Drive Your Dream Car: A Deep Dive into First Community Credit Union Car Loans

Drive Your Dream Car: A Deep Dive into First Community Credit Union Car Loans Carloan.Guidemechanic.com

Buying a car is a significant life event, often marking a new chapter of independence, convenience, or family growth. For many, securing the right financing is as crucial as choosing the perfect vehicle. While numerous options exist, credit unions consistently stand out for their member-focused approach and competitive offerings. Among them, First Community Credit Union (FCCU) has carved a niche as a trusted partner for auto financing.

This comprehensive guide will unravel everything you need to know about securing a car loan with First Community Credit Union. We’ll explore their unique advantages, guide you through the application process, and share expert insights to ensure you drive away with the best possible deal. Our goal is to equip you with the knowledge to make informed decisions, transforming what can be a daunting process into a smooth and successful journey.

Drive Your Dream Car: A Deep Dive into First Community Credit Union Car Loans

Why a Credit Union Should Be Your First Stop for a Car Loan

When it comes to financing a vehicle, you have a plethora of choices: traditional banks, dealership financing, and online lenders. However, credit unions, like First Community Credit Union, often offer a distinctly superior experience. They operate on a not-for-profit model, meaning their primary goal isn’t maximizing shareholder profits, but rather serving their members’ financial well-being.

This fundamental difference translates into tangible benefits for you, the borrower. Credit unions are typically able to offer more competitive interest rates and more flexible loan terms compared to their for-profit counterparts. They reinvest their earnings back into the community and their members, which often results in better deals and personalized service.

Based on my experience assisting countless individuals with their auto financing, credit unions consistently deliver a more human-centric approach. They are often more willing to work with members who might have less-than-perfect credit, offering tailored solutions that traditional banks might overlook. This commitment to member success makes them an invaluable resource in your car buying journey.

Understanding First Community Credit Union: Your Local Financial Partner

Before diving into the specifics of their car loans, it’s essential to understand who First Community Credit Union is. FCCU is a member-owned financial cooperative dedicated to serving specific communities or groups. Their mission revolves around empowering members to achieve their financial goals through a wide array of products and services, delivered with a personal touch.

Membership eligibility for First Community Credit Union typically depends on various factors, such as where you live, work, worship, or attend school. Often, family members of existing members are also eligible. It’s crucial to check their specific membership requirements on their official website or by contacting them directly. Becoming a member is usually a straightforward process, often requiring a small deposit into a savings account.

Once you become a member, you gain access to all their financial services, including their highly-regarded auto loan programs. This membership isn’t just a formality; it signifies your ownership stake in an institution designed to prioritize your financial health.

The First Community Credit Union Car Loan Advantage: What Sets Them Apart

First Community Credit Union’s car loan offerings are designed with the member in mind, aiming to make vehicle ownership accessible and affordable. They understand that a car is often a necessity, not just a luxury, and they strive to provide solutions that fit diverse financial situations. Let’s explore the key advantages.

Competitive Interest Rates That Save You Money

One of the most compelling reasons to choose FCCU for your car loan is their commitment to offering competitive interest rates. Because they are not-for-profit, they can often pass on savings directly to their members in the form of lower Annual Percentage Rates (APRs). A lower interest rate means a lower overall cost for your loan and more money staying in your pocket over the loan’s lifetime.

Pro tips from us, seasoned financial writers: even a half-percentage point difference in your APR can translate into hundreds or even thousands of dollars saved over a typical 5-year car loan. Always compare FCCU’s rates with other lenders, and you’ll often find them at the forefront. This competitive edge is a hallmark of credit union financing.

Flexible Loan Terms Tailored to Your Budget

FCCU understands that not all financial situations are the same. They offer a variety of flexible loan terms, allowing you to choose a repayment schedule that aligns with your budget and financial goals. Whether you prefer a shorter term to pay off your loan faster or a longer term to keep monthly payments lower, they have options available.

Common loan terms range from 36 months to 84 months, depending on the vehicle and your creditworthiness. It’s important to balance the length of the term with the total interest paid. While longer terms mean lower monthly payments, they also mean you’ll pay more in interest over the life of the loan.

A Full Spectrum of Auto Loan Types

First Community Credit Union provides a comprehensive suite of auto loan products, ensuring they can meet virtually any car buying need. This versatility means you don’t have to look elsewhere, whether you’re buying new or used, or even considering refinancing.

