Drive Your Dream Car: The Ultimate Guide to Securing a CSE Car Loan

Drive Your Dream Car: The Ultimate Guide to Securing a CSE Car Loan Carloan.Guidemechanic.com

The dream of owning a car is a universal aspiration, offering unparalleled freedom, convenience, and a touch of personal independence. For many, this dream can feel just out of reach due, to the complexities and financial hurdles of traditional car financing. However, for a specific segment of the population, a powerful and often overlooked pathway exists: the CSE Car Loan.

If you’re an employee of a cooperative society, a government servant, or a member of certain recognized organizations, a CSE Car Loan could be your golden ticket to car ownership. This comprehensive guide will demystify everything you need to know, from understanding its unique benefits to navigating the application process and securing the best possible deal. We’re here to empower you with the knowledge to drive away in your new vehicle with confidence and financial peace of mind.

Drive Your Dream Car: The Ultimate Guide to Securing a CSE Car Loan

What Exactly is a CSE Car Loan? Unveiling a Unique Financing Pathway

A CSE Car Loan, at its core, is a specialized vehicle financing option offered by Cooperative Societies or specific Employee Welfare Funds. Unlike conventional car loans provided by commercial banks or large financial institutions, these loans are tailored to serve their members or employees. This distinction is crucial, as it underpins many of the advantages and unique characteristics of this financing avenue.

These cooperative structures are built on the principle of mutual benefit and support. They primarily cater to individuals who are part of their specific ecosystem, such as government employees, public sector unit (PSU) staff, or members of registered cooperative banks and credit societies. Based on my experience, many individuals who qualify for these loans often overlook them, assuming traditional banks are their only option. This is a significant oversight, as CSE loans frequently offer more favorable terms.

The fundamental difference lies in their operational philosophy. Commercial banks are profit-driven entities, meaning their loan products are designed to maximize returns for shareholders. Cooperative societies, on the other hand, prioritize the welfare and financial upliftment of their members. This member-centric approach translates directly into more accessible and often more affordable financing solutions, making the dream of car ownership a tangible reality for thousands. Understanding this core principle is the first step towards leveraging the power of a CSE Car Loan.

Unlocking the Road Ahead: Key Benefits of Opting for a CSE Car Loan

Choosing a CSE Car Loan over a traditional bank loan can offer a multitude of compelling advantages. These benefits are specifically designed to support the financial well-being of their members, making vehicle ownership more accessible and less burdensome. Let’s delve into the specific perks that make CSE Car Loans an attractive option.

Lower Interest Rates: A Significant Financial Advantage

One of the most significant benefits of a CSE Car Loan is the often substantially lower interest rates compared to those offered by commercial banks. Cooperative societies operate with a different profit motive, focusing on member welfare rather than maximizing shareholder returns. This allows them to pass on savings in the form of reduced interest charges.

A lower interest rate directly translates into reduced overall loan costs and more manageable Equated Monthly Installments (EMIs). Over the entire loan tenure, this can amount to significant savings, freeing up your finances for other essential needs or investments. From my vantage point, even a percentage point difference in interest can save thousands over a five-year loan term.

Flexible Repayment Options: Tailored to Your Income

CSEs often provide more flexible repayment tenures and structures. They understand the varying income cycles and financial capacities of their members. This flexibility might include longer repayment periods, which can reduce your monthly EMI burden, or options for pre-payment without exorbitant penalties.

This adaptability ensures that your car loan aligns better with your personal financial situation, preventing undue stress. Pro tips from us: always inquire about the full range of repayment options and choose one that offers both affordability and the ability to repay comfortably without stretching your budget too thin.

Simplified Eligibility Criteria: A Member-Centric Approach

While traditional banks often have stringent eligibility requirements, CSEs typically offer more relaxed and member-centric criteria. Being an existing member or employee of the cooperative automatically fulfills a major part of the eligibility. This streamlines the application process and reduces the hurdles often associated with securing a loan.

Their focus is on the stability of your employment within their associated organization and your relationship as a member, rather than solely on external credit scores or extensive income proofs. This can be particularly advantageous for individuals who might have a less-than-perfect credit history but possess stable employment.

