Drive Your Dreams: The Ultimate Guide to Securing an NC Secu Car Loan

Drive Your Dreams: The Ultimate Guide to Securing an NC Secu Car Loan Carloan.Guidemechanic.com

Are you dreaming of a new car, a reliable used vehicle, or perhaps looking to lower your current auto loan payments? For residents of North Carolina, the State Employees’ Credit Union (SECU) stands out as a powerful and trusted financial partner. Their NC Secu Car Loan offerings are renowned for competitive rates, flexible terms, and a member-centric approach that truly sets them apart.

As an expert in auto financing and a long-time observer of the credit union landscape, I’ve seen firsthand how SECU empowers its members. This comprehensive guide will take you on a deep dive into everything you need to know about securing an NC Secu Car Loan, from understanding eligibility to navigating the application process and beyond. Our goal is to equip you with the knowledge to make informed decisions and confidently drive off in your next vehicle.

Drive Your Dreams: The Ultimate Guide to Securing an NC Secu Car Loan

What is SECU? Why Consider Them for Your Car Loan?

The State Employees’ Credit Union (SECU) is a not-for-profit financial cooperative primarily serving North Carolina’s state and public school employees, their families, and retirees. Unlike traditional banks, which operate to generate profit for shareholders, credit unions like SECU exist solely to serve their members. This fundamental difference translates into tangible benefits, especially when it comes to borrowing money.

Choosing SECU for your NC Secu Car Loan means becoming part of a community. Their core mission is to promote the financial well-being of their members. This ethos often leads to more favorable loan terms, lower interest rates, and a personalized banking experience that’s hard to find elsewhere.

Based on my experience, many individuals find the credit union model far more appealing for significant purchases like a vehicle. The focus isn’t just on the transaction; it’s on building a lasting relationship and providing financial guidance.

Understanding the NC Secu Car Loan: Key Features and Benefits

An NC Secu Car Loan offers a suite of features designed with the member’s best interest at heart. These aren’t just buzzwords; they represent real advantages that can save you money and provide peace of mind throughout the life of your loan.

Let’s break down the core benefits you can expect when choosing SECU for your vehicle financing needs.

1. Competitive Interest Rates

One of the most compelling reasons to choose an NC Secu Car Loan is the consistently competitive interest rates. Because SECU is a not-for-profit entity, any earnings are returned to members in the form of lower loan rates, higher savings rates, and reduced fees. This structure often allows them to undercut rates offered by larger, for-profit banks.

Lower interest rates translate directly into lower monthly payments and less money paid over the life of the loan. This can significantly impact your overall budget and financial health.

2. Flexible Loan Terms

SECU understands that every borrower’s financial situation is unique. They offer a variety of loan terms, allowing you to choose a repayment schedule that fits your budget and financial goals. Whether you prefer a shorter term to pay off your loan faster or a longer term for lower monthly payments, SECU provides options.

This flexibility ensures you aren’t boxed into a rigid repayment plan, making your NC Secu Car Loan manageable and stress-free. Pro tips from us: always balance the monthly payment with the total interest paid over the loan term.

3. Wide Range of Loan Types

Whether you’re buying brand new, pre-owned, or looking to refinance, an NC Secu Car Loan has you covered. They offer financing for:

- New Car Purchases: For vehicles straight off the dealership lot.

- Used Car Purchases: Including both dealer and private party sales.

- Refinancing Existing Loans: To potentially lower your interest rate or monthly payment.

This comprehensive approach means SECU can be your one-stop shop for almost any vehicle financing scenario.

4. No Prepayment Penalties

A significant advantage of an NC Secu Car Loan is the absence of prepayment penalties. This means you can pay off your loan early without incurring any additional fees. If your financial situation improves, you have the freedom to accelerate your payments and become debt-free sooner.

This flexibility empowers you to manage your loan on your own terms, saving you money on interest in the long run.

5. Personalized Member Service

SECU prides itself on its personalized service. When you apply for an NC Secu Car Loan, you’re not just a number. You’ll have access to knowledgeable loan officers who can guide you through the process, answer your questions, and help you find the best solution for your needs.

This human touch is a cornerstone of the credit union experience and provides invaluable support, especially for first-time borrowers.

Eligibility and Membership: Your First Steps Towards an NC Secu Car Loan

Before you can even think about driving away in your new car, understanding SECU’s membership requirements is crucial. An NC Secu Car Loan is exclusively available to members, so this is your very first step.

The good news is that membership is accessible to a broad spectrum of North Carolinians.

