Drive Your Dream: A Deep Dive into Sandy Spring Bank Car Loan Rates

Drive Your Dream: A Deep Dive into Sandy Spring Bank Car Loan Rates Carloan.Guidemechanic.com

The open road, the scent of a new car interior, the thrill of a vehicle that perfectly fits your lifestyle – for many, owning a car is more than just transportation; it’s a symbol of freedom and possibility. But before you hit the accelerator on your dream ride, there’s a crucial pit stop to make: understanding your financing options. For residents in the Mid-Atlantic region, Sandy Spring Bank car loan rates often come into the conversation as a reliable, community-focused option.

Navigating the world of auto loans can feel complex, with terms like APR, credit scores, and loan terms swirling around. As an expert blogger specializing in financial content, I’ve seen firsthand how important it is to demystify these concepts. This comprehensive guide is designed to be your ultimate resource, offering an in-depth look at what Sandy Spring Bank offers, how their rates are determined, and how you can secure the best possible financing for your next vehicle. Our ultimate goal is to empower you with the knowledge to make an informed decision, ensuring your car ownership journey starts on the right financial foot.

Drive Your Dream: A Deep Dive into Sandy Spring Bank Car Loan Rates

Understanding Car Loan Rates: The Essential Basics

Before we delve into the specifics of Sandy Spring Bank, it’s vital to grasp the fundamental principles that govern car loan rates across the board. These rates are not arbitrary; they are carefully calculated based on a variety of factors that reflect the risk involved for the lender. A clear understanding of these elements will help you approach any loan application with greater confidence.

At its core, a car loan rate is the cost you pay to borrow money. This cost is typically expressed as an Annual Percentage Rate (APR), which includes not only the interest rate but also any additional fees associated with the loan. This distinction is crucial, as the APR gives you a more accurate picture of the total cost of borrowing. A lower APR means less money paid over the life of the loan.

Several key variables influence the rate you’ll be offered. Your personal financial health, the specifics of the vehicle you wish to purchase, and even broader economic conditions all play a significant role. Being aware of these influences allows you to strategically position yourself for more favorable terms.

What Shapes Your Auto Loan Rate?

The interest rate you receive on a car loan is a dynamic figure, influenced by a blend of personal circumstances and market conditions. Understanding these drivers is the first step toward securing a competitive offer.

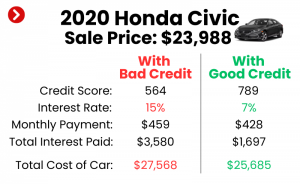

Firstly, your credit score stands as the most dominant factor. This three-digit number is a snapshot of your financial reliability, indicating to lenders how likely you are to repay your debts. A higher credit score signals lower risk, typically resulting in lower interest rates.

Secondly, the loan term, or the length of time you have to repay the loan, also impacts the rate. Shorter terms usually come with lower rates because the lender’s money is tied up for less time. Conversely, longer terms might offer lower monthly payments but often carry higher overall interest rates.

Furthermore, the size of your down payment plays a significant role. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk and can lead to more attractive rates. Finally, the type of vehicle (new vs. used) and current market interest rates also contribute to the final offer.

Sandy Spring Bank: A Local Perspective on Auto Financing

Sandy Spring Bank holds a unique position as a long-standing, community-focused institution primarily serving the Maryland, Virginia, and Washington D.C. metropolitan areas. Unlike larger national banks, a local bank like Sandy Spring often prides itself on personalized service and a deep understanding of its customer base. This can translate into a more tailored experience when seeking a car loan.

Choosing a local bank for your car financing needs can offer distinct advantages. Based on my experience, local institutions often provide a level of accessibility and relationship banking that larger, more impersonal lenders might not. You can walk into a branch, speak directly with a loan officer, and build a rapport that can be beneficial throughout the loan process. This human touch can be particularly reassuring when making a significant financial commitment like a car purchase.

Moreover, community banks are often invested in the financial well-being of their local clientele. They might be more willing to work with individuals to find solutions that fit unique situations, rather than adhering strictly to rigid, one-size-fits-all criteria. This local presence and commitment can make Sandy Spring Bank an attractive option for many seeking car financing.

Delving into Sandy Spring Bank Car Loan Rates

When considering any financial product, the first question on most people’s minds is, "What are the rates?" While I cannot provide real-time, personalized rates here – as they fluctuate based on market conditions and individual qualifications – I can guide you on how to find the most accurate information and what factors Sandy Spring Bank will likely consider.

