Drive Your Dream Car: The Ultimate Guide to Capital One Pre-Approval Car Loans

Drive Your Dream Car: The Ultimate Guide to Capital One Pre-Approval Car Loans Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but the financing part can often feel like navigating a complex maze. Imagine walking into a dealership with the confidence of knowing exactly what you can afford, what your monthly payments will look like, and even having your financing already lined up. This isn’t just a dream; it’s a reality made possible through Capital One pre-approval car loans.

As an expert in auto financing and a professional who has guided countless individuals through the car buying process, I understand the value of being prepared. Capital One’s pre-approval process, particularly through their intuitive Auto Navigator tool, empowers you to take control of your car-buying journey long before you even set foot on a car lot. This comprehensive guide will demystify everything you need to know, from the initial application to driving away in your new vehicle, ensuring you’re well-equipped for a smooth and stress-free experience.

Drive Your Dream Car: The Ultimate Guide to Capital One Pre-Approval Car Loans

Understanding Capital One Pre-Approval Car Loans: Your Financial GPS

Before we dive deep, let’s clarify what a Capital One pre-approval car loan truly means. It’s more than just an estimate; it’s a conditional offer of credit from Capital One, stating how much they are willing to lend you for a car purchase, along with a personalized interest rate and potential monthly payment. This offer is based on a preliminary review of your financial profile, giving you a powerful financial tool in your pocket.

Many people confuse pre-approval with pre-qualification. While both offer a glimpse into your borrowing potential, pre-qualification is usually a soft inquiry that provides a general idea, often without specific terms. Pre-approval, on the other hand, involves a more thorough assessment, resulting in a concrete loan offer that you can take directly to a dealership. This distinction is crucial for understanding the true power of Capital One’s offering.

The Undeniable Benefits of Getting Pre-Approved

Securing a Capital One pre-approval car loan offers a multitude of advantages that streamline your entire car buying experience. It transforms you from a speculative shopper into a serious buyer, armed with crucial financial information.

Firstly, pre-approval provides immense clarity on your budget. You’ll know your maximum loan amount and estimated monthly payments, allowing you to focus on vehicles within your financial comfort zone. This prevents the common pitfall of falling in love with a car you simply cannot afford.

Secondly, it significantly boosts your negotiation power at the dealership. When you arrive with pre-approved financing, you’re essentially a cash buyer in the eyes of the salesperson. This removes the pressure to accept potentially less favorable financing options offered by the dealership, putting you in a stronger position to negotiate the car’s price.

Finally, pre-approval saves valuable time. The financing part of car buying can be lengthy and tedious. By getting pre-approved with Capital One, you condense this process, allowing you to focus on the exciting part: choosing your perfect car and getting on the road faster.

The Capital One Auto Navigator Experience: A Step-by-Step Journey

Capital One has revolutionized the pre-approval process with its user-friendly Auto Navigator tool. This online platform is designed to make obtaining a Capital One pre-approval car loan as straightforward and transparent as possible.

Based on my experience, the Auto Navigator truly simplifies what used to be a daunting task. It’s an intuitive portal that guides you through each step, making complex financial decisions feel manageable. The tool allows you to explore various car options and financing scenarios right from your computer or smartphone.

Navigating the Pre-Approval Process

Getting started with Capital One Auto Navigator involves a few simple steps, all designed to be quick and efficient. You’ll typically be asked for basic personal information, including your name, address, employment details, and income. This initial information helps Capital One assess your financial standing.

Crucially, this initial pre-approval process often involves a "soft inquiry" on your credit report. Unlike a "hard inquiry," a soft pull does not negatively impact your credit score. This means you can explore your financing options without worrying about dinging your credit simply for checking.

Once you submit your information, Capital One quickly processes it and presents you with personalized financing offers. These offers will detail your potential interest rate, the maximum loan amount, and estimated monthly payments. You can then use the Auto Navigator to adjust factors like down payment amount and loan term to see how they affect your payments, empowering you to tailor a plan that fits your budget.

From Pre-Approval to Driving Away

After receiving your Capital One pre-approval car loan offer, the Auto Navigator takes it a step further. It allows you to browse millions of vehicles from participating dealerships that accept Capital One financing. You can filter by make, model, price, and features, seeing exactly how your pre-approved loan applies to each vehicle.

