Drive Your Dream: The Ultimate Guide on How To Buy A Car With A Car Loan (and Get Approved!)

Drive Your Dream: The Ultimate Guide on How To Buy A Car With A Car Loan (and Get Approved!) Carloan.Guidemechanic.com

The scent of a new car, the feeling of the open road, the independence of having your own wheels – buying a car is an exciting milestone for many. But let’s be honest, the process of how to buy a car with a car loan can often feel more like navigating a complex maze than a joyful journey. From understanding your credit score to comparing loan offers and deciphering dealership jargon, there’s a lot to consider.

Fear not, aspiring car owners! As an expert blogger and seasoned professional in the auto finance world, I’ve seen it all. My mission with this comprehensive guide is to demystify the entire process, providing you with invaluable insights, practical strategies, and insider tips to secure the best possible car loan and drive away with confidence. This isn’t just about getting a loan; it’s about making an informed decision that benefits your financial future.

Drive Your Dream: The Ultimate Guide on How To Buy A Car With A Car Loan (and Get Approved!)

We’ll cover everything from budgeting and pre-approval to smart shopping, negotiation tactics, and responsible car ownership. By the end of this article, you’ll be equipped with the knowledge to make your car buying experience smooth, stress-free, and successful. Let’s get started on your journey to financing a car the smart way!

Section 1: Laying the Foundation – Before You Even Look at Cars

Before you even step foot on a dealership lot or browse online listings, the most crucial work happens at home. This preparatory phase is vital for understanding your financial capabilities and strengthening your position as a buyer. Skipping these steps is a common mistake that can lead to overspending or getting stuck with unfavorable loan terms.

Understanding Your Financial Landscape: What Can You Truly Afford?

The first and most critical step in how to buy a car with a car loan is creating a realistic budget. This isn’t just about the monthly car payment; it’s about the total cost of car ownership. Many people focus solely on the payment, forgetting the myriad of other expenses that come with owning a vehicle.

Consider all potential costs: the monthly loan payment, car insurance premiums, fuel expenses, routine maintenance (oil changes, tire rotations), unexpected repairs, registration fees, and even parking costs. A good rule of thumb is to allocate no more than 10-15% of your net monthly income towards all car-related expenses, including the loan payment. Overestimating your affordability can quickly lead to financial strain down the road.

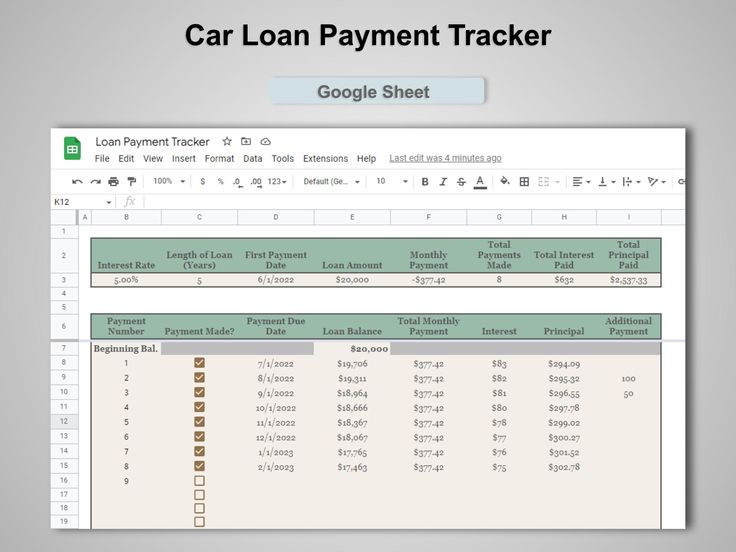

Pro Tip from Us: Create a detailed spreadsheet or use a budgeting app to itemize all your current monthly expenses. Then, factor in potential car ownership costs. This visual representation will give you a clear picture of what you can comfortably afford without compromising other financial goals. For a deeper dive into budgeting specifically for your first car, check out our article on Budgeting for Your First Car: What You REALLY Need to Consider.

Your Credit Score: The Key to Unlocking Better Rates

Your credit score is arguably the most influential factor when it comes to getting approved for a car loan and securing a favorable interest rate. Lenders use your score to assess your creditworthiness – essentially, how risky you are as a borrower. A higher score typically translates to lower interest rates, saving you hundreds or even thousands of dollars over the life of the loan.

Before applying for any loan, get a copy of your credit report from all three major credit bureaus (Experian, Equifax, TransUnion). Review it carefully for any errors, as even small inaccuracies can negatively impact your score. If you find discrepancies, dispute them immediately. Understanding your credit history is a powerful tool in the car buying process.

If your credit score isn’t where you’d like it to be, take steps to improve it. Paying bills on time, reducing existing debt, and avoiding new credit applications can all help boost your score. Even a few points can make a difference in the interest rate you’re offered. For more detailed guidance, our article on Understanding Your Credit Score: A Comprehensive Guide can provide valuable insights.

