Drive Your Dreams: The Ultimate Guide to Securing a Belco Car Loan

Drive Your Dreams: The Ultimate Guide to Securing a Belco Car Loan Carloan.Guidemechanic.com

The open road, the scent of a new car, the freedom of independent travel – for many, owning a vehicle is more than just transportation; it’s a significant life milestone and a source of joy. But before you can hit the accelerator, there’s often one crucial step: securing the right financing. If you’re considering a Belco car loan, you’re on the path to making a smart financial decision.

As an expert in auto financing and a seasoned content creator, I’ve seen firsthand how confusing the loan process can be. That’s why I’ve crafted this super comprehensive guide. We’ll dive deep into everything you need to know about Belco auto financing, from understanding their unique approach as a credit union to navigating the application process with confidence. Our goal is to equip you with the knowledge to not only secure a Belco car loan but to do so on the best possible terms, ensuring a smooth ride from start to finish.

Drive Your Dreams: The Ultimate Guide to Securing a Belco Car Loan

Understanding Belco: Your Trusted Partner in Auto Financing

Before we delve into the specifics of their car loan offerings, it’s essential to understand what Belco is and why choosing a credit union like them can be a distinct advantage. Belco Community Credit Union isn’t just another financial institution; it’s a member-owned cooperative dedicated to serving its community.

This fundamental difference shapes their entire approach to lending, including their auto loans. Unlike traditional banks that prioritize shareholder profits, credit unions like Belco focus on providing value to their members through competitive rates, lower fees, and personalized service. This philosophy translates directly into tangible benefits for you as a borrower.

Based on my experience, credit unions often offer a more personalized touch. They tend to look beyond just your credit score, considering your overall financial picture and your relationship with them. This can be incredibly beneficial, especially if you have a unique financial situation or are looking for more flexibility. Their commitment to member well-being means they often work harder to find a solution that fits your needs, rather than a one-size-fits-all approach. This dedication to their members is a cornerstone of their service.

Why Choose a Credit Union for Your Car Loan?

Opting for a credit union like Belco for your vehicle financing comes with several compelling advantages. These benefits often make them a preferred choice for informed consumers.

Firstly, credit unions are renowned for offering some of the most competitive interest rates in the market. Because they are non-profit organizations, any surplus earnings are typically returned to members in the form of lower loan rates, higher savings rates, and reduced fees. This direct benefit to members can significantly lower the overall cost of your car loan over its lifetime.

Secondly, the member-centric approach fosters a more supportive and understanding lending environment. When you apply for a Belco car loan, you’re not just a number; you’re a part-owner of the institution. This often leads to more flexible underwriting standards and a willingness to work with borrowers who might have less-than-perfect credit histories, provided they demonstrate a commitment to responsible financial management.

Finally, the personalized service is a huge differentiator. At a credit union, you’re more likely to speak with a loan officer who takes the time to understand your financial goals and helps you navigate the options. This can be invaluable, especially if you’re a first-time car buyer or looking to refinance and need guidance on the best path forward.

Types of Belco Car Loans: Finding Your Perfect Match

Belco understands that one size doesn’t fit all when it comes to vehicle financing. They offer a range of car loan options designed to meet various needs, whether you’re buying new, used, or looking to refinance an existing loan. Understanding these options is the first step toward securing the best Belco car loan for you.

New Car Loans

If you’re dreaming of that brand-new car smell and the latest features, Belco’s new car loans are tailored for you. These loans typically come with favorable interest rates, reflecting the lower risk associated with financing a new vehicle. Lenders generally view new cars as more reliable and having a higher resale value.

With a new car loan from Belco, you can expect competitive terms that make your monthly payments manageable. The specific interest rate and loan term will depend on factors like your credit score, the loan amount, and the current market conditions. Belco aims to make the process straightforward, allowing you to focus on choosing the perfect new vehicle.

Used Car Loans

Purchasing a used car can be a smart financial move, offering excellent value and often lower insurance costs. Belco provides dedicated used car loans to help you finance your pre-owned vehicle purchase. While interest rates for used car loans might be slightly higher than for new cars, Belco still strives to offer competitive rates for its members.

It’s important to note that specific criteria for used car loans often include limits on the vehicle’s age and mileage. For instance, Belco might have policies on how old a vehicle can be or how many miles it can have to qualify for their best rates. Always confirm these details with a loan officer to ensure the used car you’re eyeing meets their requirements.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. Belco’s auto loan refinancing option could be exactly what you need. Refinancing involves taking out a new loan to pay off your existing car loan, often with the goal of securing a lower interest rate, reducing your monthly payment, or changing your loan term.