This feature is incredibly powerful because it connects your financing directly to available inventory. You’re not just getting pre-approved in a vacuum; you’re seeing real cars you can buy with that specific financing. Once you find a car you like, the Auto Navigator can even help you connect with the dealership, providing them with your pre-approval details for a seamless transaction.

Key Factors Capital One Considers for Pre-Approval

To truly understand how to secure the best Capital One pre-approval car loan, it’s essential to grasp the factors Capital One evaluates. Lenders like Capital One assess your creditworthiness to determine the risk associated with lending you money.

Understanding these elements allows you to strategically improve your financial standing before applying. It’s about presenting yourself as a reliable borrower, which can lead to better terms and a higher chance of approval.

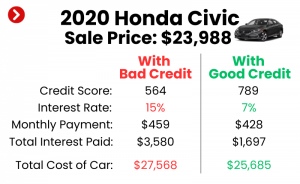

Your Credit Score: The Cornerstone of Auto Loans

Your credit score is arguably the most significant factor in securing a favorable auto loan. It’s a three-digit number that summarizes your credit history and repayment behavior. Capital One, like most lenders, uses this score to gauge your reliability.

Generally, a higher credit score indicates a lower risk, translating to better interest rates and more attractive loan terms. While there’s no official "minimum" score, borrowers with scores in the "good" (670-739) to "excellent" (740-850) ranges typically qualify for the most competitive offers. Even if your score is in the "fair" (580-669) range, Capital One pre-approval car loans can still be an option, though rates might be higher. For a deeper dive into improving your credit, check out our article on Understanding Your Credit Score and How to Boost It (simulated internal link).

Income and Employment Stability

Capital One wants to ensure you have a consistent ability to repay your loan. Your income and employment history play a crucial role in this assessment. Lenders typically look for stable employment over a period of time, demonstrating a reliable source of income.

They’ll consider your gross monthly income and may ask for proof of employment, such as pay stubs or W-2 forms. A steady job with sufficient income reassures Capital One that you can comfortably manage your monthly car payments alongside your other financial obligations.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is another vital metric. It compares your total monthly debt payments to your gross monthly income. For instance, if your monthly debt payments (including rent/mortgage, credit card minimums, student loans, etc.) are $1,500 and your gross monthly income is $4,500, your DTI is 33%.

Capital One, and most lenders, prefer a lower DTI ratio, ideally below 40%, though this can vary. A low DTI indicates that you have enough disposable income to handle new debt, like a car loan, without becoming overextended. Managing your existing debt is key here.

Payment History and Other Credit Factors

Beyond your score, Capital One reviews your payment history for all credit accounts. A consistent record of on-time payments demonstrates financial responsibility. Late payments, collections, or bankruptcies can negatively impact your chances or result in less favorable terms.

They also consider the length of your credit history, the types of credit you have (e.g., credit cards, mortgages, previous auto loans), and how much of your available credit you’re currently using (credit utilization). A diverse and well-managed credit portfolio strengthens your application.

Maximizing Your Chances for Capital One Pre-Approval

Securing the best possible Capital One pre-approval car loan isn’t just about applying; it’s about strategic preparation. By taking proactive steps, you can significantly improve your chances of approval and unlock more favorable interest rates and terms.

Pro tips from us always emphasize preparation. The more prepared you are financially, the smoother and more affordable your car buying journey will be. Think of it as fine-tuning your financial engine before hitting the road.

1. Improve Your Credit Score

If your credit score isn’t where you want it to be, take steps to improve it before applying. Pay all your bills on time, every time. Reduce your credit card balances to lower your credit utilization ratio (ideally below 30%). Avoid opening new credit accounts right before applying for a car loan, as this can temporarily lower your score.

Regularly review your credit report for errors, as even small inaccuracies can affect your score. You can get free copies of your credit report from AnnualCreditReport.com. Correcting any discrepancies can provide a quick boost to your credit standing.