Pro tip from us: The most reliable way to ascertain current Sandy Spring Bank car loan rates is to visit their official website directly or, better yet, contact a loan officer at one of their branches. Online rate calculators can provide estimates, but a personalized quote is always the most accurate.

Factors Specific to Sandy Spring Bank’s Offerings

Like most lenders, Sandy Spring Bank evaluates several criteria to determine your specific car loan rate. Understanding these can help you prepare and potentially improve your offer.

Credit Tiers and Your Score: Your credit score is paramount. Sandy Spring Bank, like other financial institutions, categorizes applicants into different credit tiers (e.g., excellent, good, fair, poor). Each tier has a corresponding range of interest rates. Generally, the higher your credit score, the lower the interest rate you’ll qualify for. For instance, someone with an 800+ FICO score will almost certainly receive a better rate than someone with a 650 score. It’s always wise to check your credit score before applying.

Loan Products: New, Used, and Refinancing: Sandy Spring Bank typically offers different rates for new and used car loans. New car loans often carry slightly lower rates due to the vehicle’s higher resale value and lower depreciation risk. Used car loan rates can be higher, especially for older models, as the risk of mechanical issues and rapid depreciation increases. They also provide refinancing options, allowing you to potentially lower your existing car loan interest rate.

Loan Terms and Their Impact: The length of your loan, typically ranging from 36 to 72 months, significantly affects both your monthly payment and the total interest paid. While a longer term (e.g., 72 months) might offer a lower monthly payment, you’ll generally pay more interest over the life of the loan. Conversely, a shorter term (e.g., 36 or 48 months) means higher monthly payments but less total interest paid. Sandy Spring Bank will offer various terms, and choosing the right one depends on your budget and financial goals.

Special Offers and Promotions: Keep an eye out for any special promotions or limited-time offers that Sandy Spring Bank might run. These can sometimes provide even more competitive rates or unique benefits. Checking their website or speaking with a representative is the best way to discover such opportunities.

The Sandy Spring Bank Car Loan Application Process

Applying for a car loan can feel daunting, but breaking it down into manageable steps makes the process much clearer. Sandy Spring Bank aims to make this experience as smooth as possible for its customers. Here’s a general overview of what you can expect when applying for a car loan with them.

The journey typically begins with preparation. Gathering all necessary documents beforehand can significantly expedite the process and prevent delays. This initial organization sets a strong foundation for a successful application.

Step-by-Step Guide to Applying

- Gather Your Documents: Before you even start, collect essential paperwork. This typically includes government-issued identification (driver’s license), proof of income (pay stubs, tax returns), proof of residency (utility bill), and information about the vehicle you intend to purchase (if known). Having these ready demonstrates your preparedness and helps the bank assess your eligibility quickly.

- Check Your Credit Score: Knowing your credit score upfront is a huge advantage. It gives you an idea of what rates you might qualify for and allows you to address any inaccuracies on your report. Based on my experience, a free credit report from AnnualCreditReport.com is a great starting point.

- Consider Pre-approval: This is a powerful step. Getting pre-approved for a loan means Sandy Spring Bank has conditionally agreed to lend you a certain amount at a specific rate before you even pick out a car. This transforms you into a cash buyer at the dealership, giving you stronger negotiation power on the vehicle’s price.

- Submit Your Application: You can typically apply for a Sandy Spring Bank car loan online, over the phone, or by visiting a local branch. Choose the method that’s most convenient for you. The application will ask for personal, financial, and employment details.

- Underwriting and Decision: Once your application is submitted, Sandy Spring Bank’s underwriting team will review your information, including your credit report and income verification. They will assess your risk level and determine your eligibility and the final loan terms. This process can take anywhere from a few hours to a couple of business days.

Common Mistakes to Avoid

Based on my experience, several pitfalls can hinder your car loan application or lead to less favorable terms.

One common mistake is not checking your credit score beforehand. This can lead to surprises and missed opportunities to correct errors. Another error is applying to too many lenders simultaneously, which can result in multiple hard inquiries on your credit report and temporarily lower your score.

Furthermore, not having all your documents ready can cause unnecessary delays and frustration. Finally, many applicants focus solely on the monthly payment without considering the total cost of the loan over its entire term. Always look at the APR and the total amount repayable.

Key Factors Affecting Your Sandy Spring Bank Car Loan Rate

While we’ve touched upon some general influences, let’s explore these factors in more detail, specifically how they relate to securing the best possible Sandy Spring Bank car loan rates. Understanding these nuances can give you an edge in the application process.