Pro tips from us: Refinancing can be particularly beneficial if your credit score has improved since you originally took out your loan, or if interest rates have dropped. It’s also a great option if you initially secured a high-interest loan and now qualify for more favorable terms. Belco can help you explore whether refinancing your current vehicle loan makes financial sense for your situation, potentially saving you a significant amount over the life of the loan.

Lease Buyout Loans

For those who are currently leasing a vehicle and have fallen in love with it, Belco also offers lease buyout loans. At the end of a lease term, you typically have the option to purchase the car for a pre-determined residual value. A lease buyout loan from Belco can help you finance this purchase, allowing you to keep the vehicle you’ve grown accustomed to.

This option can be a convenient way to transition from leasing to ownership, avoiding the hassle of finding a new car. Belco will assess your financial profile and the vehicle’s value to provide competitive financing for your lease buyout.

Navigating the Belco Car Loan Application Process: A Step-by-Step Guide

Securing a Belco car loan doesn’t have to be a daunting task. By understanding the application process, you can approach it with confidence and efficiency. Here’s a breakdown of the typical steps involved.

Step 1: Get Pre-Approved – Your Secret Weapon

The very first step you should consider, even before you start serious car shopping, is getting pre-approved for a loan. Pre-approval means Belco has conditionally agreed to lend you a certain amount of money at a specific interest rate, based on your financial information.

Based on my experience, pre-approval is your secret weapon in the car buying process. It empowers you by clearly defining your budget, allowing you to shop with confidence and focus on vehicles you can truly afford. Furthermore, it turns you into a cash buyer in the eyes of dealerships, giving you significant leverage in negotiations as you already have financing secured. This can often lead to a better overall deal on the vehicle itself.

Step 2: Gather Your Documents – Be Prepared

Once you decide to apply, whether for pre-approval or a direct loan, you’ll need to provide several key documents. Having these ready beforehand can significantly speed up the process.

Typically, you’ll need proof of identity (driver’s license, social security card), proof of income (pay stubs, W-2s, tax returns), proof of residency (utility bill, lease agreement), and information about the vehicle you intend to purchase (if known). For existing Belco members, some of this information may already be on file, streamlining the process even further.

Step 3: Submitting Your Application – Choose Your Method

Belco offers convenient ways to submit your loan application. You can typically apply online through their secure portal, which is often the quickest and most efficient method. Alternatively, you can visit a Belco branch in person to speak with a loan officer who can guide you through the application face-to-face.

Both methods have their advantages. Online applications offer speed and convenience, while in-person applications provide the opportunity for personalized assistance and immediate answers to your questions. Choose the method that best suits your comfort level and schedule.

Step 4: The Decision – Understanding What Happens Next

After submitting your application and all required documents, Belco’s lending team will review your financial profile. They will assess your creditworthiness, income, and debt-to-income ratio to determine your eligibility and the terms of your loan.

You will then receive a decision, which could be an approval, a conditional approval (requiring additional information), or a denial. If approved, you’ll receive an offer outlining your interest rate, loan term, and monthly payment. If denied, Belco should provide a reason, which can be valuable feedback for improving your financial standing for future applications. Understanding the decision allows you to move forward, whether that’s purchasing your car or working on areas for improvement.

Belco Car Loan Eligibility: Are You Ready to Drive?

Understanding the eligibility criteria for a Belco car loan is crucial for a successful application. While specific requirements can vary, several key factors generally influence whether you qualify and what terms you’re offered.

Your Credit Score: The Financial Report Card

Your credit score is arguably one of the most significant factors in loan approval and interest rate determination. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A higher credit score indicates a lower risk to lenders.

Belco, like most lenders, will use your credit score to gauge your reliability. While excellent credit will typically secure the best rates, credit unions are often more forgiving than traditional banks. They may be willing to work with individuals who have fair or even some past credit challenges, especially if you have a strong relationship with them or can demonstrate a commitment to improving your financial health. It’s always a good idea to check your credit score before applying, as this allows you to address any inaccuracies.

Income & Debt-to-Income Ratio: Demonstrating Repayment Ability

Lenders need assurance that you have the financial capacity to repay your loan. This is primarily assessed through your income and your debt-to-income (DTI) ratio. Your income should be stable and sufficient to cover your proposed monthly car payments, along with your other existing financial obligations.

The DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a less risky borrower. Belco will look for a DTI that suggests you can comfortably afford the new car loan payment without undue financial strain.

Membership Requirements: The Credit Union Difference

A fundamental requirement for obtaining a Belco car loan is typically being a member of Belco Community Credit Union. This is a standard practice for credit unions, as they serve their member-owners.

Becoming a Belco member is usually a straightforward process. It often involves meeting specific geographic or affiliation criteria (e.g., living, working, worshipping, or attending school in certain counties) and opening a basic savings account with a small initial deposit. If you’re not yet a member, don’t worry – you can usually apply for membership and a loan concurrently, simplifying the process.