Debt-to-Income Ratio: Another Lender Consideration

Beyond your credit score, lenders also scrutinize your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to manage new debt, making you a less risky borrower.

Typically, lenders prefer a DTI ratio of 36% or less, though some might go higher depending on other factors. To calculate your DTI, add up all your monthly debt payments (mortgage/rent, student loans, credit card minimums, etc.) and divide that sum by your gross monthly income. Understanding and, if necessary, improving this ratio can significantly aid your car loan application process.

Section 2: The Loan Hunt – Securing Your Financing

Once you have a clear picture of your finances, it’s time to actively seek out your car loan. This stage is where many buyers make crucial decisions that impact their overall car ownership cost. The goal here is to get the best possible terms before you even start negotiating on a car.

Pre-Approval is Your Superpower

This is perhaps the single most important auto loan tip I can give you: get pre-approved for a loan before you go car shopping. What is pre-approval? It’s when a lender reviews your credit and financial information and tentatively agrees to lend you a specific amount of money at a particular interest rate, subject to the final vehicle selection.

Benefits of Pre-Approval:

- Know Your Budget: You’ll know exactly how much you can spend, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You walk into the dealership with cash in hand (figuratively speaking). This shifts the focus from "Can I afford this car?" to "What’s the best price you can give me?"

- Compare Offers: Pre-approval allows you to compare rates from multiple lenders without pressure. It also gives you a benchmark to evaluate any financing offers from the dealership.

You can seek pre-approval from various sources: your existing bank, local credit unions (often offering very competitive rates), or reputable online lenders. Apply to several to compare interest rates and loan terms. Don’t worry about multiple inquiries affecting your score too much; credit bureaus typically count multiple auto loan inquiries within a short period (usually 14-45 days) as a single inquiry, recognizing you’re rate shopping.

Common Mistake to Avoid: Walking into a dealership without pre-approval. This puts you at a significant disadvantage. The dealer controls the financing terms, and you have no external offer to compare against, making it easier for them to push less favorable rates or longer loan terms. Always arrive with your own financing in hand, even if you intend to see what the dealership can offer.

Comparing Loan Offers: Understanding the Numbers

When you receive pre-approval offers, it’s critical to understand the key components beyond just the monthly payment. These factors determine the true cost of your loan.

- Annual Percentage Rate (APR): This is the single most important number. APR represents the true annual cost of borrowing, including the interest rate and any fees. A lower APR means less money paid over the life of the loan. Don’t just look at the interest rate; always compare the APR.

- Loan Term: This is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term means lower monthly payments but significantly higher total interest paid over time. Conversely, a shorter term has higher monthly payments but saves you money on interest.

- Based on my experience: While a 72-month loan might seem appealing due to lower monthly payments, it often means you’ll pay interest for longer, and the car might depreciate faster than you pay off the loan, leading to being "upside down" (owing more than the car is worth). Aim for the shortest term you can comfortably afford.

- Down Payment: While not always required, making a down payment is highly recommended. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. A substantial down payment (10-20% of the car’s value) also helps you avoid being upside down on your loan, especially with new cars that depreciate quickly.

Section 3: Finding Your Dream Ride – Smart Car Shopping

With your financing secured, you’re now in a powerful position to find the right vehicle. This stage involves thorough research, careful consideration, and strategic negotiation. Remember, the car itself is only one part of the equation; ensuring it fits your needs and budget is paramount.

Research, Research, Research: Making an Informed Choice

Now that you know how much you can spend, it’s time to find the car that fits your lifestyle and needs. Don’t rush this process.

- New vs. Used: Both have their merits. New cars offer the latest technology, full warranties, and that "new car smell," but they depreciate rapidly. Used cars are more budget-friendly and have already taken the biggest depreciation hit, but might require more maintenance. Consider certified pre-owned (CPO) vehicles for a good middle ground.

- Reliability, Safety, Resale Value: These are critical long-term considerations. Research consumer reports, safety ratings (like those from the NHTSA or IIHS), and projected resale values. A car that holds its value well will benefit you when it’s time to sell or trade-in.

- Test Drives: Never buy a car without a thorough test drive. Drive it on various roads – city streets, highways, uneven surfaces – to assess comfort, handling, and visibility. Pay attention to blind spots, cabin noise, and the functionality of all features. Bring a friend or family member for a second opinion.

Negotiation Strategies: Focus on the Out-the-Door Price

When you’re ready to negotiate, remember your pre-approval gives you leverage. Always focus on the "out-the-door" price, which includes the vehicle’s price, taxes, and all fees. Don’t let the salesperson shift your focus solely to the monthly payment, as they can manipulate the loan term to make payments seem lower, increasing your overall cost.

Pro Tips from Us:

- Separate Trade-ins: If you have a trade-in, negotiate the price of the new car first. Once that’s settled, then discuss the value of your trade-in. Combining these negotiations can make it harder to see if you’re getting a fair deal on either.

- Be Prepared to Walk Away: This is your strongest negotiation tool. If you’re not getting the deal you want, politely decline and leave. Often, this can prompt the salesperson to offer a better deal.

