Drive Your Dreams: The Ultimate Guide to Securing a Citadel Car Loan

Drive Your Dreams: The Ultimate Guide to Securing a Citadel Car Loan Carloan.Guidemechanic.com

The journey to owning a new or used vehicle is often exhilarating, filled with anticipation for that first drive. However, the path to financing can sometimes feel like navigating a complex maze. This is where understanding your options becomes paramount, and for many, a Citadel Car Loan emerges as a beacon of clarity and value.

As an expert in automotive financing, I’ve seen firsthand how crucial it is to choose the right lending partner. A car loan isn’t just about monthly payments; it’s about securing a reliable financial solution that aligns with your goals and budget. In this comprehensive guide, we’ll dive deep into everything you need to know about securing a Citadel Car Loan, ensuring you’re empowered with the knowledge to make the best decision for your next set of wheels.

Drive Your Dreams: The Ultimate Guide to Securing a Citadel Car Loan

Why a Citadel Car Loan Stands Out in Today’s Market

When considering a car loan, you’re faced with numerous choices: big banks, online lenders, and credit unions. Citadel Credit Union, as a member-owned financial institution, offers a distinct advantage that often translates into significant benefits for its borrowers. They aren’t just a lender; they’re a community partner.

Based on my extensive experience in automotive financing, credit unions like Citadel frequently provide more competitive rates and personalized service compared to larger, profit-driven banks. Their fundamental mission is to serve their members, not shareholders. This member-centric approach is a cornerstone of the Citadel Car Loan experience.

They are known for their commitment to helping individuals achieve financial success, and this ethos is clearly reflected in their loan products. Whether you’re purchasing your very first car or looking to upgrade, understanding this core difference is the first step towards a smarter financing decision.

Unpacking the Citadel Car Loan Application Process: A Step-by-Step Blueprint

Securing a car loan might seem daunting, but Citadel simplifies the process considerably. Knowing what to expect at each stage can alleviate stress and ensure a smoother application. Let’s break it down.

Step 1: Pre-Approval – Your Power Play

The single most valuable piece of advice I can offer any car buyer is to get pre-approved for a loan before stepping foot in a dealership. A Citadel Car Loan pre-approval gives you a clear understanding of how much you can borrow and at what interest rate. This financial clarity empowers you to negotiate like a cash buyer.

With a pre-approval in hand, you walk into the dealership knowing your budget and financing terms. This shifts the focus from negotiating loan rates with the dealer to purely negotiating the vehicle price, putting you in a much stronger position. It’s a game-changer for many of my clients.

Step 2: Submitting Your Application

The actual application for a Citadel Car Loan is straightforward and can often be completed online, over the phone, or in person at a branch. You’ll typically need to provide personal information such as your name, address, Social Security number, and employment details. Financial information, including your income and existing debts, will also be requested to assess your repayment capability.

Pro tips from us: Have all your documentation ready before you start. This includes pay stubs, bank statements, and any other income verification. A well-prepared application signals to the lender that you are a serious and organized borrower.

Step 3: Underwriting and Approval

Once your application is submitted, Citadel’s loan officers will review your financial profile. This underwriting process involves assessing your credit history, income stability, and debt-to-income ratio. They’re looking for a clear picture of your ability to repay the loan responsibly.

In many cases, Citadel aims for quick decisions, often providing an answer within a short timeframe. If approved, you’ll receive an offer outlining the loan amount, interest rate, and term. This is where the personalized service of a credit union truly shines, as they may work with you to tailor terms if your initial application needs adjustment.

Step 4: Finalizing Your Loan and Driving Away

Upon approval, the final step involves signing the loan documents. This is a critical stage where you should carefully review all terms and conditions. Ensure that the interest rate, loan term, monthly payment, and any fees match what was discussed and approved.

Once the paperwork is signed, the funds are disbursed, and you’re officially ready to take ownership of your new vehicle. This seamless process is designed to get you into your dream car with minimal hassle, backed by the trusted support of Citadel.

Who Qualifies for a Citadel Car Loan? Key Requirements Demystified

Understanding the eligibility criteria is fundamental to a successful loan application. Citadel, like all lenders, has specific requirements designed to ensure responsible lending. Here’s what they typically look for.