Each element serves as a piece of the puzzle that lenders like Sandy Spring Bank use to construct your loan offer. Optimizing these factors before you apply can directly translate into significant savings over the life of your car loan.

Your Credit Score: The Ultimate Indicator

Your FICO score, or another credit scoring model, is the primary determinant of your interest rate. Lenders view it as a report card of your financial responsibility.

- Excellent Credit (780+): You’re likely to receive the most competitive rates available, as you represent a very low risk.

- Good Credit (670-779): Still qualifies for very good rates, though perhaps not the absolute lowest.

- Fair Credit (580-669): You might face higher rates, as you represent a moderate risk.

- Poor Credit (Below 580): Securing a loan can be challenging, and rates will be significantly higher, if approved.

Sandy Spring Bank, like most lenders, will use your credit score to gauge your reliability. A strong score demonstrates a history of on-time payments and responsible debt management, making you a more attractive borrower.

Debt-to-Income (DTI) Ratio

Your DTI ratio is another critical metric. It compares your total monthly debt payments to your gross monthly income. For example, if your monthly debt payments (including the potential new car loan payment) are $1,500 and your gross monthly income is $4,500, your DTI is 33%.

Lenders use this ratio to assess your ability to take on additional debt. A lower DTI indicates you have more disposable income to cover your loan payments, making you a less risky borrower. Generally, a DTI below 36% is considered favorable.

Loan Amount and Term

The size of the loan and its repayment period directly impact the bank’s risk and, consequently, your rate.

- Loan Amount: While larger loans mean more money for the bank, they also represent a greater risk exposure. However, extremely small loans might have less favorable terms due to administrative costs.

- Loan Term: As discussed, shorter terms often mean lower rates. The longer the loan term, the more time the bank’s money is at risk, which usually translates to a higher interest rate to compensate for that extended risk.

Down Payment

Making a substantial down payment is one of the most effective ways to lower your interest rate.

A larger down payment reduces the amount you need to borrow, thus decreasing the lender’s exposure. It also shows the bank that you have significant equity in the vehicle from day one, making you less likely to default. Pro tips from us: Aim for at least 10-20% of the vehicle’s price if possible.

Vehicle Type and Age

The car itself plays a role.

- New Cars: Typically qualify for lower rates because they depreciate slower initially and are less prone to mechanical issues, making them less risky collateral.

- Used Cars: Rates are generally higher for used vehicles, especially older ones, due to faster depreciation and higher potential for mechanical problems. The bank assesses the collateral’s value and how quickly it might diminish.

Relationship with Sandy Spring Bank

If you are an existing Sandy Spring Bank customer with other accounts (checking, savings, mortgage), you might be eligible for relationship-based discounts on your car loan rate. Banks often reward loyal customers with preferential terms. It never hurts to inquire about this when you speak with a loan officer.

Comparing Sandy Spring Bank Car Loan Rates

While Sandy Spring Bank can be an excellent option, securing the best possible auto loan requires a broader perspective. Based on my experience, comparison shopping is non-negotiable. Never settle for the first offer you receive, even if it seems attractive.

The auto loan market is competitive, with numerous lenders vying for your business. By comparing multiple offers, you ensure you’re getting the most favorable terms available to you. This diligence can save you hundreds, if not thousands, of dollars over the life of your loan.

Why Comparison is Crucial

Think of it like shopping for the car itself – you wouldn’t buy the first one you see without checking out other dealerships, would you? The same logic applies to financing. Different lenders have different underwriting criteria, risk assessments, and promotional offers. What might be a good rate from one bank could be beaten by another.

Moreover, rates fluctuate based on market conditions, and a rate that was competitive last month might not be today. Active comparison ensures you’re getting the most up-to-date and favorable offer.

What to Compare Beyond Just the Rate

While the APR is a critical figure, it’s not the only element to scrutinize.

- Fees: Look for origination fees, application fees, or prepayment penalties. Some lenders charge these, while others do not. Sandy Spring Bank generally prides itself on transparency, but it’s always good to ask.

- Loan Terms: Compare the exact loan terms offered. A slightly higher rate on a shorter term might still result in less total interest paid than a lower rate on a much longer term.

- Flexibility: Does the lender offer flexible payment options? What are their policies on making extra payments?

- Customer Service: Consider the reputation for customer service. A bank that is responsive and helpful can make a big difference if issues arise.

Where Else to Look for Comparison Quotes

To get a truly comprehensive comparison, expand your search beyond just one institution.

