Drive Your Dreams: The Ultimate Guide to Navy Army Car Loans

Drive Your Dreams: The Ultimate Guide to Navy Army Car Loans Carloan.Guidemechanic.com

Navigating the world of car financing can feel like a complex journey, but securing the right loan is crucial for driving off in your dream vehicle. For many, especially those with ties to the military or specific communities, credit unions like Navy Army Community Credit Union offer a compelling alternative to traditional banks. Their car loans are renowned for competitive rates, personalized service, and a community-first approach.

This comprehensive guide will demystify Navy Army car loans, exploring everything from eligibility and application to maximizing your approval chances and understanding the finer points of their offerings. Our goal is to equip you with the knowledge to make an informed decision, ensuring a smooth and successful car buying experience.

Drive Your Dreams: The Ultimate Guide to Navy Army Car Loans

What Makes Navy Army Car Loans a Smart Choice?

When considering a Navy Army car loan, you’re looking at a financial product offered by a credit union, not a bank. This distinction is incredibly important. Credit unions are member-owned, non-profit organizations, which fundamentally changes their operational philosophy and, often, their loan products.

Unlike banks that aim to maximize profits for shareholders, credit unions like Navy Army focus on providing the best possible services and rates to their members. This cooperative model often translates into more favorable loan terms, lower interest rates, and a more personalized approach to customer service. It’s a financial institution built around its community.

The Credit Union Difference: Member-Centric Lending

At its core, a credit union is all about its members. When you become a member of Navy Army Community Credit Union, you’re not just a customer; you’re a part-owner. This structure means that any profits generated are typically returned to members in the form of lower loan rates, higher savings rates, and reduced fees.

This member-centric approach extends directly to their car loan offerings. They are often more flexible and understanding, especially when dealing with unique financial situations or those who might have less-than-perfect credit. Their mission is to serve, not just to profit.

Understanding Membership Eligibility

One of the most crucial aspects of securing a Navy Army car loan is meeting their membership eligibility requirements. Since credit unions are community-focused, their membership is typically restricted to specific groups or geographical areas. For Navy Army Community Credit Union, this usually includes:

- Active or retired military personnel and their families.

- Employees of specific companies or organizations within their service area.

- Individuals who live, work, worship, or attend school in designated counties in Texas.

- Family members of existing Navy Army members.

It’s essential to verify your eligibility before you even start the loan application process. You can easily do this by visiting their official website or contacting them directly. Don’t assume you qualify; always confirm.

The Distinct Advantages of a Navy Army Car Loan

Choosing a Navy Army car loan comes with a host of benefits that often set them apart from traditional lenders. These advantages are rooted in their credit union structure and commitment to member well-being. Understanding these can help you decide if it’s the right path for your auto financing needs.

Highly Competitive Interest Rates

Based on my experience in the financial sector, one of the primary draws of credit unions, including Navy Army, is their ability to offer remarkably competitive interest rates on car loans. Because they are not driven by shareholder profits, they can pass on savings directly to their members. This often means lower APRs compared to many big banks or dealership financing options.

A lower interest rate translates directly into significant savings over the life of your loan. Even a half-percentage point difference can save you hundreds, if not thousands, of dollars. Always compare their rates to other lenders to fully appreciate this benefit.

Personalized and Attentive Service

Another significant advantage is the personalized service you receive. Unlike large banks where you might feel like just another number, Navy Army Community Credit Union prides itself on building relationships with its members. This means you can often speak directly with a loan officer who understands your specific situation and can guide you through the process.

They are typically more willing to explain terms, answer questions, and work with you to find a solution that fits your budget. This level of personal attention can make a potentially stressful process much smoother and more transparent.

Flexible Loan Terms Designed for You

Navy Army often provides more flexible loan terms than many other lenders. They understand that every member’s financial situation is unique. This flexibility can manifest in various ways, such as:

- Adjustable Repayment Periods: Offering a wider range of loan durations, from shorter terms that save on interest to longer terms that lower monthly payments.

- Customizable Payment Schedules: Potentially allowing for bi-weekly payments or other arrangements that align with your pay cycle.

- Favorable Pre-Payment Options: Often without penalties, giving you the freedom to pay off your loan early if your financial situation improves.