2. Reduce Existing Debt

Lowering your overall debt, especially high-interest credit card debt, can dramatically improve your DTI ratio. This shows Capital One that you have more financial bandwidth to take on a new car loan. Focus on paying down smaller debts first to build momentum.

Even a slight reduction in your monthly debt obligations can make a difference in how Capital One views your application. It signals responsible financial management and a reduced risk profile.

3. Save for a Down Payment

A substantial down payment works wonders for your pre-approval chances. It reduces the amount you need to borrow, which lowers Capital One’s risk. A larger down payment also often leads to lower monthly payments and can help you secure a better interest rate.

Aim for at least 10-20% of the vehicle’s purchase price. Not only does it make you a more attractive borrower, but it also helps you build equity in your car faster and reduces the likelihood of being "upside down" on your loan (owing more than the car is worth).

4. Know Your Budget Inside and Out

Before applying, have a clear understanding of your overall budget. This includes not just the car payment, but also insurance, fuel, maintenance, and potential registration fees. Capital One’s pre-approval will give you a loan amount, but you need to ensure the total cost of car ownership fits your lifestyle.

Use online calculators to estimate these additional costs. Being realistic about your monthly expenses helps you choose a loan amount and vehicle that won’t strain your finances, leading to a more sustainable and enjoyable car ownership experience.

What Happens After Capital One Pre-Approval? Navigating the Dealership

Congratulations, you’ve secured your Capital One pre-approval car loan! This is where the real power of pre-approval comes into play. You’re now equipped to shop for your car with confidence and clarity.

However, the journey isn’t over yet. Understanding your offer and how to leverage it at the dealership is crucial for a successful purchase. Don’t let your guard down; remain informed and empowered throughout the final stages.

Understanding Your Offer

Your Capital One pre-approval offer will clearly state your approved loan amount, the Annual Percentage Rate (APR), and the loan term (e.g., 60 months, 72 months). It will also provide an estimate of your monthly payments. Review these terms carefully.

The APR is particularly important as it represents the true cost of borrowing, including interest and any fees. A lower APR means less money spent over the life of the loan. Ensure you understand the validity period of your pre-approval, as these offers typically expire after a certain number of days (often 30 days).

Visiting the Dealership with Confidence

When you arrive at a participating dealership, you’re no longer just a shopper; you’re a buyer with financing in hand. Present your Capital One pre-approval car loan offer early in the process. This immediately sets the tone and signals that you’re serious and financially prepared.

Common mistakes to avoid are allowing the dealership to run multiple credit inquiries without comparing their offer to yours. While they may try to offer their own financing, you now have a benchmark. Use your Capital One offer as a strong negotiating tool for the vehicle price, knowing your financing is already secured.

Negotiating with Pre-Approval

Your pre-approval allows you to separate the car price negotiation from the financing negotiation. Focus on getting the best possible price for the vehicle first. Since your financing is already handled, you can decline any dealership financing that isn’t more advantageous than your Capital One offer.

Remember, the dealership makes money on both the car sale and the financing. By bringing your own financing, you limit their profit on the latter, which can sometimes give you leverage to negotiate a better vehicle price. For expert strategies on getting the best deal, explore our guide on Mastering Car Dealership Negotiations: Tips and Tricks (simulated internal link).

Common Myths and Misconceptions About Pre-Approval

Despite its growing popularity, Capital One pre-approval car loans can still be surrounded by myths. Dispelling these misconceptions is vital for making informed decisions.

Myth 1: Pre-approval guarantees you’ll get any car.

Reality: While pre-approval gives you a loan amount, it doesn’t mean Capital One will finance any vehicle. The car itself must meet certain criteria, such as being from a participating dealership, falling within a certain age or mileage limit, and meeting their value assessment. Always confirm the specific vehicle you choose qualifies under your pre-approval terms.

Myth 2: The initial pre-approval is a hard credit pull.

Reality: As mentioned, the initial pre-approval with Capital One Auto Navigator typically uses a soft credit inquiry, which does not impact your credit score. A hard inquiry usually occurs only when you finalize the loan application with the dealership and Capital One, confirming the details for the actual purchase.

Myth 3: You have to use Capital One financing if you get pre-approved.

