Drive Your Dream: Unlocking the Best Car Loans in 2024 (A Comprehensive Guide)

Drive Your Dream: Unlocking the Best Car Loans in 2024 (A Comprehensive Guide) Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is exciting, but navigating the world of auto financing can often feel like a complex maze. For most people, a car loan isn’t just a convenience; it’s a necessity that makes vehicle ownership a reality. Choosing the right car loan can save you thousands of dollars over the life of your loan and significantly impact your financial well-being.

As an expert blogger and professional SEO content writer, I understand the importance of making informed financial decisions. This comprehensive guide is designed to be your ultimate resource, breaking down everything you need to know about securing the best car loans available today. We’ll delve deep into the options, demystify the process, and provide actionable insights to help you drive away with confidence and a loan that truly suits your budget.

Drive Your Dream: Unlocking the Best Car Loans in 2024 (A Comprehensive Guide)

Understanding the Landscape: What is a Car Loan and Why Does it Matter?

At its core, a car loan is a sum of money borrowed from a financial institution (like a bank, credit union, or online lender) specifically for the purpose of buying a vehicle. You agree to repay this amount, plus interest, over a predetermined period, known as the loan term. This monthly repayment is called your car payment.

The terms of your car loan – primarily the Annual Percentage Rate (APR) and the loan term – are critical. A lower APR means you pay less in interest over time, while a shorter loan term, though it might mean higher monthly payments, also reduces the total interest paid and gets you out of debt faster. Conversely, a longer loan term can make monthly payments more affordable but often results in paying significantly more interest over the loan’s life.

Based on my experience, many first-time buyers focus solely on the monthly payment without considering the total cost of the loan. This can be a costly oversight. Always look at the bigger picture: the total amount you’ll pay back, including all interest and fees.

Key Factors Influencing Your Car Loan Approval and Rates

Before we explore the top avenues for car loans, it’s essential to understand what lenders look for. Several factors play a pivotal role in determining whether your loan application is approved and what interest rate you’ll be offered.

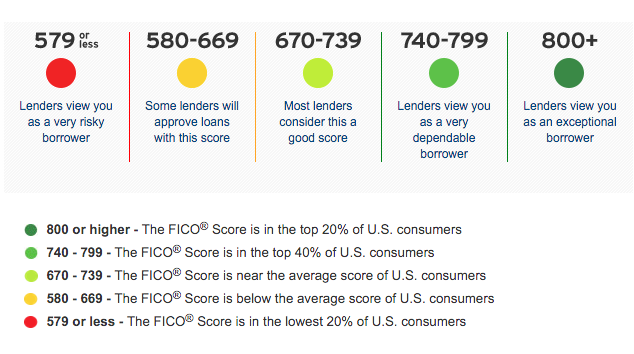

Your Credit Score: The Cornerstone of Lending

Your credit score is a numerical representation of your creditworthiness. It’s a three-digit number that tells lenders how responsibly you’ve managed debt in the past. Higher scores (generally 670 and above) indicate lower risk, leading to better interest rates and more favorable loan terms.

Pro tip from us: Before even thinking about applying for a car loan, check your credit score and report. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) annually. Rectifying any errors on your report can significantly boost your score. For more details on improving your credit, you might find our article on "" incredibly helpful.

Income and Debt-to-Income Ratio (DTI)

Lenders want assurance that you can comfortably afford your monthly payments. They’ll assess your income and compare it to your existing debt obligations. Your debt-to-income ratio (DTI) is a crucial metric here. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI (ideally below 36%) signals that you have enough disposable income to handle new debt.

Common mistakes to avoid are underestimating your current debt or overstating your income. Lenders will verify this information, and discrepancies can lead to delays or rejection.

Down Payment: Your Financial Commitment

Making a substantial down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over time. It also signals to lenders that you’re serious about your purchase and have a financial stake in the vehicle.

While a 20% down payment is often recommended, even 10% can make a difference. If you’re buying a used car, a smaller down payment might be acceptable.

Loan Term: The Repayment Horizon

The loan term, or the length of time you have to repay the loan, directly impacts your monthly payment and the total interest paid. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but less interest. Longer terms (e.g., 60, 72, or even 84 months) offer lower monthly payments but accumulate significantly more interest over time.

Based on my experience, while a longer term might seem appealing due to lower monthly payments, it often leads to being "upside down" on your loan (owing more than the car is worth) for a longer period, especially with depreciation.

Preparing for Your Car Loan Application: Steps to Success

Securing the best car loan isn’t about luck; it’s about preparation. Taking these steps before you even set foot in a dealership can give you a significant advantage.

- Determine Your Budget: Understand how much you can truly afford for a monthly car payment, including insurance, fuel, and maintenance. Don’t just focus on the loan; consider all associated costs of car ownership.

- Check Your Credit Report and Score: As mentioned, this is paramount. Dispute any errors and work to improve your score if needed.

- Get Pre-Approved: This is perhaps the most powerful step. Getting pre-approved by a lender provides you with a concrete offer (interest rate, loan amount, and terms) before you go shopping. It gives you negotiating power at the dealership and helps you understand what you can truly afford.

