Drive Your Dream Car: The Ultimate Guide to Soft Credit Check Car Loans

Drive Your Dream Car: The Ultimate Guide to Soft Credit Check Car Loans Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, especially when concerns about your credit score loom large. For many, the very thought of applying for a loan brings anxiety about potential damage to their credit report. This is where the often-misunderstood concept of a "soft credit check car loan" becomes a game-changer.

Imagine being able to explore your auto loan options, understand potential rates, and gauge your eligibility—all without any negative impact on your precious credit score. This isn’t a pipe dream; it’s the reality offered by soft credit checks. This comprehensive guide will demystify soft credit pull auto loans, empowering you to make informed decisions and confidently pursue your next vehicle.

Drive Your Dream Car: The Ultimate Guide to Soft Credit Check Car Loans

Understanding the Two Faces of Credit Inquiry: Soft vs. Hard

Before diving deep into soft credit check car loans, it’s crucial to grasp the fundamental difference between the two types of credit inquiries: soft and hard. This distinction is vital for protecting your financial standing.

The Hard Credit Check: When Lenders Get Serious

A hard credit check, also known as a "hard pull" or "hard inquiry," occurs when a lender genuinely needs to assess your creditworthiness for a final loan approval. This happens when you officially apply for new credit, such as a mortgage, personal loan, credit card, or, indeed, a traditional car loan.

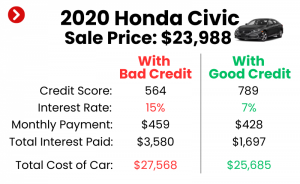

When you authorize a hard inquiry, the lender requests your full credit report and score from one or more of the major credit bureaus (Experian, Equifax, TransUnion). This detailed review helps them determine the risk associated with lending you money. Based on my experience, these inquiries are a necessary step in the final stages of securing financing.

The primary characteristic of a hard credit check is its impact on your credit score. Each hard inquiry can cause a slight, temporary dip in your score, usually by a few points. While one or two inquiries might not be catastrophic, multiple hard pulls in a short period can signal to other lenders that you’re actively seeking a lot of credit, potentially making you appear riskier.

The Soft Credit Check: Your Risk-Free Sneak Peek

In stark contrast, a soft credit check, or "soft pull," is a more casual look at your credit profile. It’s often used for pre-qualification, pre-approval, or when you check your own credit score through a personal finance app or credit monitoring service. Crucially, soft credit checks do not impact your credit score.

When a lender performs a soft pull, they access a limited version of your credit report. This allows them to get a general idea of your financial health, including your payment history and existing debt, without conducting a full, in-depth investigation. It’s like a preliminary screening that helps both you and the lender understand the landscape.

Soft credit checks are incredibly valuable because they allow you to explore various financing options without the fear of damaging your credit score. You can shop around, compare estimated rates, and understand what loan amounts you might qualify for, all while keeping your credit intact. This initial step can save you significant time and stress in the car buying process.

The Power of a Soft Credit Check for Your Car Loan Journey

Understanding the ‘soft pull’ mechanism opens up a world of strategic advantages when you’re looking to finance a car. It transforms the initial exploration phase into a low-risk, high-reward endeavor.

Gauge Your Eligibility Without Risk

One of the most significant benefits of a soft credit check car loan is the ability to determine your borrowing potential without any commitment or credit score penalty. You can discover if you’re likely to be approved for an auto loan and what kind of terms to expect. This early insight is invaluable for setting realistic expectations.

It prevents the frustration of applying for multiple loans, only to be rejected and incur several hard inquiries on your credit report. With a soft pull, you get a clear, non-binding indication of your standing, allowing you to proceed with confidence or adjust your strategy.

Shop Around Smartly for the Best Rates

The ability to compare multiple offers without affecting your credit score is a superpower for car buyers. Different lenders have varying criteria and offer different interest rates and terms based on your credit profile and their current market conditions.

By using soft credit checks, you can gather pre-approval offers from several banks, credit unions, and online lenders. This empowers you to identify the most competitive rates available to you. Based on my experience, shoppers who compare multiple offers often secure significantly better deals, saving them hundreds or even thousands of dollars over the life of the loan.