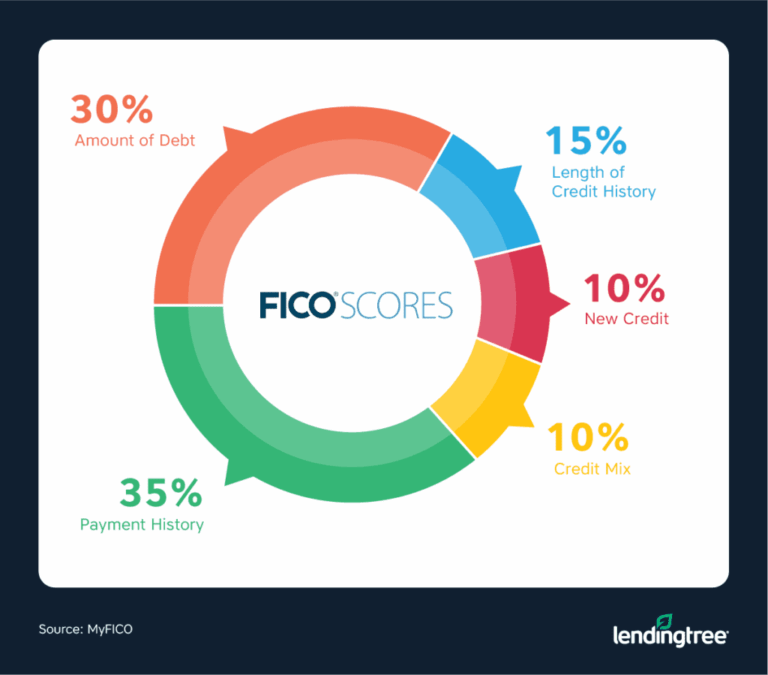

Credit Score: Your Financial Report Card

Your credit score is arguably the most significant factor in determining your eligibility and interest rate for a Citadel Car Loan. A higher credit score signals lower risk to lenders, often resulting in more favorable terms. While there isn’t a single "magic number," a score in the good to excellent range (typically 670 and above) will give you the best chances.

However, don’t be discouraged if your credit isn’t perfect. Citadel, being a credit union, often has more flexibility and may consider factors beyond just your score, such as your relationship with the institution or your overall financial history. It’s always worth discussing your specific situation with a loan officer. For more detailed information on improving your credit, consider reading our comprehensive guide on understanding your credit score. (Internal Link Placeholder: Link to "Understanding Your Credit Score: A Comprehensive Guide")

Income Stability and Debt-to-Income Ratio

Lenders want to see that you have a steady income stream that can comfortably cover your monthly loan payments, in addition to your other financial obligations. Your debt-to-income (DTI) ratio is a key metric here. This ratio compares your total monthly debt payments to your gross monthly income.

A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a more attractive borrower. Citadel will assess your DTI to ensure the car loan payment won’t overextend your finances, promoting responsible borrowing practices.

Citadel Membership Requirements

As a credit union, Citadel primarily serves its members. To qualify for a Citadel Car Loan, you’ll first need to become a member of Citadel Credit Union. Membership is typically open to individuals who live, work, worship, or attend school in specific counties (e.g., Southeastern Pennsylvania) or who are immediate family members of existing members.

Becoming a member is usually a simple process, often requiring a small deposit into a savings account. It’s a minor step that unlocks a world of member-exclusive benefits, including competitive loan rates and personalized financial services.

Vehicle Requirements: What Kind of Car Can You Finance?

Citadel provides financing for both new and used vehicles. However, there might be specific requirements for used cars, such as age and mileage limits, to ensure the vehicle retains sufficient value throughout the loan term. Generally, newer, lower-mileage used cars are easier to finance at more attractive rates.

Common mistakes to avoid are falling in love with a vehicle that doesn’t meet the lender’s criteria before checking. Always confirm any vehicle-specific requirements with Citadel early in your car search to prevent disappointment.

Navigating Interest Rates and Terms with Your Citadel Car Loan

Understanding the nuances of interest rates and loan terms is vital for managing your car loan effectively. These two factors profoundly impact your monthly payment and the total cost of your loan.

Factors Influencing Your Interest Rate

Several elements converge to determine the interest rate you’ll be offered for your Citadel Car Loan:

- Credit Score: As mentioned, a higher score typically leads to a lower rate.

- Loan Term: Shorter loan terms often come with slightly lower interest rates because the lender’s risk is reduced over a shorter period.

- Loan Amount: Larger loan amounts might sometimes qualify for slightly better rates, though this is not always a universal rule.

- Vehicle Type: New cars often secure lower rates than used cars due to their higher resale value and perceived reliability.

