Drive Your Dream Car: The Ultimate Guide to Ufcu Car Loans

Drive Your Dream Car: The Ultimate Guide to Ufcu Car Loans Carloan.Guidemechanic.com

The open road, the fresh scent of a new interior, the hum of a reliable engine – for many, owning a car represents freedom, independence, and a vital part of daily life. However, turning that dream into a reality often involves navigating the complex world of auto financing. If you’ve been searching for a trustworthy and advantageous path to car ownership, you’ve likely come across the concept of credit union loans. Among them, Ufcu car loans stand out as a highly attractive option, offering a blend of competitive rates, flexible terms, and personalized service that traditional banks often can’t match.

This comprehensive guide is designed to be your definitive resource for understanding everything about Ufcu auto loans. We’ll delve deep into the advantages of choosing a credit union, walk you through the entire application process, reveal expert tips for securing the best deal, and help you avoid common pitfalls. Our ultimate goal is to equip you with the knowledge and confidence to make an informed decision, ensuring your journey to a new vehicle is as smooth and financially sound as possible. Get ready to unlock the power of Ufcu car loans and drive away with confidence!

Drive Your Dream Car: The Ultimate Guide to Ufcu Car Loans

Understanding Ufcu and the Credit Union Advantage

Before we dive into the specifics of Ufcu car loans, it’s crucial to understand what Ufcu represents and why credit unions, in general, are often a superior choice for auto financing. Ufcu, like other credit unions, operates under a fundamentally different model than commercial banks. This distinction translates directly into tangible benefits for you, the borrower.

What Makes Credit Unions Different?

Credit unions are not-for-profit financial cooperatives owned by their members. Unlike banks, which are driven by maximizing shareholder profits, credit unions exist solely to serve their members’ financial needs. This member-centric philosophy permeates every aspect of their operations, including their loan offerings.

Based on my experience, many people overlook credit unions, assuming they are exclusive or complicated. In reality, joining is often straightforward, and the benefits are substantial. This unique structure allows Ufcu to offer more favorable terms to its members, whether it’s for savings accounts, checking accounts, or, importantly, car loans.

Why Choose a Credit Union for Your Auto Loan?

The advantages of securing an auto loan through a credit union like Ufcu are numerous and significant. These benefits stem directly from their cooperative structure and commitment to member welfare.

Firstly, credit unions often provide lower interest rates compared to traditional banks. Because they don’t have shareholders to pay, any profits generated are typically reinvested into the credit union or returned to members in the form of lower loan rates and higher savings yields. This can translate into significant savings over the life of your Ufcu car loan.

Secondly, you’ll often find more flexible loan terms at a credit union. Ufcu understands that every member’s financial situation is unique. They are generally more willing to work with you to tailor a repayment plan that fits your budget, offering various loan durations and payment schedules. This flexibility can be a game-changer when trying to manage your monthly expenses.

Finally, the personalized service you receive at Ufcu is unparalleled. As a member, you’re not just a customer; you’re an owner. This fosters a more supportive and understanding relationship. When you apply for a Ufcu auto loan, you can expect attentive assistance and clear explanations, helping you feel confident and informed throughout the process.

The Ufcu Car Loan Advantage: Key Benefits Explored

When considering auto financing, the specifics of the loan package can make a world of difference. Ufcu car loans are designed with the member in mind, offering several distinct advantages that can significantly enhance your car buying experience and long-term financial health.

Competitive Interest Rates

One of the most compelling reasons to choose a Ufcu auto loan is the potential for highly competitive interest rates. As mentioned, the not-for-profit model allows credit unions to pass savings directly to their members. This often means lower Annual Percentage Rates (APRs) on car loans compared to what you might find at larger commercial banks. Even a small difference in the interest rate can save you hundreds, if not thousands, of dollars over the life of your loan.

Pro tips from us: Always compare rates from multiple lenders, but make sure to include Ufcu in your comparison. You’ll likely find their offerings to be among the most attractive in the market.

Flexible Loan Terms Designed for You

Ufcu understands that a one-size-fits-all approach doesn’t work for auto financing. They typically offer a range of flexible loan terms, allowing you to choose a repayment period that aligns with your financial capacity and goals. Whether you prefer a shorter term to pay off your loan faster and save on interest, or a longer term to reduce your monthly payments, Ufcu often has options available.

This flexibility is crucial for budgeting. A longer term might mean lower monthly payments, making a more expensive vehicle more accessible. However, it also means paying more interest over time. A shorter term, while having higher monthly payments, saves you money on interest in the long run.

