Drive Your Dream: The Ultimate Guide to Axis Bank Car Loans

Drive Your Dream: The Ultimate Guide to Axis Bank Car Loans Carloan.Guidemechanic.com

The dream of owning a car is a shared aspiration for many. Whether it’s the freedom of hitting the open road, the convenience of daily commutes, or the joy of family road trips, a personal vehicle offers unparalleled independence. However, turning that dream into a reality often requires navigating the world of vehicle financing. This is where a reliable partner like Axis Bank comes into play, offering robust car loan solutions designed to make your journey smoother.

As expert bloggers and professional SEO content writers, we understand the importance of making informed financial decisions. In this comprehensive guide, we will delve deep into everything you need to know about Axis Bank Car Loans. Our goal is to provide you with unique insights, demystify complex terms, and equip you with the knowledge to secure the best possible financing for your next car. Let’s embark on this journey together to unlock the full potential of Axis Bank’s offerings.

Drive Your Dream: The Ultimate Guide to Axis Bank Car Loans

Why Choose Axis Bank for Your Car Loan? Unpacking the Benefits

When considering a car loan, the sheer number of options can feel overwhelming. However, Axis Bank consistently stands out for several compelling reasons. Their approach to vehicle financing is centered around customer convenience, competitive offerings, and transparency, making them a preferred choice for many aspiring car owners.

Competitive Interest Rates Tailored for You

One of the most significant factors in any loan decision is the interest rate. Axis Bank prides itself on offering attractive and competitive interest rates on its car loans. These rates are not one-size-fits-all; instead, they are often tailored based on various factors, including your credit score, loan amount, and repayment tenure.

Based on my experience in the financial sector, a favorable interest rate can significantly reduce your total cost of ownership over the loan term. Axis Bank aims to provide rates that are not only competitive but also transparent, ensuring you understand exactly what you’re committing to from the outset.

Flexible Repayment Options for Financial Comfort

Life is unpredictable, and so are financial situations. Axis Bank understands this, offering a wide range of flexible repayment tenures for their car loans. You can choose a tenure that aligns perfectly with your financial comfort and monthly budget.

Whether you prefer a shorter tenure with higher EMIs to become debt-free sooner, or a longer tenure with lower EMIs to ease your monthly burden, Axis Bank provides options. This flexibility is a crucial benefit, allowing you to manage your finances effectively without undue stress.

Quick and Seamless Approval Process

Time is often of the essence when you’ve found your dream car. Axis Bank is renowned for its streamlined and quick car loan approval process. They have invested heavily in technology and efficient workflows to ensure that your application moves swiftly from submission to disbursal.

Pro tips from us: Having all your documents in order before applying can significantly speed up this process. A prompt approval means you can drive home your new car without unnecessary delays, making the entire experience more enjoyable.

Minimal Documentation Requirements

Often, applying for a loan can feel like drowning in paperwork. Axis Bank strives to simplify this by keeping its documentation requirements minimal and straightforward. They aim to reduce the hassle, asking only for the essential papers needed for verification and regulatory compliance.

This focus on minimal documentation not only saves you time but also reduces the potential for errors or omissions that could delay your application. It’s a testament to their customer-centric approach, prioritizing ease of application.

Transparent Policies and No Hidden Charges

Transparency is a cornerstone of trust in financial dealings. Axis Bank is committed to maintaining clear and transparent policies regarding their car loans. Every fee, charge, and condition is typically laid out clearly, ensuring there are no unpleasant surprises later on.

Common mistakes to avoid are not reading the fine print. With Axis Bank, you can generally expect a clear breakdown of processing fees, pre-payment charges (if any), and other associated costs, allowing you to make a decision with complete clarity.

Excellent Customer Service and Support

Even with a smooth process, questions or concerns can arise. Axis Bank provides robust customer service and support for its car loan applicants and existing customers. Their dedicated team is available to assist you through various channels, from in-branch support to online and phone assistance.

