Drive Your Dreams: The Ultimate Guide to 3rd Party Car Loans

Drive Your Dreams: The Ultimate Guide to 3rd Party Car Loans Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering unparalleled freedom and convenience. While dealership financing is often the most straightforward path, it’s far from your only option. Enter 3rd party car loans – a powerful alternative that can unlock better rates, more flexible terms, and access to a wider range of vehicles, especially in the private sale market.

As an expert blogger and SEO content writer, I’ve delved deep into the automotive financing world. Based on my experience, understanding 3rd party car loans is crucial for any savvy car buyer looking to make an informed decision and potentially save thousands. This comprehensive guide will equip you with everything you need to know, from understanding what these loans are to navigating the application process and avoiding common pitfalls.

Drive Your Dreams: The Ultimate Guide to 3rd Party Car Loans

Let’s embark on this journey to empower your next car purchase!

What Exactly Are 3rd Party Car Loans?

When you hear "car loan," your mind might immediately jump to the dealership’s finance office. However, a 3rd party car loan refers to financing you secure directly from a financial institution that is independent of the car seller. This means you’re not getting the loan from the dealership or the vehicle manufacturer’s captive finance arm.

Instead, you’re working with a separate entity like a bank, credit union, or online lender. They approve you for a loan amount, and you then use those funds to purchase a car, effectively paying the seller in cash. This distinction is vital because it fundamentally changes your negotiating power and options.

This type of financing is particularly prevalent when buying a car from a private seller, where dealer financing isn’t available. It also offers a competitive edge even when purchasing from a dealership, allowing you to walk in with pre-approved funding.

Why Consider a 3rd Party Car Loan? Unlocking Greater Control

Many car buyers overlook 3rd party financing, assuming dealership options are always best. However, based on my experience, exploring these independent avenues can offer significant advantages. They empower you, the buyer, with more control over the entire purchasing process.

One primary reason is the ability to shop for the best interest rates and terms. Dealerships often have partnerships that limit your options, whereas 3rd party lenders are numerous and competitive. This competition can translate directly into savings for you.

Another compelling factor is the flexibility it provides, especially for private party sales. If you’ve found the perfect used car listed by an individual, a 3rd party loan is often your only viable financing solution. It bridges the gap, turning a private sale into a manageable purchase.

The Landscape of 3rd Party Lenders: Who Are They?

The world of third-party auto financing is diverse, offering various institutions tailored to different financial needs and preferences. Understanding these players is key to finding the right fit for your situation. Each type of lender brings its own advantages and disadvantages to the table.

Here are the primary types of 3rd party lenders you’ll encounter:

-

Traditional Banks: These are the large, well-known financial institutions. Banks typically offer competitive rates for borrowers with good to excellent credit scores. They provide a sense of security and often have a wide array of other financial products.

- Their application processes can sometimes be more rigorous, requiring extensive documentation. However, their established presence makes them a reliable choice for many. You might already have a relationship with a bank, which can streamline the process.

-

Credit Unions: Member-owned financial cooperatives, credit unions are renowned for offering some of the most competitive interest rates. They often have more flexible lending criteria and a strong focus on member service.

- To qualify for a loan, you typically need to become a member, which usually involves a small deposit or meeting specific eligibility requirements (e.g., living in a certain area, working for a particular employer). Their community-centric approach can be a significant benefit.

-

Online Lenders: The digital age has brought forth a multitude of online-only lenders. These platforms specialize in streamlining the application and approval process, often offering quick decisions and competitive rates.

- They are particularly convenient for those who prefer to manage their finances entirely online. Many online lenders cater to a broader range of credit scores, including those with less-than-perfect credit, making them highly accessible.

-

Peer-to-Peer (P2P) Lending Platforms: While less common for car loans specifically, P2P platforms connect borrowers directly with individual investors. These loans can offer unique terms but might require more research to ensure legitimacy.

- They represent a more niche segment of independent lenders and are generally suited for those comfortable with alternative financing models. Always exercise caution and verify the platform’s reputation before proceeding.

The Advantages of Choosing a 3rd Party Car Loan

Opting for non-dealer financing can bring a host of benefits that significantly enhance your car buying experience. These advantages often translate into greater financial flexibility and better overall value. It’s about putting you in the driver’s seat of your financial decision.

