Drive Your Dreams: The Ultimate Guide to Securing a Kinecta Car Loan

Drive Your Dreams: The Ultimate Guide to Securing a Kinecta Car Loan Carloan.Guidemechanic.com

Purchasing a new or used vehicle is often one of the most significant financial decisions many of us make. It’s an exciting time, filled with the promise of new adventures on the open road. However, securing the right financing can feel like navigating a complex maze, with countless lenders, rates, and terms to consider. This is where a trusted partner like Kinecta Federal Credit Union can make all the difference.

As an expert in financial content, I’ve seen firsthand how choosing the right Kinecta Car Loan can impact your budget and overall financial health. This comprehensive guide will peel back the layers, offering you an in-depth look at everything you need to know about Kinecta’s auto financing options. Our goal is to empower you with the knowledge to make an informed decision, ensuring a smooth and advantageous car buying experience.

Drive Your Dreams: The Ultimate Guide to Securing a Kinecta Car Loan

Why Consider a Kinecta Car Loan? The Credit Union Advantage

When it comes to vehicle financing, many consumers automatically think of big banks or dealership financing. However, credit unions like Kinecta Federal Credit Union offer a distinct advantage that’s often overlooked. They are member-owned, meaning their primary focus is on serving their members, not maximizing profits for shareholders.

This fundamental difference often translates into several tangible benefits for borrowers. From competitive interest rates to personalized service, a Kinecta Car Loan often stands out in a crowded market. It’s about more than just a loan; it’s about being part of a community that genuinely cares about your financial well-being.

Competitive Rates and Flexible Terms

One of the most compelling reasons to explore a Kinecta auto loan is their reputation for offering highly competitive interest rates. Credit unions are often able to pass on savings to their members because they operate on a not-for-profit basis. This can translate into significant savings over the life of your car loan.

Beyond attractive rates, Kinecta also understands that every borrower’s financial situation is unique. They typically offer a range of flexible loan terms, allowing you to choose a payment plan that comfortably fits your budget. Whether you prefer a shorter term to pay off your vehicle faster or a longer term to reduce your monthly payments, Kinecta strives to provide options.

Member-Centric Service and Support

Based on my experience, dealing with a credit union like Kinecta is often a more personal and pleasant experience. Unlike larger institutions, Kinecta prides itself on its member-centric approach. This means you’re not just another loan application; you’re a valued member of their community.

Their dedicated loan officers are often more willing to work with you, understand your specific needs, and guide you through the process with clarity and empathy. This level of support can be incredibly reassuring, especially for first-time car buyers or those who might feel overwhelmed by the financing process.

Unlocking the Door: Understanding Kinecta Membership Eligibility

Before you can apply for a Kinecta Car Loan, you first need to become a member of Kinecta Federal Credit Union. This is a standard requirement for all credit unions, as their services are exclusively for their members. The good news is that Kinecta has made membership accessible to a broad range of individuals.

Understanding the eligibility criteria is your first step towards securing favorable auto financing. It’s a straightforward process, but knowing the specifics beforehand can save you time and effort.

Who Can Join Kinecta Federal Credit Union?

Kinecta’s field of membership is quite extensive, typically covering individuals who:

- Live, Work, or Worship in Specific Areas: Primarily Los Angeles County, Orange County, San Bernardino County, Ventura County, Santa Barbara County, Kern County, and San Diego County in California. They also serve certain areas in Arizona and Florida.

- Are Employed by Select Employer Groups: Kinecta partners with numerous companies and organizations, making their employees eligible for membership.

- Are Family Members of Current Kinecta Members: If a direct relative (spouse, child, sibling, parent, grandparent, grandchild) is a Kinecta member, you may also be eligible to join.

It’s always a good idea to visit Kinecta’s official website or contact them directly to confirm your specific eligibility. Membership is often easier to obtain than many people assume.

How to Become a Kinecta Member

Becoming a Kinecta member is a simple process. Once you’ve confirmed your eligibility, you’ll typically need to:

- Open a Share Savings Account: This is your primary membership account and usually requires a minimum deposit, often as low as $5. This small deposit signifies your ownership share in the credit union.

