Drive Your Dream: The Ultimate Guide to Applying for a Car Loan with Bank of America

Drive Your Dream: The Ultimate Guide to Applying for a Car Loan with Bank of America Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect. Whether it’s a brand-new car fresh off the lot or a reliable used model, securing the right financing is a critical step. For many, Bank of America stands out as a leading financial institution offering competitive auto loan options. But how exactly do you navigate the process to apply for a car loan Bank of America?

This comprehensive guide will walk you through every stage, from initial preparation to final approval, ensuring you’re well-equipped to make informed decisions. Our goal is to demystify the Bank of America car loan application process, providing you with expert insights and practical tips that increase your chances of securing the best terms. Let’s hit the road towards your new car!

Drive Your Dream: The Ultimate Guide to Applying for a Car Loan with Bank of America

Why Consider Bank of America for Your Car Loan?

When you’re looking to apply for a car loan Bank of America provides several compelling reasons why they might be the right choice for your vehicle financing needs. Their long-standing reputation and extensive financial services make them a popular option for many consumers. They offer a blend of competitive rates and customer-focused services.

Based on my experience in the financial sector, a large institution like Bank of America often provides stability and a streamlined process. They are equipped to handle a high volume of applications efficiently, making the experience less daunting for borrowers. This reliability is a significant factor for many when choosing a lender.

Competitive Rates and Flexible Terms

Bank of America is known for offering competitive interest rates, especially for applicants with strong credit profiles. Lower interest rates translate directly into lower monthly payments and less overall cost for your vehicle. They also provide flexible loan terms, allowing you to choose a repayment schedule that aligns with your financial situation.

Whether you prefer a shorter term to pay off your loan faster or a longer term to reduce your monthly obligations, Bank of America typically offers various options. This flexibility is crucial for budgeting and managing your finances effectively. Always compare their rates with other lenders to ensure you’re getting the best deal.

Convenient Application Process

One of the significant advantages of opting for a Bank of America auto loan is the convenience of their application process. You can often begin your application online from the comfort of your home, saving valuable time. This digital accessibility means you can apply at your own pace, reviewing all requirements before submission.

Additionally, if you’re an existing Bank of America customer, the process can be even smoother. They often have your financial information on file, potentially simplifying data entry and accelerating the review process. This integration can be a real time-saver for busy individuals.

Trusted Institution with Excellent Support

Bank of America is a household name, synonymous with trust and reliability in the financial world. This reputation extends to their auto loan services. You can expect professional customer support throughout your application and repayment period.

Having a dependable institution backing your loan provides peace of mind. Should you have questions or encounter issues, their extensive network of branches and customer service channels are readily available to assist you. This support system is invaluable when navigating a significant financial commitment like a car loan.

Before You Apply: Essential Preparation Steps

Successfully securing a Bank of America car loan application isn’t just about filling out a form; it’s about strategic preparation. The groundwork you lay before even touching the application can significantly impact your approval odds and the terms you receive. This proactive approach shows lenders you are a responsible borrower.

Pro tips from us: Think of this pre-application phase as building a strong foundation. The more solid your foundation, the more stable your loan will be. Taking the time to get these steps right can save you money and stress in the long run.

1. Know Your Credit Score Inside Out

Your credit score is arguably the most crucial factor lenders consider when you apply for a car loan Bank of America. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score signals less risk to lenders, often resulting in better interest rates and more favorable loan terms.

Before applying, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion). You can do this annually for free through AnnualCreditReport.com. Review these reports thoroughly for any errors or discrepancies that could negatively impact your score. If you find mistakes, dispute them immediately. For a deeper dive into improving your credit, you might want to read our article on Understanding Your Credit Score and How to Improve It (internal link).

2. Determine Your Realistic Budget

Beyond the sticker price of the car, owning a vehicle involves numerous other expenses. It’s vital to determine a realistic budget that encompasses not just your monthly loan payment but also insurance, fuel, maintenance, and potential repair costs. Failing to account for these can lead to financial strain.