- New Car Loans: For those seeking the latest models, FCCU offers attractive rates and terms on brand-new vehicles. They can help finance cars directly from dealerships, providing you with the peace of mind that your financing is secured before you even step onto the lot.

- Used Car Loans: Buying a pre-owned vehicle can be a smart financial move, and FCCU supports this with specific used car loan options. These loans often come with competitive rates, although the terms might vary slightly based on the vehicle’s age and mileage.

- Auto Loan Refinancing: If you already have a car loan with another lender, FCCU can help you refinance it. Refinancing can potentially lower your interest rate, reduce your monthly payments, or even shorten your loan term, saving you money in the long run. We’ll delve deeper into refinancing later in this article.

The Power of Pre-Approval: Shop with Confidence

One of the most valuable services FCCU offers is car loan pre-approval. Getting pre-approved means the credit union reviews your financial information and determines how much you can borrow and at what interest rate, before you even start shopping for a car. This crucial step transforms your car buying experience.

With a pre-approval in hand, you become a cash buyer at the dealership. This gives you significant leverage in negotiating the vehicle’s price, as you’re not reliant on the dealer’s financing options. It also helps you set a clear budget, preventing you from falling in love with a car you can’t truly afford. Based on my experience, pre-approval is the single most effective way to gain control and confidence in the car buying process.

How to Apply for a First Community Credit Union Car Loan: Your Step-by-Step Guide

Applying for a car loan can seem intimidating, but First Community Credit Union strives to make the process as smooth and transparent as possible. Here’s a detailed breakdown of the steps involved.

Step 1: Become a Member (If You Aren’t Already)

As a member-owned institution, the first prerequisite for any loan at FCCU is membership. If you’re not already a member, you’ll need to join. This typically involves:

- Checking Eligibility: Verify if you meet their membership criteria (e.g., residency, employment, family ties).

- Opening an Account: Usually, you’ll need to open a basic savings account with a small initial deposit, which makes you a co-owner of the credit union.

This initial step is quick and straightforward, often completable online or in person at a branch.

Step 2: Gather Your Essential Documents

Preparation is key to a swift loan application process. Having all your necessary documents ready beforehand will save you time and potential delays. Common documents requested include:

- Proof of Identity: Valid government-issued ID (driver’s license, state ID, passport).

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Vehicle Information (if you’ve already found a car): Purchase agreement, VIN, make, model, and year. For refinancing, you’ll need your current loan statements.

It’s wise to have digital copies readily available if applying online, and physical copies if visiting a branch.

Step 3: Complete the Application

First Community Credit Union typically offers multiple ways to apply for a car loan, providing flexibility for their members:

- Online Application: This is often the quickest and most convenient method. You can fill out the application form from the comfort of your home, uploading documents digitally.

- In-Person at a Branch: If you prefer face-to-face assistance or have questions, visiting a local FCCU branch allows you to speak with a loan officer directly. They can guide you through the process and help with any paperwork.

- Over the Phone: Some credit unions also offer phone applications, especially for pre-approvals or simple inquiries.

During the application, you’ll provide personal details, employment history, income information, and details about the loan amount you’re requesting. Be honest and thorough to avoid any issues.

Step 4: What to Expect After Applying

Once your application is submitted, FCCU’s lending team will review your information. This typically involves:

- Credit Check: They will pull your credit report to assess your creditworthiness.

- Income Verification: Confirming your stated income.

- Debt-to-Income Ratio Assessment: Evaluating your existing debt obligations against your income.

You will usually receive a decision within one to two business days, sometimes even faster for online applications. If approved, you’ll receive an offer detailing the loan amount, interest rate, and terms. You’ll then proceed to finalize the paperwork and receive your funds.

Eligibility Requirements for a FCCU Car Loan: What They Look For

Lenders, including First Community Credit Union, assess several factors to determine your eligibility for a car loan. Understanding these criteria can help you prepare and improve your chances of approval.

Credit Score Considerations

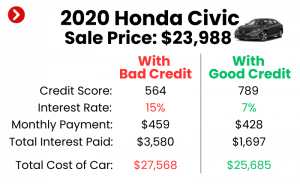

Your credit score is a crucial indicator of your financial responsibility and plays a significant role in determining your loan approval and interest rate. While FCCU is known for being more flexible than some traditional banks, a higher credit score will always lead to better terms.

