Drive Your Dreams: The Ultimate Guide to Securing a SEFCU Used Car Loan

Drive Your Dreams: The Ultimate Guide to Securing a SEFCU Used Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car can be an exciting, yet often daunting, prospect. With countless options available, finding the right vehicle and, crucially, the right financing can feel like navigating a complex maze. That’s where a trusted partner like SEFCU comes into play, offering tailored solutions for your used car loan needs.

This comprehensive guide is your ultimate resource for understanding everything about SEFCU Used Car Loans. We’ll delve deep into the benefits, eligibility, application process, and expert tips to help you secure the best financing for your next pre-owned vehicle. Our goal is to empower you with knowledge, ensuring a smooth and confident car-buying experience.

Drive Your Dreams: The Ultimate Guide to Securing a SEFCU Used Car Loan

Why a Used Car? Smart Savings, Smart Choices

Before we dive into the specifics of SEFCU’s offerings, let’s briefly touch upon the enduring appeal of used cars. Opting for a pre-owned vehicle is a financially savvy decision for many individuals and families. It offers a fantastic balance of value, reliability, and affordability.

One of the most significant advantages is avoiding the steep depreciation that new cars experience the moment they leave the dealership. A used car has already absorbed that initial drop in value, meaning your investment goes further. You can often get more car for your money, potentially upgrading to a higher trim level or a more luxurious model than you could afford new. Furthermore, insurance costs for used vehicles are typically lower, contributing to overall savings throughout your ownership.

Why Choose SEFCU for Your Used Car Loan? A Partner You Can Trust

When it comes to financing a used car, where you get your loan can be just as important as the loan itself. Credit unions like SEFCU stand out in the financial landscape, offering a member-centric approach that often translates into better rates and more personalized service. SEFCU, in particular, has built a strong reputation within its community for putting members first.

Based on my extensive experience in the financial sector, credit unions frequently provide a more personal and understanding touch compared to larger, traditional banks. They are non-profit organizations, meaning their earnings are returned to members in the form of lower interest rates on loans, higher returns on savings, and reduced fees. This fundamental difference often results in a more advantageous financial outcome for you, the borrower.

Competitive Rates and Flexible Terms

SEFCU is known for offering highly competitive interest rates on its used car loans. These favorable rates can significantly reduce the total cost of your loan over its lifetime, saving you hundreds or even thousands of dollars. They understand that every borrower’s financial situation is unique, which is why they also offer a variety of flexible loan terms.

Whether you prefer shorter terms for faster payoff or longer terms for lower monthly payments, SEFCU works with you to find a solution that fits your budget. This flexibility is crucial in ensuring your car loan is a manageable part of your financial plan, not a burden. Their commitment to offering adaptable solutions truly sets them apart.

Personalized Service and Community Focus

As a member of SEFCU, you’re not just a number; you’re part of a community. This philosophy permeates their customer service, providing a level of personalized attention that is often hard to find elsewhere. Their loan officers are dedicated to understanding your individual needs and guiding you through every step of the loan process.

This community-focused approach means they are invested in your financial well-being. They strive to educate you, answer all your questions, and ensure you feel confident and informed about your financing decisions. It’s this dedication to service that builds lasting relationships and fosters trust among their members.

Member Benefits Beyond the Loan

Becoming a SEFCU member opens the door to a host of additional financial products and services. Beyond your used car loan, you gain access to checking and savings accounts, credit cards, mortgages, and various other lending options, all designed with the member’s best interest in mind. This holistic approach to financial services means you can consolidate your banking needs with a single, trusted institution.

They also offer financial education resources, helping members make smarter financial decisions across the board. This commitment to member empowerment makes SEFCU a comprehensive financial partner, not just a loan provider. It’s an institution that truly cares about your long-term financial health.

Understanding SEFCU Used Car Loan Options: Tailored for You

SEFCU offers a range of used car loan options designed to meet diverse needs and financial situations. Their goal is to make financing your pre-owned vehicle as straightforward and beneficial as possible. Understanding these options is the first step towards making an informed decision.

Primarily, SEFCU provides standard used car loans for a wide variety of vehicles. These loans are typically secured by the vehicle itself, meaning the car serves as collateral for the loan. This common structure allows for competitive interest rates, as the risk to the lender is mitigated. They are well-versed in financing various makes, models, and ages of used cars.

Loan Terms and Amounts

The flexibility in loan terms is a significant advantage. SEFCU offers terms that can range from short periods, such as 24 or 36 months, up to longer durations, often extending to 60 or even 72 months, depending on the vehicle’s age and the loan amount. Shorter terms typically mean higher monthly payments but less interest paid over the life of the loan. Conversely, longer terms result in lower monthly payments but more interest accumulated.