This readily available support ensures that any queries you have, whether about eligibility, documents, or repayment schedules, are addressed promptly and efficiently. A reliable support system adds significant value, especially during a major financial commitment like a car loan.

Eligibility Criteria for an Axis Bank Car Loan: Are You Ready?

Understanding the eligibility criteria is the first crucial step before applying for any loan. Axis Bank has specific requirements to ensure that applicants can comfortably manage their repayment obligations. Meeting these criteria is key to a successful car loan application.

Age Requirements: A Broad Spectrum

Axis Bank typically sets an age bracket for car loan applicants. Generally, applicants should be a minimum of 21 years old at the time of application. The maximum age for loan maturity is often around 70 years, ensuring that the repayment period falls within a productive age bracket.

This broad age spectrum allows a wide range of individuals, from young professionals to those nearing retirement, to apply for a car loan. It reflects Axis Bank’s commitment to inclusive financial services for diverse customer segments.

Income Stability: Salaried vs. Self-Employed

Your income stability is a primary indicator of your repayment capacity. Axis Bank assesses this differently for salaried individuals and self-employed professionals or business owners.

- For Salaried Individuals: You will generally need to demonstrate a stable employment history and a minimum net annual income. This typically involves submitting salary slips, bank statements showing salary credits, and potentially employment verification.

- For Self-Employed Individuals/Business Owners: The focus shifts to the stability and profitability of your business or profession. You’ll likely need to provide Income Tax Returns (ITRs), profit and loss statements, balance sheets, and bank statements showing business transactions.

The bank looks for consistent income generation, indicating your ability to make regular EMI payments without strain.

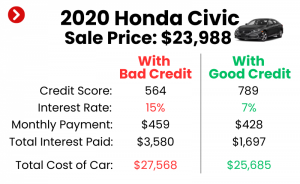

The Indispensable Role of Your Credit Score

Based on my experience as a financial analyst, your credit score is arguably the most critical factor in loan eligibility and interest rate determination. A high credit score (typically above 750) signals to Axis Bank that you are a responsible borrower with a strong repayment history.

A good credit score can unlock better interest rates and a smoother approval process for your Axis Bank Car Loan. Conversely, a low score might lead to higher interest rates or even rejection. For more detailed insights on improving your credit score, you might find our article, "Understanding Your Credit Score: A Comprehensive Guide" (internal link placeholder), very helpful.

Employment Stability: A Sign of Reliability

Beyond just income, Axis Bank also considers your employment stability. For salaried individuals, this means consistent employment with your current organization for a certain period (e.g., 1-2 years). For self-employed individuals, it pertains to the longevity and stability of your business.

A stable employment history or a well-established business reassures the bank of your long-term financial capacity. It indicates a lower risk of default, making you a more attractive borrower.

Documents Required for Your Application: Get Ready!

Gathering the necessary documents beforehand can significantly accelerate your Axis Bank Car Loan application. While the exact list might vary slightly based on your profile and the specific car loan product, here’s a general overview of what you’ll typically need.

Proof of Identity: Who You Are

To verify your identity, Axis Bank will require one or more of the following:

- Passport

- PAN Card

- Aadhar Card

- Driving License

- Voter ID

Ensuring your chosen document is valid and up-to-date is crucial to avoid any delays.

Proof of Address: Where You Live

To confirm your residential address, you’ll generally need to provide:

- Aadhar Card

- Driving License

- Passport

- Utility bills (electricity, water, gas – not older than 2-3 months)

- Rent agreement (if applicable)

Consistency between your identity and address proofs is important for a smooth verification process.

Proof of Income: Your Financial Capacity

This is a critical section, as it demonstrates your ability to repay the loan.