- Market Conditions: Overall economic conditions and the prime rate can also influence prevailing auto loan rates.

Based on my experience, even a small difference in your interest rate can save you hundreds, if not thousands, of dollars over the life of the loan. It pays to have a strong credit profile.

Choosing the Right Loan Term: Short vs. Long

Citadel offers various loan terms, typically ranging from 24 to 84 months. Your chosen term will directly affect your monthly payment and the total interest paid.

- Shorter Terms (e.g., 36-48 months): These result in higher monthly payments but significantly less total interest paid over the life of the loan. You pay off your car faster, building equity quicker.

- Longer Terms (e.g., 60-84 months): These offer lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay substantially more in total interest, and your car’s value may depreciate faster than you pay off the loan, leading to negative equity.

Pro tips from us: While a lower monthly payment is appealing, consider the total cost of the loan. Aim for the shortest term you can comfortably afford to minimize interest expenses and build equity faster.

Beyond New Purchases: Citadel Refinancing and Used Car Loans

A Citadel Car Loan isn’t just for buying a brand-new vehicle. They also offer excellent options for refinancing existing auto loans and financing used cars, catering to a broader range of financial needs.

Refinancing Your Existing Auto Loan with Citadel

Refinancing involves replacing your current car loan with a new one, often with more favorable terms. This can be a smart financial move if:

- Your Credit Score Has Improved: If your credit has significantly improved since you first took out your loan, you might qualify for a lower interest rate.

- Interest Rates Have Dropped: Market rates fluctuate. If current rates are lower than your original loan, refinancing could save you money.

- You Want a Lower Monthly Payment: By extending the loan term (though this increases total interest), you can reduce your monthly outlay.

- You Want to Shorten Your Loan Term: Conversely, if you want to pay off your car faster and can afford higher payments, you might refinance to a shorter term.

The benefits of refinancing can be substantial, from saving money on interest to freeing up cash flow each month. Our guide to car refinancing provides even more insights into this valuable option. (Internal Link Placeholder: Link to "The Ultimate Guide to Car Refinancing")

Securing a Used Car Loan from Citadel

Financing a used car comes with its own set of considerations. Citadel understands the used car market and offers competitive rates for pre-owned vehicles. Key factors for a used car loan include:

- Vehicle Age and Mileage: Lenders often have limits on the age or mileage of a used car they will finance. Older cars with high mileage are considered higher risk.

- Vehicle Value: The loan amount will be based on the car’s market value (e.g., NADA, Kelley Blue Book), not necessarily the sticker price.

- Inspection: It’s always a good idea to have a pre-purchase inspection by an independent mechanic, even when financing through a reputable lender like Citadel, to ensure you’re making a sound investment.

Citadel’s transparent approach to used car financing means you’ll understand all the terms upfront, helping you make a confident purchase.

Maximizing Your Citadel Car Loan Experience: Expert Tips

Navigating the car loan landscape can be complex, but with a few expert strategies, you can significantly enhance your experience and secure the best possible Citadel Car Loan.

1. Boost Your Credit Score Before You Apply

This is perhaps the most impactful step you can take. A higher credit score directly translates to lower interest rates. Before applying, review your credit report for errors, pay down existing debts, and make all payments on time. Even a few points can make a difference in your monthly payment and total interest.

Based on my experience, clients who dedicate a few months to credit improvement before applying often secure rates that save them thousands over the loan term. It’s an investment of time that truly pays off.

2. Save for a Healthy Down Payment

While a down payment isn’t always mandatory, making one can greatly benefit you. A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also shows the lender you’re serious about your commitment.

Furthermore, a larger down payment helps prevent you from being "upside down" on your loan, where you owe more than the car is worth, especially common with rapid depreciation in the first few years.

3. Thoroughly Research Vehicle Values

Before you even start negotiating with a dealership, know the fair market value of the car you’re interested in. Resources like Kelley Blue Book (KBB) or NADAguides provide excellent benchmarks for both new and used vehicles. This knowledge empowers you during negotiations and ensures you’re not overpaying.

This research also helps align your expectations with what Citadel might be willing to finance, preventing any surprises later in the process.

4. Understand the Fine Print

Once approved, you’ll receive a loan agreement. Do not rush through this document. Read every clause carefully. Pay close attention to the interest rate, annual percentage rate (APR), loan term, payment schedule, and any associated fees or penalties for late payments or early payoff.

