on years of experience navigating these complex financial landscapes.

The Unseen Risks: Why Car Loan Protection Matters More Than You Think

A car loan represents a significant financial commitment, often stretching over several years. While we diligently make our monthly payments, few of us truly consider the potential disruptions that could derail our ability to repay. Life is unpredictable, and unforeseen circumstances can quickly turn a manageable debt into an insurmountable one.

Based on my experience, many drivers focus solely on the vehicle itself, neglecting the financial vulnerability associated with its purchase. They might secure excellent interest rates and find the perfect car, but they overlook the crucial aspect of protecting their loan in case of a personal catastrophe or an incident involving the vehicle itself. This oversight can lead to severe financial strain, credit score damage, and even vehicle repossession.

Protecting your car loan isn’t about anticipating disaster; it’s about strategic financial planning. It’s about building resilience into your budget so that when the unexpected happens, you have mechanisms in place to mitigate the damage. This proactive approach ensures your asset remains secure and your financial health remains intact.

Demystifying "Insurance to Pay Off Car Loan": Direct and Indirect Solutions

When people talk about "insurance to pay off car loan," they’re often referring to a range of products, some specifically designed for this purpose, and others that offer indirect but powerful protection. It’s vital to understand the distinctions to make informed choices.

Let’s explore the key players in this protective ecosystem, expanding on each to give you a crystal-clear understanding.

1. Guaranteed Asset Protection (GAP) Insurance

What it is: GAP insurance is arguably the most direct form of insurance designed to help with your car loan, specifically in the event of a total loss. When your car is stolen or totaled in an accident, your standard auto insurance policy typically pays out the vehicle’s actual cash value (ACV) at the time of the loss. However, if your outstanding loan balance is more than the car’s ACV, you’re left with a "gap" – you still owe money on a car you no longer have. GAP insurance covers this difference.

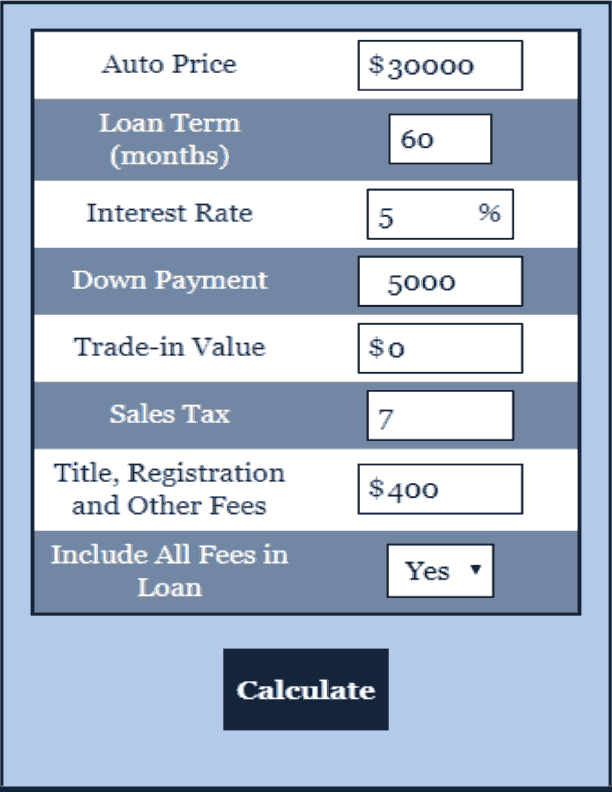

How it works: Imagine you bought a new car for $30,000, and after a year, its ACV is $22,000 due to depreciation. If your loan balance is still $25,000, your standard insurance will pay $22,000, leaving you responsible for the remaining $3,000. This is where GAP insurance steps in. It pays that $3,000 directly to your lender, effectively settling your loan.

When it’s crucial: GAP insurance is particularly valuable in several common scenarios. If you made a small down payment (or no down payment), financed for a long term (60 months or more), leased your vehicle, or bought a car that depreciates quickly, you are more likely to be "upside down" on your loan. Being upside down means you owe more than the car is worth, making GAP insurance an essential safeguard.

Pros and Cons: The primary pro is peace of mind, knowing you won’t be stuck paying for a car you no longer own. It prevents significant out-of-pocket expenses during an already stressful time. On the downside, it’s an additional cost, and it only applies to total loss situations, not personal financial hardship. Pro tips from us: Always consider GAP insurance if you’re taking out a long-term loan or have minimal equity in your vehicle.

2. Credit Life Insurance

What it is: Credit life insurance is a type of policy offered by lenders, designed to pay off your outstanding car loan balance if you, the borrower, pass away before the loan is fully repaid. The lender is typically the beneficiary of this policy.

