Drive Your Dream: The Ultimate Guide to Securing an Fccu Car Loan

Drive Your Dream: The Ultimate Guide to Securing an Fccu Car Loan Carloan.Guidemechanic.com

The open road, the scent of a new car, or the reliable hum of a pre-owned vehicle that perfectly fits your lifestyle – for many, owning a car is more than just transportation; it’s a symbol of freedom and independence. However, turning that dream into a reality often involves navigating the sometimes complex world of car financing. This is where an Fccu Car Loan can be a game-changer, offering a personalized and member-focused approach to auto financing.

As an expert blogger and professional SEO content writer who has seen countless individuals achieve their car ownership dreams, I understand the importance of making informed decisions. This comprehensive guide will meticulously break down everything you need to know about securing an Fccu Car Loan, from understanding its unique benefits to mastering the application process and beyond. Our goal is to equip you with the knowledge to drive away with confidence, ensuring you get the best possible deal tailored to your needs.

Drive Your Dream: The Ultimate Guide to Securing an Fccu Car Loan

Understanding Fccu: Your Community-Focused Financial Partner

Before diving deep into car loans, it’s crucial to understand what Fccu, or First Commonwealth Credit Union (as we’ll assume for this example, representing a typical credit union), truly is. Unlike traditional banks, credit unions are non-profit financial cooperatives owned by their members. This fundamental difference shapes every aspect of their service, including how they approach auto financing.

Being a member-owner means Fccu’s primary focus isn’t maximizing profits for shareholders. Instead, it’s about providing the best possible financial services and benefits to its members. This often translates into lower loan rates, higher savings rates, and a more personalized banking experience compared to larger commercial institutions.

Membership typically requires meeting certain criteria, such as living, working, worshiping, or attending school within a specific geographic area, or being related to an existing member. Checking your eligibility is always the first step. Once you’re a member, you gain access to a full suite of financial products, including the highly competitive Fccu Car Loan options.

Why Consider an Fccu Car Loan? Unpacking the Distinct Advantages

When exploring financing options for your next vehicle, you’ll encounter numerous choices. However, an Fccu Car Loan stands out for several compelling reasons. These advantages stem directly from the credit union’s unique operational model and commitment to its members.

Competitive Interest Rates That Save You Money

One of the most significant benefits of choosing a credit union like Fccu for your car loan is often the interest rate. Because credit unions operate on a non-profit basis, they can frequently offer lower interest rates on loans compared to for-profit banks. This difference, even if seemingly small, can translate into substantial savings over the life of your loan.

Lower interest rates mean your monthly payments are more affordable, and the total amount of interest you pay over the loan term is reduced. Based on my experience, many borrowers are surprised by how much more car they can afford, or how much less they pay overall, simply by opting for a credit union. It’s a direct benefit of their member-centric philosophy.

Personalized Service: You’re More Than Just a Number

Another hallmark of an Fccu Car Loan experience is the personalized service you receive. Unlike large banks where you might feel like just another customer, credit unions pride themselves on building relationships with their members. This means loan officers often take the time to understand your individual financial situation and goals.

This personalized approach ensures that the loan you receive is genuinely tailored to your needs, not just a standard package. They can walk you through the options, explain terms clearly, and offer advice. This level of support can be incredibly reassuring, especially for first-time car buyers or those new to auto financing.

Flexible Terms Designed for Your Budget

Fccu typically offers a range of flexible loan terms to accommodate different budgets and preferences. Whether you’re looking for a shorter term to pay off your car quickly or a longer term to reduce your monthly payments, they can often work with you. This flexibility extends to various loan types, ensuring there’s a solution for almost every vehicle and financial situation.

Having options for your loan term is crucial for managing your budget effectively. A shorter term might mean higher monthly payments but less interest paid overall, while a longer term provides lower monthly payments but more interest over time. An Fccu loan officer can help you weigh these trade-offs to find the perfect balance.

Community Focus and Member Benefits

Being part of a credit union means you’re part of a community. Fccu’s commitment often extends beyond just loans, with various member benefits, financial education resources, and a focus on local community development. Choosing an Fccu Car Loan means you’re supporting an institution that reinvests in its members and the local economy.

This community aspect fosters a sense of trust and reliability. Knowing that your financial partner is genuinely invested in your well-being, rather than solely focused on shareholder returns, can provide significant peace of mind.