This adaptability ensures that your Navy Army car loan can be tailored to meet your individual financial needs and goals.

Streamlined Pre-Approval Process

Pro tips from us: Always get pre-approved before you step foot in a dealership. Navy Army Community Credit Union offers a straightforward pre-approval process that can significantly empower you as a car buyer. Pre-approval means they’ve reviewed your credit and financial standing and have committed to lending you a certain amount at a specific interest rate.

Having a pre-approval letter in hand gives you immense leverage during negotiations. It tells the dealership you’re a serious buyer with financing already secured, allowing you to focus solely on the car’s price, not the financing terms. It truly puts you in the driver’s seat.

Understanding Navy Army Car Loan Eligibility: Beyond Membership

While membership is the first hurdle, securing a Navy Army car loan involves several other key eligibility factors that lenders, including credit unions, scrutinize. These factors help them assess your ability to repay the loan and determine the risk involved.

The Role of Your Credit Score

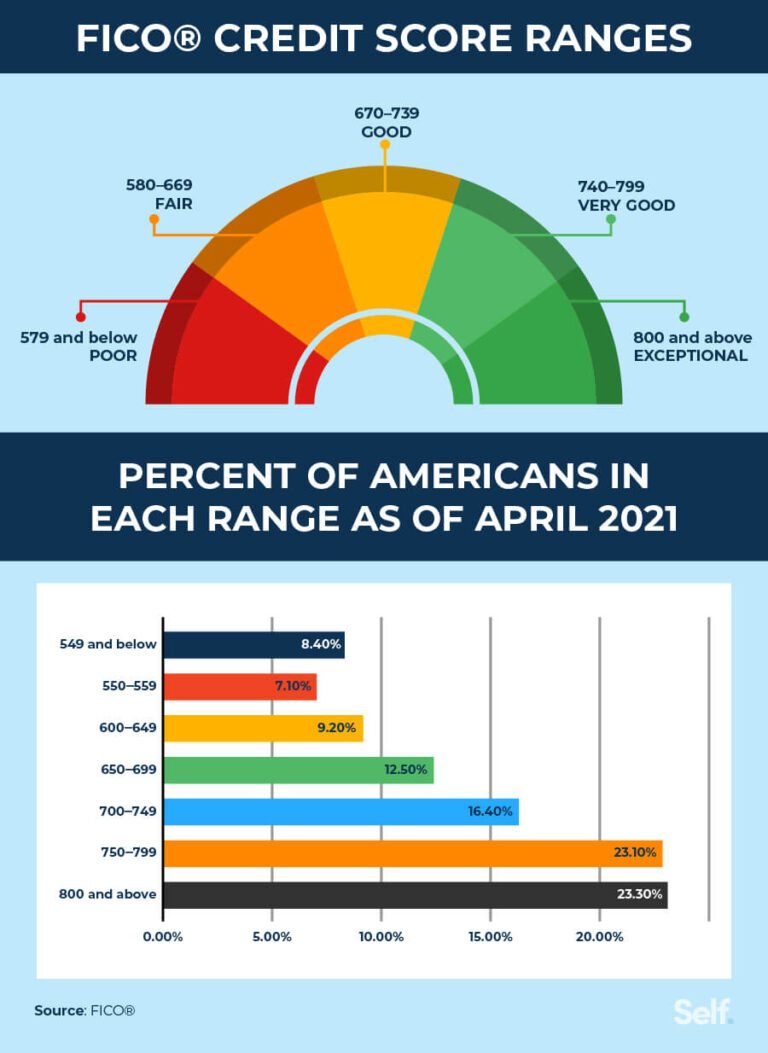

Your credit score is arguably the most critical factor in determining your loan eligibility and the interest rate you’ll receive. Lenders use this three-digit number to gauge your creditworthiness. A higher credit score (generally above 700) indicates a lower risk, often leading to the best rates and terms.

Conversely, a lower credit score doesn’t necessarily mean outright denial, especially with a credit union. Navy Army may be more willing to work with members who have fair or even some challenged credit, though you might face a slightly higher interest rate. They look at the overall picture, not just one number.