- Other Banks: Explore other regional or national banks that operate in your area.

- Credit Unions: Often known for competitive rates, credit unions are member-owned and frequently offer excellent terms, especially if you meet their membership criteria.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, or others specializing in online auto loans can provide quick quotes and sometimes very competitive rates.

- Dealership Financing: While often convenient, dealership financing sometimes includes markups. However, they can also have special manufacturer-backed rates that are hard to beat. Always get an outside quote before considering dealership financing.

Pro tip from us: Aim to get pre-approval offers from at least 3-4 different sources, including Sandy Spring Bank, within a short window (e.g., 14-30 days). This minimizes the impact on your credit score, as multiple inquiries for the same type of loan within a limited timeframe are typically counted as a single inquiry.

Maximizing Your Chances for the Best Rates

Securing the most competitive Sandy Spring Bank car loan rates – or any car loan rates, for that matter – isn’t just about finding the right lender; it’s also about presenting yourself as the ideal borrower. There are several proactive steps you can take to significantly improve your chances of getting a low interest rate.

These strategies focus on enhancing your financial profile and making informed decisions that reduce the perceived risk for lenders. Implementing even a few of these tips can lead to substantial savings over the life of your loan.

Improve Your Credit Score

This is arguably the most impactful step. A higher credit score directly correlates with lower interest rates.

- Pay Bills On Time, Every Time: Payment history is the biggest factor in your credit score. Set up auto-payments or reminders to ensure you never miss a due date.

- Reduce Existing Debt: Lowering your credit card balances and other outstanding loans can improve your credit utilization ratio, which positively affects your score.

- Avoid New Credit Applications: Limit opening new lines of credit in the months leading up to your car loan application, as new accounts can temporarily ding your score.

- Review Your Credit Report: Regularly check your credit report for errors and dispute any inaccuracies promptly.

Save for a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and the lender’s risk. Aim for at least 10-20% of the vehicle’s purchase price. Not only does this potentially lower your interest rate, but it also reduces your monthly payments and the total interest you’ll pay over time.

Shorten Your Loan Term (If Affordable)

While longer terms offer lower monthly payments, they often come with higher interest rates. If your budget allows, opting for a shorter loan term (e.g., 36 or 48 months instead of 60 or 72) can significantly reduce the total interest paid and often qualifies you for a better rate. Carefully assess your monthly budget to ensure you can comfortably manage the higher payments.

Consider a Co-signer (If Necessary)

If your credit score is fair or poor, or your income is inconsistent, a co-signer with excellent credit can help you qualify for a loan or secure a better rate. The co-signer essentially guarantees the loan, sharing the responsibility. However, understand that this is a significant commitment for the co-signer, as their credit will also be affected if payments are missed.

Negotiate the Car Price First

Before you even discuss financing, negotiate the best possible purchase price for the car itself. Dealerships sometimes try to distract you with attractive financing offers to mask a higher vehicle price. Separate the two processes: secure your financing (ideally with pre-approval) and then negotiate the car price. This puts you in a stronger position.

Refinancing Your Car Loan with Sandy Spring Bank

Even if you already have a car loan, it might be worthwhile to explore refinancing options with Sandy Spring Bank. Refinancing essentially means taking out a new loan to pay off your old one, ideally with more favorable terms. This can be a smart financial move in several scenarios.

Common mistakes to avoid when considering refinancing include not checking your current loan’s prepayment penalties or failing to compare the new loan’s total cost against your remaining balance. Always do the math.

When to Consider Refinancing

- Lower Interest Rates: If interest rates have dropped since you originally financed your car, or if your credit score has significantly improved, you could qualify for a lower rate.

- Improve Your Credit Score: If your credit has improved, you’re a less risky borrower, making you eligible for better terms.

- Change Loan Term: You might want to extend your loan term to lower your monthly payments (though you’ll pay more interest overall) or shorten it to pay off the loan faster and save on interest.

- Remove a Co-signer: If your financial situation has stabilized, you might be able to refinance and release a co-signer from their obligation.

Benefits of Refinancing with a Local Bank like Sandy Spring Bank

Refinancing with a local institution can offer similar benefits to obtaining an original loan: personalized service, the ability to speak directly with a loan officer, and potentially a more flexible approach to underwriting. If you already have a relationship with Sandy Spring Bank, they might be more inclined to offer competitive rates to retain your business.

The Refinancing Process

The process for refinancing is quite similar to applying for an original car loan. You’ll need to gather financial documents, your vehicle’s information, and apply. Sandy Spring Bank will review your credit and income, and if approved, they will pay off your old loan, and you’ll begin making payments to them under the new terms.