How it works: If you have credit life insurance and you die, the insurance company will pay the remaining balance of your car loan directly to the lender. This ensures that your loved ones are not burdened with the debt of your car loan during an already difficult time. It’s a specific product tied to a specific debt.

Pros and Cons: The main advantage is that it protects your family from inheriting your car loan debt. It can provide a sense of security for co-signers or beneficiaries. However, credit life insurance can often be more expensive than a comparable personal life insurance policy. It also only covers a single debt and usually decreases in value as your loan balance shrinks, without offering any cash value or investment component. Common mistakes to avoid are assuming this is the most cost-effective way to protect your family from debt; a personal term life insurance policy often offers broader coverage for less.

3. Credit Disability Insurance

What it is: Similar in concept to credit life insurance, credit disability insurance is designed to make your car loan payments if you become temporarily or permanently disabled and are unable to work. It’s another lender-offered product.

How it works: Should you suffer a qualifying disability that prevents you from earning an income, this insurance will typically cover your monthly car loan payments for a specified period or up to a maximum amount, often after a waiting period (e.g., 30 days). This helps prevent defaults and protects your credit score during a period of financial vulnerability.

Pros and Cons: The benefit of credit disability insurance is that it provides a safety net for your car payments when your income is disrupted due by disability. It protects your credit and prevents repossession. The drawbacks are similar to credit life: it can be expensive, often has limitations on payment duration or amount, and only covers a single loan. From an expert’s perspective, while convenient, a robust personal long-term disability insurance policy typically offers much broader income protection that can cover all your expenses, not just one loan.

4. Comprehensive & Collision Insurance (Standard Auto Insurance)

How it indirectly helps: While not directly designed to "pay off" a loan in the way GAP or credit life insurance does, comprehensive and collision coverage are absolutely critical for anyone with a car loan. In fact, lenders almost always require these coverages.

- Collision coverage pays for damages to your vehicle resulting from a collision with another car or object, regardless of fault.

- Comprehensive coverage pays for damages to your vehicle from non-collision events, such as theft, vandalism, fire, natural disasters, or hitting an animal.

If your car is severely damaged in an accident or stolen, and it’s deemed a total loss, your comprehensive or collision policy will pay out the vehicle’s actual cash value (ACV) to you and your lender. This payout, combined with GAP insurance if applicable, is what ultimately helps settle your loan. Without these foundational coverages, you’d be solely responsible for the remaining loan balance on a damaged or missing vehicle. For more insights on general auto insurance, you might find our article on Understanding Your Auto Insurance Policy helpful. (Internal Link 1 Placeholder)

5. Personal Life Insurance

How it indirectly helps: Unlike credit life insurance, which is tied to a specific loan, a personal life insurance policy (term or whole life) offers a broader, more flexible form of financial protection. Upon your death, the death benefit is paid directly to your chosen beneficiaries.

How it works: Your beneficiaries can then use this lump sum payout for any purpose, including paying off your car loan, mortgage, credit card debts, or covering ongoing living expenses. This flexibility is a key advantage. It means your family has the resources to manage their finances as they see fit, rather than having a specific debt paid off without addressing other potential needs.

Pros and Cons: Personal life insurance is generally more versatile and often more cost-effective per dollar of coverage than credit life insurance. It covers all your financial obligations, not just one loan. The main "con" is that it requires more proactive planning and decision-making on the part of your beneficiaries to allocate the funds to the car loan. However, from an expert’s perspective, a robust personal life insurance policy is almost always a superior choice for comprehensive family protection.

6. Personal Disability Insurance

How it indirectly helps: Similar to personal life insurance, a personal disability insurance policy offers much broader protection than credit disability insurance. Instead of just covering your car loan payment, it replaces a significant portion of your income if you become disabled and can’t work.

How it works: If you have a personal short-term or long-term disability policy and you become disabled, the policy will pay you a percentage of your regular income. This replacement income can then be used to cover all your expenses, including your car loan payments, mortgage, utilities, and daily living costs. This comprehensive approach ensures your entire financial life is protected, not just a single debt.

Pros and Cons: The primary advantage is comprehensive income replacement, offering far greater security than a credit disability policy. It protects your entire financial well-being, not just one debt. The downside is that it requires careful selection of coverage amounts, waiting periods, and benefit periods. Pro tips from us: Always prioritize obtaining sufficient personal disability coverage, as the ability to earn an income is often your greatest asset.

Factors to Consider When Choosing Car Loan Protection

Navigating these various insurance options requires careful thought. Here are critical factors based on my experience that you should consider before making any decisions:

- Your Loan Details: What is your loan amount? How long is the term? Do you have a high interest rate? A longer loan term or a low down payment significantly increases your risk of being upside down, making GAP insurance more valuable.