- Research Market Value: Use sites like Kelley Blue Book (KBB) or Edmunds to understand the fair market value of the car you’re interested in, both new and used. This knowledge empowers you during negotiations.

Section 4: Navigating the Dealership – Finalizing the Purchase

This is the final stretch, where you’ll sign the paperwork and take ownership of your new vehicle. While exciting, this stage also requires vigilance to avoid unnecessary costs and ensure all terms are clear. This is where your preparedness from the earlier steps truly pays off.

Understanding the Paperwork: Read Every Line!

Once you’ve agreed on a price, you’ll be directed to the finance and insurance (F&I) office. This is where you’ll sign the final sales agreement and loan documents. This is a critical point where you need to be alert and meticulous.

- Sales Agreement: Read every single line of the sales agreement before signing. Ensure the agreed-upon price, trade-in value (if applicable), and all fees are accurately reflected.

- Hidden Fees & Add-ons: This is where many dealerships try to boost their profits. Be wary of charges like VIN etching, fabric protection, extended warranties, or rustproofing that you didn’t ask for or don’t truly need. Politely decline anything you don’t want. While some extended warranties can be valuable, research their cost and coverage thoroughly.

- Gap Insurance: If you’re putting down a small down payment or financing a car that depreciates quickly, consider gap insurance. This covers the "gap" between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. While dealerships offer it, you can often find it cheaper through your car insurance provider or a separate insurer.

Dealership Financing vs. Your Pre-Approval: Always Compare

Even though you have a pre-approved loan, it’s always a good idea to see what the dealership’s finance department can offer. Sometimes, due to special promotions or relationships with specific lenders, they might be able to beat your existing offer.

Based on my experience: I always advise clients to present their pre-approval and then ask the dealership to try and beat it. If they can offer a lower APR or better terms, great! But if they can’t, you simply stick with your pre-approved loan. This strategy ensures you’re getting the absolute best interest rates for your car loan application. Never feel pressured to take dealership financing if your outside offer is better.

Take your time in the F&I office. Don’t feel rushed to sign anything you don’t fully understand or agree with. If something doesn’t look right, ask for clarification. If you’re still uncomfortable, don’t hesitate to say you need more time to review the documents or even bring them home to read more carefully (though this isn’t always feasible with busy dealerships).

Section 5: After the Purchase – Responsible Car Ownership

Congratulations! You’ve successfully navigated the complexities of how to buy a car with a car loan and are now the proud owner of a new vehicle. But the journey doesn’t end here. Responsible car ownership involves several ongoing commitments to protect your investment and ensure financial stability.

Car Insurance: A Non-Negotiable Necessity

Before you even drive your new car off the lot, you must have car insurance. Most states require a minimum level of liability insurance, and your lender will almost certainly require comprehensive and collision coverage to protect their investment (the car itself).

Factor the cost of car insurance into your budget from day one. Get quotes from multiple insurance providers before buying the car, as premiums can vary significantly based on the vehicle’s make, model, your driving history, and even where you live. This is a crucial ongoing expense that cannot be overlooked.

Loan Repayment: Staying on Track

Managing your loan repayment responsibly is paramount. Set up automatic payments from your bank account to avoid missed payments, which can incur late fees and negatively impact your credit score.

Consider making extra payments whenever possible, even if it’s just a small amount. Any additional principal payments will reduce the total interest you pay over the life of the loan and help you pay it off faster. For example, if your payment is $300, consider paying $325. That extra $25 goes directly to reducing your principal.

Maintenance: Protecting Your Investment

A car is a significant investment, and proper maintenance is key to its longevity and reliability. Follow the manufacturer’s recommended service schedule for oil changes, tire rotations, brake inspections, and other routine maintenance. Neglecting these can lead to more expensive repairs down the line and can even void your warranty.

Keep detailed records of all maintenance performed. This documentation can be valuable if you ever need to make a warranty claim or when you eventually sell the vehicle, demonstrating that it has been well cared for.

Conclusion: Driving Forward with Confidence

Buying a car with a car loan is a significant financial undertaking, but it doesn’t have to be overwhelming. By following the comprehensive steps outlined in this guide – from meticulous budgeting and securing pre-approval to smart shopping, careful negotiation, and responsible post-purchase actions – you empower yourself to make intelligent decisions. You’re not just buying a car; you’re investing in your mobility and financial well-being.

Remember, knowledge is power. Arm yourself with information, compare offers, read the fine print, and never feel pressured into a deal that doesn’t feel right. By taking a proactive and informed approach, you can successfully navigate the complexities of how to buy a car with a car loan, secure favorable terms, and drive away with the perfect vehicle for your needs and budget.

We hope this in-depth guide has provided you with the confidence and clarity needed for your next vehicle purchase. What was your biggest takeaway, or what challenge are you most looking forward to tackling in your car buying journey? Share your thoughts and experiences in the comments below!

External Link: For more information on understanding your rights as a consumer during the car buying process, visit the Federal Trade Commission’s guide on buying a car: https://www.consumer.ftc.gov/articles/0055-buying-car