Here are some compelling reasons to consider a 3rd party loan:

-

More Competitive Interest Rates: Because 3rd party lenders compete for your business, they often offer lower interest rates compared to dealer financing. Dealers sometimes mark up rates to increase their profit margins.

- Shopping around with multiple banks, credit unions, and online lenders can yield significantly better terms. This competitive environment is a huge win for consumers.

-

Increased Negotiating Power at the Dealership: Walking into a dealership with pre-approved financing from a 3rd party lender turns you into a cash buyer. This removes the financing aspect from the negotiation, allowing you to focus solely on the car’s price.

- Dealers often make more profit on financing than on the vehicle itself. By securing your own loan, you strip them of that leverage, potentially getting a better deal on the car itself.

-

Flexibility for Private Party Purchases: If you’re buying a car from an individual seller, financing a private car sale is almost exclusively done through a 3rd party loan. Dealerships don’t facilitate financing for cars they don’t sell.

- This opens up a vast market of potentially well-maintained used cars at lower prices than those found on dealership lots. It’s a game-changer for finding unique or specific models.

-

Broader Vehicle Choice: With a 3rd party loan, you’re not restricted to the inventory of a single dealership or brand. You can finance almost any vehicle, new or used car loans from third parties, as long as it meets the lender’s criteria (e.g., age, mileage limits).

- This freedom allows you to truly find the perfect car that fits your needs and budget, rather than settling for what’s available through a specific dealer.

-

Transparent Terms and Conditions: Many 3rd party lenders pride themselves on clear, straightforward loan terms. You’ll often have a better understanding of all fees, interest rates, and repayment schedules upfront.

- Pro tip from us: Always read the fine print carefully, but generally, independent lenders strive for greater transparency to attract and retain customers.

Potential Downsides and Risks to Be Aware Of

While 3rd party car loans offer numerous advantages, it’s crucial to approach them with a clear understanding of potential drawbacks. Being informed about these aspects will help you navigate the process safely and effectively. No financial product is without its considerations.

Here are some potential downsides to keep in mind:

-

More Legwork Required: Securing a 3rd party loan often means more independent research and application processes. You’ll need to compare offers from various lenders yourself.

- Unlike a dealership where they might handle multiple applications for you, with a 3rd party loan, you are the primary driver of the comparison shopping process. This requires time and effort.

-

Higher Scrutiny on Vehicle Condition (for private sales): When financing a private sale, the lender might require an independent inspection of the vehicle. This is to ensure its value and condition justify the loan amount.

- While this is an added step, it also provides an extra layer of protection for you, ensuring you’re not financing a lemon. It’s a common practice for third-party auto financing on used cars.

-

Potential for Loan Denial: If your credit score is low, or your debt-to-income ratio is high, securing a 3rd party loan can be challenging. Some independent lenders have stricter approval criteria than certain dealership finance departments.

- Common mistakes to avoid are not checking your credit score before applying. This can lead to multiple hard inquiries and further lower your score.

-

Funding Time: While many online lenders offer quick approvals, the actual transfer of funds might take a few business days. This could be a factor if you need to purchase a car immediately.

- Plan ahead and apply for pre-approval before you’re ready to buy, giving yourself ample time to receive the funds.

The Application Process: A Step-by-Step Guide

Securing a 3rd party car loan doesn’t have to be daunting. By following a structured approach, you can navigate the process efficiently and confidently. Preparation is key to a smooth and successful application.

Here’s a breakdown of the typical steps involved:

-

Assess Your Financial Health and Budget:

- Before anything else, pull your credit report and score. This will give you an idea of what rates you might qualify for. Sites like AnnualCreditReport.com offer free reports.

- Determine how much you can realistically afford for a monthly car payment, considering your income, existing debts, and other expenses. Don’t forget insurance and maintenance costs.

-

Gather Necessary Documentation:

- Lenders will typically require proof of income (pay stubs, tax returns), identification (driver’s license), proof of residence (utility bill), and potentially bank statements. Having these ready streamlines the application.

-

Shop Around for Lenders:

- Contact various banks, credit unions, and online lenders. Inquire about their auto loan rates, terms, and specific requirements for third-party loan benefits.

- Many lenders offer pre-qualification with a soft credit check, which won’t impact your score, allowing you to compare offers without commitment.