Income and Debt-to-Income Ratio

Lenders need assurance that you have a stable income sufficient to cover your monthly loan payments, along with your other financial obligations. Your debt-to-income (DTI) ratio is a key metric here. This ratio compares your total monthly debt payments to your gross monthly income.

A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a more attractive borrower. Navy Army will assess your income stability and your DTI to ensure the car loan payment won’t overextend your finances.

Vehicle Requirements and Age

The vehicle you intend to purchase also plays a role in loan eligibility. Lenders often have requirements regarding the age, mileage, and type of vehicle they will finance. For instance, very old vehicles or those with exceptionally high mileage might be considered higher risk.

Navy Army typically offers loans for new and used cars, trucks, and SUVs. They will usually require the vehicle to be appraised or valued to ensure the loan amount doesn’t exceed its market value. Always check their specific vehicle criteria before falling in love with a car.

The Step-by-Step Application Process for a Navy Army Car Loan

Applying for a Navy Army car loan is a structured process designed to be as clear as possible. Following these steps will help ensure a smooth application and increase your chances of approval.

Step 1: Confirming Your Membership Status

Before anything else, ensure you are an eligible member of Navy Army Community Credit Union. If you’re not yet a member, this will be your first step. You’ll typically need to open a savings account with a small minimum deposit (often $5-$25) to establish your membership.

This initial step is non-negotiable, as credit union services are exclusively for their members. Make sure you have all necessary identification and information ready for this.

Step 2: Gathering Essential Documents

Preparation is key to a swift application. Common documents and information required for a car loan include:

- Proof of Identity: Driver’s license, state ID, or passport.

- Proof of Income: Pay stubs, W-2s, or tax returns (for self-employed individuals).

- Proof of Residence: Utility bill or lease agreement.

- Social Security Number.

- Vehicle Information (if already chosen): VIN, make, model, year, mileage, and purchase price.

Having these documents organized and ready will prevent delays during your application.

Step 3: Deciding Between Pre-Approval and Full Application

You have two main avenues: applying for pre-approval or a full loan application. As mentioned, pre-approval is highly recommended. It gives you a clear budget and interest rate before you shop, strengthening your negotiating position.

If you already know the exact vehicle you want and are ready to purchase, you can proceed directly with a full application. However, a pre-approval often serves as a beneficial first step, allowing you to shop with confidence.

Step 4: Submitting Your Application

You can typically apply for a Navy Army car loan online, over the phone, or in person at one of their branches. The application form will ask for your personal, financial, and employment details. Be thorough and accurate in your responses.

A loan officer may contact you for additional information or clarification. Respond promptly to keep the process moving efficiently.

Step 5: Awaiting Decision and Funding

Once your application is submitted, Navy Army will review your information, conduct a credit check, and assess your financial standing. They will then notify you of their decision. If approved, you will receive details on your loan amount, interest rate, and terms.

Upon acceptance of the terms, the funds will be disbursed. For a car purchase, this usually means the funds are sent directly to the dealership or provided to you in the form of a cashier’s check.

Maximizing Your Chances of Navy Army Car Loan Approval

Even with competitive rates and member-focused service, getting approved for a Navy Army car loan requires strategic preparation. Here are some actionable steps you can take to present yourself as an ideal borrower.

Boost Your Credit Score Strategically

Your credit score is paramount. If you have time before applying, focus on improving it. This includes:

- Paying Bills on Time: Payment history accounts for a significant portion of your score.

- Reducing Existing Debt: Especially credit card balances. Lowering your credit utilization ratio (how much credit you’re using versus how much is available) can have a positive impact.

- Checking Your Credit Report: Obtain free copies from AnnualCreditReport.com and dispute any errors.

- Avoiding New Credit Applications: Multiple hard inquiries in a short period can temporarily lower your score.

A higher score signals reliability and can unlock better loan terms.

Implement a Smart Down Payment Strategy

Making a substantial down payment can significantly increase your chances of approval and secure better loan terms. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk.

Based on my experience, aiming for at least 10-20% of the vehicle’s purchase price is a strong strategy. It also reduces your monthly payments and lessens the likelihood of becoming "upside down" on your loan (owing more than the car is worth).