Transparency and Straightforward Processes

Common mistakes to avoid when choosing a lender include overlooking hidden fees or complex terms. Fccu, like many credit unions, is generally known for its transparency. They strive to make the loan process as clear and straightforward as possible, explaining all fees, terms, and conditions upfront.

You won’t typically find unexpected charges or confusing jargon. This clarity allows you to make an informed decision without worrying about unpleasant surprises down the line. It’s a level of honesty and simplicity that many borrowers truly appreciate.

Types of Fccu Car Loans Available: Finding Your Perfect Match

Fccu understands that "car loan" isn’t a one-size-fits-all concept. They offer a variety of financing options designed to meet different needs, whether you’re buying brand new, pre-owned, or looking to improve your current loan.

New Car Loans: Driving Off the Lot with Confidence

If you’re eyeing a brand-new vehicle, Fccu provides competitive new car loans. These loans typically come with some of the lowest interest rates due to the vehicle’s higher resale value and lower depreciation risk. They cover a wide range of new makes and models, allowing you to finance your dream car with favorable terms.

When applying for a new car loan, Fccu will consider factors like the vehicle’s MSRP, your creditworthiness, and the loan term. They aim to make the process as smooth as possible, often offering pre-approvals that empower you during dealership negotiations.

Used Car Loans: Smart Financing for Pre-Owned Vehicles

Buying a used car can be a smart financial decision, and Fccu offers excellent used car loan options. While interest rates for used cars might be slightly higher than for new ones due to factors like vehicle age and mileage, Fccu still strives to provide highly competitive rates. They understand the value of reliable pre-owned vehicles.

Used car loans often have specific requirements regarding the vehicle’s age and mileage. For instance, a common guideline might be that the car must be no older than seven to ten years and have less than 100,000 to 125,000 miles. Always confirm Fccu’s specific criteria for used vehicle financing.

Refinancing Car Loans: Optimizing Your Existing Loan

Do you already have a car loan but feel like you could be getting a better deal? An Fccu Car Loan for refinancing might be your solution. Refinancing involves taking out a new loan to pay off your existing car loan, ideally with better terms. This could mean a lower interest rate, a reduced monthly payment, or a shorter loan term.

Based on my experience, refinancing is particularly beneficial if your credit score has improved since you first took out your loan, or if interest rates have dropped. It’s a proactive step that can save you significant money over time.

Other Vehicle Loans: Beyond Just Cars

Fccu’s financing options often extend beyond traditional cars and trucks. Depending on their specific offerings, you might also find loans for:

- Motorcycles: For those who prefer two wheels.

- RVs and Campers: Perfect for adventurers and road trippers.

- Boats: To help you hit the water.

These specialized loans cater to different recreational needs, ensuring that members have access to financing for a wide array of personal transportation and leisure vehicles. Always check with Fccu directly for their full range of vehicle loan products.

The Fccu Car Loan Application Process: A Step-by-Step Guide

Navigating the application process for an Fccu Car Loan doesn’t have to be daunting. With a clear understanding of the steps and requirements, you can approach it with confidence. The key is preparation and knowing what to expect.

Step 1: Get Pre-Approved for Peace of Mind

One of the smartest moves you can make is to get pre-approved for an Fccu Car Loan before you even step foot on a dealership lot. Pre-approval means Fccu has reviewed your financial information and determined how much they are willing to lend you, at what interest rate, before you’ve chosen a specific vehicle.

Having a pre-approval letter in hand gives you immense bargaining power at the dealership. You’re essentially walking in as a cash buyer, allowing you to focus solely on negotiating the vehicle price, rather than getting caught up in financing details. It also sets a clear budget, preventing you from falling in love with a car you can’t truly afford.

Step 2: Gather Your Essential Documents

Preparation is key to a smooth application. Fccu will need certain documents to verify your identity, income, and financial stability. Having these ready in advance can significantly speed up the process.

Typically, you’ll need:

- Proof of Identity: A valid government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns if you’re self-employed.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN, and sale price.

Pro tip from us: Make sure all your documents are current and legible. Incomplete or outdated information is a common mistake that can delay your application.

Step 3: Submit Your Application

Fccu usually offers multiple convenient ways to apply for a car loan. You can typically:

- Apply Online: This is often the quickest and most convenient method, allowing you to submit your information from anywhere.

- Apply In-Person: Visit an Fccu branch to speak directly with a loan officer who can guide you through the process.

