Drive Your Dreams: The Ultimate Guide to Securing a Del-One Car Loan

Drive Your Dreams: The Ultimate Guide to Securing a Del-One Car Loan Carloan.Guidemechanic.com

Are you in the market for a new set of wheels, perhaps a reliable used car, or even looking to refinance your current auto loan for better terms? Navigating the world of car financing can often feel like a complex maze, with countless options and jargon. However, for many in Delaware and beyond, Del-One Credit Union stands out as a beacon of member-focused financial solutions.

This comprehensive guide is your ultimate roadmap to understanding everything about securing a Del-One car loan. We’ll delve deep into the benefits, application process, requirements, and expert tips to ensure you drive away with confidence. Our goal is to provide you with invaluable insights, making your car loan journey as smooth and successful as possible.

Drive Your Dreams: The Ultimate Guide to Securing a Del-One Car Loan

What Exactly is Del-One Credit Union? A Foundation of Trust

Before diving into the specifics of their car loans, it’s essential to understand the institution itself. Del-One Credit Union is a not-for-profit financial cooperative, meaning it’s owned by its members, not by external shareholders. This fundamental difference often translates into better rates, fewer fees, and a more personalized banking experience compared to traditional banks.

As a member-centric organization, Del-One’s primary focus is on serving the financial well-being of its community. Their profits are typically reinvested into the credit union to benefit members through improved services, lower loan rates, and higher savings yields. This cooperative model fosters a strong sense of community and mutual support among its members.

Becoming a member is usually straightforward, typically requiring a small deposit into a savings account and meeting specific eligibility criteria, such as living, working, or worshipping in certain areas. This membership is your gateway to a wide array of financial products, including their highly competitive auto loans.

Why Should You Consider a Del-One Car Loan? Unpacking the Advantages

When faced with numerous financing options, why might a Del-One car loan be an excellent choice for you? The advantages often extend beyond just competitive interest rates, encompassing a holistic approach to member service and financial support. Based on my experience observing various financial institutions, credit unions like Del-One often shine in several key areas.

Firstly, Del-One is renowned for offering highly competitive interest rates on their auto loans. Because they are not driven by shareholder profits, they can often pass savings directly onto their members in the form of lower Annual Percentage Rates (APRs). This can translate into significant savings over the life of your loan, reducing your monthly payments and overall cost of borrowing.

Secondly, the personalized service at Del-One is a frequently cited benefit. Unlike large, impersonal banks, credit unions often foster a more intimate relationship with their members. Loan officers are typically more accessible and willing to work with individuals to understand their unique financial situations, offering tailored advice and solutions. This human touch can make a substantial difference, especially if you have unique circumstances or questions.

Finally, Del-One is deeply rooted in its community. Choosing to finance with them means you’re supporting a local institution that genuinely invests in the economic health of the areas it serves. This community focus often translates into a more flexible and understanding approach to lending, aiming to help members achieve their financial goals rather than just maximizing profits.

A Closer Look at Del-One Car Loan Options: Tailored for Your Needs

Del-One understands that "one size fits all" simply doesn’t apply to car financing. They offer a diverse range of car loan products designed to meet various needs, whether you’re buying brand new, pre-owned, or looking to improve your existing loan terms. Knowing these options can help you determine the best path forward.

New Car Loans: Driving Off the Lot with Confidence

If you’re eyeing that brand-new model, Del-One’s new car loans are specifically designed to help you make that dream a reality. These loans typically come with very attractive rates and flexible terms, reflecting the lower risk associated with financing a new vehicle. You can often secure financing for up to 100% of the vehicle’s purchase price, sometimes even including taxes and fees.

The application process for new car loans is streamlined, allowing you to get pre-approved before you even step foot in a dealership. This pre-approval gives you significant negotiating power, as you walk in knowing exactly how much you can spend and what your interest rate will be. It transforms you from a mere shopper into a qualified buyer.

Used Car Loans: Smart Financing for Pre-Owned Vehicles

Buying a used car can be a smart financial move, and Del-One offers excellent financing options for pre-owned vehicles. While rates might be slightly higher than new car loans due to perceived higher risk, Del-One’s used car loan rates remain highly competitive. They understand the value of a well-maintained pre-owned vehicle and structure their loans accordingly.

Pro tips from us: When applying for a used car loan, having a clear understanding of the vehicle’s value (e.g., NADA or Kelley Blue Book) and its history (via a CarFax report) will strengthen your application. Del-One will often consider the age and mileage of the used vehicle when determining loan terms and amounts.