Who Can Join SECU?

SECU’s field of membership primarily includes:

- State of North Carolina employees: This covers a vast array of individuals working for state agencies, departments, and public universities.

- Public school employees: Teachers, administrators, support staff, and other personnel within the K-12 public education system.

- Retirees from the above categories.

- Immediate family members of existing SECU members. This includes spouses, children, parents, siblings, and even stepparents and stepchildren.

If you fall into any of these categories, you are likely eligible to join. Common mistakes to avoid are assuming you’re not eligible without checking; many people qualify through a family connection they weren’t aware of.

How to Become a SECU Member

Becoming a member is straightforward. You’ll need to:

- Verify Eligibility: Confirm you meet one of the criteria listed above.

- Open a Share Account: This is typically a basic savings account with a minimum deposit (often as little as $25). This establishes your "share" in the credit union.

- Provide Identification: You’ll need a valid government-issued ID (like a driver’s license), your Social Security number, and proof of your North Carolina address.

Once you’re a member, you gain access to all of SECU’s financial products and services, including their attractive NC Secu Car Loan options.

The Application Process for an NC Secu Car Loan: A Step-by-Step Guide

Applying for an NC Secu Car Loan is designed to be a smooth and transparent process. Whether you prefer the convenience of online applications or the personal touch of an in-branch visit, SECU offers options to suit your preference.

Based on my experience, being well-prepared significantly speeds up the approval process.

1. Gather Your Documents

Before you even start the application, assemble the necessary documentation. This usually includes:

- Proof of Income: Pay stubs (typically the most recent two), W-2 forms, or tax returns if you’re self-employed.

- Identification: Your valid driver’s license or state ID.

- Social Security Number: For credit verification.

- Proof of Residence: Utility bill or lease agreement with your current address.

- Vehicle Information (if you’ve chosen a car): Make, model, year, VIN, mileage, and purchase price.

Having these ready will prevent delays and allow the loan officer to process your application efficiently.

2. Choose Your Application Method

SECU offers several convenient ways to apply for your NC Secu Car Loan:

- Online Application: This is often the quickest method. You can apply from the comfort of your home or office via the SECU website.

- In-Person at a Branch: Visit any SECU branch across North Carolina. This option allows for direct interaction with a loan officer who can answer questions on the spot.

- By Phone: You can also initiate an application by calling SECU’s member services.

Pro tips from us: If you have complex questions or prefer a face-to-face discussion, an in-branch visit can be very beneficial.

3. Understand Pre-Approval

One of the smartest moves you can make is to get pre-approved for an NC Secu Car Loan before you start car shopping. Pre-approval means SECU has reviewed your financial information and determined how much you can borrow, at what interest rate, and for what term.

Benefits of pre-approval include:

- Budget Clarity: You know exactly how much car you can afford.

- Negotiating Power: You walk into the dealership as a cash buyer, giving you leverage to negotiate the vehicle price, not the financing.

- Confidence: You can shop with peace of mind, knowing your financing is secured.

Common mistakes to avoid are skipping pre-approval and letting the dealership handle all the financing. Dealerships often mark up interest rates, potentially costing you more.

4. The Credit Check and Decision

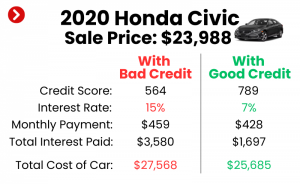

During the application, SECU will conduct a credit check. Your credit score plays a significant role in determining your eligibility and the interest rate you’ll receive for your NC Secu Car Loan. A higher credit score typically translates to lower rates.

Once your application is submitted, a loan officer will review your information. Approval times can vary but are often quick, especially for pre-approvals. You’ll then be notified of the decision and the terms of your loan.

Navigating Interest Rates and Terms with Your NC Secu Car Loan

Understanding how interest rates and loan terms work is crucial for managing your NC Secu Car Loan effectively. It directly impacts your monthly payment and the total cost of your vehicle.

SECU aims to offer competitive rates, but several factors will influence the specific rate you qualify for.

Factors Influencing Your Interest Rate

When you apply for an NC Secu Car Loan, SECU assesses various elements to determine your personalized interest rate:

- Credit Score: This is arguably the most significant factor. A strong credit history and high credit score (generally 700+) demonstrate your reliability as a borrower and typically lead to the lowest rates. For a deeper dive into improving your credit score, check out our article on .

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) usually come with lower interest rates because the risk to the lender is reduced. Longer terms (e.g., 60 or 72 months) often have higher rates.