Efficiently Manage Your Existing Debt

Lenders scrutinize your debt-to-income (DTI) ratio. Before applying for a Navy Army car loan, try to pay down other high-interest debts, such as credit card balances or personal loans. This improves your DTI and demonstrates responsible financial management.

A lower DTI shows that you have more disposable income available to comfortably handle the new car payment, making you a more attractive borrower.

Pro Tips for a Strong Application

- Be Honest and Transparent: Always provide accurate information. Discrepancies can lead to delays or denial.

- Explain Any Financial Challenges: If you have past credit issues, be prepared to explain them. Credit unions are often more understanding if you can demonstrate a plan for improvement.

- Consider a Co-Signer (If Needed): If your credit score or income is borderline, a co-signer with excellent credit can significantly boost your approval chances and help you secure a better rate.

- Show Financial Stability: A consistent employment history and a steady income stream are strong indicators of your ability to repay.

Common Mistakes to Avoid When Applying for a Navy Army Car Loan

Even well-intentioned applicants can make missteps that hinder their chances of securing the best Navy Army car loan terms. Being aware of these common pitfalls can save you time, frustration, and money.

Not Verifying Membership Eligibility

Common mistakes to avoid are jumping into the application process without first confirming your eligibility for Navy Army Community Credit Union membership. This is a fundamental requirement. Attempting to apply without being a member will lead to an immediate rejection and wasted effort.

Always visit their website or call their member services to confirm if you meet their specific membership criteria before starting any loan paperwork.

Ignoring Your Credit Report and Score

Another frequent error is neglecting to check your credit report before applying. Many individuals are unaware of errors that might be dragging down their score. These inaccuracies, if left unaddressed, can unfairly impact your loan approval and interest rate.

Pull your free annual credit reports from all three bureaus (Experian, EquiFax, TransUnion) and dispute any discrepancies. Understanding your score also allows you to anticipate the rates you might qualify for.

Applying Blindly Without Pre-Approval

Applying for a car loan without first getting pre-approved is a significant tactical error. Without pre-approval, you walk into a dealership unsure of your financing power. This puts you at a disadvantage, as the dealership might focus on monthly payments rather than the total cost, or even mark up interest rates.

Pre-approval provides you with a concrete budget and a firm interest rate, empowering you to negotiate the car’s price more effectively. It separates the car buying process from the financing process.

Overlooking the Fine Print of Loan Terms

It’s easy to focus solely on the interest rate, but the loan terms encompass much more. Failing to understand the entire loan agreement can lead to unwelcome surprises down the road. Pay close attention to:

- Loan Term (Duration): Longer terms mean lower monthly payments but more interest paid over time.

- Fees: Are there any origination fees, application fees, or pre-payment penalties? Navy Army is known for transparency, but always check.

- Insurance Requirements: Some loans require specific types of auto insurance coverage.

Read every word of your loan agreement. If something is unclear, ask your Navy Army loan officer for clarification until you fully understand it.

Refinancing Your Existing Car Loan with Navy Army

Perhaps you already have a car loan, but you’re looking for better terms. Refinancing your existing auto loan with Navy Army Community Credit Union could be an excellent financial move. This involves taking out a new loan to pay off your current one, ideally at a lower interest rate or with more favorable terms.

When to Consider Refinancing

There are several compelling reasons to explore refinancing:

- Improved Credit Score: If your credit score has significantly improved since you first took out your original loan, you might qualify for a much lower interest rate now.

- Lower Interest Rates: Market rates may have dropped, or Navy Army might simply offer better rates than your current lender.

- Reduced Monthly Payments: Refinancing can extend your loan term, lowering your monthly outlay (though it might increase total interest paid).

- Desire for Different Terms: You might want to shorten your loan term to pay it off faster or remove a co-signer.

It’s always worth exploring your options if your financial situation or the market has changed.

Benefits of Refinancing with Navy Army

Refinancing with a Navy Army car loan can yield substantial benefits:

- Significant Savings: A lower interest rate directly translates to less money paid over the life of the loan.

- More Manageable Payments: By extending the loan term, you can free up cash flow each month.

- Simplified Finances: Consolidating your loan with a trusted institution like Navy Army.

- Access to Personalized Service: Enjoy the same member-focused approach for your refinanced loan.