Car Loan Refinancing: Optimizing Your Existing Loan

Many people overlook the power of refinancing, but it can be a game-changer for your budget. If you secured your original car loan when your credit score wasn’t at its best, or if interest rates have dropped since then, refinancing with Del-One could save you a substantial amount of money. This involves taking out a new loan at a lower rate to pay off your existing, higher-interest loan.

Based on my experience, refinancing is particularly beneficial if you’ve significantly improved your credit score since your initial purchase, or if you want to reduce your monthly payments by extending the loan term. Del-One’s refinancing options are designed to provide financial relief and help you manage your budget more effectively.

Other Vehicle Loans: Beyond Cars

Del-One’s lending capabilities aren’t limited to just cars. They also offer financing for a variety of other vehicles, including motorcycles, RVs, boats, and even ATVs. This broad spectrum of loan products makes Del-One a versatile financial partner for all your recreational vehicle needs. Each type of loan will have its specific terms and conditions, so it’s always best to inquire directly with a loan officer.

Demystifying Del-One Car Loan Eligibility and Requirements

Securing any loan involves meeting specific criteria, and Del-One car loans are no exception. Understanding these requirements upfront can significantly streamline your application process and improve your chances of approval. While specific details can vary, here are the general pillars of eligibility.

Firstly, membership is paramount. As a credit union, you must be a member of Del-One Credit Union to qualify for their loans. As mentioned, this typically involves opening a basic savings account and meeting their field of membership requirements, which are often broad and inclusive.

Secondly, your credit score plays a critical role. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score (generally 670 and above) indicates a lower risk, leading to better interest rates and more favorable terms. Del-One, like other lenders, uses this as a key indicator.

Thirdly, income and employment stability are crucial. Del-One wants to ensure you have a steady source of income to comfortably make your monthly payments. They will typically ask for proof of income, such as pay stubs, W-2s, or tax returns. A stable employment history demonstrates reliability.

Finally, your debt-to-income (DTI) ratio is another important factor. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to cover new loan payments, making you a less risky borrower. Del-One will assess this to ensure the new car loan won’t overextend your finances.

The Del-One Car Loan Application Process: A Step-by-Step Walkthrough

Applying for a Del-One car loan doesn’t have to be intimidating. By understanding each step, you can approach the process with confidence and preparedness. Here’s a typical breakdown of what to expect.

Step 1: Become a Del-One Member. If you’re not already a member, this is your first stop. You can usually apply online or in person at one of their branches. This involves opening a savings account with a small minimum deposit and confirming your eligibility.

Step 2: Gather Your Documents. Before applying, collect all necessary paperwork. This commonly includes government-issued identification (driver’s license), proof of income (pay stubs, W-2s, tax returns), proof of residence (utility bill), and potentially information about the vehicle you intend to purchase (if known). Having these ready will prevent delays.

Step 3: Apply for the Loan. You can apply for a Del-One car loan online through their secure portal, over the phone, or in person at a branch. The application will ask for personal, employment, and financial information. Be thorough and accurate in your responses.

Step 4: Consider Pre-Approval. This is a highly recommended step. Applying for pre-approval means Del-One assesses your creditworthiness and provides you with an estimated loan amount and interest rate before you’ve chosen a car. This empowers you with a budget and negotiating leverage at the dealership.

Step 5: Loan Review and Decision. Once your application is submitted, Del-One’s lending team will review your financial profile, credit history, and supporting documents. They may contact you for additional information or clarification. This process can take anywhere from a few hours to a couple of business days, depending on the complexity of your application.

Step 6: Finalize the Loan. If approved, you’ll receive a loan offer detailing the terms, interest rate, and monthly payment. Once you accept, you’ll sign the necessary paperwork, and the funds will be disbursed. If you have a pre-approval, you can then take that approval to the dealership to complete your vehicle purchase.

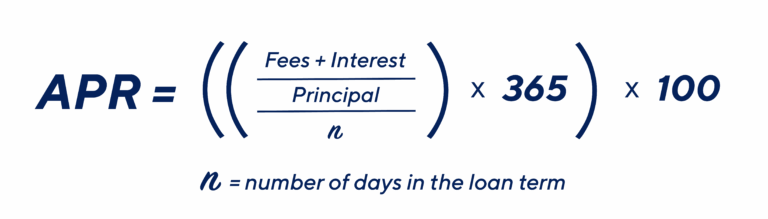

Understanding Del-One Car Loan Rates and Terms: What Influences Your Deal

The interest rate and terms of your Del-One car loan significantly impact your monthly payments and the total cost of your vehicle. Several factors come into play when Del-One determines these crucial elements. Being aware of them can help you optimize your loan.