Pro tips from us: Always use a loan calculator to see how different terms affect your total repayment and monthly budget. It’s crucial to find a balance that is comfortable for your current financial situation. Regarding loan amounts, SEFCU can finance a broad spectrum, from smaller, budget-friendly cars to more premium used vehicles, provided you meet the eligibility criteria.

Eligibility Requirements for a SEFCU Used Car Loan: What You Need to Know

Securing a SEFCU Used Car Loan begins with meeting certain eligibility criteria. These requirements are in place to ensure responsible lending and to protect both the borrower and the credit union. Understanding them upfront will help you prepare your application effectively.

SEFCU Membership is Key

The fundamental requirement for any SEFCU loan product is membership. As a credit union, SEFCU serves a specific field of membership. Typically, this includes individuals who live, work, worship, or attend school in certain counties within New York State, or those who are immediate family members of existing SEFCU members. Joining is a simple process, usually requiring a small initial deposit into a savings account, establishing your membership and ownership stake in the credit union.

Common mistakes to avoid are applying for a loan without first confirming or establishing your membership. Always verify your eligibility to join SEFCU before starting the loan application to ensure a smooth process.

Credit Score Considerations

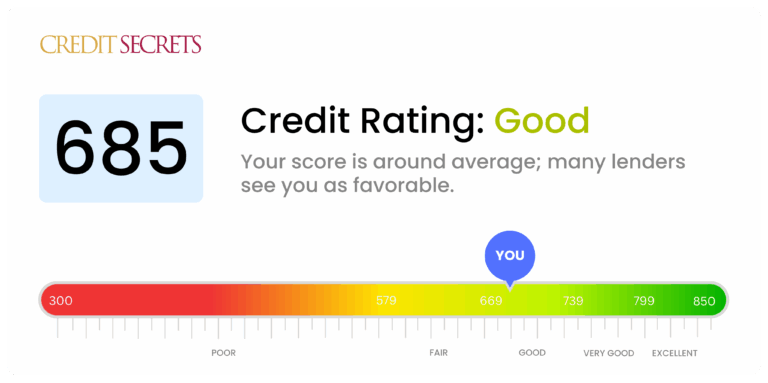

Your credit score plays a significant role in determining your eligibility and the interest rate you’ll receive. A higher credit score generally indicates a lower lending risk, making you eligible for more favorable terms. While there isn’t a single "minimum" score, SEFCU, like most lenders, looks for a history of responsible credit management.

However, based on my experience, credit unions are often more willing to work with members who may have less-than-perfect credit. They consider the whole financial picture, not just a single number. If your credit score isn’t ideal, demonstrating consistent income, a reasonable debt-to-income ratio, and a solid explanation for past credit issues can still lead to approval.

Income Stability and Debt-to-Income Ratio

Lenders need assurance that you have the financial capacity to repay the loan. This means demonstrating stable income, usually through pay stubs, tax returns, or other proof of earnings. Your employment history also plays a role, with longer, more stable employment generally viewed favorably.

Furthermore, your debt-to-income (DTI) ratio is a crucial factor. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments. SEFCU will assess this to ensure the new car loan payment won’t overextend your financial resources.

Vehicle Requirements

The used car itself must also meet certain criteria for financing. While specific requirements can vary, common factors include the vehicle’s age, mileage, and condition. Most lenders prefer to finance vehicles that are relatively new, perhaps under 10 years old, and with a reasonable amount of mileage. The vehicle also needs to have a clean title, meaning it’s not a salvage or rebuilt title, as these can pose higher risks.

Pro tips from us: Always have the vehicle’s details readily available, including VIN, make, model, year, and approximate mileage. Having an independent inspection report can also strengthen your application, demonstrating the car’s sound condition.

The SEFCU Used Car Loan Application Process: A Step-by-Step Guide

Applying for a SEFCU Used Car Loan is designed to be a straightforward and transparent process. Knowing what to expect at each stage can significantly reduce stress and speed up your approval. Let’s walk through the typical steps involved.

Step 1: Pre-Approval – Your Power Tool

We highly recommend starting with a pre-approval. This crucial step involves SEFCU assessing your creditworthiness and providing you with a maximum loan amount and an estimated interest rate before you even set foot in a dealership. Getting pre-approved gives you immense bargaining power.

With a pre-approval in hand, you know exactly how much you can afford, allowing you to shop with confidence and focus on finding the right car, not worrying about financing. It also simplifies negotiations with dealers, as you’re essentially walking in with your own financing already secured. Dealers often become more competitive when they know you have alternative financing ready.

Step 2: Gathering Your Documents

Once you’re ready to apply (either for pre-approval or a direct loan once you’ve found a car), you’ll need to gather essential documents. While the exact list may vary, common requirements include:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2s, or tax returns if self-employed.