Protect Your Credit Score for Future Needs

As discussed, hard inquiries can temporarily lower your credit score. If you’re planning other major financial moves, like applying for a mortgage in the near future, protecting your credit score is paramount. A soft credit check car loan strategy allows you to explore financing without jeopardizing these other goals.

It’s a proactive approach to managing your credit, ensuring that you only proceed with a hard inquiry when you’ve found a truly suitable offer. This measured approach reflects responsible financial planning.

Empower Your Negotiation at the Dealership

Walking into a dealership with a pre-approved car loan offer in hand, secured through a soft credit check, puts you in a powerful negotiating position. You already know the interest rate and terms you qualify for from an external lender. This baseline empowers you to challenge any less favorable offers the dealership might present.

Dealers often try to bundle financing with the car purchase. Having an independent pre-approval means you can focus on negotiating the car’s price, knowing your financing is already competitive. Pro tips from us: Always have an outside offer ready; it’s your best leverage!

Save Time and Reduce Stress

The car buying process can be notoriously time-consuming and stressful. By pre-qualifying with a soft credit check, you streamline a significant portion of the financing stage. You arrive at the dealership with a clear understanding of your budget and financing options.

This eliminates much of the uncertainty and back-and-forth typically associated with loan applications. You can focus on finding the right vehicle, rather than worrying about whether you’ll be approved for the funds to buy it. It truly makes the entire experience more efficient and enjoyable.

How Soft Credit Checks Work in the Auto Loan Process

Understanding the mechanics of a soft credit check for an auto loan helps demystify the process. It’s simpler than you might think and designed for your convenience.

The Initial Inquiry: Your First Step

The process typically begins when you initiate an inquiry for an auto loan pre-qualification or pre-approval, usually through an online form. You’ll provide basic personal information such as your name, address, date of birth, income, and employment details. Importantly, you’ll also give consent for the lender to perform a soft credit check.

This consent is crucial, but it’s different from authorizing a full loan application. It signals that you’re interested in exploring options without committing to a full application that would trigger a hard inquiry.

The Lender’s Perspective: A Broad Assessment

Once you submit your information, the lender uses it to perform a soft pull of your credit. They’re not looking for every minute detail, but rather a snapshot of your credit history and score range. This allows them to quickly assess your general risk profile.

They’ll consider factors like your payment history, credit utilization, and any major derogatory marks. This quick assessment helps them determine if you broadly fit within their lending criteria for certain loan products.

Your Results: Estimated Rates and Terms

Within minutes, often instantaneously with online lenders, you’ll receive preliminary offers. These aren’t guaranteed final loan approvals but rather estimated rates, loan amounts, and terms you might qualify for. These offers are based on the information you provided and the results of the soft credit check.

It’s essential to remember that these are preliminary. The final offer might differ slightly after a full hard credit check and verification of all your financial details. However, they provide an excellent starting point for comparison.

Next Steps: Transitioning to Final Approval

If you find an offer that looks promising, you can then choose to proceed with a full loan application. At this stage, the lender will typically perform a hard credit check to verify all your information and provide a definitive loan offer. This is the point where the temporary dip in your credit score occurs.

By using the soft pull method, you ensure that this hard inquiry is made only for an offer you’ve already vetted as suitable. This strategic approach minimizes unnecessary impacts on your credit score.

Who Offers Soft Credit Check Car Loans?

Fortunately, many types of lenders now offer soft credit check options for car loans, recognizing the benefit to both themselves and potential borrowers. Knowing where to look can significantly streamline your search.

Online Lenders: The Pioneers of Soft Pulls

Online lenders have largely pioneered and popularized the soft credit check for pre-qualification. Their digital platforms are perfectly suited for quickly processing initial inquiries without the need for extensive paperwork or in-person visits.

Many reputable online auto loan providers explicitly advertise their soft pull pre-qualification services. This makes them an excellent first stop for anyone looking to explore their options discreetly and efficiently.

Banks and Credit Unions: Expanding Their Reach

While traditional banks and credit unions historically relied more on hard inquiries, many have adapted to the market demand for soft credit checks. Larger financial institutions often have online pre-approval tools that utilize a soft pull.

Credit unions, known for their member-centric approach, are also increasingly offering soft credit check options. It’s always a good idea to check with your existing bank or credit union first, as they may offer preferential rates to established customers.