Vehicle Requirements: What Kind of Car Qualifies?

The vehicle itself plays a role in loan eligibility, especially for used cars. Lenders consider the car’s age, mileage, and overall condition to assess its value and the risk associated with financing it.

For a new car, these requirements are typically minimal. For used vehicles, Belco may have specific guidelines, such as not financing cars older than a certain number of years (e.g., 10 years old) or with mileage exceeding a certain threshold (e.g., 100,000-120,000 miles). These limits help ensure the vehicle maintains sufficient value over the loan term. It’s always best to confirm these specific vehicle criteria directly with Belco to avoid any surprises.

Decoding Belco Car Loan Rates and Terms: What to Expect

When you’re comparing loan offers, it’s not just about the monthly payment. Understanding the interest rates, loan terms, and any associated fees is critical to making an informed decision about your Belco car loan.

Interest Rates: The Cost of Borrowing

The interest rate is the percentage charged by Belco for borrowing the principal amount of money. This is a key factor in determining the total cost of your loan over time. Several factors directly influence the interest rate you’ll be offered.

Your credit score is paramount; a higher score generally translates to a lower interest rate because you’re perceived as a lower risk. The loan term also plays a role; shorter terms often have slightly lower rates but higher monthly payments. Additionally, the loan amount and whether the vehicle is new or used can affect the rate. Belco aims to offer competitive rates, especially to members with strong credit profiles.

Loan Terms: Short vs. Long

The loan term is the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). Choosing the right loan term involves balancing your monthly payment with the total interest paid.

A shorter loan term (e.g., 36 or 48 months) will result in higher monthly payments but you’ll pay significantly less in total interest over the life of the loan. Conversely, a longer loan term (e.g., 60 or 72 months) offers lower monthly payments, making the car more affordable in the short term, but you’ll pay more in total interest due to the extended period of borrowing. Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost. Always calculate the total interest paid over different loan terms.

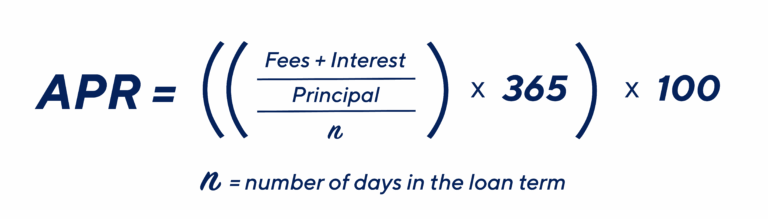

APRs vs. Interest Rates: A Crucial Distinction

While often used interchangeably, the Annual Percentage Rate (APR) and the interest rate are slightly different. The interest rate is simply the cost of borrowing the principal. The APR, however, represents the total annual cost of the loan, including the interest rate plus any additional fees or charges (like origination fees, if applicable).

The APR provides a more comprehensive picture of the true cost of borrowing. When comparing loan offers, always look at the APR, as it allows for a more accurate apples-to-apples comparison between different lenders. Belco strives for transparency in presenting both their interest rates and the overall APR.

Fees: Any Associated Costs?

While credit unions are known for lower fees, it’s always wise to inquire about any potential costs associated with your Belco car loan. These could include application fees, origination fees, or documentation fees.

Most reputable lenders, including Belco, will clearly disclose any such fees upfront. Make sure to ask your loan officer about any additional charges beyond the interest rate. Understanding all potential costs ensures there are no surprises down the road and helps you accurately budget for your new vehicle.

Maximizing Your Chances of Belco Car Loan Approval

Want to significantly increase your likelihood of getting approved for a Belco car loan on the best possible terms? Here are some actionable strategies from an expert perspective.

1. Improve Your Credit Score: Laying the Foundation

Your credit score is a powerful indicator of your financial responsibility. Before applying for a loan, take steps to improve it. This includes paying all your bills on time, reducing outstanding debt (especially on credit cards), avoiding opening new lines of credit, and checking your credit report for errors.

A higher credit score signals to Belco that you are a reliable borrower, which can lead to lower interest rates and a higher chance of approval. For more tips on boosting your credit score, check out our guide on .

2. Lower Your Debt-to-Income Ratio: Show You Can Afford It

As discussed, your DTI ratio is critical. Lenders want to see that your existing debt obligations don’t consume too much of your monthly income. Focus on paying down high-interest debts like credit card balances or personal loans.

Reducing your overall debt burden demonstrates to Belco that you have ample capacity to take on a new car payment. This financial prudence makes you a much more attractive borrower.

3. Save for a Down Payment: Reduce Risk, Increase Equity

Making a substantial down payment on your vehicle offers multiple benefits. Firstly, it reduces the amount you need to borrow, which means lower monthly payments and less interest paid over the life of the loan.

