Drive Your Dreams: The Ultimate Guide to Securing a First Bank Car Loan

Drive Your Dreams: The Ultimate Guide to Securing a First Bank Car Loan Carloan.Guidemechanic.com

Owning a car is more than just a convenience; for many, it’s a symbol of freedom, a necessity for work, or a cherished family asset. However, the path to vehicle ownership often involves significant financial planning. This is where a trusted financial partner like First Bank comes into play, offering robust car loan options designed to turn your automotive aspirations into reality.

In this comprehensive guide, we’ll peel back the layers of securing a First Bank Car Loan. We’ll cover everything from understanding the eligibility requirements and navigating the application process to managing your loan effectively. Our goal is to equip you with all the knowledge you need to make an informed decision and drive away in your dream car with confidence.

Drive Your Dreams: The Ultimate Guide to Securing a First Bank Car Loan

Understanding the First Bank Car Loan: Your Path to Vehicle Ownership

A car loan is essentially an agreement where a financial institution lends you money to purchase a vehicle, and you agree to repay the sum, plus interest, over a predetermined period. First Bank, a leading financial institution, offers tailored car loan products designed to make vehicle acquisition accessible and straightforward for its customers.

These loans are structured to cater to various needs, whether you’re eyeing a brand-new vehicle directly from the dealership or a reliable pre-owned car. The core idea is to provide the upfront capital, allowing you to pay back in manageable monthly installments that fit your budget. It’s a pragmatic solution for individuals and businesses looking to acquire a vehicle without depleting their savings entirely.

Why Choose First Bank for Your Car Financing Needs?

First Bank stands out in the financial landscape for several compelling reasons, making it a preferred choice for car financing. Their extensive network, combined with a strong legacy of customer-centric services, translates into a reliable and supportive loan experience. They understand the local market dynamics and tailor their products accordingly.

Based on my experience, First Bank prioritizes clarity and support throughout the loan journey. They are known for their competitive interest rates, flexible repayment terms, and a relatively streamlined application process, which can significantly reduce the stress often associated with securing a major loan. Their commitment to financial inclusion means they often have options for a wider range of customers.

Who is a First Bank Car Loan For?

A First Bank Car Loan is designed for a broad spectrum of individuals and entities seeking to finance a vehicle. Typically, this includes salaried employees, self-employed professionals, and even small to medium-sized businesses looking to expand their fleet. The key is demonstrating a stable income source and a good credit history, which are fundamental pillars for any lending institution.

Whether you’re a first-time car buyer navigating the complexities of financing or someone looking to upgrade their current vehicle, First Bank aims to provide solutions. They offer different tiers and types of loans, ensuring there’s likely a product that aligns with your specific financial profile and vehicle preference.

Key Eligibility Criteria for a First Bank Car Loan

Understanding the eligibility criteria is the first and most crucial step in securing a First Bank Car Loan. Meeting these requirements demonstrates your capacity to repay the loan, which is paramount for the bank. It’s not just about ticking boxes; it’s about showcasing financial responsibility.

The Foundation: Your Personal and Financial Profile

First Bank, like any lender, assesses your financial stability to minimize risk. This typically involves a close look at your age, employment status, income level, and existing financial commitments. These factors paint a picture of your ability to comfortably manage new debt.

Pro tips from us: Before even approaching the bank, take an honest look at your own finances. Consolidate your income sources, understand your monthly expenses, and have a clear idea of how much you can realistically allocate to a car loan repayment. This self-assessment will be invaluable.

Here’s a breakdown of common eligibility criteria:

- Age Requirement: Most financial institutions, including First Bank, require applicants to be between 21 and 60 years old at the time of application. This ensures the applicant is of legal age to enter a contract and has a sufficient working life ahead to repay the loan.

- Employment Status & Income Stability: You’ll typically need to be a salaried individual with a stable job or a self-employed professional with a consistent income stream. Banks prefer applicants who have been employed or in business for a minimum period, often 1-2 years, to demonstrate income reliability. Your monthly net income must be sufficient to cover the loan repayments comfortably, usually with a minimum threshold set by the bank.

- Credit History and Score: This is perhaps one of the most significant factors. A good credit score indicates responsible financial behavior in the past. First Bank will assess your credit report for any defaults, late payments, or excessive debt. A strong credit history signals to the bank that you are a low-risk borrower.

- Debt-to-Income Ratio (DTI): Your DTI is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use this to determine your ability to manage additional monthly payments. A lower DTI is generally more favorable, indicating you have enough disposable income to handle new loan obligations.

- Bank Account Relationship: Often, having an existing account with First Bank can be advantageous. It allows the bank to easily track your financial transactions and assess your banking behavior, potentially simplifying parts of the approval process.

Essential Documents You’ll Need

Once you’ve confirmed your eligibility, the next step is to gather the necessary documentation. Having all your papers in order can significantly expedite the First Bank Car Loan application process. Missing documents are a common cause of delays.