Quicker Processing and Disbursement: Get Your Car Sooner

Given the internal nature of these loans and the existing relationship with their members, the processing time for CSE Car Loans can often be significantly faster. The bureaucracy found in larger banking institutions is frequently absent, leading to a more efficient and streamlined approval process.

Once approved, the disbursement of funds can also be expedited, allowing you to finalize your car purchase much sooner. This efficiency is a huge plus, especially when you’re eager to get behind the wheel of your new vehicle without unnecessary delays.

Personalized Service and Support: A Relationship-Based Approach

Dealing with a cooperative society often means experiencing a more personalized and supportive customer service approach. As a member, you’re not just another customer; you’re part of a community. This often translates into more attentive assistance, clearer communication, and a willingness to work with you through any questions or concerns you may have during the loan process.

This relationship-based service can make the entire car loan journey far less daunting and more pleasant. They are often more understanding of individual circumstances, offering guidance that big banks might not provide.

Understanding Eligibility Criteria for a CSE Car Loan: Are You Qualified?

Before you embark on the application journey for a CSE Car Loan, it’s crucial to understand the specific eligibility requirements. While generally more relaxed than traditional banks, these criteria ensure that the cooperative society lends responsibly to its members. Meeting these prerequisites is the foundational step towards securing your car loan.

Membership Status: The Cornerstone Requirement

The most fundamental criterion for a CSE Car Loan is your existing membership or affiliation with the cooperative society or employee welfare fund offering the loan. This is non-negotiable. If you are not yet a member, you will typically need to join first, which might involve purchasing shares or meeting specific membership conditions.

Always verify your membership status and understand the process for joining if you aren’t already part of the cooperative. This initial step is paramount, as all other eligibility factors hinge on this foundational relationship.

Employment Type and Stability: A Key Indicator of Repayment Capacity

CSE Car Loans are primarily extended to individuals with stable employment within specific sectors. This usually includes government employees (state or central), employees of public sector undertakings (PSUs), or staff of recognized educational institutions or corporate entities affiliated with the cooperative. Your length of service and job stability are often critical factors.

Lenders want assurance that you have a consistent income stream to repay the loan. A minimum service period (e.g., 2-3 years) might be required, demonstrating your long-term commitment and financial reliability.

Income Requirements: Ensuring Affordability

While CSEs are member-focused, they still need to assess your ability to repay the loan. This involves evaluating your monthly income against your existing financial commitments. They will look at your Debt-to-Income (DTI) ratio, ensuring that your total monthly debt payments, including the new car loan EMI, do not exceed a certain percentage of your gross monthly income.

Each cooperative will have its own specific income thresholds. Pro tips from us: calculate your current DTI ratio before applying to get a realistic sense of what you can comfortably afford. This helps avoid applying for a loan amount that strains your finances.

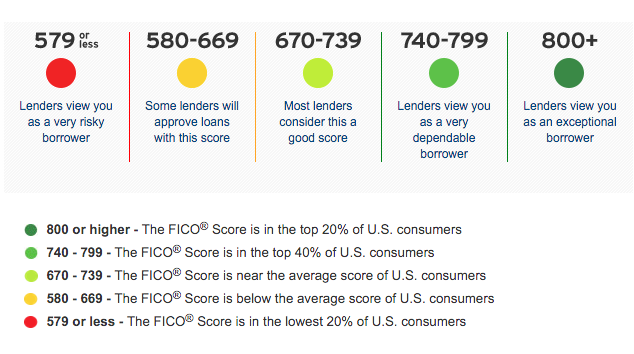

Credit Score (CIBIL/Equifax): It Still Matters, Even for CSEs

While CSEs might be more lenient than commercial banks, your credit score still plays a significant role. A good credit history demonstrates your past repayment behavior and financial discipline. A higher score (typically above 700-750) can improve your chances of approval and might even qualify you for better terms.

However, a slightly lower score might not be an outright rejection, especially if you have stable employment within the cooperative’s purview. Common mistakes to avoid are assuming your credit score doesn’t matter for a CSE loan. Always check your credit report before applying and address any discrepancies. For more details on improving your credit score, check out our guide on Mastering Your Credit Score for Loan Approvals (Internal Link 1).