Your credit score is arguably the most influential factor. Borrowers with excellent credit scores (typically 740+) usually qualify for the lowest interest rates, as they represent the lowest risk to the lender. Conversely, lower credit scores will generally result in higher rates to compensate for the increased risk.

The loan term, or the length of time you have to repay the loan, also affects your rate. Shorter loan terms (e.g., 36 or 48 months) often come with lower interest rates but higher monthly payments. Longer terms (e.g., 60 or 72 months) reduce your monthly payment but typically result in a higher overall interest paid and sometimes a slightly higher interest rate.

The age of the vehicle is another consideration. New cars generally qualify for lower rates than used cars, primarily because they are seen as having a longer lifespan and predictable value. Older used cars might carry slightly higher rates due to potential maintenance issues and depreciation.

Finally, the down payment amount can influence your rate. A larger down payment reduces the amount you need to borrow, which can sometimes lead to a slightly better interest rate because you’re financing less of the vehicle’s value. It also signals your financial commitment to the purchase.

Pro Tips for Del-One Car Loan Approval and the Best Rates

Securing a Del-One car loan isn’t just about meeting the minimum requirements; it’s about positioning yourself as an ideal borrower. Based on my experience in financial advisory, a few strategic moves can significantly enhance your approval chances and help you lock in the best possible rates.

1. Boost Your Credit Score: This is perhaps the most impactful step. Before applying, check your credit report for errors and dispute any inaccuracies. Pay down existing debts, especially credit card balances, to lower your credit utilization. Make all payments on time. Even a small improvement in your score can translate into substantial savings on interest.

2. Reduce Your Debt-to-Income Ratio: The less debt you carry relative to your income, the more attractive you are to lenders. Consider paying off small loans or credit card balances before applying for a car loan. This demonstrates your ability to manage debt responsibly and indicates you have ample room in your budget for new payments.

3. Save for a Down Payment: While not always mandatory, making a significant down payment reduces the amount you need to borrow and signals your financial commitment. It can also help you secure a lower interest rate and reduce your monthly payments, making the loan more affordable.

4. Get Pre-Approved: As mentioned, pre-approval is a powerful tool. It gives you a firm offer from Del-One, letting you know exactly what you can afford and at what rate. This allows you to shop for a car with confidence and negotiate like a cash buyer, focusing solely on the vehicle price, not the financing.

5. Gather All Documents in Advance: Nothing slows down a loan application like missing paperwork. Have your ID, proof of income, residence, and any other required documents organized and ready. This demonstrates your preparedness and ensures a smooth, efficient process.

Common Mistakes to Avoid When Applying for a Car Loan

Even with the best intentions, borrowers can sometimes make missteps that hinder their car loan application or lead to less favorable terms. Recognizing and avoiding these common mistakes can save you time, money, and frustration.

One common mistake we’ve observed is applying for too many loans in a short period. Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your credit score. While rate shopping for a car loan within a specific window (usually 14-45 days) counts as a single inquiry, excessive applications outside this window can be detrimental.

Another pitfall is not checking your credit report before applying. Errors on your credit report are surprisingly common and can negatively impact your score. By reviewing it beforehand, you can identify and dispute any inaccuracies, ensuring Del-One sees your true creditworthiness. This proactive step can prevent unnecessary rejections or higher interest rates.

Ignoring your budget and affordability is also a significant error. It’s easy to get caught up in the excitement of a new car, but it’s crucial to realistically assess what you can comfortably afford each month. Don’t just look at the monthly payment; factor in insurance, fuel, maintenance, and registration costs. Overextending yourself can lead to financial strain down the road.

Finally, not fully understanding the loan terms before signing is a critical mistake. Always read the fine print. Ask questions about the interest rate, loan term, any fees, prepayment penalties, and what happens if you miss a payment. Del-One’s loan officers are there to clarify, so don’t hesitate to ask. Ensuring you comprehend every detail protects your financial interests.