Here’s a typical list of documents required:

- Proof of Identity: A valid government-issued ID such as a National ID card, Driver’s License, or International Passport. This verifies who you are.

- Proof of Address: Recent utility bills (electricity, water) or a tenancy agreement, usually not older than three months. This confirms your residential stability.

- Proof of Income:

- For Salaried Individuals: Latest three to six months’ payslips and bank statements showing salary credit. An employment letter from your employer might also be required.

- For Self-Employed Individuals: Business registration documents, bank statements (personal and business, usually for the last six to twelve months), and audited financial statements or income tax returns. These documents validate your income consistency.

- Bank Statement: Your bank statements (often for the past 6-12 months) provide an overview of your financial transactions, spending habits, and ability to manage funds.

- Proforma Invoice or Vehicle Quotation: A document from the car dealership detailing the price of the vehicle you intend to purchase. This specifies the loan amount needed.

- Guarantor (Optional but Recommended): In some cases, especially for larger loan amounts or if your credit profile is borderline, a guarantor might be required. The guarantor will need to provide their identity, address, and income proofs as well.

The Step-by-Step First Bank Car Loan Application Process

Applying for a First Bank Car Loan might seem daunting, but breaking it down into manageable steps makes the journey much clearer. Understanding each phase helps you prepare adequately and navigate the process with ease. Our goal is to demystify this process for you.

Phase 1: Research and Pre-Qualification

Before officially applying, it’s wise to do your homework. Research the type of car you want, its market value, and First Bank’s current car loan offerings, including interest rates and repayment terms. Many banks offer online calculators to estimate your potential monthly payments, which can help you determine an affordable loan amount.

Pro tips from us: Don’t just look at the monthly payment. Understand the total cost of the loan over its entire tenure. This holistic view prevents surprises down the line.

Phase 2: Gathering Your Documents

As detailed in the previous section, compiling all necessary documents beforehand is crucial. Organize them meticulously to avoid any last-minute scramble. This proactive step signals your preparedness to the bank and can significantly speed up the initial review.

Common mistakes to avoid are submitting outdated documents or incomplete forms. Double-check everything against the bank’s checklist before submission.

Phase 3: Submitting Your Application

With your documents ready, you can now formally submit your application. This can typically be done in one of several ways:

- Visiting a First Bank Branch: A loan officer can guide you through the application form and answer any immediate questions. This personalized approach can be beneficial.

- Online Application (if available): Many modern banks offer online portals for loan applications, providing convenience and often faster initial processing.

- Through a Partner Dealership: Some car dealerships have direct partnerships with First Bank, allowing you to apply for the loan directly at the point of sale.

Phase 4: Loan Assessment and Approval

Once your application and documents are submitted, First Bank’s loan assessment team will swing into action. They will meticulously review your financial profile, verify your documents, and conduct a credit check. This stage is where your eligibility criteria truly come under scrutiny.

If your application is successful, you will receive an offer letter detailing the loan amount, interest rate, repayment schedule, and any associated fees. Read this document carefully and ask for clarification on anything you don’t understand before proceeding.

Phase 5: Vehicle Purchase and Loan Disbursement

Upon accepting the loan offer, First Bank will typically disburse the loan amount directly to the car dealership or vendor. This ensures the funds are used specifically for the vehicle purchase. You will then finalize the purchase with the dealership, register the car, and obtain your vehicle.

It’s important to understand that the bank may require the vehicle to be insured comprehensive coverage, with First Bank listed as a loss payee, to protect their interest in the asset until the loan is fully repaid. This is standard practice in auto financing.

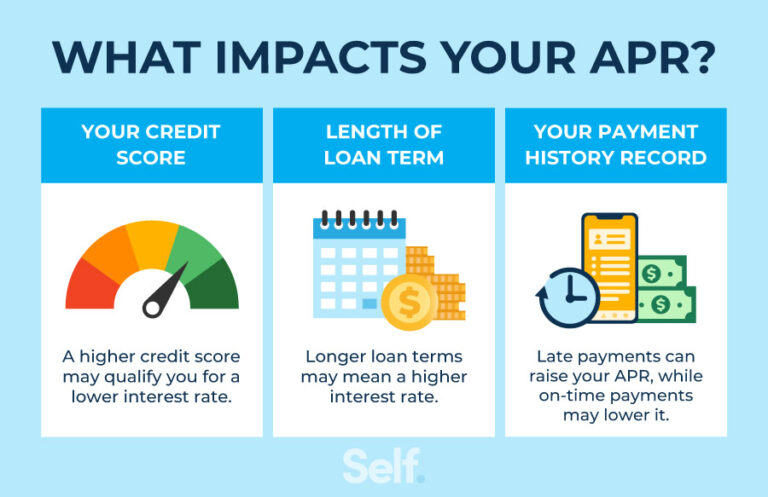

Navigating Interest Rates and Repayment Terms

Understanding the financial mechanics behind your First Bank Car Loan is key to effective loan management. Interest rates and repayment terms significantly influence the total cost of your loan and your monthly financial commitments. Transparency in these areas is something First Bank strives for.