The Power of Pre-Approval with Ufcu

Securing pre-approval for your Ufcu car loan is a strategic move that provides immense benefits before you even step foot in a dealership. Pre-approval means Ufcu has reviewed your financial situation and provisionally agreed to lend you a specific amount at a certain interest rate.

Having a Ufcu auto loan pre-approval in hand transforms you into a cash buyer at the dealership. This gives you significant negotiating power on the vehicle’s price, as you’re not reliant on the dealer’s financing options. It also establishes a clear budget, preventing you from falling in love with a car outside your financial comfort zone.

Becoming a Ufcu Member: Your First Step to a Great Car Loan

To take advantage of the excellent Ufcu car loan rates and benefits, you first need to become a member. This process is generally straightforward and designed to be as accessible as possible. Don’t let the "membership" aspect intimidate you; it’s simpler than you might think.

Eligibility Requirements for Ufcu Membership

Credit unions typically have specific fields of membership. These can vary but often include:

- Geographic location: Living, working, worshipping, or attending school in a particular county or region.

- Employer affiliation: Being employed by a specific company or organization.

- Family relationships: Being related to an existing member.

- Association or group affiliation: Being a member of a certain association or community group.

Many credit unions also offer a broader path to membership, such as joining a specific, low-cost association that automatically qualifies you. Ufcu will clearly outline its membership requirements on its website or when you inquire.

The Simple Membership Process

Once you determine your eligibility, becoming a Ufcu member is usually a quick process. You’ll typically need to open a savings account with a small initial deposit, often as little as $5 or $25. This deposit establishes your share in the credit union and grants you all the rights and privileges of membership.

You can often complete the membership application online, by phone, or by visiting a local Ufcu branch. Be prepared to provide some basic personal information and identification documents. Once you’re a member, you gain access to all of Ufcu’s financial products and services, including their competitive car loans.

The Ufcu Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for any loan can feel daunting, but with Ufcu, it’s designed to be clear and supportive. Following these steps will help you prepare thoroughly and increase your chances of securing the best possible Ufcu auto loan.

Step 1: Get Your Finances in Order

Before you even think about applying for a Ufcu car loan, it’s crucial to understand your current financial standing. This foundational step will save you time and potential frustration later on.

First, check your credit score and credit report. Your credit score is a primary factor in determining your interest rate and loan approval. You can obtain a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) annually through AnnualCreditReport.com. Review it carefully for any errors that could negatively impact your score. For more tips on improving your credit score, check out our guide on .

Next, determine your budget. This involves more than just the car’s price. Consider your down payment capabilities and what you can comfortably afford for a monthly payment. Don’t forget to factor in other car-related expenses like insurance, maintenance, and fuel. A good rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 15-20% of your net monthly income.

Finally, gather necessary documents. Having these ready will streamline the application process. Typically, you’ll need:

- Government-issued ID (driver’s license, passport).

- Proof of income (pay stubs, tax returns, employment verification).

- Proof of residency (utility bill, lease agreement).

- Social Security number.

Common mistakes to avoid are not checking your credit report beforehand or underestimating the true cost of car ownership. Being prepared financially sets the stage for a successful Ufcu car loan application.

Step 2: Apply for Pre-Approval with Ufcu

Once your finances are in order, the next logical step is to apply for a Ufcu auto loan pre-approval. This can often be done conveniently online through Ufcu’s website, over the phone, or by visiting a branch in person.

The pre-approval application will ask for details about your income, employment, existing debts, and the loan amount you’re seeking. Ufcu will then conduct a credit check and, if approved, provide you with a pre-approval letter. This letter will state the maximum loan amount you qualify for and the interest rate you can expect.

The benefits of pre-approval are immense. It clarifies your budget, empowers you to negotiate confidently at the dealership, and makes the entire car buying process less stressful. You’ll know exactly what you can afford before you even start shopping.

Step 3: Find Your Dream Car

With your Ufcu pre-approval in hand, you’re ready to find your vehicle. This is where the fun begins!

Consider whether a new or used car best fits your needs and budget. New cars offer the latest features and peace of mind, while used cars can provide excellent value and depreciate slower. Research different makes and models, read reviews, and take test drives.

Decide whether you’ll buy from a dealership or a private seller. Ufcu car loans can often finance both, but the process might differ slightly for private party sales, requiring more paperwork to verify the vehicle’s title and condition.

