Drive Your Dreams: The Ultimate Guide to Getting Bank Approval for Car Loans

Drive Your Dreams: The Ultimate Guide to Getting Bank Approval for Car Loans Carloan.Guidemechanic.com

Getting behind the wheel of your dream car is an exciting prospect, but for many, the path to ownership runs through a crucial gateway: bank approval for a car loan. Navigating the world of auto financing can seem daunting, filled with jargon and intricate requirements. However, understanding the process and preparing effectively can significantly boost your chances of success.

This comprehensive guide is designed to demystify car loan approval, offering you an expert roadmap to secure the best financing terms. Whether you’re a first-time buyer or looking to upgrade, we’ll equip you with the knowledge and strategies to approach banks with confidence and drive away with an approved loan. Let’s unlock the secrets to a smooth and successful car loan application!

Drive Your Dreams: The Ultimate Guide to Getting Bank Approval for Car Loans

Why Bank Approval is Your Best Bet for Car Financing

When it comes to financing a vehicle, you have several options, including dealership financing, online lenders, and direct bank loans. Based on my experience, securing a loan directly from a bank often presents numerous advantages that make it a highly desirable choice. Banks typically offer competitive interest rates, flexible terms, and a transparent application process.

The rigorous approval process at a bank means they scrutinize your financial health more thoroughly. While this might seem like an extra hurdle, it actually works in your favor by ensuring you receive a loan that aligns with your financial capabilities, preventing future financial strain. Moreover, having a direct relationship with a bank can simplify future financial endeavors.

Understanding the Bank’s Perspective: What Lenders Look For

To successfully navigate the car loan approval process, it’s essential to think like a lender. Banks are in the business of lending money, but they also need to mitigate risk. They want to ensure you are a reliable borrower who will repay the loan on time. Several key factors weigh heavily in their decision-making process.

Understanding these elements and proactively working on them can drastically improve your approval odds. Let’s dive deep into each of these critical components.

1. Your Credit Score: The Cornerstone of Loan Approval

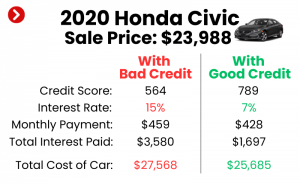

Your credit score is arguably the most influential factor in determining whether you get approved for a car loan and what interest rate you’ll receive. It’s a three-digit number that represents your creditworthiness, acting as a snapshot of your financial responsibility. Banks use this score to quickly assess the risk associated with lending you money.

A higher credit score signals to lenders that you have a history of managing debt responsibly, making you a less risky borrower. Conversely, a lower score might suggest potential payment issues, leading to higher interest rates or even outright denial. Pro tips from us: knowing your score before you apply is crucial.

What is a "Good" Credit Score for a Car Loan?

While there’s no single magic number, generally, a FICO score of 660 and above is considered "good" for an auto loan. Scores in the 700s are excellent and will likely qualify you for the most favorable interest rates. Lenders often categorize scores as follows:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

If your score falls into the "Fair" or "Poor" categories, don’t despair, but be prepared for potentially higher interest rates or the need for a co-signer.

How to Improve Your Credit Score Before Applying

Improving your credit score takes time and consistent effort, but even small gains can make a difference. Based on my experience, focusing on these areas can yield positive results:

- Pay Bills on Time, Every Time: Payment history is the most significant factor in your credit score. Set up automatic payments or reminders to avoid missing due dates.

- Reduce Existing Debt: Lowering your credit card balances, especially, can improve your credit utilization ratio (the amount of credit you’re using compared to your total available credit). Aim to keep this ratio below 30%.

- Avoid Opening New Credit Accounts: Each new application can temporarily ding your score. Try to avoid applying for new credit cards or loans in the months leading up to your car loan application.

- Check Your Credit Report for Errors: Mistakes on your credit report can unfairly drag down your score. Obtain free copies of your report from AnnualCreditReport.com and dispute any inaccuracies promptly.

- Keep Old Accounts Open: The length of your credit history contributes to your score. Don’t close old, paid-off accounts, even if you don’t use them.

Remember, building good credit is a marathon, not a sprint. Start working on it well in advance of your car purchase.

2. Income and Employment Stability: Can You Afford It?

Banks want assurance that you have a steady and sufficient income to comfortably make your monthly car loan payments. Your employment history and income level are direct indicators of your ability to repay the debt. Lenders typically look for stability, which means consistent employment with the same employer for a reasonable period, often two years or more.