- For Salaried Individuals:

- Latest 3 months’ salary slips

- Latest 6 months’ bank statements (showing salary credits)

- Latest Form 16 or Income Tax Returns (ITR) for the last 1-2 years

- For Self-Employed Individuals/Business Owners:

- Latest 2-3 years’ ITR with computation of income

- Audited balance sheet and profit & loss account for the last 2-3 years

- Latest 6 months’ bank statements (personal and business)

- Proof of business existence (e.g., Shop & Establishment Act certificate, GST registration)

Having these financial documents organized and readily available will make the income verification process seamless.

Bank Statements: A Glimpse into Your Finances

Beyond just income credits, Axis Bank will typically request your bank statements (usually for the last 6 months) to assess your spending habits, existing EMIs, and overall financial health. This helps them understand your cash flow and ensure you’re not over-leveraged.

Vehicle-Related Documents (Post-Approval)

Once your loan is sanctioned, you’ll also need documents related to the vehicle itself, such as:

- Proforma Invoice/Quotation from the car dealer

- Registration Certificate (RC) copy (for used cars)

- Insurance papers

Pro-tip: Start gathering these vehicle documents as soon as you finalize your car choice. This proactive approach ensures there are no last-minute holdups in the disbursal process.

The Axis Bank Car Loan Application Process: A Step-by-Step Guide

Applying for an Axis Bank Car Loan is a structured process designed for efficiency. Understanding each step can help you navigate it confidently and ensure a smooth experience.

Step 1: Research and Pre-Qualification

Before formally applying, it’s wise to research the specific Axis Bank Car Loan products. Use their online EMI calculators to understand potential monthly payments based on different loan amounts, interest rates, and tenures. You can also check your basic eligibility online.

Step 2: Application Submission

You have several convenient ways to apply:

- Online Application: Visit the official Axis Bank website and fill out the online car loan application form. This is often the quickest way to initiate the process.

- Branch Visit: Head to your nearest Axis Bank branch, where a loan officer can guide you through the application process and answer any questions.

- Dealer Tie-ups: Many car dealerships have tie-ups with Axis Bank. You can apply directly through the dealership’s finance desk.

Step 3: Document Submission

Once your application is submitted, you’ll be required to provide all the necessary documents as outlined in the previous section. If applying online, you might be able to upload scanned copies. If at a branch or dealership, physical copies or originals for verification will be needed.

Common mistakes to avoid are submitting incomplete or outdated documents. Double-check everything before submission to prevent delays.

Step 4: Verification Process

Axis Bank’s team will then verify the information and documents you’ve provided. This might include:

- Credit Score Check: Your CIBIL or other credit bureau score will be pulled.

- Document Verification: Authenticity of your identity, address, and income proofs will be checked.

- Tele-verification/Field Investigation: In some cases, a bank representative might contact you or even visit your residence/workplace for further verification.

Step 5: Loan Sanction and Offer Letter

If all verifications are satisfactory and you meet the eligibility criteria, Axis Bank will sanction your car loan. You will receive an offer letter detailing the sanctioned loan amount, interest rate, tenure, EMI amount, and all terms and conditions.

Carefully review this offer letter. It’s your official agreement, and understanding every clause is paramount.

Step 6: Loan Disbursal

Once you accept the offer letter and complete any remaining formalities (like signing the loan agreement and hypothecation deed), the loan amount will be disbursed. For new cars, this is usually directly to the car dealership. For used cars, it might be to the seller or directly to your account, depending on the arrangement.

Congratulations! At this stage, your dream car is officially financed, and you’re ready to drive it home.

Understanding Axis Bank Car Loan Interest Rates

The interest rate on your Axis Bank Car Loan significantly impacts the total cost of your vehicle. It’s not just a number; it’s a reflection of various financial factors.

Factors Influencing Your Interest Rate

Several key elements determine the interest rate Axis Bank offers you:

- Credit Score: As mentioned, a higher credit score (indicating lower risk) typically qualifies you for lower interest rates.