Step 4: Finalize the Loan with Ufcu

Once you’ve found the perfect car, the final step is to finalize your Ufcu car loan. This involves reviewing the loan agreement in detail.

Pay close attention to the Annual Percentage Rate (APR), the loan term, and any associated fees. Ensure that all the terms match what was discussed during your pre-approval. Don’t hesitate to ask your Ufcu loan officer any questions you have.

Once you’re satisfied, you’ll sign the paperwork, and the funds will be disbursed. Ufcu may pay the dealership directly or provide you with a check to complete the purchase. Congratulations, you’re now the proud owner of your dream car, financed by a trusted partner!

Types of Ufcu Car Loans

Ufcu typically offers a variety of car loan options to suit different needs and circumstances. Understanding these distinctions can help you choose the best fit for your specific situation.

New Car Loans

These loans are for brand-new vehicles purchased from a dealership. New Ufcu car loans often come with the most competitive interest rates and longest terms, as new cars are considered less risky collateral due to their predictable value and warranty coverage. If you’re looking for the latest model with full manufacturer backing, a new car loan from Ufcu is your primary option.

Used Car Loans

For those seeking value and lower initial costs, a used car loan is an excellent choice. Ufcu offers used car loans for pre-owned vehicles, often with slightly higher interest rates than new car loans due to factors like vehicle age, mileage, and condition. However, Ufcu’s rates for used vehicles are still highly competitive. They typically have specific requirements regarding the age and mileage of the used vehicle they will finance.

Auto Loan Refinancing

Perhaps you already have a car loan with another lender, but the interest rate is higher than you’d like, or your financial situation has improved since you first financed the vehicle. Ufcu auto loan refinancing allows you to replace your current car loan with a new one from Ufcu, potentially at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payments or the total interest paid over the loan’s life.

Based on my experience, refinancing is often overlooked but can be a powerful tool for saving money. If your credit score has improved or interest rates have dropped since you originally financed your car, exploring Ufcu auto loan refinancing is highly recommended.

Other Vehicle Loans (Motorcycle, RV, Boat)

Beyond traditional cars, many credit unions like Ufcu also offer financing for other recreational vehicles. If you’re dreaming of a motorcycle, an RV for cross-country adventures, or a boat for weekend getaways, inquire with Ufcu. They may have specific loan products tailored for these types of vehicles, often with similar benefits to their standard car loans.

Factors Influencing Your Ufcu Car Loan Approval & Rates

When you apply for a Ufcu car loan, several key factors come into play that will determine whether your application is approved and what interest rate you’ll receive. Understanding these elements can help you optimize your financial profile before applying.

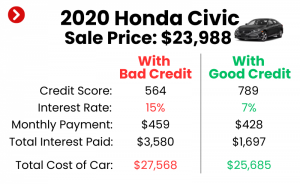

Your Credit Score

This is arguably the most significant factor. Your credit score reflects your creditworthiness – your history of borrowing and repaying debt. A higher credit score (generally 700+) indicates a lower risk to Ufcu, leading to better interest rates and easier approval. Conversely, a lower score might result in higher rates or require a co-signer.

Ufcu, like all lenders, uses your credit score to assess risk. A strong score demonstrates a history of responsible financial behavior, which is a major green light for lenders.

Debt-to-Income (DTI) Ratio

Your DTI ratio is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders use this to gauge your ability to take on additional debt. A lower DTI ratio (typically below 36-43%) indicates that you have sufficient income to manage new loan payments, making you a more attractive borrower for a Ufcu auto loan.

Loan Amount and Term

The total amount you wish to borrow and the repayment period (loan term) also impact your rate and approval. A larger loan amount or a very long loan term can sometimes increase the perceived risk, potentially affecting your interest rate. Ufcu will assess if the loan amount is appropriate for the vehicle’s value and your financial capacity.

Vehicle Age and Mileage

Especially for used car loans, the age and mileage of the vehicle play a role. Older vehicles with high mileage are generally considered higher risk due to potential mechanical issues and depreciation. Ufcu may have limits on the age or mileage of vehicles they will finance, or they may offer different rates based on these factors.

Your Down Payment

Making a substantial down payment reduces the amount you need to borrow, which can lead to a lower monthly payment and less interest paid over time. It also signals your commitment to the loan and reduces Ufcu’s risk, potentially securing you a better interest rate. A down payment of 10-20% is often recommended.