Dealerships: Exercise Caution and Ask Questions

Many car dealerships now offer "pre-qualification" or "get approved" tools on their websites. While some of these do indeed use soft credit checks for initial screening, it’s crucial to be vigilant. Pro tips from us: Always ask the finance manager explicitly if their initial check is a "soft pull" or a "hard pull" before providing your social security number.

Common mistakes to avoid are assuming all dealership pre-approvals are soft pulls. Some might jump straight to a hard inquiry to expedite the process, especially if you’re already at the dealership. Be clear about your preference to only proceed with a soft check until you’re ready for a final application.

Navigating the Pre-approval Process with a Soft Pull

Embarking on the soft credit check pre-approval journey is straightforward. With a few key pieces of information, you can quickly get a clear picture of your auto loan potential.

Gather Your Essential Information

Before you start, have the following details readily available:

- Personal Information: Full name, address, date of birth, Social Security Number (for identity verification, but usually only for a soft pull).

- Employment Details: Employer’s name, job title, length of employment.

- Income Information: Gross monthly or annual income, and any other sources of income.

- Housing Information: Whether you rent or own, and your monthly housing payment.

Having these details handy will make filling out the online forms quick and seamless.

Fill Out the Online Form

Visit the websites of various lenders (online lenders, banks, credit unions). Look for sections like "pre-qualify," "get pre-approved," or "estimate your rate." You’ll typically be guided through a simple online form where you input the information you gathered.

Most of these forms are designed for speed and convenience, taking only a few minutes to complete. Remember, at this stage, you are typically not committing to a loan, just exploring your options.

Review Your Offers

After submitting your information, lenders will usually provide you with estimated loan terms, including the interest rate, loan amount, and monthly payment. You might receive offers from multiple lenders if you use a comparison platform.

Take your time to review each offer carefully. Pay attention to the Annual Percentage Rate (APR), the loan term (number of months), and any fees associated with the loan.

Choose Your Best Option (for Hard Inquiry)

Once you’ve compared all the soft credit check offers, identify the one that best suits your financial situation and car buying goals. This is the offer you’ll likely pursue for a final application.

Common mistakes to avoid are simply choosing the lowest monthly payment without considering the total cost of the loan or the interest rate. A lower monthly payment might come with a longer loan term, meaning you pay more interest over time.

Soft Credit Checks for Different Credit Scenarios

The beauty of soft credit checks is their versatility, offering benefits across the entire spectrum of credit profiles.

Excellent Credit: Confirming Your Advantage

If you boast an excellent credit score, a soft credit check primarily serves to confirm the favorable rates and terms you already expect. It streamlines your process, allowing you to quickly identify lenders offering the absolute best rates without impacting your pristine credit.

You can use these pre-approvals as a strong negotiating tool at the dealership, confident in the low interest rates you qualify for. It’s about efficiently securing the optimal deal.

Good/Average Credit: Unlocking Competitive Offers

For those with good or average credit, soft credit checks are invaluable. They help you pinpoint lenders who are most willing to work with your credit tier and offer competitive rates. You might find that some lenders are more lenient or have specific programs tailored for your credit range.

This allows you to avoid applying to lenders who primarily cater to excellent credit, saving you from potential rejections and unnecessary hard inquiries. It’s about finding the best fit for your specific credit profile.

Bad Credit: A Crucial First Step

For individuals with bad credit, soft credit check car loans are perhaps the most critical tool. Based on my experience, navigating the auto loan market with a low credit score can be incredibly disheartening, with multiple rejections leading to further credit damage from hard inquiries.

A soft pull allows you to discover which lenders specialize in bad credit car loans without risking further harm to your score. It helps set realistic expectations about interest rates and loan amounts, preventing wasted time and unnecessary credit pulls. This initial step can be the difference between finding a viable loan and compounding your credit woes. For more detailed insights, you might want to check out our article on Tips for Getting a Car Loan with Bad Credit (Internal Link Placeholder).

Maximizing Your Chances After a Soft Credit Check

A successful soft credit check is a great start, but there’s more you can do to ensure you secure the best possible final loan offer. Proactive steps can make a big difference.