- Provide Identification: You’ll need to provide standard identification documents, such as a government-issued ID (driver’s license or passport) and your Social Security number.

- Complete the Application: Fill out the membership application, either online or in person at a branch.

Once your membership is established, you gain access to all of Kinecta’s financial products and services, including their attractive Kinecta auto loan options. This initial step is a small investment for potentially significant long-term benefits.

Your Options: Types of Kinecta Car Loans Available

Kinecta Federal Credit Union offers a diverse portfolio of car loan products designed to meet various needs and situations. Whether you’re buying a brand-new vehicle, a pre-owned gem, or looking to save money on an existing loan, Kinecta likely has a solution for you. Understanding these options is crucial for making the best choice.

Based on my experience in the auto finance sector, having multiple options ensures that your financing aligns perfectly with your vehicle and financial goals.

New Car Loans

If you’re eyeing that shiny new model straight from the dealership, Kinecta’s new car loans are tailored for you. These loans typically come with some of the most competitive rates and favorable terms, reflecting the lower risk associated with brand-new vehicles.

- Key Features: Attractive interest rates, flexible terms, and financing for vehicles directly from the manufacturer.

- Pro Tip: Even if the dealership offers financing, always compare it with a Kinecta Car Loan pre-approval. You might be surprised by the savings.

Used Car Loans

Purchasing a used car can be a smart financial move, and Kinecta supports this with dedicated used car loan options. These loans are available for pre-owned vehicles, though there might be specific age or mileage limits.

- Key Features: Competitive rates for pre-owned vehicles, often with similar flexibility in terms as new car loans.

- Common Mistakes to Avoid: Don’t assume older vehicles automatically mean higher rates. Kinecta evaluates used cars individually, and a good condition vehicle can still qualify for excellent terms.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for a better deal. Kinecta auto loan refinance options can be a game-changer. Refinancing involves replacing your current car loan with a new one, ideally with more favorable terms.

- Why Refinance? Lower interest rates, reduced monthly payments, or shortening your loan term to pay off debt faster.

- When to Consider: If your credit score has improved since you first took out your loan, if market rates have dropped, or if you want to adjust your monthly budget.

- Internal Link: To delve deeper into the benefits and process, check out our detailed article: The Smart Way to Refinance Your Auto Loan for Maximum Savings (Simulated Internal Link).

Lease Buyout Loans

If your vehicle lease is nearing its end and you’ve fallen in love with your car, a lease buyout loan from Kinecta can help you purchase it. This converts your leased vehicle into an owned asset.

- Process: Kinecta will finance the residual value of the vehicle, allowing you to keep it without returning it to the dealership.

- Benefit: Avoid mileage penalties and keep a vehicle you’re already familiar with and enjoy.

Pre-Approval: Your Secret Weapon

One of the most powerful tools in your car buying arsenal is Kinecta car loan pre-approval. This process allows you to get approved for a specific loan amount before you even step foot on a dealership lot.

- Advantages:

- Budget Clarity: You know exactly how much you can afford, preventing overspending.

- Negotiating Power: You walk into the dealership as a cash buyer, giving you leverage to negotiate the vehicle price without the pressure of financing.

- Peace of Mind: Reduces stress and streamlines the purchase process.

Based on my experience, securing pre-approval is a game-changer. It transforms you from a vulnerable buyer to a confident negotiator.

The Kinecta Car Loan Application Process: A Step-by-Step Guide

Applying for a Kinecta Car Loan is designed to be as straightforward as possible, ensuring a smooth journey from application to approval. While the specifics can vary slightly depending on the loan type and your individual circumstances, the general outline remains consistent.

Following these steps meticulously can significantly expedite your application and improve your chances of approval. Preparation is key!

Step 1: Gather Your Documentation

Before you begin the application, having all necessary documents readily available will save you time. Common documents required include:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Residency: Utility bill, lease agreement.

- Proof of Income: Recent pay stubs, W-2s, tax returns (if self-employed).

- Social Security Number.

- Vehicle Information (if applicable): VIN, make, model, year, mileage, and purchase price.