Age Limits: Meeting the Demographic Criteria

Most lenders, including CSEs, impose age restrictions on loan applicants. There’s typically a minimum age (e.g., 18 or 21 years) and a maximum age (e.g., 58-60 years, or up to retirement age) by which the loan must be fully repaid. These limits are in place to ensure the applicant has sufficient earning years to complete the repayment tenure.

Required Documentation: Prepare for a Smooth Process

Gathering the correct documents is essential for a seamless application. While the exact list may vary slightly between cooperatives, common documents include:

- Proof of Identity: Aadhaar card, PAN card, Passport, Voter ID.

- Proof of Address: Utility bills (electricity, water, gas), rent agreement.

- Proof of Income: Salary slips (last 3-6 months), bank statements (last 6-12 months), Form 16/ITR.

- Proof of Employment: Employer ID card, appointment letter, service certificate.

- Membership Proof: Cooperative society membership card or statement.

- Vehicle Quotation: Proforma invoice from the car dealership.

- Photographs: Recent passport-sized photographs.

Meticulous preparation of these documents beforehand can significantly speed up your application.

The Step-by-Step Application Process for a CSE Car Loan: Your Path to Ownership

Applying for a CSE Car Loan can be a straightforward process, especially when you understand each step involved. Breaking it down helps demystify the journey and ensures you’re well-prepared at every turn. Let’s walk through the typical application process.

Step 1: Research and Preparation – Laying the Groundwork

Before you even fill out an application form, thorough research is paramount. Identify the specific cooperative societies or employee funds you are eligible for. Investigate their current car loan offerings, including interest rates, processing fees, maximum loan amounts, and repayment tenures. Don’t just settle for the first option; compare a few if possible.

During this phase, it’s also wise to determine the type of car you want and get a proforma invoice from the dealership. This provides a concrete figure for your loan application. This preparation ensures you approach the process with clear objectives and a solid understanding of your options.

Step 2: Membership Confirmation (or Enrollment) – The Gateway

As highlighted earlier, membership is key. If you are already a member, confirm your active status. If not, this is the time to understand the membership requirements and complete the enrollment process. This might involve submitting an application form, paying a membership fee, or purchasing a certain number of shares in the cooperative.

This step is critical because without valid membership, your car loan application cannot proceed. Ensure all membership formalities are completed and verified before moving forward.

Step 3: Document Gathering – Assemble Your Portfolio

This is where you collect all the necessary paperwork. Based on the eligibility criteria discussed previously, compile every required document. This includes identity proof, address proof, income statements, employment verification, and the vehicle’s proforma invoice. Make sure all documents are current, clear, and complete.

Pro tips from us: create a checklist and tick off each item as you gather it. Make photocopies of everything, and keep the originals safe. Incomplete documentation is a common mistake that can significantly delay your application.

Step 4: Application Submission – Formalizing Your Request

Once all documents are in order, obtain the official car loan application form from your chosen cooperative society. Fill it out accurately and completely. Be meticulous with details, ensuring consistency across all forms and documents. Attach all the required supporting papers, double-checking that nothing is missed.

Submit the application to the designated department within the cooperative. You might receive an acknowledgment receipt or a reference number, which is important for tracking your application’s progress.

Step 5: Verification and Assessment – The Lender’s Due Diligence

After submission, the cooperative society will begin its internal verification process. This involves cross-referencing the information provided in your application with the supporting documents. They may conduct background checks, verify your employment, and assess your credit history. They will also evaluate your Debt-to-Income ratio to ensure the loan is affordable for you.

This stage is crucial for the lender to confirm your eligibility and assess the risk associated with lending to you. Be prepared for potential calls or requests for additional information during this period.

Step 6: Loan Sanction and Offer Letter – The Green Light

If your application meets all the criteria and is approved, the cooperative society will issue a loan sanction letter or offer letter. This document will detail the approved loan amount, the interest rate, the repayment tenure, EMI amount, any specific terms and conditions, and processing fees.

Carefully review this letter. Understand every clause, especially regarding pre-payment penalties, foreclosure options, and any hidden charges. If anything is unclear, do not hesitate to ask for clarification before accepting the terms.