Beyond the Rate: What Else to Consider

While Sandy Spring Bank car loan rates are a critical component of your decision, a truly comprehensive evaluation goes beyond just the numbers. The overall lending experience, customer support, and additional benefits can significantly impact your satisfaction throughout the loan’s duration.

As an expert blogger, I always advise looking at the bigger picture. A slightly higher rate might be worth it for exceptional service, while a rock-bottom rate could come with hidden inconveniences.

Customer Service and Accessibility

One of the primary advantages of a local bank like Sandy Spring is their emphasis on customer service and accessibility.

- Local Branch Access: Having physical branches means you can speak to a person face-to-face, which can be invaluable for questions, concerns, or complex situations.

- Personalized Experience: Local banks often foster stronger customer relationships, leading to more personalized advice and support compared to large online-only lenders.

Flexibility in Repayment

Inquire about the flexibility of their repayment options.

- Payment Due Dates: Can you adjust your payment due date to align with your paychecks?

- Extra Payments: Are there any fees or penalties for making extra payments or paying off the loan early? Reputable lenders like Sandy Spring Bank typically do not have prepayment penalties, which is a significant advantage.

Additional Products and Services

Sometimes, banks offer additional benefits or products that can add value.

- Insurance Products: They might offer payment protection plans or gap insurance. Evaluate these carefully to see if they align with your needs.

- Online Banking and Mobile App: A user-friendly online portal and mobile app for managing your loan, making payments, and checking your balance are essential for modern convenience.

Transparency

A trustworthy lender provides clear and transparent information about all loan terms, fees, and conditions. Ensure you understand every aspect of the loan agreement before signing. Sandy Spring Bank’s commitment to community often translates into clear communication.

FAQs about Sandy Spring Bank Car Loans

Here are some frequently asked questions to further clarify the car loan process with Sandy Spring Bank:

Can I get pre-approved for a car loan at Sandy Spring Bank?

Yes, Sandy Spring Bank typically offers a pre-approval process for auto loans. This allows you to know how much you can borrow and at what rate before you even visit a dealership, giving you greater negotiating power.

What credit score do I need for a Sandy Spring Bank car loan?

While Sandy Spring Bank doesn’t publish a minimum credit score, generally, a score of 670 or higher (considered "good" credit) will give you the best chance of approval and competitive rates. Applicants with lower scores may still be approved but might face higher interest rates.

How long does the approval process take for a car loan?

The approval timeline can vary. If you have all your documents ready and apply online, you might receive a decision within one business day. In-branch applications or those requiring additional documentation may take slightly longer.

Does Sandy Spring Bank finance older or high-mileage used cars?

Sandy Spring Bank, like most lenders, will have criteria regarding the age and mileage of used vehicles they finance. These details are often assessed on a case-by-case basis, but generally, newer used cars with lower mileage are more likely to be approved for favorable terms. It’s best to discuss your specific vehicle with a loan officer.

Can I apply for a car loan with a co-applicant?

Yes, if you wish to apply with a co-applicant, Sandy Spring Bank typically allows this. Applying with a co-applicant who has a strong credit history and stable income can sometimes help you qualify for a better interest rate or a larger loan amount.

Conclusion: Driving Forward with Confidence

Navigating the world of car loans can seem complex, but with the right information, you can make a decision that puts you in the driver’s seat of your financial future. We’ve explored the essential factors that influence Sandy Spring Bank car loan rates, the application process, and key considerations that extend beyond just the interest rate.

Remember, securing the best car loan involves thorough research, understanding your financial standing, and diligently comparing offers from various lenders. While Sandy Spring Bank stands out as a strong, community-focused option known for personalized service and competitive rates, it’s always prudent to compare their offerings with other financial institutions to ensure you’re getting the absolute best deal for your unique situation.

Armed with this in-depth knowledge, you’re now well-equipped to approach your car financing with confidence. Whether you’re buying a brand-new vehicle or a reliable used car, understanding your options and preparing effectively will pave the way for a smooth and affordable journey. We encourage you to visit the Sandy Spring Bank website or speak with a loan officer to get personalized quotes and start your path toward driving your dream car.

External Link: For more information on understanding your credit score, a key factor in car loan rates, you can visit the Consumer Financial Protection Bureau’s official guide: https://www.consumerfinance.gov/consumer-tools/debt-collection/credit-reporting/credit-scores-and-reports/