Ensure all documents are current and accurately reflect your information. Incomplete applications can lead to delays.

Step 2: Apply for Pre-Approval (Highly Recommended)

As discussed, Kinecta pre-approval is highly recommended. You can typically apply for pre-approval online, over the phone, or in person at a Kinecta branch. This initial application will involve providing personal and financial information, and Kinecta will perform a credit check.

The pre-approval process gives you a clear understanding of the loan amount you qualify for and the potential interest rate, empowering you before you start car shopping.

Step 3: Formal Application Submission

Once you’ve found the perfect vehicle, you’ll finalize your loan application. If you have a pre-approval, this step is usually quicker. You’ll provide the specific details of the vehicle you intend to purchase, and Kinecta will confirm all information.

This is also the stage where you’ll review and agree to the final terms of your Kinecta Car Loan, including the interest rate, loan term, and monthly payment.

Step 4: Credit Review and Decision

Kinecta’s lending team will review your application, credit history, income, and debt-to-income ratio. They use this information to assess your creditworthiness and determine the final loan offer.

- Pro Tip: Make sure your credit report is accurate before applying. You can get a free copy from annualcreditreport.com. Any discrepancies should be addressed promptly. (External Link: https://www.annualcreditreport.com)

Step 5: Loan Closing and Funding

Upon approval, you’ll sign the necessary loan documents. Once all paperwork is complete, Kinecta will disburse the funds directly to you or the dealership, completing your vehicle purchase. The process is streamlined to get you into your new vehicle as quickly as possible.

Eligibility and Requirements for a Kinecta Car Loan

Securing a Kinecta Car Loan hinges on meeting certain eligibility criteria. While credit unions are often more flexible than traditional banks, understanding these requirements upfront can significantly boost your chances of approval.

These factors help Kinecta assess your ability to repay the loan and determine the most appropriate loan terms for your situation.

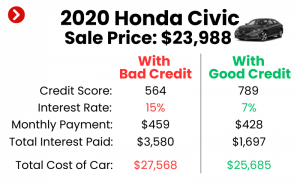

Credit Score Expectations

Your credit score is a major factor in determining your loan approval and the interest rate you receive. Generally, a good to excellent credit score (typically 670 and above) will qualify you for the most competitive Kinecta auto loan rates.

- For excellent credit (740+): You can expect the best possible rates and terms.

- For good credit (670-739): Still qualify for very good rates, possibly with a slightly higher APR.

- For fair credit (580-669): Approval is still possible, but rates may be higher, and a larger down payment or a co-signer might be beneficial.

Common mistakes to avoid are not checking your credit report beforehand or assuming a less-than-perfect score means no chance of approval. Kinecta often works with members to find solutions.

Income and Debt-to-Income Ratio

Lenders want to ensure you have a stable income source sufficient to cover your monthly loan payments in addition to your other financial obligations. Your debt-to-income (DTI) ratio is crucial here. This ratio compares your total monthly debt payments to your gross monthly income.

- Ideal DTI: Most lenders prefer a DTI ratio below 36%, though some may go higher depending on other factors.

- What Kinecta Looks For: Consistent employment history and an income level that supports the proposed loan payment without causing financial strain.

Down Payment Considerations

While not always strictly required, making a down payment on your car loan can significantly improve your chances of approval and secure a better interest rate. A down payment reduces the amount you need to borrow, which lowers the lender’s risk.

- Benefits of a Down Payment:

- Lower monthly payments.

- Less interest paid over the life of the loan.

- Reduced risk of being "upside down" on your loan (owing more than the car is worth).

- Potential for a lower interest rate.

Vehicle Requirements

The vehicle itself also plays a role in the loan approval process, especially for used car loans. Kinecta may have specific requirements regarding:

- Age and Mileage: Limits on how old or how many miles a used vehicle can have.

- Title and Condition: The vehicle must have a clear title, and its overall condition will be assessed, often through a vehicle inspection or valuation.

It’s always best to discuss any specific vehicle concerns with a Kinecta loan officer early in the process.