- Proof of Residence: Utility bill or lease agreement.

- Vehicle Information: If you’ve already found a car, you’ll need its VIN, make, model, year, and mileage.

Common mistakes to avoid are not having all your documents organized and readily accessible. This can cause delays in the application process. Prepare these materials in advance to ensure a smooth submission.

Step 3: Submitting Your Application

SEFCU offers multiple convenient ways to apply:

- Online: Their user-friendly website typically features an online application portal, allowing you to apply from the comfort of your home.

- By Phone: You can speak directly with a loan officer who can guide you through the application over the phone.

- In-Person: Visiting a SEFCU branch allows for face-to-face interaction, where you can ask questions and receive personalized assistance.

Choose the method that best suits your preferences. Regardless of how you apply, ensure all information is accurate and complete to prevent any processing delays.

Step 4: What to Expect After Applying

After submitting your application, SEFCU will review your information, conduct a credit check, and verify your income and other details. The processing time can vary, but credit unions often pride themselves on quick turnaround times. You’ll typically receive a decision within a few business days, sometimes even sooner.

If approved, you’ll receive a loan offer outlining the approved amount, interest rate, and loan terms. You’ll then proceed to finalize the paperwork, which may involve signing loan agreements and arranging for the funds to be disbursed. This is often done directly to the dealership if you’re purchasing from one, or to you if it’s a private sale.

Getting the Best Rates and Terms with SEFCU: Expert Strategies

Securing a SEFCU Used Car Loan is one thing; optimizing it for the best possible rates and terms is another. With some strategic planning, you can significantly improve your loan offer.

Maximize Your Credit Score

Your credit score is arguably the most impactful factor in determining your interest rate. Lenders view higher scores as an indication of lower risk. Before applying, check your credit report for any errors and work to improve your score. This could involve paying down existing debts, making all payments on time, and avoiding opening new lines of credit.

Pro tips from us: Always check your credit report from all three major bureaus (Experian, Equifax, TransUnion) at least a few months before you plan to apply. This gives you time to dispute inaccuracies and make improvements. A few points increase in your score can translate into significant interest savings over the life of the loan.

Make a Strong Down Payment

From my experience, a strong down payment can significantly lower your monthly payments and reduce the total interest paid. When you put down a larger sum upfront, you’re borrowing less, which means less risk for the lender and potentially a lower interest rate for you. A substantial down payment also builds immediate equity in your vehicle.

Aim for at least 10-20% of the vehicle’s purchase price if your budget allows. This not only makes your loan more attractive to SEFCU but also protects you from becoming "upside down" on your loan, where you owe more than the car is worth.

Understanding APR vs. Interest Rate

It’s crucial to differentiate between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal amount. The APR, however, includes the interest rate plus any additional fees associated with the loan, such as administrative fees.

When comparing loan offers, always look at the APR, as it provides a more accurate representation of the true cost of borrowing. SEFCU is transparent about their APR, ensuring you have a clear understanding of your loan’s total expense.

Negotiating with Dealers (with Pre-Approval in Hand)

If you’re purchasing from a dealership, having a SEFCU pre-approval empowers you greatly. It separates the car-buying negotiation from the financing negotiation. You can focus solely on getting the best price for the vehicle, knowing your financing is already secured at a competitive rate.

Common mistakes to avoid are letting the dealership roll your loan into their financing without comparing it to your pre-approval. Always compare their offer against SEFCU’s pre-approval. If the dealer can beat your SEFCU rate, great! But often, your pre-approval provides a benchmark that ensures you’re getting a fair deal.

Refinancing Your Existing Used Car Loan with SEFCU: Save Money, Gain Control

Perhaps you already have a used car loan but aren’t happy with the terms. Or maybe your financial situation has improved since you first took out the loan. In these scenarios, refinancing your existing used car loan with SEFCU could be a highly beneficial move.

When to Consider Refinancing

There are several compelling reasons to consider refinancing:

- Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a much lower rate.

- Lower Monthly Payments: Refinancing to a lower rate or extending your loan term can reduce your monthly payment, freeing up cash flow.

- Improve Loan Terms: You might want to switch from a variable interest rate to a fixed rate, or adjust your loan term to better suit your current budget.

- Remove a Co-signer: If your financial standing has strengthened, you might be able to refinance and remove a co-signer from the original loan.

A common scenario where refinancing makes sense is when your credit score has improved by 50 points or more since your initial loan. This often indicates you’re eligible for better rates.

Benefits of Refinancing with SEFCU

Refinancing with SEFCU brings the same member-centric benefits as their original used car loans. You’ll likely encounter competitive rates, flexible terms, and personalized service. They aim to make the refinancing process as smooth as possible, helping you achieve your financial goals.