Co-signer (If Applicable)

If your credit score is less than ideal or your DTI ratio is high, Ufcu might suggest or require a co-signer. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you default. This can significantly improve your chances of approval and help you secure a better rate.

Pro Tips for a Smooth Ufcu Car Loan Experience

Securing a Ufcu car loan can be a smooth and rewarding experience if you approach it strategically. Based on my years of helping clients with auto financing, these tips are crucial for getting the best deal and avoiding common pitfalls.

Don’t Just Look at the Monthly Payment

While a low monthly payment is appealing, it shouldn’t be your sole focus. A low payment often means a longer loan term, which can result in paying significantly more interest over the life of the loan. Always consider the total cost of the loan, including all interest and fees, not just the monthly installment.

Read the Fine Print Carefully

Before signing any loan agreement, take the time to read every single detail. Understand the Annual Percentage Rate (APR), any fees, late payment penalties, and prepayment clauses. If anything is unclear, ask your Ufcu loan officer for a detailed explanation. Don’t be afraid to ask questions until you fully comprehend the terms.

Negotiate with Confidence (Especially with Pre-Approval)

Your Ufcu car loan pre-approval is a powerful negotiating tool. It means you’ve already secured financing, allowing you to focus purely on negotiating the vehicle’s price with the dealer. Don’t let them push you into their financing options if your Ufcu rate is better. You are in control of the financing aspect.

Consider GAP Insurance

Guaranteed Asset Protection (GAP) insurance is an optional coverage that can be invaluable. If your car is totaled or stolen, and you owe more on your loan than the vehicle’s actual cash value (ACV), GAP insurance covers the difference. This is especially relevant for new cars, which depreciate rapidly. Discuss this option with Ufcu or your auto insurance provider.

Budget for More Than Just the Car Payment

Remember that car ownership involves more than just the loan payment. You’ll have insurance premiums, fuel costs, routine maintenance (oil changes, tires), and potential unexpected repairs. Factor all these expenses into your monthly budget to ensure your Ufcu car loan doesn’t become a financial burden. Learn more about budgeting for your new car in our article .

Common Questions About Ufcu Car Loans

It’s natural to have questions when considering a significant financial commitment like a car loan. Here are some frequently asked questions about Ufcu car loans.

Can I get a Ufcu car loan with bad credit?

While a higher credit score generally leads to better rates, Ufcu, as a member-focused institution, is often more willing to work with individuals who have less-than-perfect credit. They may offer specific programs, require a larger down payment, or suggest a co-signer. It’s always best to speak directly with a Ufcu loan officer to discuss your options.

How long does Ufcu car loan approval take?

The approval time for a Ufcu car loan can vary. Online pre-approvals can sometimes be processed within minutes or a few hours during business days. Full loan approval after submitting all documents might take anywhere from one to three business days, depending on the complexity of your application and the volume of applications Ufcu is processing.

What’s the maximum loan amount Ufcu offers?

The maximum loan amount for a Ufcu car loan depends on several factors, including your creditworthiness, debt-to-income ratio, the value of the vehicle you’re purchasing, and Ufcu’s internal lending policies. There isn’t a universal maximum, as it’s assessed on a case-by-case basis to ensure responsible lending.

Can I refinance an existing loan with Ufcu?

Yes, Ufcu typically offers auto loan refinancing options. If you have an existing car loan with another lender and believe you could get a better interest rate or more favorable terms, you can apply to refinance that loan with Ufcu. This is a common way for members to save money or adjust their monthly payments.

Conclusion: Your Road to Smart Car Ownership Starts with Ufcu

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, and choosing the right financing partner is a critical step in making that dream a reality without financial stress. Throughout this comprehensive guide, we’ve explored the myriad benefits of securing a Ufcu car loan, highlighting their competitive interest rates, flexible terms, and the personalized service that truly sets credit unions apart.

By understanding the Ufcu membership process, preparing your finances, and leveraging the power of pre-approval, you position yourself for a smooth and advantageous car buying experience. Whether you’re purchasing a brand-new vehicle, a reliable used car, or looking to refinance an existing loan, Ufcu offers tailored solutions designed with your financial well-being in mind. Their commitment to members means you’re not just getting a loan; you’re gaining a partner dedicated to helping you achieve your goals.

Don’t let the complexities of auto financing deter you from driving the car you need and want. We encourage you to explore Ufcu for your auto financing needs. Visit their website, speak with a loan officer, and discover how a Ufcu car loan can put you in the driver’s seat with confidence and peace of mind. Your dream car is within reach – let Ufcu help you get there.