Understanding Kinecta Car Loan Rates and Terms

The interest rate and loan term are two of the most critical components of your Kinecta Car Loan, directly impacting your monthly payment and the total cost of borrowing. A thorough understanding of how these factors work will help you make the most financially sound decision.

Don’t just look at the monthly payment; consider the long-term implications of your choices.

Factors Influencing Your Rate

Several elements contribute to the interest rate you’re offered on a Kinecta auto loan:

- Credit Score: As mentioned, a higher credit score generally leads to a lower interest rate.

- Loan Term: Shorter loan terms often come with slightly lower rates because the lender’s risk exposure is reduced.

- Vehicle Type: New cars typically qualify for lower rates than used cars due to their higher value and perceived reliability.

- Loan Amount: Larger loan amounts might sometimes have slightly different rate structures.

Kinecta strives to provide competitive rates across the board, but these individual factors will ultimately tailor your specific offer.

Fixed vs. Variable Rates

Almost all Kinecta Car Loans come with fixed interest rates. This means your interest rate will remain the same throughout the entire loan term, providing predictability and stability in your monthly payments.

- Advantage of Fixed Rates: You’ll know exactly what your payment will be each month, making budgeting much easier. You’re also protected if market interest rates rise.

Available Loan Terms

Kinecta typically offers a range of loan terms to suit different budgets and repayment preferences. Common terms include:

- 36 months (3 years)

- 48 months (4 years)

- 60 months (5 years)

- 72 months (6 years)

- And sometimes even longer terms for higher-value vehicles.

Impact of Loan Term on Payments and Total Interest

Choosing the right loan term is a balancing act between monthly affordability and the total cost of the loan.

- Shorter Terms (e.g., 36 or 48 months):

- Higher monthly payments.

- Significantly less interest paid over the life of the loan.

- You’ll own your car outright sooner.

- Longer Terms (e.g., 60, 72, or 84 months):

- Lower monthly payments, making the car more "affordable" on a monthly basis.

- More interest paid over the life of the loan.

- You’ll be paying for the car for a longer period.

Pro tips from us: While lower monthly payments are appealing, always calculate the total interest paid over the life of the loan. A shorter term, if manageable, almost always saves you money in the long run.

Pro Tips for Securing the Best Kinecta Car Loan

Navigating the car loan landscape can be made much simpler and more financially advantageous with a few expert strategies. As an expert blogger, I’ve distilled years of financial insight into actionable tips that will help you secure the most favorable Kinecta Car Loan possible.

These proactive steps can significantly improve your position as a borrower and save you thousands of dollars.

1. Improve Your Credit Score

Your credit score is your financial report card. Before you even think about applying for a Kinecta auto loan, take steps to improve it.

- Pay Bills on Time: Payment history is the biggest factor in your score.

- Reduce Existing Debt: Lowering your credit utilization (how much credit you use vs. how much you have available) can boost your score.

- Check for Errors: Review your credit report for inaccuracies and dispute them immediately.

- Internal Link: For a deeper dive into credit improvement, read our article: Understanding Your Credit Score: The Key to Better Loan Rates (Simulated Internal Link).

2. Save for a Down Payment

As discussed, a larger down payment reduces the amount you need to borrow and signals to Kinecta that you’re a responsible borrower. Aim for at least 10-20% of the vehicle’s purchase price if possible.

- Benefits: Lower monthly payments, less interest paid, and immediate equity in your vehicle.

3. Get Pre-Approved First

This cannot be stressed enough. Obtaining a Kinecta pre-approval before you visit the dealership gives you immense power. You’ll know your budget and interest rate, allowing you to focus solely on negotiating the car’s price.

- Dealer Perspective: Dealers often try to bundle financing with the car sale. Having pre-approval lets you separate these two transactions, often leading to a better deal on both fronts.

4. Consider a Co-Signer if Needed

If your credit score is less than ideal or your income is marginal, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate.

- Important Note: A co-signer is equally responsible for the loan. Ensure both parties understand this commitment.

5. Research Vehicle Values Thoroughly

Before you negotiate, know the fair market value of the car you’re interested in. Tools like Kelley Blue Book (KBB) or Edmunds can provide excellent estimates for both new and used vehicles.