While a high income is certainly a plus, stability is often equally, if not more, important. A fluctuating income or frequent job changes might raise red flags, even if your current income is high. Banks prefer predictable income streams.

What Banks Look For in Your Income & Employment

- Consistent Employment: A stable work history, ideally with the same employer for at least two years, demonstrates reliability.

- Sufficient Income: Your income must be high enough to cover the proposed car payment along with your existing financial obligations.

- Verifiable Income: Be prepared to provide pay stubs, W-2 forms, tax returns, or bank statements to prove your income. Self-employed individuals may need to provide more extensive documentation.

- Debt-to-Income (DTI) Ratio: This crucial metric measures how much of your gross monthly income goes towards debt payments. We’ll delve into DTI in the next section.

Common mistakes to avoid are underestimating the importance of documenting all income sources clearly. If you have multiple income streams, ensure you can provide verifiable proof for all of them.

3. Debt-to-Income (DTI) Ratio: A Key Financial Health Indicator

Your Debt-to-Income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. It’s a critical tool banks use to assess your ability to take on additional debt without becoming overextended. A high DTI suggests you might struggle to manage a new car loan, even if your income is substantial.

Lenders generally prefer a DTI ratio below 36% for optimal approval chances, though some may approve loans with a DTI up to 43% if other factors (like an excellent credit score) are strong. Pro tips from us: aim for the lowest DTI possible.

Calculating Your DTI

To calculate your DTI, simply add up all your monthly debt payments, including:

- Rent or mortgage payments

- Credit card minimum payments

- Student loan payments

- Other loan payments (personal loans, existing car loans)

- Do not include utility bills, food, or insurance in this calculation.

Then, divide that total by your gross monthly income (your income before taxes and deductions).

Example:

- Monthly Debt Payments: $1,200 (mortgage) + $200 (credit cards) + $300 (student loan) = $1,700

- Gross Monthly Income: $5,000

- DTI = ($1,700 / $5,000) * 100 = 34%

This 34% DTI would be considered good by most lenders.

How to Improve Your DTI

- Pay Down Existing Debts: Reducing credit card balances or paying off smaller loans before applying for a car loan can significantly lower your monthly debt obligations.

- Increase Your Income: While not always immediately feasible, finding ways to boost your gross monthly income (e.g., a raise, a side hustle) will naturally lower your DTI.

- Avoid Taking on New Debt: Just like with credit scores, refrain from opening new credit lines or taking out other loans in the months leading up to your car loan application.

4. Down Payment: Your Commitment to the Loan

Making a substantial down payment is one of the most effective ways to strengthen your car loan application. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. More importantly, it signals to the bank that you are a serious and responsible borrower.

When you put money down, you have immediate equity in the vehicle, reducing the bank’s risk. If you were to default, they would likely recover more of their money. Based on my experience, a good down payment can often offset a slightly less-than-perfect credit score.

How Much Down Payment is Ideal?

While any down payment is better than none, a common recommendation for new cars is 10-20% of the vehicle’s purchase price. For used cars, aiming for 10% is generally a good starting point. However, the more you can put down, the better your loan terms will likely be.

Benefits of a Larger Down Payment:

- Lower Monthly Payments: Less money borrowed means smaller installments.

- Less Interest Paid: You’re borrowing less, so you accrue less interest over time.

- Reduced Risk of Negative Equity: You’re less likely to owe more than the car is worth (being "upside down" on your loan).

- Improved Approval Chances: Lenders see you as a lower risk.

- Potentially Better Interest Rates: A lower loan amount and higher equity can sometimes lead to a lower APR.

5. Loan-to-Value (LTV) Ratio: The Car’s Value vs. The Loan Amount

The Loan-to-Value (LTV) ratio is another metric banks use, comparing the amount of money you want to borrow against the actual market value of the car. It’s essentially the inverse of your equity. If a car is valued at $20,000 and you’re borrowing $18,000, your LTV is 90% ($18,000 / $20,000).

Banks prefer a lower LTV because it means they are lending less relative to the asset’s value, which reduces their risk. A higher LTV, especially above 100% (which can happen if you roll negative equity from a trade-in into a new loan), makes the loan riskier for the bank. Pro tips from us: aim for an LTV of 100% or less.