-

Submit Your Application:

- Once you’ve chosen a lender, complete their formal application. This will involve a hard credit inquiry, which might temporarily ding your score by a few points.

- Be honest and thorough with all information provided to avoid delays or rejections.

-

Receive Loan Offer and Review Terms:

- If approved, you’ll receive a loan offer outlining the interest rate, loan term, monthly payment, and any fees.

- Carefully review all aspects, including any prepayment penalties, before signing. Don’t hesitate to ask questions if anything is unclear.

-

Purchase Your Vehicle:

- With your loan approved and funds secured (or a letter of guarantee from the lender), you can now confidently shop for your car.

- Whether it’s a dealership or a private seller, you’re effectively a cash buyer, giving you significant leverage in negotiations.

What to Look For in a 3rd Party Car Loan: Key Considerations

Not all third-party auto financing offers are created equal. To ensure you’re getting the best deal, it’s vital to know what factors to scrutinize beyond just the headline interest rate. A thorough comparison can save you money and headaches down the line.

Here are the critical elements to evaluate:

-

Interest Rates: This is arguably the most significant factor impacting your total loan cost. Compare the Annual Percentage Rate (APR), which includes fees, not just the nominal interest rate.

- A lower APR means lower monthly payments and less money paid over the life of the loan. Even a half-percent difference can add up significantly.

-

Loan Term: This refers to the length of time you have to repay the loan (e.g., 36, 48, 60, 72 months). A longer term means lower monthly payments but more interest paid overall.

- Conversely, a shorter term means higher monthly payments but less interest. Find a balance that fits your budget and financial goals.

-

Fees and Charges: Be vigilant for any hidden fees, such as origination fees, application fees, or documentation fees. Some lenders are more transparent than others.

- Pro tip from us: Ask for a complete breakdown of all costs associated with the loan before you commit.

-

Prepayment Penalties: Some loans charge a fee if you pay off your loan early. This can negate the benefit of accelerated payments if you plan to do so.

- Ideally, look for loans with no prepayment penalties, allowing you the flexibility to pay down your debt faster without extra cost.

-

Customer Service and Reputation: Research the lender’s reputation. Read reviews and check their ratings with consumer protection agencies.

- A lender with good customer service can make a huge difference if you encounter any issues during the loan term. This aspect of how to get a third-party car loan is often overlooked.

-

Loan-to-Value (LTV) Requirements: Lenders might have limits on how much they’re willing to lend compared to the car’s value, especially for older used car loans from third parties. Ensure your desired car meets these criteria.

- This is particularly important for private sales where the valuation might be less clear-cut than a dealer’s advertised price.

Navigating Credit Scores and 3rd Party Loans

Your credit score is the single most influential factor in determining the interest rates for third-party loans you’ll be offered. A strong credit history opens doors to the best rates and terms, while a lower score can present challenges. Understanding this relationship is crucial for any car buyer.

The Impact of Your Credit Score

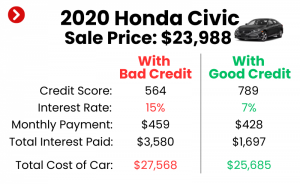

Lenders use your credit score as a snapshot of your financial reliability. A higher score (generally 670 and above) indicates a lower risk, leading to lower interest rates. Conversely, a lower score suggests higher risk, resulting in higher interest rates or even loan denial. This is a fundamental aspect of all lending.

- Excellent Credit (780+): You’ll likely qualify for the lowest rates available, often below 4-5%.

- Good Credit (670-779): You’ll still get competitive rates, perhaps in the 5-8% range.

- Fair Credit (580-669): Rates will be higher, potentially 10-15% or more, and options might be limited.

- Poor Credit (below 580): Securing a loan can be very difficult, with rates potentially exceeding 20%, if approved at all.

Tips for Improving Your Credit Score

If your credit score isn’t where you want it to be, here are some actionable steps to improve it before applying for a third-party loan:

- Pay Bills on Time: Payment history is the biggest factor in your credit score. Set up reminders or automatic payments.

- Reduce Debt: Lowering your credit utilization ratio (how much credit you use vs. how much you have available) can boost your score.

- Check Your Credit Report for Errors: Incorrect information can negatively impact your score. Dispute any inaccuracies immediately.