- Why it Matters: Prevents you from overpaying for the vehicle, which in turn reduces the amount you need to finance.

6. Read the Fine Print

Once you receive your loan offer from Kinecta, read every detail carefully. Understand the interest rate, term, any fees, and the total cost of the loan. Don’t hesitate to ask questions if anything is unclear.

- Common Mistakes to Avoid: Rushing through the documents and signing without fully comprehending the terms can lead to unpleasant surprises later.

Kinecta Auto Loan Refinancing: Is It Right for You?

Refinancing your current auto loan with Kinecta can be a strategic financial move that puts more money back in your pocket. It’s not just for those struggling with payments; it’s a smart option for anyone looking to optimize their finances.

Consider if your current loan terms are still the best fit, or if a Kinecta auto loan refinance could offer significant improvements.

When to Consider Refinancing

Several scenarios make refinancing a highly attractive option:

- Your Credit Score Has Improved: If your credit score has significantly increased since you took out your original loan, you’re likely eligible for a much lower interest rate.

- Market Rates Have Dropped: Auto loan interest rates fluctuate. If current rates are lower than your existing loan’s rate, refinancing can save you money.

- You Want to Lower Your Monthly Payments: Extending your loan term through refinancing can reduce your monthly outlay, freeing up cash flow. Be mindful of paying more interest over time, though.

- You Want to Pay Off Your Loan Faster: Conversely, if you can afford higher payments, refinancing to a shorter term with a lower rate can help you become debt-free sooner.

- You Want to Remove a Co-signer: If your financial situation has improved, refinancing in your name alone can release a co-signer from their obligation.

Benefits of Refinancing with Kinecta

- Lower Interest Rate: The most common and often most impactful benefit, leading to substantial savings.

- Reduced Monthly Payments: Makes your budget more manageable.

- Shorter Loan Term: Accelerates debt repayment.

- Better Customer Service: Experience Kinecta’s member-focused approach if you’re coming from a less-satisfactory lender.

The process for Kinecta auto loan refinance is similar to applying for a new loan. You’ll submit an application, provide vehicle details, and Kinecta will assess your creditworthiness. It’s a relatively simple process that could yield significant financial rewards.

Managing Your Kinecta Car Loan

Once you’ve secured your Kinecta Car Loan, managing it effectively is crucial for maintaining good financial health and building a strong credit history. Kinecta provides various tools and support to make loan management convenient and straightforward.

Responsible loan management ensures you avoid late fees, protect your credit score, and ultimately pay off your vehicle as planned.

Convenient Payment Options

Kinecta offers multiple ways to make your car loan payments, allowing you to choose the method that best fits your lifestyle:

- Online Banking: Easily manage your loan, set up recurring payments, and view your loan details through Kinecta’s secure online portal.

- Automatic Payments (ACH): Set up automatic deductions from your checking or savings account to ensure payments are always on time, avoiding late fees.

- Phone Payments: Make payments over the phone with a representative.

- Mail: Send payments via postal service.

- In-Branch: Visit a Kinecta branch location to make payments in person.

Pro tips from us: Setting up automatic payments is the best way to ensure you never miss a due date, which is critical for maintaining a good credit score.

Accessing Your Loan Information

Kinecta’s online banking platform is a valuable resource for managing your car loan. Through your secure account, you can typically:

- View your loan balance and payment history.

- Access statements and tax documents.

- Make extra payments towards your principal.

- Update your contact information.

This transparency empowers you to stay on top of your loan and track your progress toward ownership.

Early Payoff Considerations

If you find yourself in a position to pay off your Kinecta Car Loan early, it’s generally a wise financial move. Paying off your loan ahead of schedule saves you money on interest and frees up your monthly budget.

- Kinecta’s Policy: Most auto loans from credit unions like Kinecta do not have pre-payment penalties, meaning you won’t be charged extra for paying off your loan early. Always confirm this in your loan agreement.

- How to Do It: You can typically make extra payments towards your principal through your online account or by contacting customer service.