Step 7: Documentation and Agreement – Formalizing the Loan

Upon accepting the loan offer, you will need to sign the final loan agreement and other necessary legal documents. This typically includes a hypothecation agreement, which legally binds the vehicle to the lender until the loan is fully repaid. The original vehicle documents (like the Registration Certificate) will be endorsed with the lender’s name.

Ensure you read and understand the entire loan agreement before signing. This is a legally binding contract, and your signature confirms your acceptance of all its terms.

Step 8: Loan Disbursement and Vehicle Purchase – Driving Your Dream

Once all formalities are completed and the agreement is signed, the loan amount will be disbursed. In most cases, the funds are directly transferred to the car dealership or vendor, or sometimes to your bank account, depending on the cooperative’s policy. With the funds secured, you can then proceed to finalize the purchase of your new car.

Congratulations! You’ve successfully navigated the CSE Car Loan process and are now ready to drive your dream car.

Factors Influencing Your CSE Car Loan Approval: Maximizing Your Chances

While CSE Car Loans are often more accessible, certain factors significantly influence the likelihood of your application being approved and the terms you receive. Understanding these elements allows you to strategically position yourself for the best possible outcome.

Credit History and Score: A Reflection of Financial Responsibility

Even within a cooperative framework, your credit history and score remain pivotal. A strong credit score (e.g., 750+) signals to the lender that you are a reliable borrower with a history of timely repayments. It demonstrates financial discipline and reduces the perceived risk for the cooperative.

Conversely, a poor credit history with defaults or late payments can raise red flags. While CSEs might be more understanding, a significantly low score could still lead to rejection or less favorable terms. From my vantage point, a strong down payment always strengthens your application, especially if your credit score isn’t perfect.

Loan Amount vs. Income: The Affordability Test

Lenders meticulously assess your income to ensure the proposed EMI is affordable within your financial capabilities. They use the Debt-to-Income (DTI) ratio to determine if you can comfortably manage the new loan payment alongside your existing financial commitments. Applying for a loan amount that results in an excessively high DTI ratio (e.g., over 40-50%) is a common mistake and a primary reason for rejection.

Be realistic about what you can afford. A loan amount that aligns well with your income and current expenses will be viewed much more favorably. For a deeper dive into managing your DTI, check out our article on Understanding DTI: A Key to Financial Health (Internal Link 2).

Down Payment: Your Commitment and Reduced Risk

The size of your down payment plays a significant role. A larger down payment demonstrates your financial commitment and reduces the loan amount, thereby lowering the risk for the cooperative. It also typically results in a lower EMI and less interest paid over the life of the loan.

Lenders often see a substantial down payment as a sign of financial prudence and seriousness, making your application more appealing. Aim for at least 15-20% of the car’s value, or even more if possible.

Co-applicant or Guarantor: Strengthening Your Application

If your income or credit score alone isn’t robust enough, having a financially strong co-applicant or guarantor can significantly bolster your application. A co-applicant shares the responsibility for the loan, while a guarantor pledges to repay if you default.

This adds an extra layer of security for the lender, especially if you’re a younger employee with limited credit history or if your income barely meets the thresholds. Choose someone with a good credit score and stable income, and ensure they understand their responsibilities.

Vehicle Type and Age: Impact on Loan Terms

The type and age of the vehicle you intend to purchase can also influence the loan. Newer cars typically attract better interest rates and longer repayment tenures because they are considered less risky (e.g., lower maintenance, higher resale value).

Used cars, especially older models, might come with higher interest rates and shorter repayment periods due to increased depreciation and potential maintenance costs. Some cooperatives might even have restrictions on the maximum age of a used car they will finance. Always check these specific vehicle-related policies.

Common Mistakes to Avoid When Applying for a CSE Car Loan: Learn from Others’ Errors

Navigating the loan application process can be tricky, and even seasoned applicants can make errors. Being aware of common pitfalls can save you time, frustration, and potentially secure a better outcome for your CSE Car Loan.

1. Incomplete or Inaccurate Documentation: The Biggest Hurdle

This is, without a doubt, the most frequent reason for delays or outright rejection. Submitting an application with missing documents, outdated proofs, or incorrect information forces the lender to request clarifications, stalling the process. Common mistakes include submitting blurry copies, expired IDs, or salary slips from an incorrect period.