Consider your current income, existing debts, and monthly expenses to calculate how much you can comfortably afford to pay each month for a car. Use online auto loan calculators to estimate payments based on different loan amounts, interest rates, and terms. This comprehensive approach ensures your new car is an asset, not a burden.

3. Research the Vehicle You Want

Having a clear idea of the vehicle you intend to purchase is beneficial before you apply for a car loan Bank of America. Whether you’re eyeing a brand-new SUV or a reliable pre-owned sedan, knowing the make, model, year, and approximate price helps you determine the loan amount you’ll need. This specificity helps the lender assess the loan’s collateral.

Researching also extends to understanding the typical market value of your chosen vehicle. This knowledge empowers you during negotiations with dealerships and helps prevent you from overpaying. Be prepared to share details about the vehicle with Bank of America during the application process.

4. Gather All Required Documents

Preparation includes compiling all necessary paperwork in advance. This step can significantly speed up your Bank of America car loan application. Having your documents ready demonstrates organization and efficiency, which can positively influence the lender.

Common documents typically include proof of identity (driver’s license, passport), proof of income (pay stubs, tax returns, bank statements), proof of residence (utility bills, lease agreement), and details about the vehicle you intend to purchase (if known). Ensure all documents are current and accurate.

Understanding Bank of America’s Car Loan Requirements

When you apply for a car loan Bank of America, they will assess several key factors to determine your eligibility and the terms of your loan. Understanding these requirements beforehand helps you present yourself as a strong candidate. Each criterion plays a role in the overall decision.

Common mistakes to avoid are assuming your good credit alone is enough or neglecting to understand income verification needs. Bank of America looks at a holistic financial picture, so being prepared for each requirement is key.

Credit Score Expectations

While Bank of America doesn’t publish a minimum credit score, generally, applicants with good to excellent credit (typically FICO scores of 670 or higher) stand the best chance of approval and securing the most favorable rates. A strong credit history demonstrates your reliability as a borrower.

If your credit score is lower, you might still qualify, but expect higher interest rates or potentially a requirement for a larger down payment or a co-signer. Bank of America, like most lenders, uses your credit score to gauge the risk associated with lending to you.

Income Verification

Bank of America needs assurance that you have a stable and sufficient income to comfortably repay the loan. They will require proof of income, which typically includes recent pay stubs, W-2 forms, or tax returns if you are self-employed. The consistency and amount of your income are critical.

Be prepared to provide documentation that clearly reflects your earning potential. Lenders want to see a steady stream of income that can easily cover your proposed monthly car payment, alongside your other financial obligations.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another vital metric. It compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new debt payments, making you a less risky borrower.

While specific DTI limits vary, most lenders prefer a DTI ratio below 36%, though some may go higher depending on other factors. To calculate your DTI, sum all your monthly debt payments (credit cards, student loans, mortgage, etc.) and divide that by your gross monthly income.

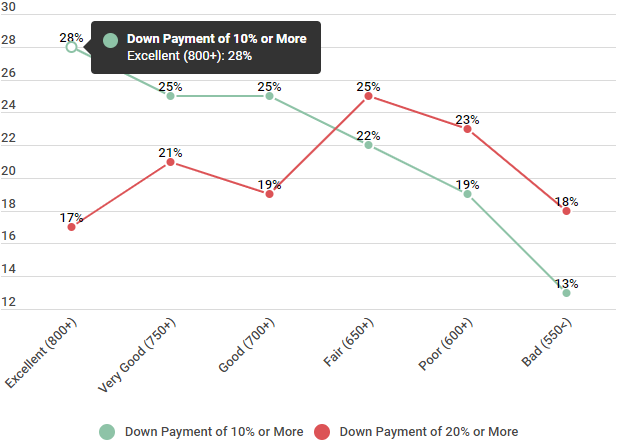

Down Payment Considerations

While not always strictly required, making a down payment significantly improves your chances of approval and can lead to better loan terms. A down payment reduces the loan amount, thereby lowering your monthly payments and the total interest paid over the life of the loan.

It also shows the lender your commitment to the purchase and reduces their risk, as you have immediate equity in the vehicle. Based on my experience, even a modest down payment of 10-20% can make a substantial difference in your loan offer.