- Loan Amount and Tenure: Larger loan amounts or longer tenures might sometimes influence rates, though this varies.

- Applicant’s Profile: Your income stability, employment type (salaried vs. self-employed), and relationship with Axis Bank can play a role.

- Type of Car: New car loans often have slightly lower rates than used car loans due to perceived lower risk.

- Market Conditions: General economic conditions and the Reserve Bank of India’s (RBI) policies also influence lending rates across the board.

Fixed vs. Floating Rates: Which is Better?

Axis Bank typically offers car loans with a fixed interest rate.

- Fixed Interest Rate: The interest rate remains constant throughout the entire loan tenure. Your EMI amount will not change.

- Benefit: Provides predictability and stability. You know exactly what your monthly outflow will be, making budgeting easier.

- Consideration: You won’t benefit if market interest rates fall, but you’re also protected if they rise.

Based on my experience, for personal car loans, a fixed interest rate is generally preferred by most borrowers because it offers peace of mind and simplifies financial planning. It removes the uncertainty of fluctuating EMIs.

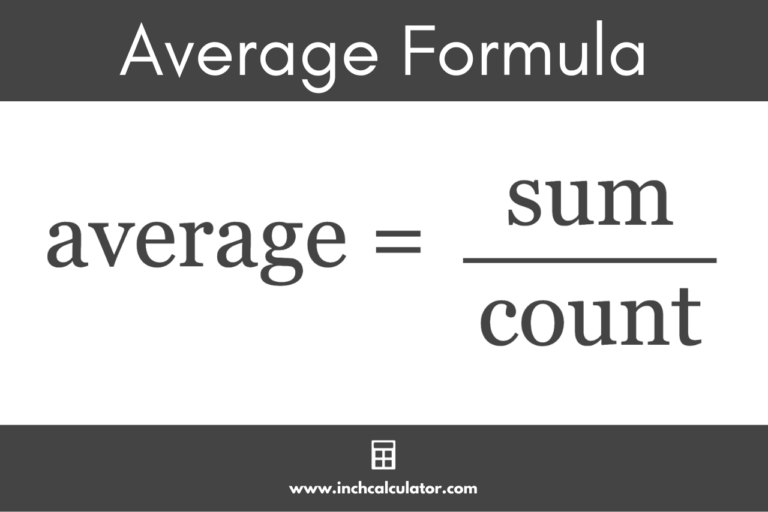

EMI Calculation and Repayment Strategies

EMI, or Equated Monthly Installment, is the fixed amount you pay to the bank each month until your loan is fully repaid. It comprises both the principal loan amount and the interest accrued.

How EMI is Calculated

Axis Bank, like other lenders, uses a standard formula to calculate EMI:

EMI = /

Where:

- P = Principal Loan Amount

- R = Monthly Interest Rate (Annual Rate / 12 / 100)

- N = Loan Tenure in Months

While understanding the formula is useful, Axis Bank’s website and various online financial portals offer user-friendly EMI calculators. These tools allow you to input different loan amounts, interest rates, and tenures to instantly see your potential EMI.

Strategies for Comfortable Repayment

Effective repayment strategies can help you manage your Axis Bank Car Loan without financial strain:

- Choose the Right Tenure: Opt for a tenure that provides a manageable EMI without extending the loan unnecessarily. A longer tenure means lower EMIs but higher total interest paid.

- Automate Payments: Set up an auto-debit facility from your Axis Bank account to ensure EMIs are paid on time, avoiding late payment penalties and protecting your credit score.

- Budgeting: Incorporate your car loan EMI into your monthly budget to ensure you have sufficient funds available.

- Pre-payment Considerations: If you have surplus funds, consider pre-paying a part of your loan. This can significantly reduce the total interest burden over time.

Pre-payment and Foreclosure: What You Need to Know

Understanding pre-payment and foreclosure options is vital for any borrower. These terms relate to paying off your loan earlier than the scheduled tenure.