- Down Payment: A larger down payment reduces the amount you need to borrow, which can sometimes result in a slightly better interest rate as it lowers the lender’s risk.

- Vehicle Age and Mileage: For used car loans, the age and mileage of the vehicle can sometimes influence the rate, as older vehicles are perceived as having a higher risk of mechanical issues.

Understanding APR vs. Interest Rate

It’s important to differentiate between the interest rate and the Annual Percentage Rate (APR).

- Interest Rate: This is the percentage charged by the lender for borrowing the principal amount.

- APR: This is the total cost of borrowing money for one year, expressed as a percentage. It includes the interest rate plus any additional fees associated with the loan (e.g., administrative fees, application fees).

When comparing NC Secu Car Loan offers with other lenders, always compare the APR, as it gives you the most accurate picture of the total cost.

How to Get the Best Possible Rate

Based on my experience, these strategies can help you secure the most favorable terms for your NC Secu Car Loan:

- Improve Your Credit Score: Pay bills on time, reduce existing debt, and check your credit report for errors before applying.

- Make a Down Payment: Even a small down payment can signal financial responsibility and reduce your loan amount.

- Choose a Shorter Loan Term: If your budget allows, opting for a shorter term can significantly lower your interest rate.

- Shop Around (Even with SECU): While SECU is competitive, it’s always wise to understand the market. However, for members, SECU’s offers are often hard to beat.

Common mistakes to avoid are accepting the first offer without understanding the breakdown of the APR, and not considering how a longer loan term, while lowering monthly payments, can drastically increase the total interest paid.

New vs. Used vs. Refinancing: Exploring Your NC Secu Car Loan Options

The beauty of an NC Secu Car Loan lies in its versatility. SECU offers financing solutions for various vehicle acquisition scenarios, ensuring you find the right fit for your needs.

Let’s delve into the specifics of each type of auto loan they provide.

New Car Loan with SECU

If you’re eyeing a brand-new vehicle straight from the dealership, an NC Secu Car Loan for a new car is an excellent option.

- What to Expect: Generally, new car loans tend to have slightly lower interest rates compared to used car loans, as new vehicles typically hold their value better initially and pose less risk to the lender.

- Typical Terms: SECU offers various terms, often up to 72 or even 84 months for new vehicles, depending on the loan amount and your creditworthiness. While longer terms mean lower monthly payments, remember they also mean more interest paid over time.

- Manufacturer Incentives: While SECU provides the loan, always inquire about any manufacturer incentives or rebates that could further reduce your overall cost.

Used Car Loan with SECU

Purchasing a used car is a smart financial move for many, and SECU fully supports this with their used car loan options. An NC Secu Car Loan for a used vehicle can be just as competitive as a new car loan, though rates might be marginally higher due to the perceived risk of an older vehicle.

- Vehicle Age/Mileage Restrictions: SECU, like most lenders, may have restrictions on the maximum age or mileage of a vehicle they will finance, especially for the longest loan terms. These limits are in place to ensure the vehicle remains valuable collateral throughout the loan period. Always confirm these details with a loan officer.

- Inspections: It’s highly recommended to get a pre-purchase inspection from an independent mechanic for any used vehicle. This ensures you’re making a sound investment, regardless of your financing source. If you’re weighing the pros and cons of new versus used vehicles, our comprehensive guide, ”, offers valuable insights.

Refinancing Your Current Auto Loan with SECU

Many people overlook the significant savings possible through refinancing their existing auto loan. An NC Secu Car Loan for refinancing can be a game-changer if your financial situation has improved or if you initially secured a high-interest loan.

- When to Consider Refinancing:

- Your Credit Score Has Improved: If your credit score has significantly increased since you took out your original loan, you’re likely eligible for a lower interest rate.

- Interest Rates Have Dropped: Market interest rates fluctuate. If current rates are lower than your original loan’s rate, refinancing makes sense.

- You Want to Lower Your Monthly Payment: Extending your loan term through refinancing can reduce your monthly outlay, though it might increase total interest.

- You Want to Shorten Your Loan Term: If you want to pay off your car faster and can afford higher payments, refinancing to a shorter term can save you a lot in interest.

- Benefits of Refinancing with SECU: SECU’s competitive rates and member-focused approach often mean significant savings for those looking to refinance. It’s a straightforward process that can free up money in your budget.

Private Party Car Loan with SECU

Buying a car directly from an individual (a private party sale) can often yield better deals than purchasing from a dealership. SECU makes this process easy with specialized NC Secu Car Loan options for private party purchases.