Vehicle Eligibility

Bank of America also has specific requirements regarding the vehicle itself. This includes factors like the vehicle’s age, mileage, and type (new vs. used). While they finance both new and used vehicles, the terms for each can differ.

For used vehicles, there might be limits on the maximum age or mileage allowed. Luxury vehicles or highly customized cars might also have different considerations. Ensure the car you are considering meets Bank of America’s eligibility criteria before finalizing your choice.

The Bank of America Car Loan Application Process: Step-by-Step Guide

The journey to securing your vehicle financing with Bank of America is structured and straightforward. Understanding each step helps you navigate the process confidently. This guide will clarify what to expect from your Bank of America auto loan process.

Pro tips from us: Don’t rush through any step. Read all disclosures carefully and ask questions if anything is unclear. Your thoroughness now will prevent future headaches.

Step 1: Get Pre-Approved

Starting with pre-approval is a highly recommended strategy. When you apply for a car loan Bank of America offers a pre-approval option that provides you with an estimated loan amount and interest rate before you even set foot in a dealership. This is typically a "soft inquiry" on your credit, which doesn’t negatively impact your score.

Pre-approval empowers you as a buyer. You’ll know your budget in advance, giving you strong negotiating power with dealers. It also simplifies the car-buying process, as you already have financing secured, allowing you to focus solely on finding the right vehicle.

Step 2: Complete the Full Application

Once you’re ready to proceed, or if you’re skipping pre-approval and applying directly, you’ll complete the full loan application. This can be done conveniently online through Bank of America’s website or by visiting a local branch. The application will ask for detailed personal, financial, and employment information.

Be prepared to provide accurate and comprehensive data, including your full legal name, social security number, current address, employment history, income details, and existing debt obligations. Accuracy is paramount to avoid delays or rejections.

Step 3: Await Decision and Underwriting

After submitting your application, Bank of America’s underwriting team will review your information. This involves a "hard inquiry" on your credit report, which can slightly lower your score temporarily. They will verify your income, employment, and other financial details.

The decision time can vary, but many online applications receive a response within minutes or a few business days. If additional information is needed, a loan officer will contact you. Be responsive to any requests to keep the process moving smoothly.

Step 4: Review Loan Offer & Sign

If approved, Bank of America will present you with a loan offer detailing the loan amount, interest rate (APR), term, and monthly payment. It is crucial to read this offer carefully and understand all the terms and conditions before signing. Pay close attention to the Annual Percentage Rate (APR), which includes the interest rate and any associated fees.

Don’t hesitate to ask questions if any part of the offer is unclear. Once you are satisfied, you will sign the loan agreement, officially committing to the financing terms.

Step 5: Purchase Your Vehicle

With your Bank of America auto loan secured, you can now confidently purchase your vehicle. If you received pre-approval, you’ll simply finalize the purchase with the dealer, providing them with your Bank of America loan details. Bank of America will then work directly with the dealership to disburse the funds.

This streamlined process makes buying a car much smoother, as the financing aspect is already handled. You can drive off the lot knowing your financial arrangements are firmly in place.

Common Mistakes to Avoid When Applying for a Car Loan

Even with thorough preparation, some common pitfalls can derail your Bank of America car loan application. Being aware of these mistakes can help you navigate the process more effectively and avoid unnecessary setbacks. Pro tips from us: Forewarned is forearmed.

1. Not Checking Your Credit Report

One of the most frequent errors is failing to review your credit report before applying. As mentioned, errors can exist, and they can significantly impact your credit score, potentially leading to a higher interest rate or even denial. Always verify your report’s accuracy.

A credit report check also allows you to identify areas for improvement. If you have time before applying, addressing minor issues can boost your score.

2. Applying for Too Many Loans Simultaneously

Each time you apply for a car loan Bank of America or any other lender, a "hard inquiry" is typically placed on your credit report. While one or two inquiries within a short period for the same type of loan are often grouped and treated as a single inquiry (rate shopping), multiple applications spread out over time can lower your score.

This signals to lenders that you might be desperate for credit, which is considered a risk. Focus on one or two strong applications rather than numerous scattered ones.