Secondly, a larger down payment immediately gives you equity in the vehicle, reducing the risk for Belco. This can make you a more appealing applicant and potentially qualify you for better loan terms. Aim for at least 10-20% of the vehicle’s purchase price if possible.

4. Shop Smart for Your Vehicle: Value Matters

Before applying for a loan, research the market value of the car you intend to buy. Negotiating a fair price for the vehicle directly benefits your loan application, as it means you’re not borrowing more than the car is worth.

Belco will also assess the vehicle’s value to ensure it aligns with the loan amount. Showing that you’ve done your homework and are making a sensible purchase decision can subtly reinforce your image as a responsible borrower.

Beyond Approval: Managing Your Belco Car Loan

Getting approved for your Belco car loan is a fantastic achievement, but the journey doesn’t end there. Responsible loan management ensures a smooth repayment period and can even save you money.

Setting Up Payments: Convenience and Consistency

Belco makes it easy to manage your loan payments. Most credit unions offer convenient options such as automatic payments (ACH) directly from your checking or savings account. This is a highly recommended approach as it ensures your payments are always made on time, helping you avoid late fees and maintaining a positive credit history.

You can also typically make payments online through Belco’s member portal, by phone, or in person at a branch. Choose the method that best fits your lifestyle, but prioritize consistency.

Making Extra Payments: Accelerate Your Savings

One of the smartest ways to save money on your car loan is to make extra payments whenever possible. Even small additional contributions can significantly reduce the principal balance, which in turn reduces the total interest you’ll pay over the life of the loan.

Pro tips from us: Consider rounding up your monthly payment, making bi-weekly payments (which results in one extra payment per year), or applying any unexpected windfalls (like a work bonus or tax refund) directly to your loan principal. Always confirm with Belco that extra payments will be applied to the principal and won’t incur any prepayment penalties (which are rare for credit union auto loans but always good to check).

Understanding Your Statements: Stay Informed

Regularly review your Belco car loan statements. These statements provide a detailed breakdown of your payments, how much went towards principal versus interest, your remaining balance, and the next payment due date.

Understanding your statements helps you track your progress and identify any discrepancies. It’s a key part of staying on top of your financial obligations and ensuring your loan is being managed correctly. To learn more about responsible credit management, a great resource is the Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/consumer-tools/auto-loans/.

Common Questions and Misconceptions About Belco Car Loans

Let’s address some frequently asked questions and clear up common misconceptions about securing a Belco car loan.

Can I get a Belco car loan with bad credit?

While a strong credit score definitely helps, "bad credit" isn’t an automatic disqualifier. Belco, as a credit union, is often more flexible and willing to work with members who have less-than-perfect credit. They may consider your overall financial history, your relationship with the credit union, and your ability to demonstrate repayment capacity. You might get approved, though potentially with a higher interest rate or requiring a larger down payment. It’s always worth applying and discussing your situation with a Belco loan officer.

What if I’m not a Belco member yet?

No problem! You can typically apply for Belco membership and a car loan at the same time. The process is usually integrated. You’ll need to meet their membership eligibility criteria (often based on geographic location or affiliation) and open a basic savings account, usually with a small initial deposit. Once you’re a member, you gain access to all their services, including competitive car loans.

How long does the approval process take?

The approval process for a Belco car loan can be quite efficient. If you have all your documents ready and apply online, you might receive a decision within a few hours or one to two business days. In-person applications might take a similar timeframe, depending on the complexity of your financial situation and the volume of applications. Pre-approval can often be even faster, giving you quick insight into your borrowing power.

Can I refinance a loan from another lender with Belco?

Absolutely! Belco’s auto loan refinancing service is designed specifically for this purpose. If you have an existing car loan with another financial institution, you can apply to refinance it with Belco. This is a popular option for members looking to secure a lower interest rate, reduce their monthly payments, or change their loan term, especially if their credit score has improved since the original loan was taken out.

Drive Away Confidently with a Belco Car Loan

Securing the right car loan is a cornerstone of responsible vehicle ownership. Throughout this comprehensive guide, we’ve explored the unique advantages of a Belco car loan, from their member-centric approach and competitive rates to the various loan types and the step-by-step application process. We’ve also armed you with strategies to maximize your approval chances and tips for effectively managing your loan.

Belco Community Credit Union stands out as a financial partner truly invested in its members’ success. By choosing a Belco car loan, you’re not just getting financing; you’re gaining a supportive relationship with an institution that prioritizes your financial well-being.

Don’t let the complexities of auto financing deter you from your dream car. With the insights provided here, you are now well-equipped to navigate the journey with confidence. Take the next step: explore Belco’s current car loan rates and speak with one of their knowledgeable loan officers today. Your ideal vehicle, backed by the ideal financing, awaits!