- Gather Necessary Documents: Lenders will typically ask for proof of income (pay stubs, tax returns), proof of residence (utility bills), identification (driver’s license), and potentially bank statements. Having these ready will streamline the application process.

The Top 5 Avenues for Car Loans: Your Best Bets in 2024

Now, let’s dive into the core of finding the right financing. Instead of listing specific banks, which can change their offerings frequently, we’ll focus on the types of lenders that consistently offer competitive rates and services. Understanding these categories will empower you to shop smart and find the ideal match for your needs.

1. Credit Unions: The Member-First Advantage

Who they are: Credit unions are non-profit financial cooperatives owned by their members. Unlike traditional banks, their primary goal isn’t to maximize profits for shareholders but to provide financial services at competitive rates to their members.

Why they’re a top choice:

- Lower Interest Rates: Based on my observations over the years, credit unions often offer some of the lowest interest rates on auto loans, especially for borrowers with good to excellent credit. Their non-profit status allows them to pass savings directly to their members.

- Personalized Service: You often get a more personalized and less transactional experience compared to larger banks. They tend to be more flexible and willing to work with members facing unique financial situations.

- Favorable Terms: Beyond just rates, credit unions might offer more flexible repayment schedules or fewer fees.

Potential drawbacks:

- Membership Requirement: You need to be a member to apply for a loan. Membership typically requires meeting certain criteria, such as living in a specific geographic area, working for a particular employer, or being affiliated with a certain organization.

- Fewer Branches/Online Presence: While many credit unions are expanding their digital footprint, some may have a smaller branch network or less sophisticated online banking platforms than national banks.

Best for: Borrowers with good to excellent credit who value competitive rates and a community-oriented banking experience, and who are willing to join a credit union.

2. Online Lenders: Speed, Convenience, and Wide Reach

Who they are: A rapidly growing segment of the lending industry, online lenders operate entirely or primarily through digital platforms. They include fintech companies and online-only banks that specialize in various types of loans, including auto loans.

Why they’re a top choice:

- Convenience and Speed: You can apply for and often get approved for a car loan from the comfort of your home, often within minutes or hours. The entire process, from application to funding, can be incredibly efficient.

- Competitive Rates: Due to lower overhead costs, online lenders can often offer highly competitive interest rates, rivaling or even beating traditional banks.

- Variety of Options: Many online lending marketplaces allow you to compare offers from multiple lenders with a single application, making it easier to find the best deal without impacting your credit score multiple times.

- Broader Credit Spectrum: Some online lenders specialize in loans for borrowers with less-than-perfect credit, providing options when traditional banks might decline.

Potential drawbacks:

- Less Personal Interaction: If you prefer face-to-face assistance, an online lender might not be for you. The entire process is digital.

- Potential for Information Overload: With many options, it can sometimes be overwhelming to sift through all the offers.

Best for: Tech-savvy borrowers seeking speed, convenience, competitive rates, and the ability to compare multiple offers quickly. Also a strong option for those with varying credit profiles.

3. Dealership Financing: The One-Stop Shop

Who they are: Dealerships often act as intermediaries, connecting you with a network of banks, credit unions, and captive finance companies (like Toyota Financial Services or Ford Credit) to secure a loan.

Why they’re a top choice:

- Convenience: It’s a "one-stop shop" experience. You can choose your car and arrange financing all in the same place, often on the same day.

- Special Offers and Incentives: Dealerships, particularly those offering manufacturer financing, frequently have special low-APR deals, cash back offers, or lease programs that can be very attractive, especially for new cars.

- Negotiating Power: If you have a pre-approval in hand, you can use it as leverage to see if the dealership can beat your outside offer.

Potential drawbacks:

- Higher Rates (Sometimes): Without pre-approval, dealerships might mark up the interest rate they receive from their lending partners to earn a profit. This means you might not always get the absolute best rate available to you.

- Focus on Monthly Payment: Salespeople often try to negotiate based solely on the monthly payment, which can distract from the overall cost of the loan and lead to longer terms or higher total interest.

Best for: Buyers who prioritize convenience, want to take advantage of manufacturer incentives, or have excellent credit and can qualify for special promotional rates. Always get pre-approved elsewhere first to ensure you’re getting a competitive offer.

4. Traditional Banks (Large National and Regional Banks): Familiarity and Range of Services

Who they are: These are the large, well-known financial institutions like Chase, Bank of America, Wells Fargo, and many regional banks. They offer a full suite of financial products, including auto loans.

Why they’re a top choice:

- Established Reputation: Many people already bank with these institutions, which can simplify the application process if you have an existing relationship.

- Branch Network: Extensive physical branch networks mean you can often get in-person assistance if needed.

- Competitive Rates (for strong credit): For borrowers with excellent credit, traditional banks can offer very competitive rates, especially if you have a history with them.

Potential drawbacks:

- Less Flexibility: Compared to credit unions, traditional banks might be less flexible with their lending criteria, especially for borrowers with lower credit scores.