- How it Works: SECU can help you finance a private party purchase by providing you with a check or direct deposit for the agreed-upon amount. They’ll also guide you through the necessary paperwork, such as transferring the title and lien information.

- Key Considerations: Ensure the seller has a clear title. SECU will also likely require an inspection of the vehicle and proof of its market value to ensure the loan amount is appropriate. This is a common service that many traditional banks don’t offer as smoothly.

Beyond the Loan: Additional Benefits and Services from SECU

An NC Secu Car Loan isn’t just about the money you borrow; it’s about the comprehensive support and additional protections SECU offers its members. These services can add significant value and peace of mind to your vehicle ownership experience.

SECU strives to be a holistic financial partner, extending beyond just the primary loan product.

GAP Insurance

Guaranteed Asset Protection (GAP) insurance is an optional but highly recommended add-on for your NC Secu Car Loan.

- What it Is: If your car is totaled or stolen, your standard auto insurance policy will only pay out the vehicle’s actual cash value. However, you might owe more on your loan than the car is worth, especially in the early years of ownership (due to depreciation). GAP insurance covers this "gap" between your insurance payout and the remaining loan balance.

- Why it’s Important: Based on my experience, many new car buyers find themselves "upside down" on their loan shortly after purchase. GAP insurance protects you from a significant financial loss in an unfortunate event. SECU offers competitive rates for this crucial protection.

Extended Warranties

While your new car comes with a manufacturer’s warranty, and some used cars have limited dealer warranties, an extended warranty (also known as a Vehicle Service Agreement) offers long-term protection against unexpected repair costs.

- SECU’s Offerings: SECU often partners with reputable providers to offer extended warranty options to its members. These plans can cover major components and systems beyond the manufacturer’s warranty period.

- Peace of Mind: Knowing that significant repairs won’t derail your budget can be incredibly reassuring. This is particularly valuable for used car loans, where out-of-warranty repairs can quickly become expensive.

Payment Protection

Life is unpredictable. Payment protection programs offered by SECU can help you cover your loan payments during difficult times.

- Coverage: These programs typically offer protection in events such as disability, involuntary unemployment, or even death, ensuring your NC Secu Car Loan payments are made when you’re unable to.

- Security: This optional add-on provides a safety net, protecting your credit and your vehicle during unforeseen circumstances.

Online Banking and Payment Management

Managing your NC Secu Car Loan is made easy through SECU’s robust online banking platform and mobile app.

- Convenience: You can view your loan balance, make payments, set up automatic payments, and access statements 24/7 from anywhere.

- Financial Control: This digital access empowers you to stay on top of your loan and manage your finances efficiently, ensuring you never miss a payment.

Common Mistakes to Avoid When Getting an NC Secu Car Loan

Even with the best intentions, borrowers can sometimes make missteps that impact their auto loan experience. Knowing these common pitfalls can help you navigate the process for your NC Secu Car Loan more effectively.

Based on my years in the industry, these are the errors I frequently see.

1. Not Checking Your Credit Score

Many individuals jump into car shopping without first reviewing their credit report and score. Your credit score is the primary determinant of your interest rate.

- The Mistake: Not knowing your score means you won’t know what rates to expect, making it harder to spot a good deal or challenge an unfavorable one.

- Pro Tip: Get your free credit report from AnnualCreditReport.com and review it for accuracy well before applying. Address any errors promptly.

2. Not Getting Pre-Approved

As discussed earlier, pre-approval is a powerful tool. Skipping this step puts you at a significant disadvantage at the dealership.

- The Mistake: Relying solely on dealership financing means you might be pushed into higher interest rates or less favorable terms. The focus shifts from the car’s price to the monthly payment, potentially obscuring the true cost.

- Pro Tip: Always secure an NC Secu Car Loan pre-approval first. This gives you a clear budget and the leverage of a "cash buyer."

3. Ignoring the Total Cost of Ownership

It’s easy to get fixated on the monthly payment, but the true cost of a car involves much more than just the loan.

- The Mistake: Overlooking expenses like insurance, maintenance, fuel, and potential repairs can lead to financial strain down the road, even if your NC Secu Car Loan payment is manageable.

- Pro Tip: Create a realistic budget that includes all potential car-related expenses before you commit to a purchase.

4. Rushing the Decision

Buying a car is a significant financial commitment. Rushing through the process can lead to buyer’s remorse and unfavorable terms.