- Your Financial Situation: Do you have a robust emergency fund? What other debts do you carry? Your overall financial health dictates how much risk you can comfortably absorb.

- Your Health and Dependents: If you have dependents relying on your income, life and disability insurance become non-negotiable. Your current health status might also influence the availability and cost of personal life/disability policies.

- Cost vs. Benefit: Every insurance product comes with a premium. Compare the cost of the coverage against the potential financial burden it alleviates. Sometimes, a slightly higher premium for broader personal coverage is a better investment than cheaper, highly specific credit-based insurance.

- Existing Policies: Review any life or disability insurance policies you already hold. You might already have sufficient coverage that indirectly protects your car loan, making additional credit-specific insurance redundant or unnecessary.

- Vehicle Depreciation: Some cars depreciate faster than others. If you’re buying a car known for rapid value loss, GAP insurance becomes even more important.

Where to Get These Insurance Products

The source of your insurance can significantly impact its cost and terms.

- Dealerships: Dealerships often offer GAP, credit life, and credit disability insurance as part of the financing process. While convenient, these options can sometimes be marked up significantly. Common mistakes to avoid are buying these products without comparison shopping, as they might be rolled into your loan, increasing your interest payments over time.

- Banks & Credit Unions: Your lending institution may also offer credit-specific insurance products. Their pricing can sometimes be more competitive than dealerships.

- Independent Insurance Agents: For GAP insurance, and especially for personal life and disability insurance, an independent agent can be invaluable. They can shop multiple carriers to find the best rates and coverage tailored to your specific needs.

- Online Providers: Many reputable online platforms offer quotes and policies for personal life and disability insurance, allowing for easy comparison.

Common Mistakes to Avoid When Protecting Your Car Loan

Based on countless consultations and observations, a frequent oversight is failing to critically evaluate insurance offerings. Here are common pitfalls:

- Assuming You’re Fully Covered: Many drivers believe their standard auto insurance is enough. It’s not. It won’t cover the "gap" in a total loss, nor will it make payments if you’re disabled or pass away.

- Not Reading the Fine Print: Insurance policies are contracts. Understand what triggers a payout, what exclusions exist, and any waiting periods or maximum benefit limits.

- Bundling Without Understanding: Dealerships or lenders might bundle credit insurance products. Always ask for an itemized breakdown and understand each component before agreeing.

- Ignoring Personal Life/Disability Insurance: Over-reliance on credit-specific insurance can be a costly mistake. Personal policies often provide broader, more flexible, and more affordable protection for all your financial obligations.

- Forgetting to Re-evaluate: Your financial situation changes. As your loan balance decreases, or if you get a new job, your insurance needs might evolve. Don’t set it and forget it.

Pro Tips for Smart Car Loan Protection

To ensure you make the best decisions for your financial well-being, consider these expert recommendations:

- Shop Around, Always: Never take the first offer for any insurance product. Get quotes from multiple sources for GAP, credit life, and especially personal life and disability insurance.

- Understand Your Specific Needs: Are you highly leveraged on your car loan? Do you have dependents? Is your job physically demanding? Tailor your insurance choices to your unique circumstances.

- Prioritize Broader Protection: Pro tips from us: always prioritize comprehensive personal life and disability insurance. These policies provide a safety net for all your financial obligations, not just one specific loan, offering greater peace of mind and flexibility.

- Review Policies Regularly: Annually review your auto insurance, life insurance, and disability policies. Ensure they still meet your needs and that you’re getting the best rates.

- Consider a Holistic Financial Plan: Protecting your car loan is just one piece of the puzzle. Integrate your insurance decisions into a broader financial strategy that includes an emergency fund, savings, and debt management. For further reading on managing your finances, check out Financial Planning for Major Purchases. (Internal Link 2 Placeholder)

Driving Towards Financial Security

Protecting your car loan isn’t about fear; it’s about empowerment. It’s about making informed choices that safeguard your financial future against the unexpected. While no one wants to imagine their car being totaled or facing a personal crisis, being prepared is the hallmark of responsible financial management.

By understanding the distinct roles of GAP insurance, credit life, credit disability, and especially the broader protection offered by personal life and disability policies, you can build a robust safety net around your automotive investment. Don’t leave your car loan vulnerable to life’s uncertainties. Take the time to assess your needs, compare your options, and secure the right "insurance to pay off car loan" for you.

Remember, true financial freedom comes from making smart, proactive decisions today that protect your assets and your peace of mind tomorrow. For more information on responsible lending and consumer protection, you can visit the Consumer Financial Protection Bureau’s website at www.consumerfinance.gov. (External Link)