Common mistakes to avoid are signing without fully comprehending the terms. If anything is unclear, ask your Citadel loan officer for clarification. They are there to help you understand every aspect of your Citadel Car Loan.

5. Communicate Openly with Loan Officers

Citadel’s loan officers are a valuable resource. If you have questions about the application, your eligibility, or the loan terms, don’t hesitate to reach out. Open communication can help resolve potential issues early and ensure a smooth process.

Their expertise can guide you through complex decisions, from choosing the right loan term to understanding the implications of different financing options. Leverage their knowledge!

Common Pitfalls to Avoid When Securing Any Car Loan

Even with the best intentions, borrowers can sometimes fall into traps that cost them money or lead to frustration. As an expert, I’ve seen these recurring issues.

Pitfall 1: Not Getting Pre-Approved

As discussed, skipping pre-approval puts you at a significant disadvantage at the dealership. You lose negotiating power on the car’s price and might end up accepting less favorable financing terms offered by the dealer, which may not always be in your best interest.

Pitfall 2: Focusing Only on the Monthly Payment

While your monthly payment is important, fixating solely on it can lead to problems. Dealers might extend the loan term to lower the payment, but this significantly increases the total interest you pay over time. Always consider the total cost of the loan and not just the immediate monthly outlay.

Pitfall 3: Ignoring the Total Cost of the Loan

Beyond the monthly payment, calculate the full amount you’ll pay back over the loan’s life. This includes the principal, all interest, and any fees. A seemingly low monthly payment over a very long term can result in a shockingly high total cost.

Pitfall 4: Forgetting About Insurance and Other Car Costs

The car loan payment is only one part of car ownership. Don’t forget to budget for insurance, maintenance, fuel, and potential repairs. Factor these into your overall monthly budget to ensure your chosen vehicle and loan are truly affordable.

Pitfall 5: Signing Without Understanding

Impatience or intimidation can lead borrowers to sign loan documents without fully grasping their contents. This can result in unexpected fees, unfavorable terms, or a misunderstanding of your obligations. Always take your time and ask questions until you’re completely clear.

The Citadel Difference: Why Choose a Credit Union for Your Car Loan?

The decision to choose a credit union like Citadel for your car loan is often rooted in their unique operational model and commitment to their members. This difference is substantial and worth exploring.

Citadel Credit Union operates as a not-for-profit financial cooperative. This means that instead of maximizing profits for external shareholders, their primary goal is to provide the best possible financial services and value to their members. Any earnings are typically reinvested into the institution to offer lower loan rates, higher savings rates, and reduced fees.

This structure often translates into more competitive interest rates for Citadel Car Loans compared to traditional banks. Furthermore, you’ll frequently find a more personalized and attentive customer service experience, as their staff are focused on building long-term relationships with members rather than just processing transactions.

The community focus of a credit union also means they are often more willing to work with members facing unique financial situations, potentially offering more flexible terms or guidance than larger, more rigid institutions. When you get a car loan from Citadel, you’re not just a customer; you’re a part-owner of the institution.

Getting Started with Your Citadel Car Loan Journey Today

Embarking on your car buying journey with a solid financing plan is a smart move. A Citadel Car Loan offers a pathway to vehicle ownership that is often more advantageous due to their competitive rates, flexible terms, and member-focused approach. They are committed to providing real value and support throughout the financing process.

Whether you’re looking for a new car, a reliable used vehicle, or considering refinancing your current auto loan, Citadel is equipped to help. Their transparent processes and dedicated loan officers ensure you receive the guidance you need every step of the way.

To explore your options further and begin the application process for your next car, we highly recommend visiting Citadel’s official auto loan page directly (External Link Placeholder: Link to Citadel’s official auto loan page, e.g., https://www.citadelbanking.com/personal/loans-credit/auto-loans). Their online resources and branch staff are ready to assist you in driving your dreams into reality.

Final Thoughts: Your Road to a Smarter Car Loan

Navigating the world of car financing doesn’t have to be a bumpy ride. By understanding the ins and outs of a Citadel Car Loan, from the application process and qualification requirements to optimizing your terms and avoiding common pitfalls, you’re well-equipped to make an informed and confident decision.

Remember, a car loan is a significant financial commitment. Choosing a partner like Citadel Credit Union, with its member-first philosophy and commitment to competitive rates, can make all the difference in your car ownership experience. Drive smart, drive confidently, and let Citadel help you get behind the wheel of your next vehicle.