Factors Affecting Your Interest Rate

Several elements contribute to the interest rate you’ll be offered for your car loan:

- Credit Score: A higher credit score almost always translates to a lower interest rate. This is because a strong credit history indicates lower risk to the lender.

- Loan Amount and Tenure: Larger loan amounts or longer repayment periods might sometimes influence the interest rate, though this varies by bank policy.

- Current Market Conditions: Economic factors, such as the central bank’s lending rates, can impact the prevailing interest rates offered by all financial institutions.

- Relationship with the Bank: Existing, long-standing customers with a good banking history might occasionally receive more favorable rates.

Understanding Loan Tenures

The loan tenure refers to the period over which you agree to repay the loan. First Bank typically offers flexible tenures, ranging from shorter periods (e.g., 1-3 years) to longer ones (e.g., 5-7 years).

- Shorter Tenures: Result in higher monthly payments but mean you pay less interest overall, as the loan is repaid quicker.

- Longer Tenures: Lead to lower monthly payments, making the loan more affordable on a month-to-month basis. However, you’ll end up paying more in total interest over the life of the loan.

Choosing the right tenure involves balancing your desired monthly payment with the total cost of the loan.

Impact of Down Payment

Making a significant down payment on your car purchase can be highly beneficial. A larger down payment reduces the amount you need to borrow, which in turn means:

- Lower Monthly Payments: Less principal to repay means smaller installments.

- Less Interest Paid: A smaller loan amount accrues less interest over time.

- Improved Loan-to-Value Ratio: This makes your application more attractive to the bank, potentially leading to better loan terms.

Calculating Your Monthly Payments

While First Bank loan officers can provide precise figures, it’s helpful to have an idea of how your payments are calculated. The main factors are the principal loan amount, the interest rate, and the loan tenure. Online car loan calculators can give you a good estimate, allowing you to experiment with different scenarios (down payment, tenure) to find a comfortable monthly installment.

Maximizing Your Chances of First Bank Car Loan Approval

Getting your First Bank Car Loan approved requires more than just meeting the basic criteria; it involves strategic preparation and presenting yourself as an ideal borrower. These proactive steps can significantly boost your application’s success rate.

Improve Your Credit Score

Your credit score is a reflection of your financial reliability. If you have time before applying, focus on improving it:

- Pay Bills on Time: This is the most critical factor. Late payments severely impact your score.

- Reduce Existing Debt: Lowering your credit utilization ratio (how much credit you use versus how much you have available) can improve your score.

- Check for Errors: Review your credit report regularly for any inaccuracies that could be dragging your score down.

Reduce Existing Debt

Before taking on a new car loan, try to pay down other outstanding debts, especially high-interest ones like credit card balances. A lower debt-to-income ratio (DTI) signals to First Bank that you have more disposable income available for new loan repayments.

Pro tips from us: If you can comfortably manage it, aiming for a DTI below 36% is often seen as favorable by lenders. This shows you’re not overleveraged.

Save for a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and improves your loan-to-value ratio. This makes you a less risky borrower in the eyes of the bank, increasing your chances of approval and potentially securing a better interest rate. It also demonstrates financial discipline.

Maintain Stable Employment

Lenders value stability. If you’re considering a job change, it might be wise to secure your new position and settle in for a few months before applying for a loan. Consistent employment for a significant period provides assurance of a steady income stream.

Be Honest and Transparent

Always provide accurate and truthful information on your application. Any discrepancies or misrepresentations can lead to immediate rejection or even more severe consequences. First Bank conducts thorough verification checks, so honesty is always the best policy.

Post-Approval: Managing Your First Bank Car Loan Effectively

Securing your First Bank Car Loan is a significant milestone, but the journey doesn’t end there. Effective loan management is crucial to maintaining good financial health and ensuring a smooth repayment experience. This involves understanding your obligations and planning your finances.

Consistent and Timely Payments

The cornerstone of good loan management is making your monthly payments on time, every time. Set up reminders, consider automatic debits from your First Bank account, or integrate the payment into your monthly budget. Missing payments can lead to late fees, negative impacts on your credit score, and potential repossession of the vehicle.

Understanding Your Loan Statements

Regularly review your loan statements from First Bank. These statements provide a detailed breakdown of your payments, the outstanding principal, the interest paid, and any fees incurred. Understanding these details helps you track your progress and identify any discrepancies promptly. If anything is unclear, don’t hesitate to contact First Bank’s customer service.