Kinecta Car Loan vs. Other Financing Options

In the vast landscape of auto financing, Kinecta Federal Credit Union stands out for distinct reasons compared to traditional banks and dealership financing. Understanding these differences can solidify your decision to choose a Kinecta Car Loan.

It’s about finding the financing partner that aligns with your financial goals and offers the best overall value.

Credit Unions (Kinecta) vs. Banks

- Kinecta (Credit Union):

- Member-Owned: Prioritizes member benefits, often leading to lower rates and fewer fees.

- Personalized Service: Known for a more hands-on, supportive approach.

- Community Focus: Invests in its members’ financial well-being.

- Membership Required: Must join to access services.

- Traditional Banks:

- Profit-Driven: Focused on shareholder returns, which can sometimes translate to higher rates or fees.

- Broader Reach: Often have more branches and a larger national presence.

- Less Personalized: May feel more transactional.

Credit Unions (Kinecta) vs. Dealership Financing

- Kinecta (Credit Union):

- Transparent Rates: Offers pre-approval with clear rates before you enter the dealership.

- Focus on Your Best Interest: Their goal is to get you the best loan, not to profit from the financing.

- Separates Car Price from Loan: Empowers you to negotiate the car price first.

- Dealership Financing:

- Convenience: One-stop shop for car and financing.

- Markups: Dealers often add their own markup to the interest rate they get from lenders, increasing your cost.

- Pressure Tactics: Can use financing to obscure the true cost of the vehicle.

- Limited Options: May only offer a few lenders they have relationships with.

Based on my experience, always get independent financing (like a Kinecta Car Loan pre-approval) before heading to the dealership. It’s the ultimate safeguard against high-pressure sales and hidden markups.

Common Questions About Kinecta Car Loans

Even with a comprehensive guide, specific questions often arise. Here are answers to some of the most frequently asked questions about Kinecta auto loan options.

Q1: Can I get a Kinecta car loan with less-than-perfect credit?

A: Yes, it’s often possible. While an excellent credit score will secure the best rates, Kinecta, as a credit union, is known for being more flexible and member-focused. They may consider your overall financial picture, including income, employment history, and other factors. A co-signer or a larger down payment can also improve your chances.

Q2: What documents do I need to apply for a Kinecta car loan?

A: You’ll typically need proof of identity (driver’s license, SSN), proof of residency, and proof of income (pay stubs, W-2s). For the vehicle itself, you’ll need its make, model, year, VIN, and purchase price.

Q3: How long does the Kinecta car loan application process take?

A: The pre-approval process can often be completed quickly, sometimes within minutes online or a few hours. Once you have your vehicle details, the final loan approval and funding can often happen within one to two business days, sometimes even faster.

Q4: Does Kinecta offer loans for private party car purchases?

A: Yes, Kinecta often provides financing for vehicles purchased from private sellers. The requirements may be slightly different than for dealership purchases, potentially including a vehicle inspection or specific title transfer processes. It’s best to confirm the details with a Kinecta loan officer.

Q5: Are there any fees associated with a Kinecta car loan?

A: Kinecta is generally transparent about any fees. While some standard loan fees might apply (e.g., origination fees, though less common for auto loans), credit unions are known for having fewer fees compared to traditional banks. Always ask for a full disclosure of any potential fees before signing.

Drive Confidently with a Kinecta Car Loan

Securing a Kinecta Car Loan can be one of the smartest financial decisions you make on your journey to vehicle ownership. By understanding their membership requirements, exploring the diverse loan options, and leveraging the power of pre-approval, you put yourself in a position of strength.

Kinecta Federal Credit Union’s commitment to competitive rates, flexible terms, and member-centric service makes them an exceptional choice for your auto financing needs. They prioritize your financial well-being, offering a transparent and supportive lending experience.

Don’t let the complexities of car financing deter you from your dream vehicle. Take the proactive steps outlined in this guide, connect with Kinecta, and drive off with confidence, knowing you’ve secured a Kinecta Car Loan that truly works for you. Start your journey today by visiting Kinecta’s official website or contacting a loan specialist to explore your options. Your ideal car—and the perfect loan to go with it—awaits!