How LTV Impacts Your Loan

- Risk Assessment: A high LTV indicates higher risk for the lender.

- Approval Likelihood: Banks are more likely to approve loans with a lower LTV.

- Interest Rates: A lower LTV can sometimes lead to more favorable interest rates.

- Depreciation: New cars begin to depreciate the moment they leave the lot, so a high LTV on a new car can quickly lead to negative equity.

A significant down payment directly helps in achieving a lower LTV, reinforcing its importance.

6. Vehicle Choice: New vs. Used, and Its Impact on Approval

The type of vehicle you choose also plays a role in bank approval. While it might seem counterintuitive, banks view new cars differently than used cars, primarily due to factors like depreciation and reliability.

- New Cars: Generally seen as lower risk because they come with warranties, have no prior history of accidents or maintenance issues, and their value is more predictable in the short term. However, they depreciate quickly.

- Used Cars: Can be higher risk due to unknown maintenance history, potential for unforeseen repairs, and less predictable depreciation. Banks might be more cautious with older, high-mileage vehicles.

The Bank’s Perspective on Vehicle Age and Mileage

Banks often have specific policies regarding the age and mileage of used vehicles they are willing to finance. For instance, some may not finance vehicles older than 10 years or with more than 100,000-120,000 miles. This is because older, higher-mileage cars represent a greater risk of breakdown, which could lead to the borrower defaulting on the loan.

Common mistakes to avoid are falling in love with a car that’s too old or has too many miles for most bank financing criteria. Always check with your lender about their specific vehicle restrictions before you commit to a purchase.

7. Co-signer or Co-borrower: A Boost for Your Application

If your credit score is less than ideal, your income is borderline, or you have a high DTI, a co-signer or co-borrower can significantly improve your chances of getting bank approval for a car loan. These individuals essentially vouch for you, agreeing to take on responsibility for the loan if you fail to make payments.

What’s the Difference?

- Co-signer: A co-signer adds their creditworthiness to your application but typically doesn’t have ownership rights to the vehicle. They are responsible for the debt if you default.

- Co-borrower: A co-borrower shares equal responsibility for the loan and typically has ownership rights to the vehicle. Their income and credit history are both considered.

Benefits of a Co-signer/Co-borrower:

- Increased Approval Odds: Their strong credit and income can compensate for your weaker profile.

- Potentially Lower Interest Rates: A stronger application often qualifies for better terms.

Risks to Consider:

- Impact on Co-signer’s Credit: If you miss payments, it negatively affects their credit score as well.

- Strained Relationships: Financial obligations can put a strain on personal relationships.

Based on my experience, consider a co-signer only if absolutely necessary and ensure both parties fully understand the responsibilities involved. It’s a significant commitment.

Step-by-Step Guide to Applying for a Car Loan

Now that you understand what banks look for, let’s walk through the practical steps to secure your car loan approval.

1. Preparation: Gather Your Documents

Before you even step foot in a bank or dealership, gather all necessary documentation. Being prepared not only speeds up the process but also demonstrates your seriousness and organization.

- Personal Identification: Driver’s license, Social Security card.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms (last 2 years), tax returns (last 2 years for self-employed), bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Credit Report: While banks pull their own, having a copy of yours helps you anticipate any issues.

- Existing Debt Information: Statements for credit cards, student loans, or other outstanding debts.

- Vehicle Information (if applicable): If you’ve already chosen a car, have its VIN, make, model, and mileage.

2. Researching Lenders: Shop Around for the Best Deal

Don’t just go with the first bank you find or the one your dealership recommends. Shopping around for a loan is one of the most important steps to secure favorable terms. Different lenders have varying criteria, rates, and fees.

- Traditional Banks: Your current bank or other major financial institutions often offer competitive rates.

- Credit Unions: These member-owned institutions often have lower interest rates and more flexible terms than traditional banks. It’s worth exploring if you qualify for membership.

- Online Lenders: Many reputable online platforms specialize in auto loans and can offer quick pre-approvals.

Apply for pre-approval with 2-3 different lenders within a short window (typically 14-45 days) to minimize the impact on your credit score. Multiple inquiries for the same type of loan within this period are usually counted as a single inquiry.

3. Pre-approval: Your Power Tool for Negotiation

Getting pre-approved for a car loan is a game-changer. It means a bank has reviewed your financial information and agreed to lend you a specific amount at a particular interest rate, before you even choose a car.