Reality: Pre-approval is an offer, not an obligation. You are free to explore other financing options, including those from the dealership, other banks, or credit unions. If another lender offers you a better deal, you’re absolutely at liberty to choose it. Capital One pre-approval simply gives you a strong starting point and a solid fallback.

Pros and Cons of Capital One Pre-Approval

Like any financial product, Capital One pre-approval car loans come with their own set of advantages and potential drawbacks. A balanced view helps you decide if it’s the right path for your car buying journey.

Pros of Capital One Pre-Approval

- Simplicity and Speed: The online Auto Navigator tool makes the process incredibly easy and fast, often providing offers in minutes.

- No Initial Credit Score Impact: The soft inquiry for pre-approval protects your credit score during the shopping phase.

- Budget Clarity: You know exactly what you can afford, preventing overspending and financial stress.

- Enhanced Negotiation Power: Arriving with pre-approved financing gives you a significant advantage at the dealership.

- Wide Network: Capital One has a large network of participating dealerships, offering a broad selection of vehicles.

- Convenience: You can shop for cars online with your personalized financing already in place, streamlining the entire process.

Cons of Capital One Pre-Approval

- Not a 100% Guarantee: While strong, pre-approval is conditional. Final approval depends on verifying information and the chosen vehicle meeting criteria.

- Limited to Participating Dealerships: You must purchase your vehicle from a dealership within Capital One’s network.

- Offer Expiration: Pre-approval offers have a validity period, typically 30 days, meaning you need to act within that timeframe.

- Terms Can Change (Slightly): While rare, the final terms at the dealership could vary slightly if your financial situation changes or if the vehicle doesn’t perfectly match the pre-approval parameters.

Beyond Capital One: Exploring Other Auto Loan Options

While Capital One pre-approval car loans offer an excellent starting point, it’s always wise to explore your options. The goal is to secure the best possible financing for your specific situation.

Banks, credit unions, and even dealership financing can all be viable alternatives. Each has its own application process, eligibility requirements, and potential rates. Shopping around for auto loans is a critical step that can save you thousands of dollars over the life of your loan. For more general guidance on auto loans, consider reviewing resources from trusted external sources like the Consumer Financial Protection Bureau (CFPB) on their auto loan guide (external link simulation).

Comparing multiple offers ensures you’re getting the most competitive interest rate and favorable terms available to you. Even a small difference in APR can result in significant savings over several years.

Frequently Asked Questions About Capital One Pre-Approval

Let’s address some common questions that arise when considering a Capital One pre-approval car loan.

Q: Can I get pre-approved with bad credit?

A: Capital One considers a range of credit scores. While a higher score will yield better rates, they do offer options for individuals with less-than-perfect credit. The Auto Navigator tool will provide you with offers tailored to your specific credit profile.

Q: How long does Capital One pre-approval last?

A: Typically, Capital One pre-approval offers are valid for 30 days. This gives you ample time to shop for a car but also encourages you to act within a reasonable timeframe.

Q: What documents do I need for final approval?

A: While pre-approval is often done with minimal information, for final approval at the dealership, you’ll generally need a valid driver’s license, proof of income (pay stubs, bank statements), proof of residency (utility bill), and potentially proof of insurance.

Q: Is the pre-approved interest rate guaranteed?

A: The interest rate provided during pre-approval is a strong offer, but it’s conditional. It’s subject to final verification of your information, the specific vehicle chosen, and the final loan terms. However, it provides a very reliable estimate.

Q: What if I don’t buy a car within the pre-approval period?

A: If your pre-approval expires, you can simply reapply. Since the initial check is a soft inquiry, reapplying shouldn’t harm your credit score.

Drive Confidently with Capital One Pre-Approval

Embarking on the journey to purchase a new or used vehicle is a significant financial decision. By leveraging the power of a Capital One pre-approval car loan, you’re not just securing financing; you’re equipping yourself with knowledge, control, and immense confidence.

From understanding your budget and boosting your negotiation power to streamlining the entire dealership experience, Capital One’s Auto Navigator tool empowers you every step of the way. Don’t let the financing process be a source of anxiety. Take control, get pre-approved, and drive away in your dream car with peace of mind. Start your stress-free car buying journey today!