Pre-payment: Paying Extra Towards Your Principal

Pre-payment refers to paying a lump sum amount towards your outstanding principal balance before your regular EMI due date, or in addition to your EMI.

- Benefits of Pre-payment:

- Reduced Interest Burden: Every rupee you pre-pay goes directly towards reducing your principal, which in turn reduces the total interest you pay over the loan tenure.

- Shorter Loan Tenure: Consistent pre-payments can lead to a significant reduction in your loan tenure, allowing you to become debt-free sooner.

- Financial Flexibility: Freeing up your monthly EMI commitment provides more financial flexibility for other investments or expenses.

Associated Charges (Pre-payment Penalties)

Pro tips from us: While pre-payment is generally beneficial, some banks might levy a pre-payment penalty or charge. This is a fee for closing the loan earlier than expected, compensating the bank for the loss of future interest income.

Axis Bank’s specific policies on pre-payment charges should be clearly outlined in your loan agreement. It’s crucial to review these terms before making any pre-payments to ensure the benefits outweigh the charges. Often, after a certain lock-in period, these charges might be waived or reduced.

Foreclosure: Closing Your Loan Completely

Foreclosure means paying off the entire outstanding principal amount of your Axis Bank Car Loan in one go, thereby closing the loan account completely before its original tenure ends.

- Foreclosure Process: You’ll need to contact Axis Bank to get the exact foreclosure amount, which includes the outstanding principal, any accrued interest up to the foreclosure date, and any applicable foreclosure charges. Once paid, the bank will issue a No Objection Certificate (NOC) and release the hypothecation on your vehicle.

- Implications: Foreclosing your loan frees you from EMI obligations and gives you full ownership of your car. However, like pre-payment, it may involve foreclosure charges as per your loan agreement.

Axis Bank Car Loans for Different Needs

Axis Bank understands that car ownership dreams come in various forms. They offer financing solutions tailored to different requirements.

New Car Loans: Driving Home a Brand New Ride

Axis Bank’s new car loans are designed for individuals looking to purchase a brand-new vehicle directly from a dealership. These loans typically offer:

- Higher Loan-to-Value (LTV): You can often finance a significant portion (up to 80-90% or even more for certain models/customers) of the car’s on-road price.

- Lower Interest Rates: New car loans generally come with more attractive interest rates compared to used car loans, as new vehicles are considered lower risk.

- Longer Tenures: Repayment tenures can extend up to 7 years, making EMIs more affordable.

This is the most common and straightforward car loan product offered by the bank.

Used Car Loans: Affordable Access to Quality Vehicles

For those who prefer the value proposition of a pre-owned vehicle, Axis Bank also offers used car loans. These loans allow you to finance the purchase of a second-hand car.

- Specific Considerations:

- Vehicle Age Restriction: There might be limitations on the maximum age of the used car at the time of loan application (e.g., not older than 5 years).

- Lower LTV: The loan-to-value ratio might be slightly lower than for new cars, meaning you might need a larger down payment.

- Slightly Higher Interest Rates: Due to the higher perceived risk associated with older vehicles, interest rates on used car loans are typically a bit higher than new car loans.

- Shorter Tenure: Repayment tenures might also be shorter (e.g., up to 5 years) compared to new car loans.

Choosing between a new and used car loan is a personal decision based on budget and preference. You might find our article, "Choosing Between New vs. Used Car Loans: What’s Right for You?" (internal link placeholder), helpful in making this choice.

Tips for a Smooth Axis Bank Car Loan Journey

Securing an Axis Bank Car Loan can be a seamless experience if you approach it strategically. Here are some pro tips to ensure your journey is smooth and successful.

Maintain a Stellar Credit Score

As repeatedly emphasized, your credit score is your financial passport. Regularly check your credit report for errors and strive to maintain a score above 750. Pay all your bills on time, keep credit utilization low, and avoid applying for multiple loans simultaneously. A good score will open doors to better rates and faster approvals.