- The Mistake: Feeling pressured by a salesperson or being too eager to get a new car can lead to hasty decisions, such as agreeing to a loan term that’s too long or accepting unnecessary add-ons.

- Pro Tip: Take your time. Research vehicles, compare NC Secu Car Loan offers, and don’t be afraid to walk away if you feel pressured or unsure.

5. Not Understanding All Loan Terms

Before signing any documents, it’s critical to fully comprehend every aspect of your NC Secu Car Loan.

- The Mistake: Many borrowers sign without understanding the APR, total interest paid, or any potential fees, which can lead to surprises later.

- Pro Tip: Ask questions! A SECU loan officer will be happy to explain everything. Make sure you understand the fine print, including any early payment clauses (though SECU typically doesn’t have prepayment penalties, it’s always good to confirm).

Pro Tips for a Successful NC Secu Car Loan Experience

To truly maximize the benefits of an NC Secu Car Loan and ensure a smooth journey from application to ownership, consider these expert recommendations.

These insights come from years of observing successful borrowers and understanding the nuances of auto financing.

- Research Thoroughly: Don’t just research the car; research your financing options. Understand current rates, compare SECU’s offerings with others (though for members, SECU is often top-tier), and know what terms you’re comfortable with. A well-informed borrower is a powerful borrower.

- Budget Wisely: Beyond just the monthly loan payment, factor in all car ownership costs: insurance, fuel, maintenance, registration, and potential repairs. Use an auto loan calculator to see how different loan amounts, interest rates, and terms affect your monthly payment and total interest.

- Communicate with SECU: If you have questions or encounter any issues during the application process or while managing your loan, reach out to SECU. Their member service is a key advantage, and they are there to help. Don’t hesitate to leverage their expertise.

- Maintain Good Credit: Your credit score isn’t just for getting the loan; it impacts everything from insurance rates to future financing. Continue to make all payments on time, keep credit utilization low, and regularly monitor your credit report. A good credit score ensures you’ll always have access to the best financial products, including future NC Secu Car Loan options.

- Consider the "Total Package": When comparing different loan offers, look beyond just the interest rate. Consider the fees, the flexibility of the terms, and the quality of customer service. With an NC Secu Car Loan, you’re often getting a superior total package due to the credit union’s member-first philosophy.

Frequently Asked Questions (FAQs) about NC Secu Car Loans

Here are some common questions prospective borrowers have about securing an NC Secu Car Loan.

Q1: Can I apply for an NC Secu Car Loan online?

Yes, absolutely! SECU offers a convenient online application portal for its car loans. You can complete the process from your computer or mobile device at your leisure.

Q2: What if I’m not a SECU member yet? Can I still apply for a car loan?

You must be a SECU member to qualify for an NC Secu Car Loan. However, you can typically apply for membership and a loan simultaneously. During the application process, SECU will guide you on how to become a member if you aren’t already.

Q3: How long does it take to get approved for an NC Secu Car Loan?

Approval times can vary. For pre-approvals, it can often be quite quick, sometimes within the same day or a couple of business days, especially if all your documentation is in order. Full loan approval once you’ve selected a vehicle also aims to be efficient.

Q4: Is there a minimum credit score required for an NC Secu Car Loan?

While SECU doesn’t publicly state a strict minimum credit score, a higher score will always yield better interest rates and a higher likelihood of approval. They consider your overall financial picture, not just a single number. If your credit isn’t perfect, speak with a loan officer; they may have options or advice for improving your chances.

Q5: Can I get a car loan for a private party sale through SECU?

Yes, SECU absolutely offers financing for private party car sales. They will guide you through the process, which typically involves verifying the vehicle’s title and value.

Conclusion: Your Road to a Great NC Secu Car Loan Starts Here

Securing an NC Secu Car Loan offers a powerful combination of competitive rates, flexible terms, and unparalleled member service. As a pillar of financial stability for North Carolina’s state and public school employees and their families, SECU consistently prioritizes the financial well-being of its community.

By understanding the membership requirements, preparing for the application process, and making informed decisions about rates and terms, you can confidently navigate your journey to vehicle ownership. Remember the value of pre-approval, the importance of knowing your credit score, and the benefit of SECU’s dedicated support.

Don’t let the car buying process be daunting. With an NC Secu Car Loan, you’re not just getting financing; you’re gaining a trusted partner committed to helping you drive your dreams. Visit the official SECU website at https://www.ncsecu.org/ to explore their current loan offerings and begin your application today.