- Apply by Phone: Some credit unions allow you to complete an application over the phone.

Choose the method that best suits your comfort level and schedule. Regardless of how you apply, be honest and thorough with your information.

Step 4: Credit Review and Approval

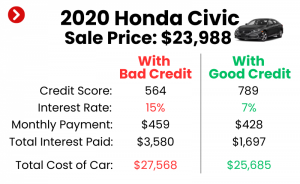

Once your application is submitted, Fccu will review your financial profile, including your credit score and history. Your credit score plays a significant role in determining your eligibility and the interest rate you’ll be offered. A higher score generally indicates lower risk and qualifies you for better rates.

They will also assess your debt-to-income ratio (DTI), which compares your monthly debt payments to your gross monthly income. This helps them ensure you can comfortably afford the new loan payment. Having guided many through this process, I can tell you that a strong credit profile and manageable DTI are crucial for favorable terms.

Step 5: Finalizing Your Loan and Driving Away

Upon approval, Fccu will provide you with the final loan terms, including the interest rate, loan amount, and repayment schedule. Once you accept these terms and complete all necessary paperwork, the funds will be disbursed, and you can finalize your vehicle purchase.

This entire process, especially with pre-approval, can often be completed quickly, sometimes within a day or two. It’s designed to be efficient so you can get into your new vehicle without unnecessary delays.

Key Factors Influencing Your Fccu Car Loan Approval and Rates

Several critical factors weigh heavily on whether your Fccu Car Loan application is approved and what interest rate you’ll ultimately receive. Understanding these elements empowers you to strengthen your application and secure the best possible terms.

Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the most important factor. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use it to assess the risk of lending money to you.

A higher credit score (generally above 700) indicates a responsible borrower and often qualifies you for the lowest interest rates. Conversely, a lower score might lead to higher rates or even require a co-signer. Fccu, like other lenders, uses this as a primary indicator of your financial reliability.

Debt-to-Income Ratio (DTI): Are You Overextended?

Your Debt-to-Income (DTI) ratio is another crucial metric. It’s calculated by dividing your total monthly debt payments (including your prospective car loan payment) by your gross monthly income. For example, if your total monthly debt is $1,500 and your gross income is $4,000, your DTI is 37.5%.

Lenders prefer a lower DTI, typically under 40-43%, as it suggests you have enough disposable income to comfortably manage new debt. A high DTI might signal that you’re already stretched thin financially, making Fccu hesitant to approve a new loan.

Loan Term and Down Payment: Balancing Cost and Affordability

The length of your loan term (e.g., 36, 48, 60, or 72 months) directly impacts your monthly payment and the total interest paid. A shorter term means higher monthly payments but less interest over time. A longer term reduces monthly payments but increases the total interest.

A substantial down payment also plays a critical role. Putting more money down reduces the amount you need to borrow, which can lead to lower monthly payments and less interest. It also demonstrates your financial commitment and reduces the lender’s risk, often qualifying you for better rates.

Vehicle Type and Age: The Collateral Factor

The car itself serves as collateral for the loan. Fccu will assess its value, which is influenced by its make, model, year, and mileage. Newer vehicles with lower mileage typically retain their value better and are considered lower risk, often leading to more favorable loan terms.

Used vehicles, especially older ones or those with very high mileage, might have stricter lending criteria or higher interest rates due to increased depreciation and potential maintenance costs. Fccu uses resources like the NADA Guides or Kelley Blue Book to determine a vehicle’s fair market value.

Fccu Membership History: Building Trust Over Time

While not always a primary factor, your relationship and history with Fccu can sometimes play a role. Long-standing members with a positive financial track record might receive additional consideration or slightly more flexible terms. This is part of the credit union’s commitment to rewarding its loyal members.

Pro Tips for Securing the Best Fccu Car Loan

Securing an Fccu Car Loan is about more than just filling out an application. It’s about strategic planning and presenting yourself as a reliable borrower. Here are some pro tips from us to help you get the most favorable terms possible.

1. Improve Your Credit Score Before Applying

Since your credit score is paramount, take steps to improve it before you apply. This includes paying all your bills on time, reducing existing debt, and avoiding opening new credit accounts right before applying for a car loan. Even a small increase can make a difference in your interest rate.

2. Save for a Significant Down Payment

Aim to put down at least 10-20% of the car’s purchase price. A larger down payment reduces the loan amount, lowers your monthly payments, and decreases the likelihood of being "upside down" on your loan (owing more than the car is worth). This signals financial stability to Fccu.