Maximizing Your Del-One Car Loan Experience: Beyond Approval

Getting approved for your Del-One car loan is a fantastic achievement, but your journey doesn’t end there. There are ways to ensure a positive and financially smart experience throughout the life of your loan. Building a strong relationship with your credit union can yield long-term benefits.

Consider setting up automatic payments for your car loan. This simple step ensures that your payments are always made on time, helping you avoid late fees and protecting your credit score. Consistent on-time payments are a cornerstone of good financial health and demonstrate reliability to lenders.

Furthermore, keep an open line of communication with Del-One if your financial situation changes. If you anticipate difficulty making a payment, reach out to them before you miss a deadline. Many credit unions, including Del-One, are willing to work with members facing temporary hardships, potentially offering solutions like payment deferrals or modified terms. Proactively addressing issues is always better than ignoring them.

Also, be aware of any opportunities for prepayment. If you find yourself with extra funds, making additional principal payments can significantly reduce the total interest you pay over the life of the loan. Del-One typically does not have prepayment penalties, allowing you the flexibility to pay off your loan faster if you choose.

Del-One Car Loan vs. Traditional Bank Loans: The Credit Union Difference

When it comes to car financing, the choice often boils down to a credit union like Del-One or a traditional bank. While both offer similar products, the underlying philosophy and operational structure create distinct differences that are worth considering. Understanding these can help you make an informed decision.

Credit unions, by their very nature, are member-owned. This means that any profits are returned to members in the form of lower loan rates, higher savings rates, and reduced fees. Banks, on the other hand, are typically for-profit entities, answerable to shareholders, which can sometimes lead to less competitive rates and higher fees to maximize profitability.

Based on my experience, Del-One often excels in offering personalized service. Loan officers at credit unions tend to have more autonomy and a deeper understanding of their members’ financial situations. This can be particularly beneficial if your credit history isn’t perfect, as they might be more willing to look beyond just the numbers and consider your overall financial picture. Banks, especially larger ones, often have more rigid lending criteria.

Furthermore, the community focus of Del-One is a significant differentiator. They are invested in the local economy and the financial well-being of their members. This often translates into a more flexible and understanding approach to lending, aiming to support you in achieving your goals rather than just processing transactions. For example, .

Frequently Asked Questions About Del-One Car Loans

To further assist you in your journey, let’s address some common questions prospective borrowers often have about Del-One car loans.

Q: Do I need excellent credit to get a Del-One car loan?

A: While a good credit score will always help you secure the best rates, Del-One often works with members across a range of credit profiles. Their member-centric approach means they may be more flexible than traditional banks. It’s always worth applying or speaking with a loan officer to discuss your options, even if your credit isn’t perfect.

Q: Can I get a Del-One car loan if I’m not a Delaware resident?

A: Del-One’s field of membership is primarily focused on Delaware residents, employees, or those who worship in specific counties. However, eligibility rules can sometimes extend to family members of existing members. It’s crucial to check their specific membership requirements on their official website (e.g., Del-One’s Official Website).

Q: How long does it take to get approved for a Del-One car loan?

A: The approval timeline can vary, but Del-One often prides itself on quick decisions. Many applicants receive a response within one business day, especially if all required documents are submitted promptly. Pre-approvals can sometimes be even faster.

Q: Are there any fees associated with Del-One car loans?

A: Del-One is known for its transparent fee structure, often having fewer and lower fees compared to traditional banks. However, specific fees might apply, such as late payment fees or processing fees. Always ask for a full disclosure of all potential costs before finalizing your loan.

Q: Can I use my Del-One car loan for a private party purchase?

A: Yes, Del-One typically offers financing for both dealership and private party car purchases. The process might involve a few extra steps for a private sale, such as ensuring the vehicle title is clear and arranging for payment directly to the seller. .

Drive Your Dreams Forward with Del-One

Securing a car loan is a significant financial decision, and choosing the right lender can make all the difference. Del-One Credit Union offers a compelling package of competitive rates, personalized service, and a genuine commitment to its members’ financial well-being. By understanding their offerings, preparing your application thoroughly, and utilizing the expert tips provided in this guide, you are well-equipped to navigate the process successfully.

Whether you’re purchasing a brand-new vehicle, a reliable used car, or looking to refinance for better terms, a Del-One car loan could be the key to unlocking your automotive dreams. Take the next step with confidence, knowing you have a dedicated partner in your corner. Visit Del-One’s website or a local branch today to begin your journey toward a new ride.