- Good to Excellent Credit (700+): You’re likely to qualify for the best rates and terms.

- Fair Credit (600-699): You may still qualify, though rates might be slightly higher. FCCU might be more willing to work with you than other lenders.

- Limited or Poor Credit (<600): Approval is still possible, especially if you have a strong relationship with FCCU or can offer a larger down payment or a co-signer. They often look at your overall financial picture, not just a single number.

Based on my observations, credit unions often take a holistic view, considering your membership history and other accounts with them, which can sometimes compensate for a less-than-perfect credit score.

Debt-to-Income (DTI) Ratio

Your debt-to-income ratio is another key metric. This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to gauge your ability to take on additional debt. A lower DTI ratio indicates less financial risk.

FCCU typically looks for a DTI ratio below a certain threshold (often around 36-43%, though this can vary). If your DTI is high, it suggests you might be overextended, making it harder to manage new loan payments. You can calculate your DTI by adding up all your monthly debt payments (credit cards, existing loans, rent/mortgage) and dividing it by your gross monthly income.

Stable Income and Employment History

Lenders want to see a consistent source of income that demonstrates your ability to make regular loan payments. This means a stable employment history is highly valued. Typically, they prefer to see at least two years of consistent employment with the same employer or within the same industry.

If you’re self-employed, you’ll likely need to provide more extensive documentation, such as two years of tax returns, to prove your income stability. Any gaps in employment or frequent job changes might raise questions, but can often be explained.

Vehicle Requirements (for specific loans)

For used car loans, there might be specific requirements regarding the vehicle itself. These can include:

- Age Limit: The car might need to be no older than a certain number of years (e.g., 8-10 years old).

- Mileage Limit: A maximum mileage cap (e.g., 100,000 to 120,000 miles) might apply.

- Vehicle Value: The loan amount cannot exceed the vehicle’s appraised value (e.g., as determined by NADAguides or Kelley Blue Book).

- Title Status: The vehicle must have a clean title, free from salvage or rebuilt status.

These requirements are in place to ensure the vehicle serves as adequate collateral for the loan.

Pro Tips for Securing the Best FCCU Car Loan

Getting approved is one thing; securing the best possible terms is another. Here are some expert tips to help you maximize your chances of getting a low interest rate and favorable conditions on your First Community Credit Union car loan.

1. Improve Your Credit Score

Before you even apply, take steps to boost your credit score. Pay down existing debts, especially credit card balances, and ensure all your bills are paid on time. Dispute any errors on your credit report. A higher score directly translates to lower interest rates. Even a 20-point increase can make a difference.

2. Save for a Down Payment

Making a significant down payment reduces the amount you need to borrow, which can lower your monthly payments and the total interest paid. It also shows the lender you are financially committed, potentially leading to better loan terms. Aim for at least 10-20% of the vehicle’s purchase price if possible.

3. Know Your Budget Inside and Out

Before you start shopping for a car or a loan, determine how much you can truly afford each month, considering all your expenses. Don’t just focus on the monthly loan payment; factor in insurance, fuel, maintenance, and potential registration fees. A realistic budget prevents financial strain down the road.

4. Leverage the Power of Pre-Approval

As mentioned, getting pre-approved by First Community Credit Union is one of the most powerful tools in your arsenal. It empowers you to negotiate the car price with confidence, knowing exactly how much you can spend and what your financing terms will be. This separates the car buying negotiation from the loan negotiation, giving you an advantage.

5. Consider a Co-Signer (If Necessary)

If your credit score is on the lower side or your income is inconsistent, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. However, ensure both parties understand the responsibility; the co-signer is equally liable for the loan.

Common Mistakes to Avoid During Your Car Loan Journey

The car buying process is rife with potential pitfalls. Avoiding these common mistakes can save you money, stress, and regret.

1. Not Getting Pre-Approved

This is perhaps the biggest mistake. Without pre-approval, you walk into a dealership blind to your true borrowing power. Dealers may then try to "bundle" financing into the car purchase, potentially leading to higher rates or less favorable terms than you could get independently. Always secure your financing first.

2. Focusing Only on Monthly Payments

While a low monthly payment is appealing, it shouldn’t be your sole focus. Dealers often try to stretch out loan terms (e.g., 72 or 84 months) to make payments seem more affordable. This dramatically increases the total interest you’ll pay and can leave you "upside down" on your loan (owing more than the car is worth) for a longer period.