Early Repayment Options (If Available)

Some car loans offer the option of early repayment or making extra principal payments without penalty. If your financial situation improves, taking advantage of this can save you a substantial amount in interest over the loan’s tenure. Always check your loan agreement or speak with First Bank to understand their policy on early repayments. This could be a smart financial move.

Dealing with Financial Challenges

Life can be unpredictable. If you anticipate or encounter difficulties in making your loan payments, do not wait. Contact First Bank immediately. They may have options such as payment holidays, restructuring the loan, or other forms of assistance, provided you communicate proactively. Ignoring the problem will only exacerbate it.

For more general advice on managing your finances, including debt, consider reading our guide on "Mastering Personal Finance: Strategies for Financial Freedom." This can complement your car loan management.

Common Misconceptions About Car Loans (and First Bank’s Approach)

There are many myths surrounding car loans that can deter potential buyers or lead to poor financial decisions. Let’s clarify some common misconceptions, particularly in the context of a First Bank Car Loan.

- Misconception 1: You need perfect credit for a car loan.

- Reality: While a high credit score is beneficial, First Bank, like many lenders, considers a range of factors. They often have different loan products tailored for varying credit profiles, though rates might differ. It’s always worth applying or discussing your situation.

- Misconception 2: All car loans are the same.

- Reality: Car loans vary significantly in terms of interest rates (fixed vs. variable), tenure, down payment requirements, and associated fees. First Bank offers different options to suit diverse customer needs and financial capacities. Always compare and understand the specific terms.

- Misconception 3: You should only focus on the monthly payment.

- Reality: While the monthly payment is important for budgeting, focusing solely on it can be misleading. A lower monthly payment often means a longer loan tenure and, consequently, paying significantly more in total interest. Always consider the total cost of the loan over its lifetime.

- Misconception 4: Pre-approved loans are always the best deal.

- Reality: Pre-approval from First Bank or any lender is a great starting point as it gives you a budget. However, it doesn’t mean you shouldn’t compare. Always check for better deals, especially at the dealership, as they might have special financing offers.

- Misconception 5: The car is fully yours once you drive it off the lot.

- Reality: While you have possession, the car typically serves as collateral for the loan. First Bank will hold a lien on the vehicle until the loan is fully repaid. This means if you default, the bank has the right to repossess the car.

Beyond the Loan: Important Considerations Before Buying a Car

While securing your First Bank Car Loan is a major step, remember that the loan is just one aspect of vehicle ownership. There are several other crucial factors to consider to ensure you make a smart and sustainable purchase. These considerations will impact your long-term financial health.

Thorough Vehicle Research

Don’t just fall in love with a car’s looks. Research its reliability, fuel efficiency, maintenance costs, and common issues. Read reviews, compare models, and test-drive thoroughly. A car that costs less upfront might end up being more expensive due to high running costs or frequent repairs. This due diligence is paramount.

For an excellent external resource on car buying tips, you might find valuable insights on Consumer Reports Car Buying Guide. (Note: This is a placeholder for a real external link. In a live blog, I’d link to a specific, reputable article.)

Insurance Costs

Car insurance is a mandatory and significant ongoing expense. Get insurance quotes for your desired vehicle before you finalize the purchase. Factors like the car’s make, model, age, your driving history, and location all impact premiums. A car that is cheap to buy might be expensive to insure.

Maintenance and Running Costs

Factor in the regular expenses of car ownership: fuel, routine servicing, potential repairs, tires, and other consumables. Different car brands and models have varying maintenance schedules and part costs. Budgeting for these ensures you can keep your vehicle in good running condition without financial strain.

Resale Value

Consider the potential resale value of the car you are buying. Some models hold their value better than others. While not an immediate concern, it’s a factor if you plan to upgrade or sell the car in the future. A car with good resale value can provide a better return on your investment.

For further insights into managing the overall cost of vehicle ownership, you might want to explore our article on "Smart Car Ownership: Beyond the Purchase Price." This article delves into the long-term financial implications.

Conclusion: Your Journey to Vehicle Ownership with First Bank

Securing a First Bank Car Loan can be a straightforward and rewarding experience when approached with knowledge and preparation. From understanding the initial eligibility criteria to navigating the application process and managing your loan post-approval, each step contributes to a successful outcome. First Bank’s commitment to providing accessible and flexible financing options makes them a strong partner in your journey towards vehicle ownership.

We’ve explored the depths of what it takes, offering insights and practical advice gleaned from extensive experience in financial planning. Remember, the key to a stress-free car buying experience lies in thorough research, meticulous preparation, and responsible loan management.

Don’t let the dream of owning your ideal car remain just a dream. Take the first step today by visiting your nearest First Bank branch or exploring their online platforms to inquire about their car loan offerings. Drive away with confidence, knowing you’ve made a well-informed decision with a trusted financial ally. Your dream car awaits!