- Rates Can Vary Widely: While some rates are competitive, others might be higher than what you could find at a credit union or online lender. It pays to shop around.

Best for: Existing bank customers who prefer to keep all their financial services under one roof, or those who value the security and extensive branch network of a large institution, especially if they have strong credit.

5. Manufacturer Financing (Captive Finance Companies): The Brand Specialists

Who they are: These are the lending arms directly associated with car manufacturers, such as Toyota Financial Services, Ford Credit, Honda Financial Services, etc. They exist to help sell their parent company’s vehicles.

Why they’re a top choice:

- Promotional Rates: This is where you’ll often find those enticing 0% APR offers or extremely low interest rates on new cars. These are powerful incentives designed to move inventory.

- Brand Specific Expertise: They are specialists in financing their brand’s vehicles and often have a deep understanding of their product lines.

Potential drawbacks:

- Strict Credit Requirements: To qualify for those ultra-low promotional rates, you typically need impeccable credit (often 720+ FICO score).

- Limited Choice: You’re limited to financing vehicles from that specific manufacturer.

- Shorter Terms for Best Rates: The lowest promotional rates often come with shorter loan terms (e.g., 36 or 48 months), meaning higher monthly payments. Longer terms might have higher, non-promotional rates.

Best for: Buyers with excellent credit looking to purchase a new car from a specific manufacturer and who can qualify for special promotional interest rates.

Common Mistakes to Avoid When Getting a Car Loan

Based on my experience guiding countless individuals through the car buying process, certain pitfalls repeatedly trip people up. Being aware of these common mistakes can save you significant time and money.

- Not Getting Pre-Approved: This is perhaps the biggest mistake. Without pre-approval, you walk into a dealership blind, without knowing your true buying power or the best rate you qualify for. You lose valuable negotiation leverage.

- Focusing Only on the Monthly Payment: As discussed earlier, a low monthly payment can hide a longer loan term and much higher total interest paid. Always ask for the total cost of the loan and the APR.

- Accepting the First Offer: Never take the first loan offer you receive, whether it’s from a bank, credit union, or dealership. Shopping around and comparing offers is crucial.

- Ignoring Your Credit Score: Your credit score is your financial report card. Neglecting to check it or improve it before applying can lead to higher interest rates and limited options.

- Adding Unnecessary Extras to Your Loan: Dealerships might try to roll extended warranties, GAP insurance (which can be important, but often cheaper elsewhere), or other add-ons into your loan. While some are beneficial, evaluate them critically and consider purchasing them separately if they inflate your loan amount unnecessarily.

- Not Understanding the Terms and Conditions: Always read the fine print of your loan agreement. Understand the APR, loan term, any prepayment penalties, and late payment fees.

Pro Tips for Securing the Best Car Loan

Beyond avoiding common mistakes, there are proactive steps you can take to optimize your car loan experience.

- Shop Your Loan First, Then Your Car: Get pre-approved before you start car shopping. This separates the financing negotiation from the car price negotiation, making both easier.

- Negotiate the Car Price Separately: Once you have your financing in place, focus on getting the best price for the vehicle itself. Treat your pre-approval as if you’re paying cash for the car.

- Consider a Shorter Loan Term: If your budget allows, opt for the shortest loan term possible (e.g., 36 or 48 months). You’ll pay significantly less interest over the life of the loan.

- Make a Significant Down Payment: The more you put down, the less you borrow, which translates to lower monthly payments and less interest. It also reduces your risk of being "underwater" on your loan.

- Boost Your Credit Score: Even a few points on your credit score can make a difference in your interest rate. Pay down credit card debt, avoid new credit applications, and pay all bills on time in the months leading up to your application.

- Understand APR vs. Interest Rate: The APR (Annual Percentage Rate) includes the interest rate plus any fees associated with the loan, giving you the true cost of borrowing. Always compare APRs, not just interest rates. For a deeper dive into these terms, check out our article on "".

- Get Multiple Offers: Don’t settle for the first offer. Apply to at least 3-4 different lenders (credit unions, online lenders, banks) to compare rates and terms. Multiple applications within a short window (typically 14-45 days) will usually count as only one hard inquiry on your credit report for rate shopping purposes.

Conclusion: Drive Away with Confidence

Securing a car loan doesn’t have to be a stressful ordeal. By understanding the factors that influence your approval and rates, preparing thoroughly, and knowing where to look for the best financing, you can make an informed decision that benefits your financial future.

Whether you choose the personalized service of a credit union, the speed of an online lender, the convenience of dealership financing, the familiarity of a traditional bank, or the promotional rates of manufacturer financing, the key is to shop around. Compare APRs, understand loan terms, and never hesitate to ask questions. Your dream car awaits, and with the right car loan, you’ll be driving it with peace of mind.

Ready to take the next step? Start by checking your credit, determining your budget, and exploring pre-approval options today!

External Link: For further unbiased information on auto loans and consumer financial protection, visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/