3. Ignoring the Total Cost of the Loan

Always look at the total amount you’ll repay over the life of the loan, including principal and interest. A seemingly small difference in APR can add up to thousands of dollars. Use an online loan calculator to compare different scenarios.

4. Skipping the Fine Print

Loan agreements can be complex, but it’s crucial to read every line before signing. Understand all terms, conditions, fees, and penalties. If anything is unclear, ask your FCCU loan officer for clarification. Don’t feel rushed into signing anything you don’t fully comprehend.

5. Forgetting About Additional Costs

Beyond the loan payment, remember to budget for car insurance, registration fees, taxes, and ongoing maintenance. These can significantly impact your overall cost of ownership. Pro tip: Get insurance quotes before you finalize your car purchase.

Refinancing Your Car Loan with First Community Credit Union

Perhaps you already have a car loan but are looking for better terms. First Community Credit Union offers excellent auto loan refinancing options that can significantly benefit your financial situation.

When Does Refinancing Make Sense?

Refinancing your car loan with FCCU is a smart move in several scenarios:

- You’ve Improved Your Credit Score: If your credit score has significantly improved since you took out your original loan, you might qualify for a much lower interest rate.

- Interest Rates Have Dropped: Market interest rates fluctuate. If current rates are lower than your original loan’s rate, refinancing could save you money.

- You Want Lower Monthly Payments: By extending your loan term (though this might mean more total interest), you can reduce your monthly outflow.

- You Want to Shorten Your Loan Term: If you’re in a better financial position, you could refinance to a shorter term, pay off the loan faster, and save on total interest.

- You Got a High Rate at the Dealership: Dealership financing sometimes comes with higher rates. Refinancing with FCCU can help correct this.

Benefits of Refinancing with FCCU

Refinancing with First Community Credit Union can lead to substantial savings and improved financial flexibility. You might:

- Reduce Your Interest Rate: The most common and impactful benefit, leading to lower overall costs.

- Lower Your Monthly Payment: Free up cash flow for other expenses or savings.

- Pay Off Your Loan Faster: If you opt for a shorter term, you’ll be debt-free sooner.

- Simplify Your Finances: Consolidate your loan with a trusted credit union partner.

The process for refinancing is very similar to applying for a new car loan, requiring an application, credit check, and verification of your current loan details. It’s a highly recommended strategy for many car owners.

Comparing FCCU Car Loans to Other Lenders: Why the Credit Union Shines

While banks and dealerships offer car loans, understanding the distinct advantages of First Community Credit Union can solidify your decision.

- Credit Unions vs. Banks: Banks are for-profit institutions with shareholders to satisfy. This often means higher interest rates and stricter lending criteria, especially for those with average credit. Credit unions, being member-owned, prioritize lower rates, fewer fees, and more personalized service.

- Credit Unions vs. Dealerships: Dealerships primarily focus on selling cars. While they offer financing, it’s often a profit center for them. They may mark up interest rates or push less favorable terms. Getting pre-approved with FCCU puts you in a stronger negotiating position, allowing you to focus on the car price, not the finance rate.

Based on my experience, dealership financing is rarely the best option available. It’s convenient, but convenience often comes at a cost. Always secure independent financing first, then see if the dealership can beat it. More often than not, they can’t match the rates offered by a dedicated credit union like FCCU.

Final Thoughts: Your Road to Affordable Auto Ownership Starts Here

Securing a car loan doesn’t have to be a stressful ordeal. By understanding your options and leveraging the benefits offered by institutions like First Community Credit Union, you can navigate the process with confidence and clarity. Their commitment to competitive rates, flexible terms, and member-focused service makes them an exceptional choice for financing your next vehicle.

From getting pre-approved to potentially refinancing an existing loan, FCCU provides the tools and support you need to make smart financial decisions. Remember to do your research, prepare your documents, and always ask questions. With First Community Credit Union as your partner, you’re well on your way to driving the car of your dreams, backed by financing that truly serves your best interests.

Ready to explore your options? Visit the First Community Credit Union website or stop by a local branch to speak with a loan officer today. For more insights into smart financial planning, explore our article on How to Build an Emergency Fund and learn about Understanding Your Credit Report. You can also find valuable resources on car buying and financial literacy from trusted external sources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.