Review Your Credit Report Thoroughly

Even after a soft pull, it’s always a good idea to obtain a full copy of your credit report from AnnualCreditReport.com. This is the only authorized site for free annual credit reports. Review it for any inaccuracies, errors, or fraudulent activity.

Disputing and correcting errors can potentially boost your credit score, which might lead to better loan terms. Common mistakes to avoid are neglecting to check your report, as even small errors can have an impact.

Strategically Improve Your Credit Score

If your soft credit check results weren’t as favorable as you hoped, you might consider taking a few months to improve your score before applying for a hard inquiry.

- Pay Bills On Time: Payment history is the most significant factor in your credit score. Ensure all your payments are made promptly.

- Reduce Existing Debt: Lowering your credit utilization (the amount of credit you use compared to your available credit) can quickly improve your score.

- Avoid New Credit Applications: Don’t apply for any other new credit during this period, as additional inquiries can be detrimental.

Save for a Larger Down Payment

A substantial down payment reduces the amount you need to borrow, which can make you a less risky borrower in the eyes of lenders. It can also lead to lower monthly payments and potentially better interest rates.

Furthermore, a larger down payment demonstrates your commitment and financial responsibility. It’s a clear signal that you’re invested in the purchase.

Consider a Co-signer (If Necessary)

If your credit score is still a hurdle, a co-signer with excellent credit might be an option. A co-signer agrees to be equally responsible for the loan, which can help you qualify for better rates.

However, understand the implications for both parties. The co-signer’s credit will also be affected if payments are missed. This is a significant responsibility and should only be considered with someone you trust implicitly.

Pro Tips from an Expert Blogger

Having advised countless individuals on their financing journeys, I’ve gathered some insights that can further enhance your soft credit check experience.

- Don’t Be Afraid to Ask: Always, always ask a lender or dealership if their initial pre-qualification or rate check is a "soft pull" or a "hard pull." Be explicit and confirm before proceeding. This simple question can save you from unwanted credit score dings.

- Read the Fine Print: While soft pulls don’t impact your score, the terms of pre-approval offers can vary. Pay close attention to the fine print regarding estimated rates, validity periods, and any conditions for final approval.

- Bundle Hard Inquiries: If you do proceed with hard inquiries, try to do them within a short window (typically 14-45 days, depending on the credit scoring model) for the same type of loan. Credit scoring models often treat multiple inquiries for the same type of loan within this window as a single inquiry, minimizing the impact on your score. This applies after you’ve used soft pulls to narrow down your choices.

- Understand Your Budget Beyond the Loan: While securing a great loan is important, remember to factor in other costs of car ownership: insurance, maintenance, fuel, and registration. A fantastic loan rate for a car you can’t truly afford in the long run isn’t a win. For more on this, explore our guide on Understanding Car Loan Interest Rates (Internal Link Placeholder).

Common Misconceptions About Soft Credit Check Car Loans

Despite their benefits, soft credit checks are often misunderstood. Let’s clear up some common myths.

- "A soft credit check guarantees loan approval." This is false. A soft pull provides pre-qualification or pre-approval, which are estimates. Final approval always requires a hard credit check and verification of all your financial information.

- "All lenders offer soft credit checks." While increasingly common, not every lender provides a soft pull option for pre-approval. Always confirm before proceeding.

- "It’s the same as a hard inquiry, just a different name." Absolutely not. The fundamental difference lies in the credit score impact. Soft pulls have none; hard pulls have a temporary, minor impact.

- "You can get a soft credit check with no information." You will always need to provide basic personal and financial information for a soft pull, as lenders need something to base their assessment on.

The Road Ahead: From Soft Pull to Driving Away

The soft credit check is your guiding light in the initial stages of securing a car loan. It empowers you to navigate the complex landscape of auto financing with confidence and strategic insight. By understanding your options without risk, you can make smarter decisions, secure better rates, and protect your financial health.

From the moment you begin your search for a new vehicle to the exhilarating moment you drive it off the lot, having a clear understanding of your financing capabilities is paramount. A soft credit check offers that clarity, transforming a potentially stressful process into an informed and efficient one. It’s about empowering you to take control of your car buying journey.

Ready to explore your options without fear? Start your soft credit check car loan journey today and take the first confident step towards driving your dream car. To learn more about managing your credit and understanding how inquiries affect your score, visit a trusted resource like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.