Research Thoroughly Before You Apply

Don’t rush into an application. Take the time to understand the different car loan products offered by Axis Bank. Compare interest rates, processing fees, and other charges. Use online calculators to estimate your EMIs for various scenarios. Informed decisions are always the best decisions.

Understand All Terms and Conditions

Before signing any document, meticulously read and understand the entire loan agreement. Pay close attention to interest rates, repayment tenure, EMI schedule, processing fees, pre-payment penalties, foreclosure charges, and any other clauses. If anything is unclear, do not hesitate to ask for clarification from the bank representative.

Don’t Over-Leverage Yourself

Common mistakes to avoid are borrowing more than you can comfortably repay. While it’s tempting to get the most expensive car you desire, ensure your EMI fits comfortably within your monthly budget. A good rule of thumb is that your total EMI commitments (including your car loan) should not exceed 30-40% of your net monthly income.

Keep Your Documents Organized

Having all required documents neatly organized and readily accessible can significantly expedite the application process. Create a checklist and tick off each document as you gather it. This prevents last-minute scrambling and potential delays.

Common Myths About Car Loans Debunked

The world of finance is often riddled with misconceptions. Let’s clear up some common myths surrounding car loans, especially when considering an Axis Bank Car Loan.

Myth 1: A Low Interest Rate is the Only Factor That Matters.

While a low interest rate is highly desirable, it’s not the only factor to consider. Processing fees, pre-payment penalties, and the overall transparency of the loan agreement are equally important. A slightly higher interest rate with no hidden charges and excellent customer service might be more beneficial than a rock-bottom rate laden with hidden fees. Always look at the total cost of the loan.

Myth 2: Car Loans Are Only for Brand New Vehicles.

This is a widespread misconception. As we’ve discussed, Axis Bank, like many leading financial institutions, offers robust used car loan options. These cater to a significant market segment looking for more affordable vehicle ownership without compromising on quality or reliability.

Myth 3: Pre-payment is Always Free and Beneficial.

While pre-payment is generally beneficial in reducing your overall interest burden, it’s not always free. Many loan agreements, including some car loans, might have pre-payment or foreclosure charges, especially if you pay off the loan within a short period after disbursal. Always check your loan agreement for these specific clauses before making a pre-payment.

Myth 4: You Need a Huge Down Payment to Get a Car Loan.

While a larger down payment can reduce your loan amount and thus your EMI, it’s not always "huge" or mandatory. Axis Bank offers high loan-to-value ratios, meaning you can finance a significant portion of the car’s cost. The exact down payment depends on your eligibility, the car’s price, and the bank’s specific offering.

Conclusion: Your Road to Car Ownership with Axis Bank

Embarking on the journey of car ownership is an exciting prospect, and securing the right financing is a critical step. An Axis Bank Car Loan offers a compelling blend of competitive interest rates, flexible repayment options, a streamlined application process, and transparent policies. Their commitment to customer satisfaction makes them a strong partner in turning your automotive dreams into a tangible reality.

By understanding the eligibility criteria, preparing your documents, navigating the application process, and being aware of the nuances of interest rates and repayment strategies, you can confidently secure a car loan that fits your financial landscape. Remember to always prioritize financial prudence, maintain a healthy credit score, and meticulously review all terms and conditions.

Don’t let the complexities of financing deter you. With the insights provided in this comprehensive guide, you are now well-equipped to make an informed decision and drive home your dream car with an Axis Bank Car Loan. Your journey towards vehicle ownership starts here – happy driving!

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Readers are advised to consult with a financial advisor and refer to the official Axis Bank website or a bank representative for the most current and accurate information regarding car loan products, eligibility, terms, and conditions.

External Link: For the most up-to-date information directly from the source, please visit the official Axis Bank Car Loan page: https://www.axisbank.com/retail-banking/loans/car-loan