3. Not Understanding the Loan Terms

Signing a loan agreement without fully comprehending the interest rate, APR, term length, and any associated fees is a major mistake. The APR is the true cost of borrowing, encompassing interest and other charges. A lower interest rate doesn’t always mean a lower APR.

Ensure you understand the total amount you will pay over the life of the loan. Don’t be afraid to ask for clarification on any jargon or clauses you don’t understand.

4. Buying More Car Than You Can Afford

It’s easy to get caught up in the excitement of a new car and stretch your budget. However, overextending yourself financially for a vehicle can lead to payment struggles, missed payments, and even repossession. Always stick to your carefully calculated budget.

Remember that the monthly payment is just one piece of the puzzle. Consider the long-term financial commitment and all associated costs of vehicle ownership.

5. Ignoring the Down Payment

While zero-down loans exist, they often come with higher interest rates and mean you’ll owe more than the car is worth as soon as you drive it off the lot (negative equity). Neglecting a down payment can put you in a vulnerable financial position.

A substantial down payment shows financial responsibility and reduces your loan amount, making it more affordable in the long run. It’s a key factor that can improve your loan terms.

Pro Tips for a Smooth Bank of America Car Loan Experience

Beyond avoiding common mistakes, there are proactive steps you can take to ensure your Bank of America auto loan experience is as smooth and successful as possible. These strategies are born from years of observing successful borrowers.

Improve Your Credit Score Beforehand

If you have a few months before you need a car, focus on improving your credit score. Pay down existing debts, especially high-interest credit card balances. Make all payments on time, every time. Avoid opening new lines of credit. Even a small increase in your score can lead to significantly better loan terms.

Save for a Larger Down Payment

The more you can put down upfront, the less you’ll need to borrow, and the lower your monthly payments will be. A larger down payment also reduces your loan-to-value ratio, making you a more attractive borrower to Bank of America. Aim for 10-20% if possible.

Shop Around for Rates (Even with BoA in Mind)

While you’re set on Bank of America, it’s wise to compare their offer with other lenders. This doesn’t mean applying everywhere, but rather getting a few pre-approvals within a short window (typically 14-45 days) to minimize credit score impact. This allows you to leverage the best offer.

You can visit Bank of America’s official auto loan page for more details on their current offerings and application process: Bank of America Auto Loans (external link).

Consider a Co-Signer (If Necessary)

If your credit isn’t strong enough, or your DTI ratio is high, a co-signer with excellent credit can significantly improve your chances of approval and secure better terms. A co-signer shares responsibility for the loan, so choose someone you trust and who understands the commitment.

Understand Your APR vs. Interest Rate

Remember that the Annual Percentage Rate (APR) is the most accurate measure of the total cost of your loan, as it includes the interest rate plus any fees. Focus on the APR when comparing loan offers, not just the quoted interest rate. This ensures you’re comparing apples to apples.

After Approval: Managing Your Bank of America Car Loan

Securing your loan is a major milestone, but the journey doesn’t end there. Effectively managing your Bank of America vehicle financing is crucial for maintaining good credit and achieving financial success. This final phase focuses on responsible loan management.

Setting Up Payments

Bank of America offers various convenient ways to make your monthly car loan payments. You can typically set up automatic payments from your checking or savings account, ensuring you never miss a due date. This is a highly recommended strategy to avoid late fees and protect your credit score.

Other options usually include online payments through your Bank of America account, payments by mail, or in-person payments at a branch. Choose the method that best suits your lifestyle.

Online Account Management

Utilize Bank of America’s online banking platform or mobile app to manage your car loan account. Here, you can view your payment history, check your remaining balance, and access important loan documents. This digital access provides transparency and control over your financing.

Regularly reviewing your account ensures everything is in order and helps you stay on track with your repayment schedule.