Pro tips from us: Create a detailed checklist based on the cooperative’s requirements. Double-check every document for accuracy, validity, and completeness before submission. It’s better to spend extra time organizing than to face delays later.

2. Underestimating Your Debt-to-Income (DTI) Ratio: Overstretching Your Finances

Many applicants fail to accurately assess their current debt obligations against their income. They might apply for a loan amount that, when combined with existing EMIs (personal loans, home loans, credit card bills), pushes their DTI ratio beyond the lender’s acceptable limits. This signals a high risk of default.

Common mistakes to avoid are: not accounting for all monthly expenses or underestimating the new car loan EMI. Be realistic about what you can comfortably afford and aim for a loan amount that keeps your DTI within healthy bounds.

3. Not Researching Multiple CSEs (If Applicable): Missing Out on Better Deals

While you might be affiliated with one primary cooperative, it’s possible you qualify for loans from other affiliated or sister organizations. Limiting your research to just one option might mean missing out on more competitive interest rates, lower processing fees, or more flexible terms.

Pro tips from us: If your affiliations allow, explore all available cooperative car loan options. A few hours of research could lead to significant savings over the loan’s tenure.

4. Ignoring Your Credit Score: Assuming It Doesn’t Matter

There’s a misconception that because CSEs are member-focused, credit scores are less important. While they might be more flexible than commercial banks, a poor credit score still reflects negatively on your financial responsibility. Defaults, late payments, or too many credit inquiries can hurt your chances.

Common mistakes to avoid are: not checking your credit score before applying or not trying to improve it if it’s low. A good score demonstrates reliability and can lead to better loan terms.

5. Lack of Follow-Up: Being Passive in the Process

After submitting your application, it’s easy to assume the process will unfold automatically. However, a lack of proactive follow-up can sometimes lead to applications getting stuck or overlooked. This isn’t about being pushy, but rather about politely checking on the status.

Pro tips from us: After a reasonable waiting period (as advised by the cooperative), make a polite inquiry about your application’s status. Be prepared to provide any additional information or documents requested promptly.

By steering clear of these common errors, you can significantly enhance your chances of a smooth and successful CSE Car Loan application, bringing you closer to driving your desired vehicle.

Pro Tips for Securing the Best CSE Car Loan Deal: Maximize Your Savings

Getting approved for a CSE Car Loan is one thing; securing the absolute best deal is another. With some strategic planning and proactive steps, you can position yourself to receive the most favorable terms, saving you money and enhancing your financial comfort.

1. Prioritize Improving Your Credit Score: Your Financial Report Card

Even if your credit score is decent, striving for an excellent score (750+) can open doors to the lowest interest rates and most flexible terms. Start by paying all your bills on time, reducing existing debts, and avoiding new credit applications in the months leading up to your car loan application.

A strong credit score tells the cooperative that you are a reliable borrower, directly impacting the risk assessment and, consequently, the interest rate they offer. It’s your financial report card, so make it shine.

2. Save for a Higher Down Payment: The Power of Upfront Investment

A larger down payment is arguably one of the most effective ways to secure a better car loan deal. It directly reduces the principal loan amount, which means lower EMIs and less interest paid over the loan’s life. Furthermore, it signals financial stability and commitment to the lender, potentially unlocking more favorable terms.

Pro tips from us: Aim for at least 20-30% of the car’s value as a down payment. The more you put down upfront, the better your overall loan experience will be.

3. Compare Offers (Even Within CSEs): Don’t Settle for the First Quote

If you are eligible for car loans from multiple cooperative societies or employee funds, take the time to compare their offerings. Look beyond just the advertised interest rate. Consider processing fees, pre-payment penalties, and the flexibility of repayment options.

Even a small difference in interest rates or fees can lead to substantial savings over a typical 5-7 year loan tenure. This due diligence ensures you select the most cost-effective solution tailored to your needs.

4. Negotiate Terms (Where Possible): Don’t Be Afraid to Ask

While interest rates might be relatively fixed, there might be room for negotiation on other aspects, such as processing fees, administrative charges, or even the repayment tenure. Don’t assume everything is set in stone.