- Avoid New Credit Applications: Limit hard inquiries on your report in the months leading up to a car loan application.

- For a deeper dive into credit management, consider exploring resources on understanding your credit score. (Internal Link Placeholder)

Options for Bad Credit 3rd Party Car Loans

Even with a less-than-perfect credit score, all hope is not lost. Here are a few strategies for securing third-party loan benefits with bad credit:

- Cosigner: A trusted individual with good credit can co-sign your loan, making you more attractive to lenders. They share responsibility for repayment.

- Secured Loans: Some lenders offer secured auto loans, where the car itself acts as collateral. This can reduce risk for the lender and potentially lower your interest rate.

- Smaller Loan Amount/Older Car: Opting for a less expensive car reduces the loan amount, making it easier to get approved.

- Subprime Lenders: There are lenders who specialize in bad credit third-party car loans, though their interest rates will be significantly higher. Exercise caution and compare offers carefully.

Common Mistakes to Avoid When Getting a 3rd Party Car Loan

Based on my experience in the finance industry, many car buyers fall prey to similar missteps when seeking independent financing. Being aware of these common pitfalls of third-party loans can save you from costly errors and unnecessary stress. Forewarned is forearmed.

Here are the most frequent mistakes to sidestep:

-

Not Comparing Offers: This is perhaps the biggest mistake. Settling for the first loan offer without checking at least 3-5 different lenders means you’re likely leaving money on the table.

- Each lender has different criteria and rates, so extensive comparison shopping is non-negotiable for the best deal.

-

Neglecting the Fine Print: It’s easy to get excited about an approval and skim through the loan agreement. However, critical details like prepayment penalties, late fees, and specific terms are buried in the fine print.

- Always read the entire loan document thoroughly. If you don’t understand something, ask for clarification.

-

Overextending Your Budget: Just because you’re approved for a certain amount doesn’t mean you should spend it all. Factor in insurance, maintenance, fuel, and registration costs, not just the monthly payment.

- Common mistakes we’ve seen are buyers getting approved for a higher amount than they truly need, leading to financial strain later on. Stick to your initial, realistic budget.

-

Ignoring Your Credit Score: Applying for loans without knowing your credit score can lead to rejections and multiple hard inquiries, further damaging your score.

- Always check your score beforehand and work to improve it if necessary. This preparation is a crucial step in the documents for third-party car loans process.

-

Not Considering the Car’s Value (for private sales): If buying from a private seller, lenders will often base their loan amount on the car’s market value (e.g., Kelley Blue Book, Edmunds). Overpaying for a vehicle means you’ll have to cover the difference out of pocket.

- Ensure the car’s price aligns with its fair market value to avoid this discrepancy.

-

Applying to Too Many Lenders at Once: While comparison is good, submitting applications to dozens of lenders can result in numerous hard inquiries, negatively impacting your credit score.

- Group your applications within a short window (e.g., 14-45 days), as FICO typically treats multiple inquiries for the same type of loan within that period as a single inquiry.

When a 3rd Party Loan Might Be Your Best Bet

While dealer financing has its place, there are specific scenarios where a 3rd party car loan truly shines and becomes the optimal choice. Understanding these situations can guide you toward the most advantageous financing path. It’s about recognizing the right tool for the job.

Consider a 3rd party loan in these situations:

- Buying from a Private Seller: This is the most common and compelling reason. Dealerships cannot finance cars they don’t sell. If you’ve found a great deal on a used car from an individual, a 3rd party loan is your primary financing option.

- Seeking the Absolute Lowest Interest Rate: If you have excellent credit, you’re likely to find the most competitive rates from banks, credit unions, or online lenders, rather than relying on a dealer’s limited options.

- Desiring More Control and Transparency: If you prefer to separate the car negotiation from the financing negotiation, a 3rd party loan gives you that power. You can focus purely on the vehicle’s price.

- Refinancing an Existing Car Loan: If you’re looking to refinancing with third-party lenders to get a lower interest rate or better terms on an existing car loan, independent lenders are your go-to. They specialize in offering competitive refinance options.

- Purchasing a Niche or Older Used Vehicle: Some dealerships might be reluctant to finance very old or unique vehicles. 3rd party lenders often have more flexible criteria, making it easier to finance these specific types of cars.