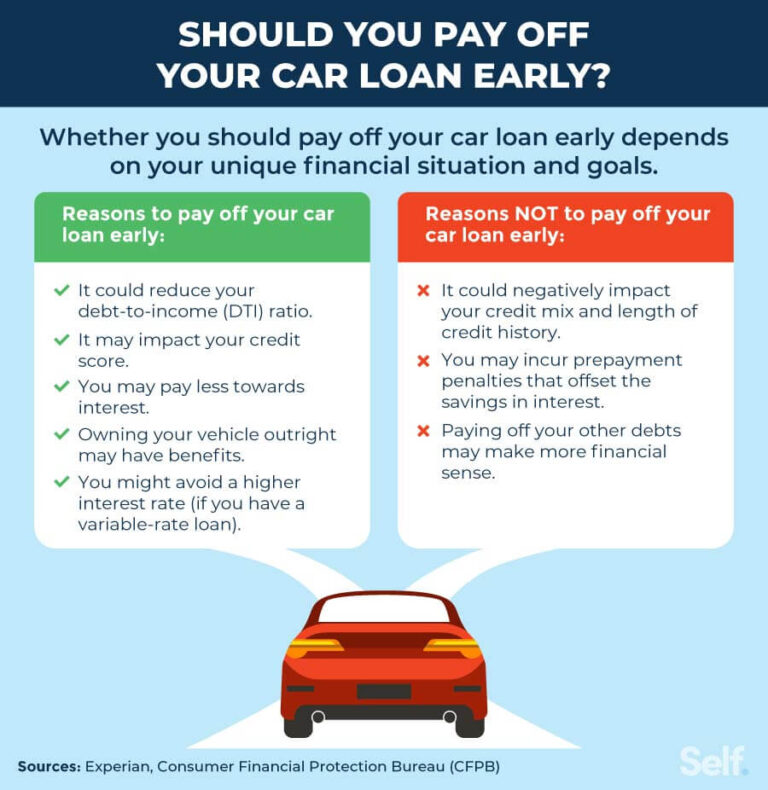

Early Payoff Options

If your financial situation improves, you might consider paying off your car loan early. Most Bank of America auto loans do not have prepayment penalties, meaning you can save on interest by paying more than your minimum monthly payment or making lump-sum payments.

Always confirm with Bank of America if any prepayment penalties apply, though they are uncommon for consumer auto loans. Paying off early can free up cash flow and reduce your overall debt burden.

What If You Miss a Payment?

Life happens, and sometimes a payment might be missed. If you anticipate difficulty making a payment, contact Bank of America immediately. They may offer options like deferment or a temporary payment adjustment, depending on your situation.

Ignoring missed payments can lead to late fees, negative impacts on your credit score, and eventually, repossession of your vehicle. Open communication with your lender is always the best approach.

Frequently Asked Questions (FAQs)

Here are some common questions people ask when they want to apply for a car loan Bank of America.

Q1: How long does Bank of America car loan approval take?

A1: Many applicants receive an instant decision when applying online. However, if additional documentation or review is required, it can take a few business days. Pre-approval typically provides a quick response.

Q2: Can I get a car loan with bad credit from Bank of America?

A2: While Bank of America prefers applicants with good credit, they may consider those with less-than-perfect credit. However, you might face higher interest rates, require a larger down payment, or need a co-signer to qualify. It’s always best to improve your credit score first.

Q3: What’s the minimum loan amount for a Bank of America auto loan?

A3: Bank of America typically has a minimum loan amount, which can vary. It’s usually around $7,500, but it’s best to check their official website or speak with a loan officer for the most current information.

Q4: Does Bank of America finance used cars?

A4: Yes, Bank of America provides financing for both new and used vehicles. They often have specific requirements for used cars, such as age and mileage limits, so ensure your chosen vehicle meets these criteria.

Conclusion: Your Journey to a Bank of America Car Loan

Applying for a car loan, especially with a reputable institution like Bank of America, can be a smooth and rewarding experience when approached with preparation and knowledge. By understanding your credit, setting a realistic budget, and meticulously navigating the Bank of America car loan application process, you significantly enhance your chances of securing favorable terms.

Remember, the goal is not just to get approved, but to get approved for a loan that genuinely fits your financial life. With the insights provided in this comprehensive guide, you are now well-equipped to drive forward confidently. Start your journey today and make that dream car a reality with Bank of America financing.