The process for refinancing is similar to applying for a new loan. You’ll submit an application, provide necessary documentation, and SEFCU will review your credit and income. If approved, they will help you pay off your old loan, and your new, more favorable loan with SEFCU will begin.

Beyond the Loan: SEFCU’s Additional Auto Resources

SEFCU’s commitment to its members extends beyond just providing a used car loan. They often offer additional products and services that can enhance your car ownership experience and protect your investment.

GAP Insurance and Extended Warranties

When financing a vehicle, especially a used one, considering Guaranteed Asset Protection (GAP) insurance is a smart move. If your car is totaled or stolen, your auto insurance policy typically pays out the actual cash value of the vehicle, which might be less than what you still owe on your loan. GAP insurance covers this "gap" between your loan balance and the insurance payout, preventing you from being responsible for a debt on a car you no longer have.

SEFCU may also offer options for extended warranties, providing peace of mind against unexpected repair costs after the manufacturer’s warranty expires. These products can be invaluable for protecting your financial stability.

Financial Counseling and Online Tools

SEFCU often provides access to financial counseling services, helping members navigate various financial challenges and make informed decisions. This can be particularly helpful if you’re new to car loans or want to ensure your overall budget is on track.

They also typically offer online tools and calculators on their website. These resources allow you to estimate loan payments, calculate potential savings from refinancing, and manage your accounts conveniently from anywhere. Leveraging these tools can significantly aid in your financial planning.

Common Pitfalls and How to Avoid Them in Your Used Car Loan Journey

While SEFCU strives to make your loan experience positive, there are common mistakes car buyers make that can lead to financial headaches. Being aware of these pitfalls is your first line of defense.

- Not Reading the Fine Print: Always read your loan agreement thoroughly before signing. Understand all terms, conditions, fees, and the total cost of the loan. Don’t hesitate to ask your SEFCU loan officer to clarify anything you don’t understand.

- Buying More Car Than You Can Afford: It’s easy to get carried away by the excitement of a new-to-you car. However, ensure the monthly payment, insurance, fuel, and maintenance costs comfortably fit within your budget. Pro tips from us: Create a realistic budget before you start shopping, factoring in all potential car-related expenses.

- Ignoring the Total Cost of Ownership: Beyond the loan payment, consider fuel efficiency, insurance premiums, maintenance schedules, and potential repair costs for the specific used car model you’re eyeing. A cheaper car upfront might be more expensive to maintain in the long run.

- Not Getting Pre-Approved: As discussed, pre-approval is your superpower. Skipping this step means you lose valuable negotiation leverage and might end up with less favorable financing terms offered by a dealership.

- Focusing Only on Monthly Payment: While a low monthly payment is appealing, extending the loan term too much can lead to paying significantly more interest over time. Balance monthly affordability with the total cost of the loan.

By being diligent and informed, you can navigate the used car buying process with confidence and avoid these common traps.

FAQs About SEFCU Used Car Loans

- Q: How quickly can I get approved for a SEFCU Used Car Loan?

- A: SEFCU often provides quick decisions, sometimes within a few business days, especially if all your documentation is in order. Pre-approvals can be even faster.

- Q: Can I get a SEFCU Used Car Loan with bad credit?

- A: While a good credit score helps, SEFCU considers your overall financial picture. They may offer options or work with you to improve your credit before applying. It’s always best to speak directly with a loan officer.

- Q: Does SEFCU finance older used cars?

- A: Generally, there are age and mileage limits. It’s best to confirm the specific vehicle requirements with SEFCU directly, as these can vary.

- Q: What documents do I need to apply?

- A: Typically, you’ll need proof of identity, income, residence, and specific vehicle information if you’ve chosen a car.

- Q: Can I refinance a loan from another institution with SEFCU?

- A: Yes, SEFCU offers competitive refinancing options for existing auto loans, potentially saving you money.

Drive Your Future Forward with a SEFCU Used Car Loan

Securing a SEFCU Used Car Loan is more than just obtaining financing; it’s about partnering with a financial institution that genuinely cares about your financial well-being. From competitive rates and flexible terms to personalized service and valuable additional resources, SEFCU is dedicated to making your used car buying experience positive and empowering.

By understanding the process, preparing diligently, and leveraging the expert tips shared in this guide, you are well-equipped to navigate the world of used car financing with confidence. Don’t let the complexities of car buying deter you from finding the perfect pre-owned vehicle. Take the next step towards driving your dreams – explore SEFCU’s used car loan options today.

For more detailed information on current rates and to start your application, visit the SEFCU official website. You might also find our comprehensive guide on Understanding Car Loan Interest Rates helpful in preparing for your application.