Benefits of Pre-approval:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You walk into the dealership as a cash buyer, giving you leverage to negotiate the car’s price without the added stress of financing.

- Faster Purchase Process: Once you find the car, the financing is already largely handled, streamlining the buying experience.

- Compare Offers: Use your pre-approval as a benchmark against any financing offered by the dealership.

4. The Application Process: Filling Out the Forms

Once you’ve chosen a lender and are ready to apply (either for pre-approval or a final loan), you’ll fill out an application form. Be honest and accurate with all information. The bank will then review your application, pulling your credit report and verifying your income and employment.

This process can take anywhere from a few hours to a couple of business days, depending on the lender and the complexity of your financial situation.

5. Negotiating Terms: Don’t Settle for the First Offer

Even after you’ve been approved, there might be room for negotiation, especially on the interest rate and loan duration.

- Interest Rate (APR): If you have multiple pre-approval offers, use them to leverage a better rate from your preferred lender. Even a quarter-point difference can save you hundreds over the life of the loan.

- Loan Term: While a longer loan term means lower monthly payments, it also means paying more interest over time. Aim for the shortest term you can comfortably afford. Common terms are 36, 48, 60, or 72 months. A 48- or 60-month term is often a good balance between manageable payments and lower total interest.

Common Mistakes to Avoid When Applying for a Car Loan

Based on my experience, many applicants inadvertently jeopardize their chances by making avoidable errors. Here are some common pitfalls:

- Not Checking Your Credit Score: Going into the process blind is a major mistake. You need to know your standing.

- Applying to Too Many Lenders Simultaneously: While rate shopping is good, submitting dozens of applications can negatively impact your score. Group your inquiries within a short period.

- Ignoring Your DTI: Many focus only on income, forgetting that high existing debt can be a deal-breaker.

- Underestimating the Down Payment: Trying to get a loan with no money down significantly increases your risk profile for lenders.

- Lying on the Application: This is a serious offense that can lead to fraud charges and immediate loan denial.

- Impulse Buying: Rushing into a car purchase without proper research or financial preparation often leads to unfavorable loan terms.

- Focusing Only on Monthly Payment: While important, also consider the total cost of the loan (including interest) over its entire term.

Pro Tips for Increasing Your Approval Chances

Beyond avoiding common mistakes, here are some proactive strategies to boost your likelihood of getting bank approval for a car loan:

- Get Your Finances in Order Well in Advance: Start improving your credit and saving for a down payment months before you plan to buy.

- Maintain a Low Credit Utilization Ratio: Keep your credit card balances well below their limits.

- Have a Clear Budget: Know exactly what you can afford for a monthly payment, insurance, and maintenance.

- Consider a Reputable Dealer: While you’re getting bank financing, a dealership with a good reputation can sometimes facilitate the process.

- Be Prepared to Explain Any Credit Anomalies: If you have a legitimate reason for a past late payment (e.g., medical emergency), be ready to explain it concisely and professionally.

- Bundle Services with Your Bank: Sometimes, having multiple accounts (checking, savings, mortgage) with one bank can give you a slight edge or access to special rates.

After Approval: What Happens Next?

Once your car loan is approved, the bank will provide you with the final loan documents outlining all the terms: the approved loan amount, interest rate (APR), monthly payment, and the loan term. Carefully review everything before signing.

You’ll then typically receive a check or a direct deposit to facilitate the purchase of your vehicle. Present this financing to the dealership, and you’re ready to complete the purchase and drive away in your new car! Remember, the goal is not just approval, but approval on terms that are sustainable for your financial future.

Conclusion: Drive Towards Smart Financial Decisions

Getting bank approval for a car loan doesn’t have to be a stressful ordeal. By understanding the key factors banks consider—your credit score, income stability, DTI ratio, down payment, LTV, and even your vehicle choice—you can strategically prepare your application. Applying for pre-approval and diligently shopping for rates are powerful tools that put you in control.

Remember, the ultimate goal is not just to get approved, but to secure a loan with terms that are beneficial and sustainable for your financial health. Take your time, do your homework, and apply these expert strategies. With careful preparation and a clear understanding of the process, you’ll be well on your way to driving off in your desired vehicle with confidence and peace of mind. Happy car hunting!