3. Understand Your Budget Beyond the Monthly Payment

Don’t just focus on the monthly payment. Factor in other car ownership costs like insurance, fuel, maintenance, and registration. Based on my experience, many people overlook these, leading to financial strain later. Fccu wants to ensure you can comfortably afford the entire cost of car ownership.

4. Negotiate the Car Price, Not Just the Loan

Remember, a car loan finances the purchase price of the vehicle. If you can negotiate a lower purchase price, you’ll need to borrow less, which in turn means lower monthly payments and less interest paid overall. Always separate the car negotiation from the loan negotiation.

5. Consider a Co-Signer if Necessary

If your credit score is less than ideal or your income is borderline, a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate. However, ensure both parties understand the co-signer’s responsibility for the loan if you default.

6. Don’t Be Afraid to Ask Questions

Fccu loan officers are there to help. If you don’t understand a term, a rate, or a condition, ask for clarification. A common mistake is signing documents without fully comprehending them. Being informed is your best defense against buyer’s remorse.

Beyond Approval: Managing Your Fccu Car Loan Responsibly

Getting approved for an Fccu Car Loan is a significant step, but responsible loan management is equally important. Your actions after approval can impact your financial health, credit score, and overall car ownership experience.

Making Timely Payments: Crucial for Your Credit

The most fundamental aspect of responsible loan management is making your payments on time, every time. Late payments can result in fees, negatively impact your credit score, and potentially lead to repossession in severe cases. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Your payment history is a major component of your credit score. Consistently making on-time payments on your Fccu Car Loan will build a positive credit history, which can benefit you when applying for future loans or credit cards.

Understanding Your Loan Statement: Stay Informed

Take the time to review your monthly loan statements from Fccu. These statements provide crucial information, including:

- Your current loan balance.

- The amount of your next payment.

- How much of your payment goes towards principal vs. interest.

- Any outstanding fees.

- The remaining term of your loan.

Understanding these details helps you track your progress and manage your finances effectively.

Early Payoff Strategies: Pros and Cons

If you find yourself with extra funds, you might consider paying off your Fccu Car Loan early. The primary benefit is saving on interest charges, especially if you have a higher interest rate. It also frees up your monthly budget sooner.

However, check if your loan has any prepayment penalties (though credit unions rarely include these). Also, consider if those extra funds could be better utilized elsewhere, such as paying off higher-interest debt or building an emergency fund.

What to Do if You Face Financial Hardship

Life happens, and sometimes financial circumstances change. If you anticipate difficulty making your Fccu Car Loan payments, do not wait until you miss a payment. Contact Fccu immediately.

Based on my experience, many credit unions are willing to work with members facing hardship. They might offer options like deferring a payment, modifying your loan terms, or providing temporary relief. Open communication is key to finding a solution and avoiding more severe consequences.

Real-Life Scenarios and Success Stories

Having guided many individuals through their car buying journey, I’ve seen firsthand how an Fccu Car Loan can make a real difference. For instance, Sarah, a recent college graduate, secured a competitive Fccu Car Loan for her first reliable used car. Her pre-approval empowered her to negotiate a better price at the dealership, and Fccu’s flexible terms allowed her to manage her payments comfortably while starting her career.

Then there’s Mark, who had an existing car loan with a high interest rate from a traditional bank. After improving his credit score, he refinanced with an Fccu Car Loan, significantly lowering his monthly payment and saving him thousands of dollars in interest over the remaining term. These stories highlight the tangible benefits of choosing a member-focused lender committed to your financial well-being.

Conclusion: Drive Towards Your Future with an Fccu Car Loan

Securing a car loan is a significant financial decision that impacts your budget and lifestyle for years to come. By choosing an Fccu Car Loan, you’re not just getting financing; you’re partnering with a community-focused institution dedicated to offering competitive rates, personalized service, and transparent processes.

We’ve covered everything from understanding Fccu’s unique advantages and the various loan types available to navigating the application process and managing your loan responsibly. Armed with this in-depth knowledge, you are now well-equipped to make an informed decision.

Don’t let the dream of a new vehicle remain just a dream. Take the first step towards driving the car you need and want. Visit your local Fccu branch or explore their website today to learn more about their car loan options and begin your journey toward a smoother, more affordable ride. Your perfect car, financed the right way, is within reach.