Remember to factor in any potential fees associated with the new loan or your old loan to ensure the savings outweigh the costs.

The Refinancing Process

The process for refinancing a car loan with Navy Army is very similar to applying for a new loan:

- Check Eligibility: Ensure you meet Navy Army’s membership and credit requirements.

- Gather Documents: Prepare income proof, vehicle information (VIN, mileage, current loan balance), and personal identification.

- Apply for Refinancing: Submit your application, indicating it’s for refinancing.

- Review Offer: If approved, carefully review the new loan terms, comparing them to your current loan.

- Finalize: If you accept, Navy Army will pay off your old loan, and you’ll begin making payments to them.

Comparing Navy Army Car Loans to Other Options

To truly appreciate the value of a Navy Army car loan, it’s helpful to understand how they stack up against other common financing sources. Each option has its own set of pros and cons.

Banks vs. Credit Unions

- Banks: Typically larger, publicly traded institutions. They often have broader service offerings but can be less flexible with loan terms and may charge higher interest rates to meet profit goals. Their customer service can sometimes feel less personal.

- Credit Unions (like Navy Army): Member-owned, non-profit. Known for lower interest rates, fewer fees, and personalized service. Their membership requirements are a key distinction, and their focus is on member well-being rather than shareholder profits.

For car loans, credit unions often have a competitive edge in terms of rates and service.

Dealership Financing

- Pros: Convenient, one-stop shopping. Dealerships can sometimes offer promotional rates (especially for new cars).

- Cons: Often higher interest rates than credit unions or banks. The focus might be on the monthly payment rather than the total loan cost. They may also "mark up" the interest rate you qualify for to earn extra profit.

Pro tip: Always secure outside financing (like a Navy Army pre-approval) before discussing dealership financing. This gives you a benchmark and strengthens your negotiating power.

Online Lenders

- Pros: Fast application and approval process, often competitive rates, and convenience from home.

- Cons: Less personalized service, can be harder to negotiate terms. You might miss out on the community benefits and relationship building offered by a credit union.

While online lenders are an option, they often lack the human touch and dedicated support that Navy Army provides.

Frequently Asked Questions About Navy Army Car Loans

Here are some common questions we encounter regarding Navy Army car loans:

Q: Do I need excellent credit to get a Navy Army car loan?

A: While a good credit score will always secure the best rates, Navy Army is often more flexible than traditional banks. They may work with members who have fair or even some challenged credit, looking at your overall financial picture.

Q: How long does the Navy Army car loan application process take?

A: The application itself can be completed quickly online or in person. Approval times can vary, but many members receive a decision within 1-2 business days, especially if all required documents are readily available.

Q: Can I get a Navy Army car loan for a used car?

A: Yes, Navy Army Community Credit Union offers financing for both new and used vehicles. They will have specific criteria regarding the age and mileage of used cars they will finance.

Q: Are there any prepayment penalties with Navy Army car loans?

A: Based on my experience with credit unions, most do not charge prepayment penalties. This means you can pay off your loan early without incurring extra fees, saving you money on interest. Always confirm this in your specific loan agreement.

Q: What if I’m not a member yet? Can I still apply?

A: You must be an eligible member to apply for a loan. However, you can typically apply for membership and a loan concurrently. The first step is to establish your membership.

Conclusion: Driving Forward with Confidence

Securing a Navy Army car loan offers a compelling blend of competitive rates, flexible terms, and the unwavering support of a member-focused institution. By understanding the unique advantages of credit unions, meeting eligibility requirements, and approaching the application process strategically, you can significantly enhance your chances of driving away with the perfect vehicle and a loan that truly works for you.

Remember, preparation is your most powerful tool. Confirm your membership, gather your documents, and consider pre-approval to empower your car-buying journey. With Navy Army Community Credit Union, you’re not just getting a car loan; you’re gaining a financial partner dedicated to your success. Make an informed decision, and hit the road with confidence.

Internal Links (Hypothetical):

- For more tips on improving your credit score, check out our in-depth guide:

- Interested in other credit union benefits? Read our article on "The Ultimate Guide to Credit Union Membership"

External Link (Reputable Source):

- For more information on credit unions and their regulation, visit the National Credit Union Administration (NCUA) website: https://www.ncua.gov/