- You Have Pre-Approval: Having a pre-approved loan in hand before stepping onto a dealership lot gives you immense leverage and confidence, making you a "cash buyer."

Alternatives to 3rd Party Car Loans

While 3rd party car loans are a fantastic option, they aren’t the only way to finance a vehicle. It’s important to be aware of other avenues to ensure you’re making the most informed decision for your unique circumstances. Each alternative has its own set of pros and cons.

Here are some common alternatives:

-

Dealership Financing: This is the most common option, where you arrange financing directly through the car dealership. They act as an intermediary, working with various banks and lenders (including their own captive finance companies).

- Pros: Convenience, one-stop shop, potential for special manufacturer incentives.

- Cons: Rates might be marked up, limited lender options, less negotiating power on the car price.

-

Personal Loans: An unsecured personal loan can be used for any purpose, including buying a car. These loans are based purely on your creditworthiness.

- Pros: Flexible use of funds, no collateral required (usually).

- Cons: Interest rates can be higher than secured auto loans, especially for larger amounts, and repayment terms might be shorter.

-

Home Equity Loan or Line of Credit (HELOC): If you own a home and have significant equity, you can borrow against it.

- Pros: Often very low interest rates due to being secured by your home.

- Cons: Your home is collateral, meaning you risk losing it if you default. Not recommended for typical car purchases due to the risk.

-

Leasing: While not a loan, leasing is an alternative to buying. You essentially rent the car for a set period and mileage, then return it or buy it at the end of the term.

- Pros: Lower monthly payments than buying, always driving a new car, less maintenance worry.

- Cons: No ownership, mileage restrictions, fees for excess wear and tear, never-ending payments if you always lease.

Future Trends in Auto Financing: What’s Next?

The world of automotive financing is constantly evolving, driven by technological advancements and shifting consumer expectations. Keeping an eye on future trends in auto financing can help you anticipate new opportunities and challenges. Innovation is always on the horizon.

Here’s a glimpse into what we might expect:

-

Further Digitization and AI: Online lenders are already popular, but expect even more streamlined digital application processes. Artificial intelligence will likely play a larger role in credit assessment, potentially leading to faster and more personalized loan approvals.

- This could mean quicker access to third-party auto financing with less manual paperwork.

-

Personalized Rates: AI and big data analytics will enable lenders to offer highly personalized interest rates based on a comprehensive assessment of an individual’s financial behavior, not just their credit score.

- This might open doors for those with non-traditional credit histories to secure better rates.

-

Embedded Finance: Imagine applying for and securing a car loan directly within a car shopping app or even on a manufacturer’s website, with 3rd party lenders integrated seamlessly. This "embedded finance" makes the process almost invisible.

- This frictionless experience could further blur the lines between third-party lenders vs. dealerships in terms of convenience.

-

Subscription Models and Mobility Services: While not direct loans, the rise of car subscription services and various mobility-as-a-service options could reduce the need for traditional car ownership and, by extension, traditional loans for some segments of the population.

- This represents a significant shift in how people access transportation, potentially impacting the long-term demand for car loans.

-

Focus on ESG (Environmental, Social, Governance) Factors: Lenders might start offering more favorable terms for electric vehicles or cars with strong environmental credentials, aligning with broader sustainability goals.

- This could create new niches for third-party loan benefits for eco-conscious buyers.

Conclusion: Empowering Your Car Buying Journey

Navigating the world of car loans can feel complex, but understanding 3rd party car loans is a powerful step toward making an informed and financially savvy decision. From the flexibility they offer for private sales to the potential for securing more competitive interest rates, independent financing puts you in a position of strength.

By meticulously comparing lenders, understanding all the terms, and preparing your finances, you can unlock significant advantages. Remember, knowledge is power, and in the realm of car buying, it translates directly into savings and peace of mind.

Don’t let the convenience of dealership financing blind you to potentially better options. Take the time to explore banks, credit unions, and online lenders. Your ideal car and optimal financing solution might just be a click or a conversation away. Drive your dreams forward with confidence and smart financial choices!

For further resources on making sound financial decisions, visit the Consumer Financial Protection Bureau website. (External Link Placeholder: https://www.consumerfinance.gov/consumer-tools/auto-loans/)