Pro tips from us: Politely inquire if there’s any flexibility on these terms, especially if you have a strong credit profile and a good relationship with the cooperative. A well-informed request can sometimes lead to unexpected benefits.

5. Understand the Fine Print: Avoid Hidden Surprises

Before signing any loan agreement, meticulously read and understand every clause. Pay close attention to details like pre-payment penalties, foreclosure charges, late payment fees, and any other administrative costs. Sometimes, attractive low interest rates might be offset by high hidden fees.

Common mistakes to avoid are: rushing through the agreement or assuming all terms are standard. If anything is unclear, ask for clarification. Knowledge is power, and understanding the fine print protects you from unexpected financial burdens down the line.

Navigating Repayment and Post-Loan Management: A Smooth Journey Ahead

Securing your CSE Car Loan is a major milestone, but the journey doesn’t end there. Effective repayment and post-loan management are crucial for maintaining good financial health and ensuring a smooth experience until your car is fully yours.

Understanding Your EMIs: Consistency is Key

Your Equated Monthly Installment (EMI) is the fixed amount you’ll pay back to the cooperative society each month. Ensure you fully understand the EMI amount, its due date, and the specific mode of payment (e.g., direct debit from your salary account, standing instruction). Consistency in timely payments is paramount.

Setting up auto-debit facilities is a smart way to ensure you never miss a payment, protecting your credit score and avoiding late fees. My observation has been that borrowers who set up automated payments rarely encounter issues.

Pre-payment Options: Paying Off Sooner

Many CSE Car Loans offer the flexibility of pre-payment, allowing you to pay off a portion of your loan principal before its due date. This can significantly reduce the total interest paid and shorten your loan tenure. Always check the terms for any pre-payment penalties. Some cooperatives might allow partial pre-payments without penalty after a certain period.

If you receive a bonus or an unexpected windfall, using a portion of it for a partial pre-payment can be a wise financial move, accelerating your journey to debt-free car ownership.

Foreclosure: Settling Your Loan Early

Foreclosure refers to paying off your entire outstanding loan amount before the scheduled end of the loan tenure. This can save you a substantial amount in future interest. Again, inquire about any foreclosure charges or specific procedures that need to be followed.

While there might be a small penalty, the long-term savings often outweigh it. Foreclosing your loan frees up your monthly budget and removes the hypothecation from your vehicle’s registration certificate, giving you full ownership.

Insurance Requirements: Protecting Your Asset

Most CSEs, like other lenders, will require you to maintain comprehensive car insurance throughout the loan tenure. This protects both your asset and the lender’s interest in case of an accident, theft, or damage. The cooperative society will often be listed as a beneficiary in your insurance policy.

Ensure you renew your insurance policy promptly each year and provide proof of renewal to the cooperative. Lapses in insurance can lead to penalties or even legal implications.

Maintaining Good Financial Health: The Long-Term View

Beyond the car loan, continuously practice good financial habits. Keep your other debts manageable, maintain a healthy credit score, and build an emergency fund. Timely repayment of your CSE Car Loan will reflect positively on your credit report, making it easier to secure future loans for other needs, such as a home or education.

For detailed insights into general car loan repayment strategies and managing your financial commitments, refer to this comprehensive guide from Investopedia (External Link).

Your Journey to Car Ownership Starts Here!

Securing a CSE Car Loan is more than just obtaining financing; it’s about leveraging a unique opportunity tailored for specific communities. This comprehensive guide has walked you through every critical aspect, from understanding its fundamental benefits and navigating eligibility to mastering the application process and managing your loan post-approval. We’ve shared insights from experience, highlighted common pitfalls to avoid, and provided pro tips to ensure you secure the best possible deal.

The dream of driving your own car is now within closer reach, especially if you are part of a cooperative society or a recognized employee group. By arming yourself with this in-depth knowledge, you are well-equipped to make informed decisions, avoid common mistakes, and confidently navigate the path to car ownership. Remember, meticulous preparation, understanding the fine print, and proactive management are your allies in this journey.

Don’t let the complexities of financing deter you. Embrace the advantages of a CSE Car Loan, follow these guidelines, and embark on the exciting journey of driving your dream car. What are your next steps? Share your thoughts or questions in the comments below – we’re here to help you every mile of the way!